Elastomers Market Size by Type, Process, Application and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

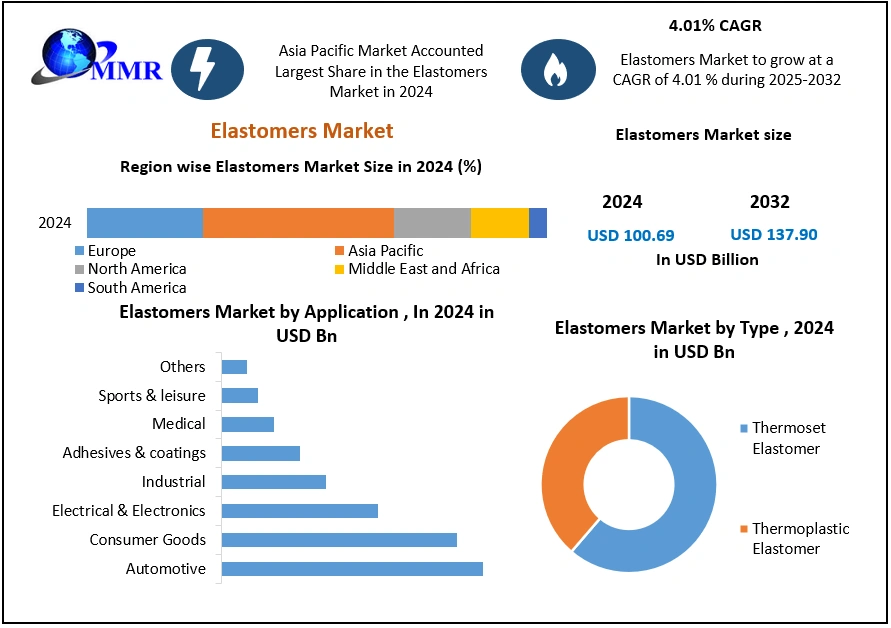

The Elastomers Market size was valued at USD 100.69 Billion in 2024 and the total revenue is expected to grow at a CAGR of 4.01 % from 2025 to 2032, reaching nearly USD 137.90 Billion.

The MMR report provides a data-driven, and multi-dimensional analysis of the global Elastomers Market, covering all critical operational, technological, commercial, and regulatory aspects shaping industry growth. It evaluates manufacturing & production capabilities, including the global distribution of facilities, capacity utilization, energy-efficiency benchmarks, automation, and Industry 4.0 impacts. The report examines end-use demand patterns across automotive, medical, electronics, construction, and industrial applications, supported by detailed insights into regional pricing dynamics, cost drivers, tariff impacts, and substitution trends. It further explores technology innovation pathways, such as breakthroughs in thermoplastic elastomer chemistry, advanced curing, nanocomposites, and smart functional materials. Extensive coverage of trade flows, logistics constraints, supply chain vulnerabilities, and value chain economics enhances strategic clarity. the report analyzes R&D pipelines, investment feasibility, market attractiveness, financial risk, and backward/forward integration options. Sustainability is addressed through carbon footprint assessments, recycling technologies, bio-based elastomer development, and evolving global regulatory standards. these insights empower stakeholders to make informed, future-ready decisions.

Elastomers Market Overview:

Polymers with elastic properties are known as elastomers. They are indefinitely structured cross-linked polymers with weak intermolecular forces. Their tensile strength is strong, while their electrical conductivity is poor. Elastomers are divided into two types: thermoset and thermoplastic. Thermoplastic elastomers have both rubber and elastic properties. This sort of elastomer is simple to work with. The key advantages of thermoplastic are its chemical resistance and recyclability. In the meantime, when thermoset polymers are treated, cross-linking linkages are formed. Elastomer linkages are irreversible, and deformation is difficult to achieve. Elastomers have strong heat resistance and are considered to be cost-effective and attractive materials.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Elastomers Market Dynamics:

Automobiles, medicines, electrical and electronics, building and construction, and other expanding industries are all seeing rising demand for elastomers. In the automotive industry, the elastomer is used to replace PVC and other materials, improving fuel efficiency and performance. In the construction sector, elastomers are in high demand for purposes such as sealing and electrical insulation. The use of elastomers is also increasing as the global demand for medical products rises. They are also utilized in the manufacture of gloves, gaskets, and molding products due to their toughness and flexibility.

