Endoscopy Equipment Market Size by Product, Application, Hygiene, End-User, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

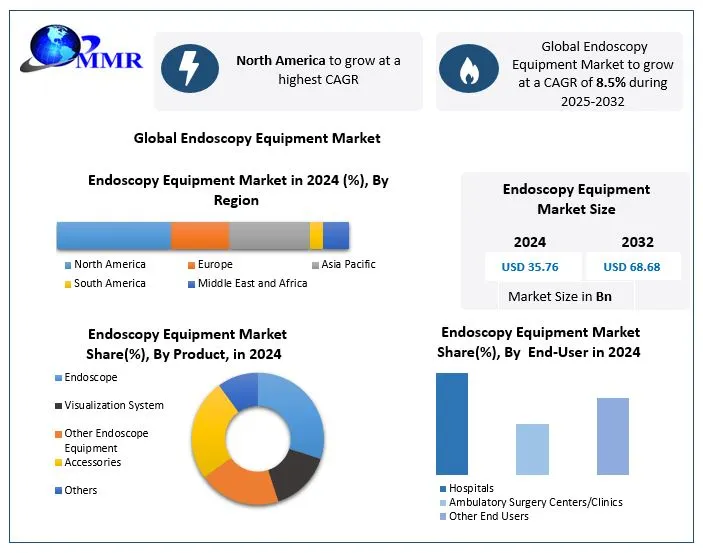

Global Endoscopy Equipment Market size was valued at USD 35.76 Bn in 2024, and the Global Endoscopy Equipment revenue is expected to grow by 8.5 % from 2025 to 2032, reaching nearly USD 68.68 Bn

Endoscopy Equipment Market Overview:

Surgical and endoscopy equipment refers to the medical instruments that help with visualization and procedural work inside the body, with or without being introduced through small incisions. It encompasses tools like endoscopes, cameras, light sources, and surgical accessories for minimally invasive diagnosis and treatment. This demand for minimally invasive diagnosis and treatment procedures is essentially propelling growth in the endoscopy equipment market. Growing applications in cancer screening and GI-related disorders serve as an adjuvant for adoption, while new avenues are coming into the picture for the endoscopy equipment market through healthcare innovations like AI-assisted imaging and robotic endoscopy. Apart from that, all of these advancements essentially contribute to improving the accuracy and efficiency of procedures as well as the outcomes, from the patient's perspective. North America accounted for the world's Endoscopy Equipment Market in 2024 due to its high incidences of chronic diseases and strong healthcare infrastructure in 2024. Leading clinical companies such as KARL STORZ SE & Co. KG and Stryker Corporation have maintained their presence in the region through the introduction of advanced products and strategic expansions. Some of the driving forces behind the global demand for advanced endoscopic surgical procedures are technological developments and a rise in incidences of chronic ailments. With increased investments being made in the healthcare sector in these emerging markets, access is growing, thereby fostering market growth. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Endoscopy Equipment Market Dynamics:

High demand for Endoscopy therapy and diagnosis to drive the Endoscopy Equipment Market

Robotic-assisted flexible endoscopy aims to increase patient exam tolerance by allowing the physician to adjust the flexible endoscope within a set distance, lowering the possibility of infection. According to an article "Technology Can Make Endoscopy Safer," a mix of new technology, like as robots and computer vision, can help improve the status of colorectal cancer, the world's third most prevalent malignancy. The robotic flexible endoscopic system is employed for endoscopic applications like bronchoscopy, pancreatic endoscopy, and gastroscopy in unstructured conditions, as these diseases require urgent treatment during the COVID pandemic. As a result of the aforementioned reasons, the examined market had a significant influence on the studied market. The growing desire for less invasive procedures increased acceptance of endoscopes for treatment and diagnostics, and technical improvements leading to better applications are the primary drivers driving the market's growth.

Because minimally invasive procedures (MIS) generate less post-operative discomfort, patients are given lower doses of pain relievers. Because there are few incisions or stitches, the hospital stay is usually brief, and patients do not need to return frequently. People are increasingly interested in minimally invasive procedures rather than typical open operations, which include large incisions made into the muscles, and these muscles take a long time to recuperate. Minimally invasive surgery (MIS) uses tiny incisions, resulting in faster recovery. Additionally, the scars left by minimally invasive operations (MIS) are scarcely visible. The fundamental benefit of minimally invasive surgeries (MIS) over traditional open operations is the increased accuracy provided by video-assisted technology, which produces a better and enlarged view of the organs or body parts being operated on. Because of the reduced recovery period, these operations are becoming more popular among the older population.

