Digital Pathology Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

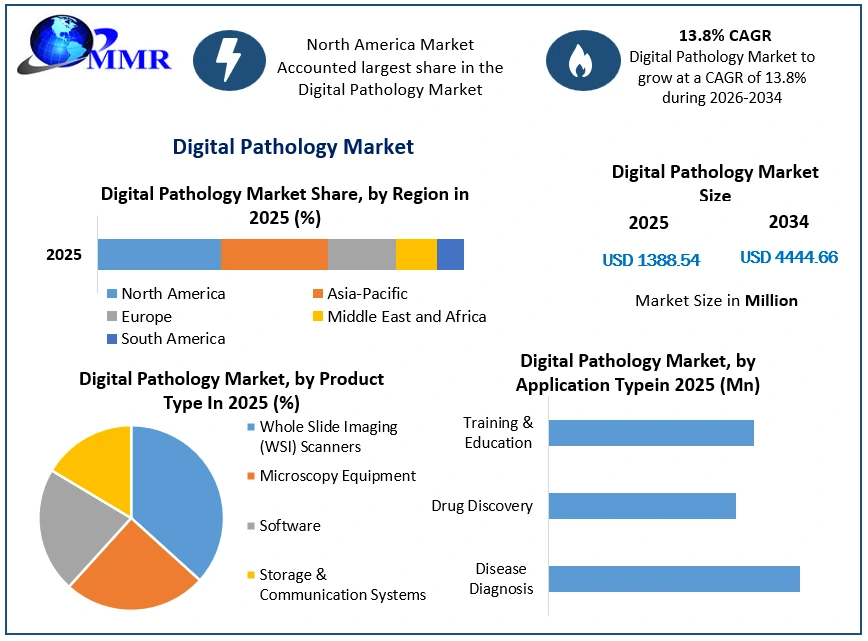

The Digital Pathology Market size was valued at USD 1388.54 Mn in 2025, and the total Digital Pathology revenue is expected to grow at a CAGR of 13.8% from 2026 to 2034, reaching nearly USD 4444.66 Mn.

Global Digital Pathology Market Overview

Digital pathology is a field that collects, interprets, analyses, and shares data using digital tools. Digital slides are created using either a full-slide scanning device or a digital microscope, directly from previously prepared slides. The digital slide is then analyzed using high-throughput algorithms, disseminated over the air (OTA), or saved for future use.

Over the last few years, digital pathology and image analysis have experienced rapid growth. This is primarily due to the use of whole-slide scanning, advancements in software and computer processing power, and the growing relevance of tissue-based research for biomarker identification and stratified medicine.

The Digital Pathology Market has been driven by an increased emphasis on enhancing workflow efficiency and a desire for rapid diagnosis tools for chronic illnesses such as cancer. The increased frequency of chronic diseases is expected to increase clinical urgency to embrace digital pathology to enhance existing patient diagnostic imaging measures and lower the high costs associated with conventional diagnostics. Likewise, the growing elderly population, which is sensitive to chronic illnesses, is expected to increase the demand for technologically advanced diagnostic techniques.

Increasing technological advancements in digital pathology systems are also expected to drive market growth during the forecast period. Digital imaging, computerization, robotic light microscopy, and numerous fiber optic links are all contributing to the growth. Whole slide imaging is one such approach that has several benefits over traditional light microscopes and is expected to generate profitable chances in this industry. The use of AI in healthcare is increasing, with a growing emphasis on enhancing patient care quality by incorporating AI into many elements of healthcare services, such as pathological diagnosis.

The report explores the Global Digital Pathology market's segments (Product Type, Application, End-User, and Region). Data has been provided by market participants, and regions (North America, Asia Pacific, Europe, Middle East & Africa, and South America). It provides a thorough analysis of the rapid advances that are currently taking place across all industry sectors. Facts and figures, illustrations, and presentations are used to provide key data analysis for the historical period from 2019 to 2024. The report investigates the Global Digital Pathology Market's drivers, limitations, prospects, and barriers. This MMR report includes investor recommendations based on a thorough examination of the Global Digital Pathology Market's contemporary competitive scenario.

