Electric Bus Market Size by Propulsion Type, Component, Range, Battery Capacity, Application, Battery Type, Level of Autonomy, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2034

Overview

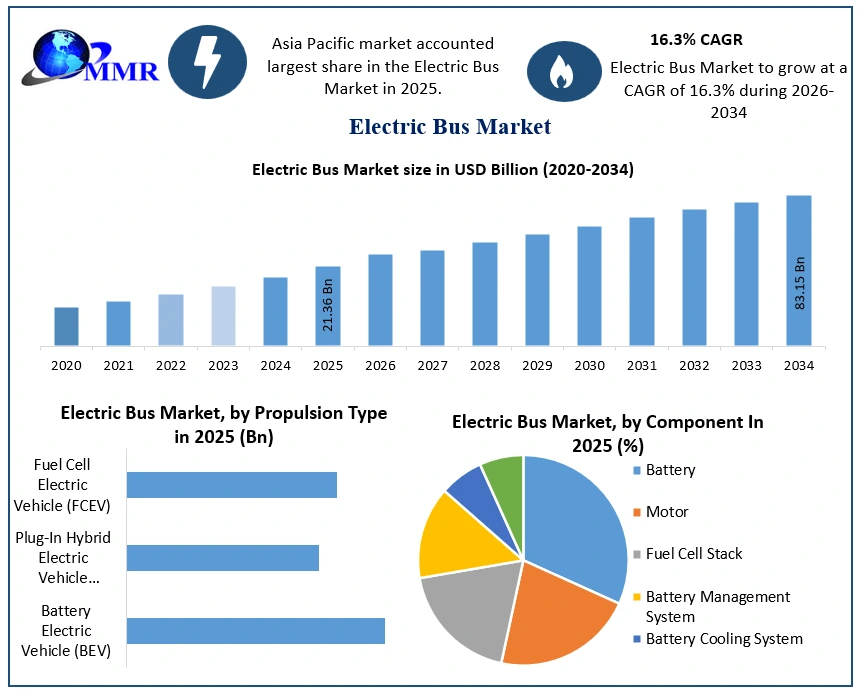

The Electric Bus Market size was valued at USD 21.36 Billion in 2025 and the total Electric Bus revenue is expected to grow at a CAGR of 16.3% from 2026 to 2034, reaching nearly USD 83.15 Billion.

An electric bus is one that is propelled by electric motors rather than an internal combustion engine. Electric buses can either store the required power on board or be fed constantly from an external source. Although there are examples of different storage types, such as the gyrobus, which employs flywheel energy storage, the bulk of buses storing electricity is battery electric buses (which this page largely deals with), where the electric motor derives energy from an on-board battery pack. When no electricity is stored on board, it is obtained by interaction with external power sources. For example, overhead cables used in trolleybuses, a ground-level power source, or inductive charging. The three key causes driving the gradual transition from hydrocarbon-based to electric public transportation are rising pollution levels, possible operating cost reductions, and high reliance on public transportation.

Electric Bus Market Growth Outlook

To know about the Research Methodology :- Request Free Sample Report

The total number of electric buses in the globe is predicted to expand by 35-60% from 14 Million in 2025 to around 33 Million in 2030, with China accounting for 98% of the total. Electric bus usage in metropolitan public transportation fleets is increasing across the world. It began in China, and it has taken several years for other regions to catch up.

However, Europe is currently growing, with electric bus registrations increasing by 48% in 2021 compared to 2020. Last year, 3,282 e-buses were delivered, increasing the total number of vehicles registered on the continent to over 8,500 since 2012. In 2020, six European nations registered a number of zero-emission buses (battery-electric + fuel cell buses), accounting for more than 25% of Class I registrations. For the first time, three European nations registered more than 500 e-buses in 2021, with Germany leading the way (555 units), followed by the United Kingdom (540), and France (540). (512).