On the other hand, market growth is constrained by its negative impact on the environment. Stringent regulatory laws for manufacturers are another issue that limits growth. The fluctuating price of elastomers is also a key source of concern for manufacturers. One of the major opportunities for the elastomer market is market growth and demand in sports accessories and vehicle manufacturing.

Elastomers Market Challenges:

The price of crude oil fluctuates, creating price changes in synthetic rubber.

Because synthetic rubber is made from crude oil, crude oil and synthetic rubber prices have changed in lockstep. However, natural rubber is an alternative to synthetic rubber, as it has had a significant impact on costs. When the price of crude oil rises, the price of synthetic rubber climbs with it. For oil, gas, and chemical businesses, the impact of COVID-19 and the oil price war is proving to be a two-pronged problem. Oil prices are falling because of failed production-cut agreements, and demand for chemicals and refined goods is slowing due to industrial slowdowns and travel restrictions in the aftermath of the global pandemic. Hence, changes in crude oil are a big problem for the elastomers industry's growth, as petrochemicals (crude oil derivatives) are a key raw ingredient for synthetic rubber. The disposal of elastomers raises environmental problems since hazardous waste is released.

The disposal of elastomers is a major source of worry for environmental organizations, as it releases a large number of harmful substances into the environment. Elastomer recycling alternatives are limited, and it is only achievable with uncured elastomers, while the majority of them are cured. These materials can be disposed of in two ways: incineration or landfills, both of which pose a risk to the environment. When elastomers are burned, carbon monoxide and hydrogen cyanide are released, both of which are unfavorable to the environment.

Increased Usage of High-performance Elastomers in Automotive Industry Creating New Opportunities

The automotive industry is expected to remain the largest application end-use industry of thermoplastic elastomer throughout the forecast period, followed by building & construction, in terms of volume.

Exterior body parts such as exterior filler panels, wipers, rocker panels, body seals, automotive gaskets, door & window handles, and vibration damping pads are made of thermoplastic elastomers.

Recent advancements in thermoplastic elastomer have allowed it to be used in under-the-hood automotive applications like belts and hoses, clamps, fuel lines, bonnet and boot buffer blocks, and bellows.

The thermoplastic elastomers market is expected to increase due to rising demand from the Asia-automotive Pacific's industry, the environmentally benign nature of thermoplastic elastomers, and advancements in the thermoplastic elastomer processing industry. The main restraints on the thermoplastic elastomers market are raw material price volatility and technical challenges in manufacturing low-cost, cost-effective thermoplastic elastomer products.

Elastomers Market Segmentation:

Elastomers Market Segmentation:

Based on Type, in 2024, Thermoset Elastomers dominated the Global Elastomers Market, supported by their superior heat resistance, durability, and compatibility with high-stress industrial applications such as automotive under-the-hood components, heavy machinery, and sealing systems. Their established manufacturing base and strong OEM reliance ensure a stable, leading share. Thermoplastic Elastomers (TPEs) are rapidly gaining momentum, driven by increasing demand for lightweight, recyclable, and easy-to-process materials across consumer goods, medical devices, electronics, and automotive interiors. Growth is further supported by advancements in TPE chemistry and sustainability-driven material substitution. Overall, market momentum is shifting toward flexible, eco-efficient, and high-performance elastomer solutions, strengthening the long-term adoption of TPEs alongside traditional thermosets.

Based on Application, in 2024, the Automotive segment dominated the Global Elastomers Market, driven by extensive use in sealing systems, hoses, belts, vibration damping, and lightweight interior components. Consumer Goods and Electrical & Electronics follow as major contributors, supported by rising demand for flexible, durable, and high-performance elastomeric materials in appliances, cables, connectors, and daily-use products. Industrial applications maintain a strong, stable share due to continuous use in gaskets, rollers, and machinery components. The Medical segment is rapidly expanding, fueled by growth in tubing, seals, wearables, and biocompatible elastomer adoption. Adhesives & Coatings and Sports & Leisure segments show steady growth, driven by product innovation and lifestyle-driven demand. Overall, application growth reflects a shift toward high-performance, lightweight, and sustainable elastomer solutions across diversified end-use industries.