To know about the Research Methodology :- Request Free Sample Report

Digital Pathology Market Dynamics

Digital Pathology Enhances Lab Efficiency to Boost the Digital Pathology Market Growth

Digital pathology enhances lab efficiency by lowering costs, shortening turnaround times, and providing users with subject-matter knowledge. Improvements in lab efficiency are crucial because patients and clinicians rely on lab data for diagnosis, and diagnostic tests must be conducted and reported swiftly and precisely. Similarly, pathologists may obtain digitized slides via web services, which minimizes shipping expenses and travel time.

High costs of digital pathology devices to create the Digital Pathology market restraint

A typical digital pathology system costs between USD 500,000 and USD 700,000 and contains a slide scanner, an image server, and software. In the Asia Pacific, the typical price of a digital pathology scanner is between USD 110,000 and USD 130,000. Although major hospitals with substantial capital budgets may purchase these technologies, pathologists and academic institutes with limited funds are unable to buy them.

Healthcare providers, particularly those in developing nations such as India, Brazil, and Mexico, lack the financial capacity to invest in such expensive technologies. Additionally, skilled professionals are necessary for the efficient operation and maintenance of digital pathology equipment. The expense of these systems, along with the difficulty of finding competent individuals to run digital pathology equipment, is expected to reduce their deployment.

Lack of trained professionals to address the Digital Pathology Market Challenge

Pathologists play an important role in executing laboratory tests that are required for disease diagnosis. However, there is a global supply-demand imbalance for pathologists, particularly in Africa and the Asia-Pacific area. According to Springer's research (2020), Switzerland has 35,355 residents per pathologist, while Canada and the United States have 20,658 and 25,325, respectively. In Germany, there is one pathologist for every 47,989 people.

Digital pathology enables healthcare professionals to safely and quickly communicate critical information with pathologists across geographical boundaries. Nevertheless, emerging technologies such as artificial intelligence (AI) and machine learning assist pathologists in identifying illnesses faster and improving their efficacy and efficiency. As a result, the worrisome lack of pathologists is expected to restrain the market growth.

Introduction of Artificial Intelligence (AI) to Create Digital Pathology Market Opportunity

Pathology is the most significant field of Medical Science since it deals with the genesis, cause, and type of disease. This domain provides the majority of the diagnostic infrastructure. Tissues, organs, and bodily fluids are all examined during a pathological examination. In this examination, the tissue is mounted on a glass slide using certain methods and then examined for the disease under a microscope. With technological innovation, classic pathological surgery is evolving into Digital pathology.

Digital pathology is the digitization of Histopathological slides using a Whole-slide scanner, which is a microscope under robotic and computer control, and the computational analysis of these digitalized pictures or whole-slide images. This digitization produces a high-resolution, improved pixel picture of diseased materials, resulting in massive amounts of data, up to terabytes per biopsy.

Artificial intelligence and machine learning have grown their roots in healthcare and clinical applications in recent decades as a result of algorithmic improvement and more convenient computer capacity. The synergy between artificial intelligence and digital pathology is one example of how these two areas overlap. This collaboration would provide spectacular results in diagnostic, prognostic, and predictive analysis of whole-slide pictures.

Digital Pathology Market Segment Analysis

Based on Product Type,The Digital Pathology market is segmented into Whole Slide Imaging (WSI) Scanners, Microscopy Equipment, Software, and Storage & Communication Systems. Whole Slide Imaging (WSI) Scanners segment dominated the Digital Pathology market in 2025 and is expected to hold the largest market share over the forecast period. Dominance is due to their critical role in digitizing slides for AI analysis and remote diagnostics. Among WSI scanners, high-throughput models lead as they meet the demand for rapid, large-scale scanning in hospitals and labs. Software, especially AI-powered image analysis, is growing fast but relies on WSI scanners. Cloud-based storage is gaining traction for scalability, yet on-premise solutions remain strong for data security. While microscopy equipment is essential, it’s being replaced by WSI for digital workflows. Thus, WSI scanners, particularly high-throughput ones, drive market dominance.