Research Methodology

The research report highly depends on both primary and secondary data sources. The research process involves the investigation of various factors affecting the industry, such as government policy, market environment, competitive landscape, historical data, current market trends, technological innovation, upcoming technologies, and technical progress in related industries, as well as market risks, opportunities, market barriers, and challenges. All conceivable elements influencing the markets included in this research study have been considered, examined in depth, validated through primary research, and evaluated to provide the final quantitative and qualitative data. The market size for top-level markets and sub-segments is normalised, and the impact of inflation, economic downturns, regulatory & policy changes, and other variables is factored into the market forecast.

This data is combined and added with detailed inputs and analysis, and presented in the report. Extensive primary research was conducted to acquire information and verify and confirm the crucial numbers arrived at after comprehensive market engineering and calculations for market statistics; market size estimations; market forecasts; market breakdown; and data triangulation. Bottom-up technique is widely employed in the whole market engineering process, along with multiple data triangulation methodologies, to perform market estimation and forecasting for the overall market segments and sub-segments covered in this research.

Electric Bus Market Dynamics

Increasing need for zero-emission and energy-efficient mass transportation solutions: The transportation industry is a major contributor to global greenhouse gas (GHG) emissions. According to the United Nations Environment Program (UNEP), the transportation sector accounts for around one-quarter of all energy-related greenhouse gas (GHG) emissions and is a major source of urban and regional air pollution. According to the US Environmental Protection Agency (EPA), buses produced 1.1% of total GHG emissions from the transportation sector in 2019. Vehicle emissions are solely responsible for emitting 29% of ozone-depleting chemicals, which cause air pollution and are hazardous to the environment.

Various governments during the world have launched programmes to make urban public transportation more sustainable and fuel-efficient through the use of electric buses. The Netherlands has a Green Deal for Electric Transport 2016-2020. The green deal's main goal is to eliminate automobile emissions by 2025, which would enhance the electric bus business. In addition, the US Department of Transportation's Federal Transit Administration (FTA) has committed USD 130 million in support for Low or No Emission vehicles in June 2020. Electric buses will revolutionise public transit in the future years by improving air quality, lowering noise levels, and increasing fuel efficiency.

Government support for public transportation electrification:

To push the commitment to decrease greenhouse gas (GHG) emissions and improve air quality in cities, governments during the world have provided lucrative monetary incentives to encourage shared mobility and clean transportation. Governments all around the world have created enticing efforts and programmes to encourage the usage of electric buses. Developed-country governments have launched the bidding process to promote the usage of electric buses in their cities. In London, for example, there were 3,846+ hybrid buses, 580+ electric buses, and 20 hydrogen buses operational as of March 2024, out of a total bus fleet of 9,123+, with intentions to boost this figure to 9,500+ electric buses by 2037.

A move to sustainable energy for public transportation has several benefits. The introduction of e-buses will contribute to local emission reduction commitments. The benefits would be considerably larger if power generation in densely populated nations like China and India is also greened. The government of India's National Electric Mobility Mission Plan (NEMMP) 2020 focuses on boosting the manufacture and uptake of EVs in the country.

Battery capacity: Current electric bus batteries have modest capacities, long charging times, and a restricted range per charge. The performance and service life of the batteries have a direct impact on the performance and cost of electric buses. Lead-acid, nickel cadmium, nickel metal hydride, lithium-ion, and supercapacitors are now utilised to power electric buses. Because lithium-ion batteries have a longer battery life, they are increasingly replacing lead-acid, nickel cadmium, and nickel metal hydride batteries in electric buses. However, the capacity of lithium-ion batteries is insufficient to power commercial vehicles such as electric buses, as heavier loads need more power to provide maximum torque. The charging-discharging performance of batteries decreases dramatically in cold temperatures, making it harder for the batteries to give maximum power.

The time necessary to charge an electric bus with the existing market equipment is quite long, resulting in time waste. With a 7 kW charging station, it takes more than 4 hours to charge an electric car from 0% to 100%. Furthermore, the majority of the charging infrastructure is outfitted with low-capacity chargers. These issues must be addressed in order for the electric bus industry to expand.