Endoscopy systems are often employed in minimally invasive operations to determine the origin of certain disorders and symptoms, according to the study "Anatomic Study of Endoscopic Transnasal Approach to Petrous Apex’’ Endoscopic-aided technology has traditionally been used to expose much of the region that is difficult to examine with a microscope. Through the natural human foramen, endoscopy varies the angle and sees the surrounding anatomical structure. It gives the surgeon an unobstructed viewing field and an operating channel without retraction, considerably improving surgical quality. As a result, surgeons favour flexible endoscopic devices. As a result of the aforementioned factors, the worldwide endoscopy devices market is expected to increase significantly during the forecast period.

Endoscopy is becoming increasingly important for diagnosis to drive the Endoscopy Equipment Market

Endoscopy operations are minimally invasive surgeries that use small tubes, tiny cameras, and surgical equipment to be performed through one or more small incisions. Endoscopy treatments provide several advantages, including reduced discomfort, a shorter or no hospital stay, and fewer issues connected to pre-and post-surgery care. Owing to these operations are less expensive, more successful, and safer than traditional open surgeries. Additionally, these treatments are covered by health insurance carriers in wealthy nations such as the United States, Canada, the United Kingdom, Germany, Australia, and a few Middle Eastern countries such as the United Arab Emirates. These reasons contribute to patients' and physicians' strong preference for endoscopic treatments. The United States performs roughly 11.2 million colonoscopies, 6.5 million upper endoscopies, 313,050 flexible sigmoidoscopies, 178,405 upper endoscopic ultrasonography tests, and 169,500 endoscopic retrograde cholangiopancreatography operations each year.

Endoscopy is rapidly being utilized to diagnose and treat a variety of significant diseases, including cancer, orthopedic issues, neurological disorders, and gastric reflux disease (GERD). According to GLOBOCAN, 457 960 new cancer cases were identified in the UK , with this figure expected to rise to 27.5 million by 2040 (a 61.7% increase). As a result, the frequency of cancer procedures will skyrocket; for example, around 80.2% of cancer patients are expected to necessitate surgery. Owing to the increased prevalence of target illnesses such as cancer, neurodegenerative, infectious, immunological, metabolic, and cardiovascular diseases is expected to increase the need for endoscopic operations, propelling the endoscopy equipment market growth in the forecast years.

Healthcare sector innovations to create the opportunity for the Endoscopy Equipment Market

Brazil, Russia, India, China, and South Africa (BRICS) have some of the world's fastest-growing economies. According to the World Economic Forum, developing nations will account for around one-third of global healthcare spending in 2025. Because India and China have more than half of the world's population, these countries have the biggest number of patients. The rising cancer burden, quick improvements in healthcare infrastructure, the rapid growth of medical tourism, and the availability of flexible legislation in these nations all drive endoscopic equipment manufacturers to extend their presence in emerging markets.

Several endoscopic equipment manufacturers are now establishing operations in the Asia Pacific, the Middle East, and Latin America. Stryker and KARL STORZ have previously established production and R&D centers in these nations. Furthermore, market saturation in established countries such as North America and Europe will force endoscopic equipment producers to concentrate their efforts in emerging markets in the future years.

Shortage of skilled physicians and endoscopists to restrain the Endoscopy Equipment Market

Endoscopy physicians and surgeons are limited across the world. This lack of skilled endoscopy experts is expected to be felt throughout the Asia Pacific, Latin America, and Europe as well (excluding the UK, where training has been provided for nurse endoscopists for the last 10 years by the United Kingdom Central Council for Nursing, Midwifery, and Health).

Endoscopic operations must be performed by trained specialists in order to minimise the spread of infections in endoscopy facilities. The global lack of competent endoscopy physicians and nurses is expected to have a detrimental influence on the number of endoscopic operations performed each year. To address this worry, a few industry participants, such as Olympus, have developed training facilities. The organisation has 22 endoscopic training locations in Asia alone. These programs will raise awareness of the most recent technical advances in the area of endoscopy while also increasing the number of qualified endoscopy experts.