Based on Application, The Digital Pathology market is segmented into Disease Diagnosis, Drug Discovery, and Training & Education. The Disease Diagnosis segment dominated the Digital Pathology market in 2025 and is expected to hold the largest market share over the forecast period. Dominance due to the urgent clinical need for accurate and efficient diagnostic solutions, particularly in oncology and chronic diseases, where AI-powered tools enhance precision and speed. The widespread adoption by hospitals and labs, regulatory approvals for AI-based diagnostic platforms, and the integration of digital pathology into routine workflows further solidify its lead. While drug discovery leverages digital pathology for biomarker research and preclinical studies, its application remains more specialized and less scalable than diagnostics. Training and education, though growing, have slower adoption rates, making disease diagnosis the clear leader in market share and impact.

Based on End-User, The Digital Pathology market is segmented into Hospitals & Diagnostic Labs, Pharmaceutical & Biotechnology Companies, and Academic & Research Institutions. Hospitals & Diagnostic Labs segment dominated the Digital Pathology market in 2024 and is expected to hold the largest market share over the forecast period. Dominance due to the increasing adoption of digital solutions for accurate and faster disease diagnosis, particularly in cancer and chronic diseases. The shift from traditional microscopy to whole-slide imaging (WSI) and AI-powered diagnostics enhances efficiency and reduces errors. Meanwhile, pharmaceutical & biotech companies use digital pathology for drug development and toxicology studies, but their market share is smaller due to niche applications. Academic & research institutions contribute to growth through education and training, but lack the scale of clinical adoption. Thus, hospitals & labs lead, driven by diagnostic demand and technological advancements.

Digital Pathology Market Regional Analysis

North America Dominated the Digital Pathology Market in 2025

North America dominated the digital pathology market, driven by advanced healthcare infrastructure, high adoption of AI-based diagnostics, and strong government support for digital healthcare. The U.S. led due to widespread use of whole-slide imaging in hospitals, large investments in precision medicine, and key industry players like Roche and Philips. Europe followed, with growth fueled by telepathology adoption and regulatory approvals. Meanwhile, Asia-Pacific showed rapid expansion due to increasing healthcare digitization but lagged behind North America in market share. Early adoption, robust R&D, and favorable reimbursement policies solidified North America’s leadership in 2025.

Digital Pathology Market Competitive Landscape

In 2025, the digital pathology market was led by Roche (Ventana Medical Systems) and Philips, both dominating due to their advanced whole-slide imaging (WSI) systems and AI-powered pathology solutions. Roche generated approximately $1.2 billion in revenue from its digital pathology segment, driven by its VENTANA DP 600 scanner and strong oncology diagnostics portfolio. Philips followed closely with around $900 million, leveraging its Intelli Site Pathology Solution and cloud-based platforms for seamless integration in hospitals. Both companies maintained leadership through strategic partnerships, AI innovations, and extensive global distribution networks. Competitors like Leica Biosystems and Hamamatsu trailed behind, focusing on niche markets. Roche’s dominance stemmed from its stronghold in cancer diagnostics, while Philips excelled in workflow efficiency and telepathology, making them the top two players in 2025’s competitive landscape.

Digital Pathology Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 06 May 2026 | Artera | Artera received U.S. Food and Drug Administration (FDA) clearance for its ArteraAI Breast test to support risk stratification in patients with early-stage breast cancer. | This milestone introduces the first digital pathology-based multimodal artificial intelligence prognostic tool for breast oncology, delivering rapid, localized risk scores without additional tissue requirements. |

| 23 February 2026 | Labcorp | Labcorp announced an expanded national collaboration with PathAI to deploy the FDA-cleared AISight Dx digital pathology platform across its comprehensive laboratory network. | The deployment scales fully digital workflows and AI-enabled computational insights across anatomic pathology hubs to improve turnaround times and precision medicine data infrastructure. |

| 01 October 2025 | Leica Biosystems | Leica Biosystems introduced its advanced image management software, Aperio HALO AP, alongside the debut of the integrated Aperio AI Store platform. | Developed in tandem with Indica Labs, this roll-out unifies algorithms from multiple vendors under a single interoperable slide-review architecture to minimize software tool fragmentation. |

| 15 May 2025 | Bioptimus | Bioptimus announced the public deployment of its open-source pathology foundation model, H-optimus-1, on the AWS Marketplace. | This release drastically lowers the technical barrier for life science research institutions seeking to run complex image-based diagnostic classification and multi-modal cellular analysis. |

Global Digital Pathology Market Recent Trends

1. AI and Machine Learning Integration

• AI-powered image analysis tools are enhancing diagnostic accuracy and workflow efficiency.