Elastomers Market Regional Insights:

Because more than half of elastomer is used in tyre manufacturing, Asia Pacific held the biggest share of the Elastomers market in 2024, up to 63%, thanks to increased automotive production in countries like India, Malaysia, and others. Demand is expected to be fueled by government investment, liberalization policies, and private companies focusing on technology advancement. Also, the increased use of TPE to replace ethylene propylene diene monomer in construction equipment is expected to boost the market. Because of the cheap operating costs and rising demand for passenger automobiles, major automotive OEMs are relocating their production bases to these markets.

The objective of the report is to present a comprehensive analysis of the global Elastomers market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Elastomers dynamics, structure by analyzing the market segments and projecting the Elastomers size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the global Elastomers market make the report investor’s guide.

Elastomers Market Scope: Inquire before buying

| Global Elastomers Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 100.69 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 4.01% | Market Size in 2032: | USD 137.90 Bn. |

| Segments Covered: | by Type | Thermoset Elastomer Natural Rubber Synthetic Rubber Styrene-Butadiene Elastomer Butyl Elastomer Butadiene (Polybutadiene) Elastomer Nitrile Elastomer Acrylic Elastomer Ethylene-Propylene Elastomer Silicone (Q) Elastomers Fluoroelastomers Fluorocarbon (FKM) Elastomer Fluorsilicone (FQ) Elastomer Perfluorocarbon (FFKM) Elastomer Thermoplastic Elastomer Styrene Block Copolymer Thermoplastic Polyurethane Thermoplastic Polyolefins Thermoplastic Vulcanizates Thermoplastic polyester Elastomers Polyether Block Amide |

|

| by Type | Extrusion Injection Moulding Blow Moulding Compression Moulding Others |

||

| by Application | Automotive Adhesives & coatings Consumer Goods Medical Sports & leisure Electrical & Electronics Industrial Others |

||

Elastomers Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Elastomers Market, Key Players are

1. BASF

2. Dow Inc.

3. Covestro AG

4. LANXESS AG

5. DuPont de Nemours, Inc.

6. Kuraray Co., Ltd.

7. Huntsman International LLC

8. INEOS / Kraton Corporation

9. Asahi Kasei Corporation

10. LG Chem Ltd.

11. ExxonMobil Corporation

12. Arkema S.A.

13. JSR Corporation

14. Zeon Corporation

15. Wacker Chemie AG

16. Trinseo LLC

17. Evonik Industries AG

18. Mitsui Chemicals, Inc.

19. Teknor Apex Company

20. Wanhua Chemical Group Co., Ltd.

21. Ace Elastomer Co., Ltd.

22. ARLANXEO

23. Avient Corporation

24. DingZing Advanced Materials Co., Ltd.

25. Firestone Building Products

26. HEXPOL AB

27. KRAIBURG TPE GmbH

28. Lion Elastomers

29. Sirmax S.p.A.

30. UBE Corporation

31. Others

Frequently Asked Questions:

1] What segments are covered in the Elastomers Market report?

Ans. The segments covered in the Elastomers Market report are based on Type, Process, Application, and region

2] Which region is expected to hold the highest share of the Elastomers Market?

Ans. Asia Pacific region is expected to hold the highest share of the Elastomers Market.

3] What is the market size of the Elastomers Market by 2032?

Ans. The market size of the Elastomers Market by 2032 is USD 137.90 Bn.

4] What is the growth rate of the Elastomers Market?

Ans. The Global Elastomers Market is growing at a CAGR of 4.01 % during the forecasting period 2025-2032.

5] What was the market size of the Elastomers Market in 2024?

Ans. The market size of the Elastomers Market in 2024 was USD 100.69 Bn.