Data Center Construction Market Size by Infrastructure Type, Tier Standard, Data Centre, End User, and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

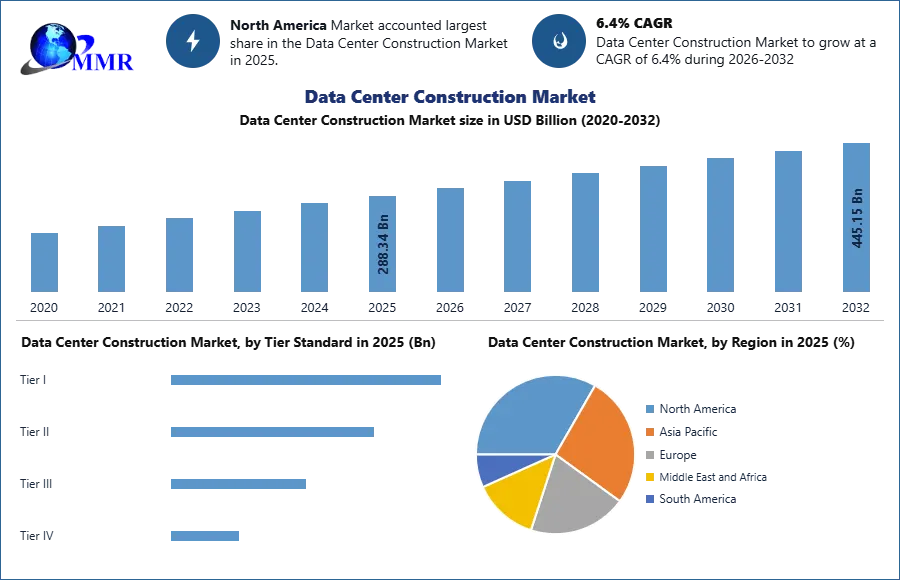

Data Center Construction Market was valued at USD 288.34 billion in 2025, and total global Data Center Construction Market revenue is expected to grow at a CAGR of 6.40% from 2026 to 2032, reaching nearly USD 445.15 billion. Rising adoption of cloud computing and big data analytics.

Data Center Construction Market Overview:

The data center construction market plays a critical role in the development of specialized facilities tailored to accommodate computer systems and associated components like telecommunications and storage systems. These facilities are essential for facilitating data processing, storage, and management functions for a wide array of entities, including businesses, government agencies, and cloud service providers. Key elements of data center construction involve thorough processes such as site selection, design, engineering, construction, and installation, all aimed at ensuring optimum functionality and performance. These processes take into account various factors, including power access, network connectivity, security, and environmental considerations. Following construction, meticulous commissioning and testing procedures are carried out to verify compliance with performance and reliability standards. Once operational, ongoing maintenance, monitoring, and management are necessary to uphold reliability, efficiency, and security. The data center construction market is witnessing significant growth fueled by escalating demands for data storage and processing capacity, the expansion of cloud computing, the proliferation of digital services, and continuous technological advancements.

To know about the Research Methodology:- Request Free Sample Report

The surge in data consumption and the heightened demand for cloud computing among enterprises are significant catalysts propelling the growth of the data center construction market. The exponential increase in data consumption is driven by a multitude of factors, including the widespread adoption of digital technologies across various industries. With the advent of e-commerce, social media platforms, digital content streaming, Internet of Things (IoT) devices, and big data analytics, businesses are generating and processing immense volumes of data to gain insights, enhance customer experiences, and optimize operations. Consequently, the need for robust data storage and processing infrastructure is paramount, leading to a surge in demand for data center facilities.

Usage Rate (%) Social Platform in 2025

Simultaneously, the growing reliance on cloud computing is reshaping the IT landscape, with enterprises increasingly turning to cloud-based services for their scalability, flexibility, and cost-effectiveness. Cloud computing offers businesses the ability to access IT resources and applications on-demand, without the need for on-premises hardware and infrastructure. This shift towards cloud adoption is fueled by factors such as the need for greater agility, the rise of remote work, and the desire to reduce IT operational costs. As more businesses migrate their workloads to the cloud, there is a corresponding increase in demand for data centers to host cloud infrastructure and support cloud service providers.

Furthermore, the scalability and agility offered by modern data centers play a crucial role in meeting the dynamic needs of businesses undergoing digital transformation. Today's data centers are designed to be modular and adaptable, allowing for seamless expansion and customization to accommodate changing workloads and emerging technologies. This flexibility is essential for businesses seeking to leverage innovations such as artificial intelligence (AI), machine learning (ML), and edge computing to gain a competitive edge in their respective industries. Public cloud providers like Facebook, Google, and Amazon.com, Inc. are expected to persist in their investments aimed at enhancing their current infrastructure. This ongoing commitment is poised to unlock growth prospects for the data center construction market.