High development costs: A key constraint for electric bus manufacturers is the high cost of developing electric buses and coaches, as well as related components such as batteries and monitoring systems (battery management systems, CAN bus modules). The cost of developing infrastructure for EVs is also quite significant. Global infrastructure construction will require around USD 2.8 trillion. An EV's battery requires regular and rapid charging via extra equipment such as electric chargers, which are only available at EV charging stations. High-capacity charging stations must be installed in many places. The cost of the battery, charger, and charger installation adds to the cost of electric buses and coaches, making them more expensive than regular ICE buses and coaches.

Electric Bus Market Segment Analysis:

Based on propulsion type, the market is segmented into fuel cell electric vehicles, plug-in hybrid electric vehicles, and battery electric vehicles. In 2025, the battery-electric cars sector had 91.4% of the market. The high-capacity battery sets onboard battery-electric buses store electricity. These buses are designed to take advantage of the benefits of those batteries in order to power the electrical motor and all onboard electronics. The fuel cell electric vehicle category is also expected to increase exponentially during the forecast period since hydrogen fuel cell buses run longer and have faster refilling capabilities than standard e-buses. During the forecast period, the plug-in hybrid electric car category is expected to increase steadily. These buses may charge the battery by both hooking into an external power supply and regenerative braking.

Based on range, the market is segmented into less than 200 miles and more than 200 miles. Due to reduced total operating cost (TCO)/km and less recharging time, the segment of less than 200 miles accounted for the biggest proportion of the market. The segment of more than 200 miles is expected to grow at a faster rate during the forecast period. Reduced battery costs, as well as improvements in energy consumption and mileage of new e-buses, will support the expansion of this market.

Based on battery capacity, the market is segmented into up to 400 kWh and above 400 kWh. In 2025, the category of up to 400 kWh had the biggest market share. Buses with battery capacities of up to 400 kWh are significantly less expensive, lighter, and more efficient since they can be quickly fast-charged at regular intervals. These factors are to blame for this segment's dominance. Because of the capacity to travel greater distances on a single charge, the over 400 kWh sector is predicted to increase steadily in the market.

Electric Bus Market Regional Insights:

During the forecast period, the Asia Pacific region is expected to lead the global electric bus market. The Asia Pacific electric bus market is being pushed by the need to reduce urban pollution and reliance on fossil fuels, as well as expanding national government initiatives toward sustainable public transportation. China leads the regional and global markets since it has the largest market in terms of volume. The Chinese government has made significant investments in converting the traditional public transportation fleet to electric. For the usage of these types of buses, the Chinese government has created public transit zones. The government's initiatives have increased the usage of battery-powered buses in the region. Chinese firms such as BYD, Yutong, Ankai, and Zhongtong dominate both the Chinese and global markets. Due to the availability of cheaper parts and components, these players have been able to design and deliver a wide range of electric bus models at reduced pricing. As a result, the country leads the Asia Pacific Electric Bus market, beating both European and American competitors.

For example, BYD secured its first order from TMB (Transportes Metropolitanos de Barcelona) in November 2021 for 25 new-generation 40-foot BYD electric buses, which are planned to be delivered between 2022 and 2024. This directive is part of a plan to phase out polluting diesel buses in Barcelona by 2025. Furthermore, the rapidly expanding charging infrastructure in this region bodes well for the regional market. Japan and South Korea are also contributing to the region's brisk sales of these types of buses. Because of the high adoption rate of electric buses in China, Asia Pacific dominates the industry. Other Asian countries have begun to include electric buses into their public transportation networks.

During the forecast period, North America is likely to have considerable expansion in the global market. Long-term expansion in the North American electric bus industry is ascribed to growing worries about the depletion of fossil fuels and rising levels of environmental pollution. To address the aforementioned difficulties, governments in the region, such as Canada, have launched reforms in public transportation systems, such as promising to electrify their whole electric bus fleet in regions such as Montreal and British Columbia. With expanded governmental measures such as tariff waiver programmes for electric bus operators, the United States has led the region's electric bus sector.