Endoscopy Equipment Market Segment Analysis:

Based on Product, the Endoscopy Equipment Market is segmented into Endoscope, Visualization System, Other Endoscope Equipment and Accessories in this Endoscope dominated the market in in 2024 and is expected to dominate in forecast period as the Widespread use during endoscopy procedures and increasing application for the visualization and diagnosis of complex disease conditions such as cancer, GI disorders, urinary disorders, and lung disorders, endoscopy visualization systems accounted for the largest revenue share of 40.5% in 2024. Additionally, the emergence of next-generation endoscopic visualisation technologies, which allow surgeons to see the internal organ of choice with minimally invasive treatment, is increasing their use and indicating a bigger sector share.

Furthermore, throughout the projection period, the endoscopes sector accounted for a CAGR of 9.4% in the market for endoscopic equipment. This rapid expansion can be ascribed to the rising number of endoscopic operations, as well as the widespread use of endoscopes to perform surgeries and biopsies for improved diagnosis and treatment. Due to its high preference for usage by medical professionals and advantages such as safety, better efficiency, and superior ergonomics as compared to rigid endoscopes, the flexible endoscopes segment led the endoscopes segment.

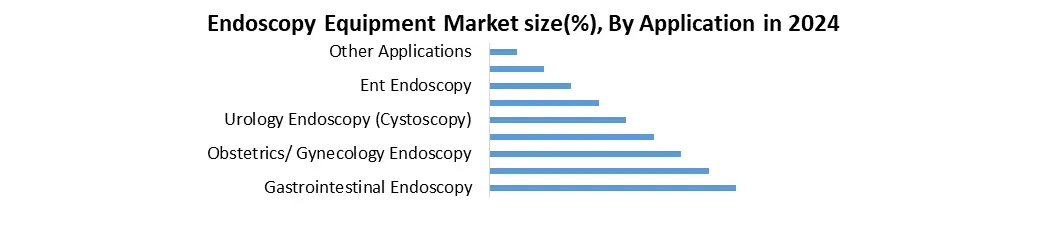

Based on the Application, the Endoscopy Equipment Market is segmented into Gastrointestinal Endoscopy, Laparoscopy, Obstetrics/Gynaecology Endoscopy, Arthroscopy, Urology Endoscopy (Cystoscopy), Bronchoscopy, Ent Endoscopy, Mediastinoscopy and Other Applications. In this Gastrointestinal (GI) endoscopy dominated the market in in 2024 and is expected to dominate in the forecast period. The Gastrointestinal (GI) endoscopy segment led the endoscopic device market in 2024, accounting for 60.7% of sales. The increased prevalence of gastrointestinal illnesses in the young, adult, and elderly populations globally is one of the primary factors driving the growth of the gastroenterology segment. gastrointestinal issues include dyspepsia, irritable bowel syndrome, and constipation. In addition, gastroesophageal reflux disease is a common type of organic gastrointestinal problem. The growing prevalence of gastrointestinal illnesses, along with an ageing population, is boosting the need for gastrointestinal endoscopy. Gastrointestinal tumours are the world's second leading cause of cancer-related fatalities. Endoscopy has been shown to be the gold standard for detecting gastrointestinal malignancies.

Owing to the surge in endoscopic treatments for early detection of gastrointestinal malignancies is likely to drive the market in the forecast period. The vast majority of gastrointestinal stromal tumors begin in the rectum, colon, or esophagus. The majority of persons diagnosed with a gastrointestinal stromal tumors are over the age of 50. The market is driven by the increasing prevalence of malignant cancers. According to the American Cancer Society (ACS), there will be 106,185 new cases of colon cancer and 44,890 new cases of rectal cancer in the United States.

According to the American Cancer Society, the lifetime chance of having colorectal cancer is around one in 23 (4.3%) for men and one in 25 (4.0%) for women. According to the World Health Organisation (WHO), there will be around 1.93 million occurrences of colon and rectum cancer in 2025. Furthermore, increasing product approval in the sector will add to market expansion. For example, Ambu received 510(k) regulatory approval from the United States Food and Drug Administration for the Ambu a scope Gastro and Ambu aBox 2. Ambu's first sterile single-use gastroscope, the scope Gastro, incorporates new superior imaging and design characteristics in a combined solution with next-generation display and processing technologies. As a result of the aforementioned factors, the category is predicted to increase significantly during the forecast period.