• Deep learning algorithms aid in the automated detection of cancer, fibrosis, and other pathologies.

2. Rising Demand for Telepathology & Remote Diagnostics

• The post-pandemic era has accelerated the adoption of telepathology, enabling remote consultations.

• Cloud-based digital pathology platforms facilitate real-time collaboration among pathologists globally.

• Global Digital Pathology Market Dynamics.

Digital Pathology Market Scope: Inquire before buying

| Digital Pathology Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 1388.54 Mn. |

| Forecast Period 2026 to 2034 CAGR: | 13.8% | Market Size in 2034: | USD 4444.66 Mn. |

| Segments Covered: | by Product Type | Whole Slide Imaging (WSI) Scanners Microscopy Equipment Software Storage & Communication Systems |

|

| by Application Type | Disease Diagnosis Drug Discovery Training & Education |

||

| by End User | Hospitals & Diagnostic Labs Pharmaceutical & Biotechnology Companies Academic & Research Institutions |

||

Digital Pathology Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Philippines, Thailand, and Rest of Asia Pacific)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

North America Digital Pathology Market Key Players

1. Inspirata (USA)

2. Proscia (USA)

3. PathAI (USA)

4. Corista (USA)

5. Ibex Medical Analytics (USA)

6. DeepBio (USA)

7. Indica Labs (USA)

8. Paige AI (USA)

Europe Digital Pathology Market Key Players

1. Sectra (Sweden)

2. 3DHISTECH (Hungary)

3. VisioPharm (Denmark)

4. Leica Biosystems (Germany)

5. Philips Digital Pathology Solutions (Netherlands)

6. Definiens (Germany)

7. Aiforia (Finland)

8. Indica Labs Europe (UK)

9. Amphivena Therapeutics (Switzerland)

10. Finland (Finland)

11. ContextVision (Sweden)

Asia Pacific Digital Pathology Market Key Players

1. DeepBio (South Korea)

2. Lunit (South Korea)

3. Pantarhei Bioscience (Singapore)

4. Hamamatsu Photonics (Japan)

5. Mindpeak (China)

6. Yitu Healthcare (China)

7. Jiangsu RichMed Technology (China)

8. 3DHISTECH Asia (South Korea)

9. TRIBVN Healthcare (Vietnam)

10. Sysmex (Japan)

Middle East and Africa Digital Pathology Market Key Players

1. Veolity Technologies (UAE)

2. Xybion Digital (UAE)

3. Pathology Insights (South Africa)

4. Medopad (UAE/UK)

5. Elite Diagnostics (Saudi Arabia)

6. Cerner Middle East (UAE)

South America Digital Pathology Market Key Players

1. Phelcom Technologies (Brazil)

2. HI solutions (Brazil)

3. Medvision (Argentina)

4. Dasa (Brazil)

5. Clínica Alemana (Chile)

FAQ

1. Which is the potential market for Digital Pathology in terms of the region?

Ans. North America is the potential market for Digital Pathology in terms of region.

2. What are the opportunities for new market entrants?

Ans. The key opportunity in the market is the Introduction of Artificial Intelligence (AI) in Digital Pathology.

3. What is expected to drive the growth of the Digital Pathology market in the forecast period?

Ans. A major driver in the Digital Pathology market is the rising deployment of Digital Pathology for enhanced lab efficiency.

4. What is the projected market size & growth rate of the Digital Pathology Market?

Ans. The Digital Pathology Market size was valued at USD 1388.54 Mn. in 2025, and the total Digital Pathology revenue is expected to grow at 13.8% from 2026 to 2034, reaching nearly USD 4444.66 Mn.

5. What segments are covered in the Digital Pathology Market report?

Ans. The segments covered are Product, Application, End-User, and Region.