Furthermore, the market for electric buses in the United States has grown tremendously in recent years as a result of new federal policies to reduce carbon emissions from buses. President Biden and the Federal Transit Administration (FTA) granted USD 409.3 million to 70 projects in 39 states in 2022 to upgrade and electrify America's buses. Across addition to the foregoing, the Mexican government's attempts to boost the percentage of power generated by diverse clean sources to 35% by 2024, 40% by 2035, and 50% by 2050 are driving demand for electric buses in the rest of North America. Furthermore, increased awareness about the consequences of toxic gases emitted by traditional IC engine vehicles is expected to boost sales of electric buses in the region.

Report Scope:

The Electric Bus Market research report includes product categorization, product application, development trend, product technology, competitive landscape, industrial chain structure, industry overview, national policy and planning analysis of the industry, and the most recent dynamic analysis, among other things. The study discusses the global market's drivers, opportunities, and limitations. It discusses the influence of various drivers, trends, and constraints on market demand during the forecast period. The research also outlines market potential on a global scale. The research includes the production time, base distribution, technical characteristics, research and development trends, technology sources, and raw material sources of significant Electric Bus Market firms in terms of production bases and technologies. The more precise research also contains the key application areas of market and consumption, significant regions and consumption, major producers, distributors, raw material suppliers, equipment providers, and their contact information, as well as an analysis of the industry chain relationship. This report's study also contains product specifications, manufacturing processes, cost structure, and data information organised by area, technology, and application.

Electric Bus Industry Ecosystem

Electric Bus Market Scope: Inquire before buying

| Electric Bus Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 21.36 Billion |

| Forecast Period 2026 to 2034 CAGR: | 16.3 % | Market Size in 2034: | USD 83.15 Billion |

| Segments Covered: | by Propulsion Type | Battery Electric Vehicle (BEV) Plug-In Hybrid Electric Vehicle (PHEV) Fuel Cell Electric Vehicle (FCEV) |

|

| by Component | Battery Motor Fuel Cell Stack Battery Management System Battery Cooling System EV Connector |

||

| by Range | Up to 200 miles Above 200 miles |

||

| byPower Output | Up to 250 kW Above 250 kW |

||

| by Battery Capacity | Up to 400 kWh Above 400 kWh |

||

| by Application | Intracity Intercity |

||

| by Battery Type | Lithium-nickel-manganese-cobalt oxide Lithium-iron-phosphate Others |

||

| by Level of Autonomy | Semi-autonomous Autonomous |

||

Electric Bus Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Electric Bus Market, Key Players

1. BYD Company Ltd.

2. Yutong

3. New Flyer Industries Inc.

4. Proterra Inc.

5. Solaris Bus & Coach SA

6. Zhongtong Bus Holding Co., Ltd.

7. Shenzhen Wuzhoulong Motors Co., Ltd.

8. EBUSCO BV.

9. Dongfeng Automobile Co., Ltd

10. Alexander Dennis

11. King Long

12. FAW Group

13. AB Volvo

14. Daimler AG

15. TATA Motors

16. Ashok Leyland

17. Nova Bus

18. Foton Motor Inc.

19. Ashok Leyland Electric Bus.

20. JBM Solaris ECOLIFE.

21. Electric Bus K9.

22. SKYPAK XL Bus.

Frequently Asked Questions:

1] What segments are covered in the Global Electric Bus Market report?

Ans. The segments covered in the Electric Bus Market report are based on Propulsion Type, Component, Range, Power Output, Battery Capacity, Application, Battery Type, and Level of Autonomy.

2] Which region is expected to hold the highest share in the Global Electric Bus Market?

Ans. The Asia Pacific region is expected to hold the highest share in the Electric Bus Market.

3] What is the market size of the Global Electric Bus Market by 2034?

Ans. The market size of the Electric Bus Market by 2034 is expected to reach USD 83.15 Billion.

4] What is the forecast period for the Global Electric Bus Market?

Ans. The forecast period for the Electric Bus Market is 2026-2034.

5] What was the Global Electric Bus Market size in 2025?

Ans: The Global Electric Bus Market size was USD 21.36 Billion in 2025.