Based on the End User, the Endoscopy Equipment Market is segmented into Hospitals, Ambulatory Surgery Centres/Clinics and Other End Users. In this, Hospitals dominated the market in 2024 and is expected to dominate the market in the forecast period. In 2024, the hospital sector led the market for endoscopic equipment, accounting for 55.1% of total sales. Hospitals are widely regarded as primary healthcare systems, and the patient population's preference for hospitals for the diagnosis and treatment of chronic illnesses is also supporting sector expansion. Moreover, a significant number of hospital surgeries, including endoscopic procedures, enhance endoscopy equipment usage, consequently promoting sector growth.

Additionally, the ambulatory surgery centres/clinics category is expected to grow at the fastest rate throughout the projection period. Growing demand for minimally invasive treatments to minimise total costs and the number of days spent in the hospital are some of the primary reasons projected to drive market growth. Moreover, shorter recovery time and reduced discomfort due to the usage of less invasive keyhole endoscopic procedures hasten the use of endoscopy equipment in ambulatory surgical centres/clinics, which is expected to boost sector growth during the forecast period.

Endoscopy Equipment Market Regional Insights:

North America region dominated the Endoscopy Equipment Market in 2024 due to the growing incidence of chronic diseases

North America had the biggest revenue share of 48.0% in the market for endoscopic devices market in 2024. The growing incidence of chronic diseases such as cancer, as well as an ageing population, are likely to drive the endoscopy devices market in North America during the forecast period, as are technical breakthroughs and new product releases.

Colorectal cancer is the third greatest cause of cancer-related deaths in men and women, and the second highest cause of cancer deaths in the combined population in the United States, according to the American Cancer Society. It is anticipated that the country would have 106,180 new instances of colon cancer and 44,850 new cases of rectal cancer in the upcoming years, resulting in 52,580 fatalities. As a result of the rising prevalence of colorectal cancer, the market for endoscopic equipment will be driven by its detection and treatment.

Endoscopy Equipment Market Competitive Landscape

In the Endoscopy Equipment Market, the top companies like Stryker Corporation, KARL STORZ SE & Co. KG, Olympus Corporation, Karl Storz Endoscopy, and Intral S/A hold the largest share in the market, whereas Stryker Corporation and KARL STORZ SE & Co. KG are important manufacturers of endoscopic instruments, and they present a vast array of advanced solutions. Stryker has a unique offering: innovative endoscopic systems accompanied by HD visualisation platforms (such as the 1688 AIM 4K platform), laparoscopes, arthroscopes, insufflators, and surgical navigation technologies for mainly minimally invasive surgeries in orthopaedics, general surgery, and urology. KARL STORZ, as an endoscopic innovator, gives a complete product line comprising flexible endoscopes and camera systems, integrated OR solutions, and modern imaging technologies such as IMAGE1 S™ and 3D systems. Their scope covers endoscopy for ENT, gastroenterology, gynaecology, and neurology, focusing heavily on precision optics and digital integration. Both companies work on the edge of technology to improve surgical efficiency and visualisation as a platform for global operations.

Endoscopy Equipment Market Key Trends

• Technological Advancements: Integration of AI, robotics, 4K/8K imaging, and 3D visualisation systems is enhancing diagnostic precision and minimally invasive capabilities.

• Growing Healthcare Investments in Emerging Markets: Countries in Asia-Pacific, Latin America, and the Middle East are increasing healthcare expenditure, driving endoscopy infrastructure development.

• Ageing Population and Chronic Diseases: Rising global geriatric population and prevalence of cancer, gastrointestinal, and respiratory disorders are significantly boosting the market.

Endoscopy Equipment Market Key Developments

| Year | Company Name | Recent Development |

| August 11, 2023 | Stryker Corporation (Kalamazoo, Michigan, USA) | Launched the 4K 1788 Camera Platform, enhancing visualisation across specialities like urology and ENT. |

| January 8, 2025 | KARL STORZ SE & Co. KG (Tuttlingen, Germany) | Announced acquisition of T1V, a digital collaboration platform provider for OR environments. |

| January 12, 2024 | Olympus Corporation (Tokyo, Japan) | Entered strategic collaboration with Canon Medical Systems to co-develop endoscopic ultrasound (EUS) systems. |

| May 14, 2024 | Al Faisaliah Medical Systems (Saudi Arabia) | Received SAR 23.8 million in purchase orders via NUPCO for medical devices under Tender NPT0028/22 |

| December 24.2024 | Bioméc LTDA – (Brazil) | A major shift toward single-use devices to address infection risks, with growth rates of 12.5% annually |

Endoscopy Equipment Market Scope: Inquire before buying

| Endoscopy Equipment Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 35.76 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 8.5 % | Market Size in 2032: | USD 68.68 Bn. |

| Segments Covered: | by Product | Endoscope Visualization System Other Endoscope Equipment Accessories |

|

| by Application | Gastrointestinal Endoscopy Laparoscopy Obstetrics/Gynaecology Endoscopy Arthroscopy Urology Endoscopy (Cystoscopy) Bronchoscopy Ent Endoscopy Mediastinoscopy Other Applications |

||

| by Hygiene | Single-use Reprocessing Sterilization |

||

| by End-User | Hospitals Ambulatory Surgery Centres/Clinics Other End Users |

||

Endoscopy Equipment Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Taiwan, Indonesia, Philippines, Malaysia, Vietnam, Thailand, Rest of Asia Pacific region)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Endoscopy Equipment Market Key Players

North America

1. Stryker Corporation (Kalamazoo, Michigan, USA)

2. Boston Scientific Corporation (Marlborough, Massachusetts, USA)

3. JOHNSON & JOHNSON (New Brunswick, New Jersey, USA)

4. Medtronic Inc. (Minneapolis, Minnesota, USA)

5. ConMed Corporation (Utica, New York, USA)

6. Intuitive Surgical, Inc. (Sunnyvale, California, USA)

7. Cook Medical (Bloomington, Indiana, USA)

8. CapsoVision, Inc. (Saratoga, California, USA)

9. The Cooper Companies, Inc. (San Ramon, California, USA)

10. Laborie Medical Technologies Inc. (Burlington, Ontario, Canada)

11. Teleflex Incorporated (Wayne, Pennsylvania, USA)

12. Cantel Medical Corp. (Little Falls, New Jersey, USA)

13. Arthrex, Inc. (Naples, Florida, USA)

Europe

14. KARL STORZ SE & Co. KG (Tuttlingen, Germany)

15. Smith & Nephew Plc (London, United Kingdom)

16. Richard Wolf GmbH (Knittlingen, Germany)

17. Ambu A/S (Ballerup, Denmark)

18. Fortimedix Surgical B.V. (Geleen, Netherlands)

19. B. Braun Melsungen AG (Melsungen, Germany)

20. Medi-Globe (Achenmühle, Germany)

21. Dantschke Medizintechnik (Dresden, Germany)

22. Carl Zeiss AG (Oberkochen, Germany)

Asia Pacific

23. Olympus Corporation (Tokyo, Japan)

24. Fujifilm Holdings Corporation (Tokyo, Japan)

25. Hoya Corporation (Tokyo, Japan)

26. Nipro Corporation (Osaka, Japan)

Middle East and Africa

27. MIS (Medical Innovations & Systems) (South Africa)

28. Al Faisaliah Medical Systems (Saudi Arabia)

South America

29. Intral S/A (Brazil)

30. Bioméc LTDA(Brazil)

Frequently Asked Questions:

1] What segments are covered in the Global Endoscopy Equipment Market report?

Ans. The segments covered in the Endoscopy Equipment Market report are based on Product, Application, End User, Hygiene and Region.

2] Which region is expected to hold the highest share in the Global Endoscopy Equipment Market?

Ans. The North America region is expected to hold the highest share in the Endoscopy Equipment Market.

3] What is the market size of the Global Endoscopy Equipment Market by 2032?

Ans. The market size of the Endoscopy Equipment Market by 2032 is expected to reach USD 68.68 Bn.

4] What is the forecast period for the Global Endoscopy Equipment Market?

Ans. The forecast period for the Endoscopy Equipment Market is 2025-2032.

5] What was the market size of the Global Endoscopy Equipment Market in 2024?

Ans. The market size of the Endoscopy Equipment Market in 2024 was valued at USD 35.76 Bn.