Moreover, the heightened focus on data security, privacy, and regulatory compliance is driving investments in secure and compliant data center facilities. With an increasing number of cyber threats and stringent data protection regulations, businesses are prioritizing the security of their data assets and ensuring compliance with regulatory requirements. Data center construction addresses these concerns by implementing advanced security measures such as access controls, encryption, firewalls, and surveillance systems to safeguard sensitive information and mitigate the risk of data breaches.

The surge in data consumption and the growing demand for cloud computing services are fundamental drivers behind the expansion of the data center construction market. As businesses continue to embrace digital transformation and rely on data-driven strategies to drive innovation and growth, the need for scalable, secure, and agile data center infrastructure will only continue to grow, driving further investment in data center construction projects worldwide.

Asia Pacific IT infrastructure market booms in 2025, driven by networking equipment surge and digital transformation. In 2025, the Asia Pacific IT infrastructure market experienced notable growth, primarily driven by a surge in sales of networking equipment, including switches and routers. This growth was propelled by key players such as Huawei Technologies Co. Ltd., Dell Inc., and Hewlett Packard Enterprise Development LP, which played pivotal roles in shaping the data center construction market dynamics in the region. These companies' strategic initiatives, including the introduction of new products in the servers and networking sectors, significantly contributed to the growth of the IT infrastructure segment across the Asia Pacific region.

Huawei Technologies Co. Ltd., known for its comprehensive portfolio of networking solutions, continued to strengthen its presence in the Asia Pacific data center construction market with innovative offerings. Dell Inc., renowned for its high-performance servers and networking equipment, capitalized on the region's growing demand by introducing advanced products tailored to meet the evolving needs of businesses. Similarly, Hewlett Packard Enterprise Development LP leveraged its expertise in data center solutions to drive growth, launching cutting-edge products aimed at enhancing networking capabilities across the Asia Pacific region.

The increased adoption of digital technologies, coupled with the region's expanding economy, created a favorable environment for investments in IT infrastructure. Companies across various industries sought to modernize their IT environments to support digital transformation initiatives, leading to heightened demand for networking equipment and servers. This trend is expected to persist as businesses continue to prioritize technological advancements to improve operational efficiency and maintain competitiveness in the evolving digital landscape.

The growth of the Asia Pacific IT infrastructure market during fiscal year 2025 underscores the region's importance as a key driver of global technological innovation. With continued investments from leading players and ongoing digital transformation initiatives, the Asia Pacific region is poised to remain a significant growth engine for the IT infrastructure market during the forecast period.

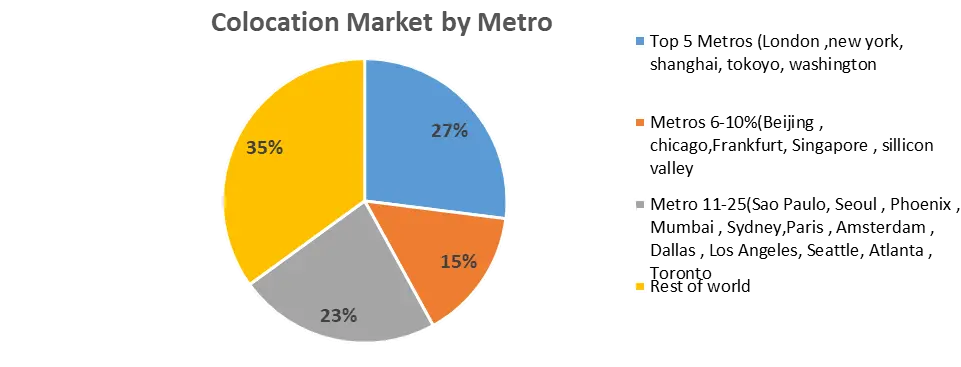

Growth in colocation facilities poised to drive future data center construction market.

The growth of colocation facilities is poised to play a pivotal role in driving the future development of the data center construction market. Colocation, also referred to as multi-tenant data centers, entails the sharing of physical space and infrastructure by multiple tenants, typically businesses or organizations, each maintaining their own computing equipment and servers. This approach offers a multitude of advantages, including cost savings, scalability, reliability, and access to advanced infrastructure and services. As businesses increasingly acknowledge the benefits of colocation, the demand for such facilities is on the rise, necessitating additional construction and expansion projects within the data center industry.

Top 25 metros create 65% of worldwide colocation revenues in 2025

One fundamental driver behind the proliferation of colocation facilities is the swift digitization of businesses and the proliferation of data-intensive applications and services. With the exponential growth in data volumes and the pressing need for secure and dependable data storage and processing capabilities, businesses are turning to colocation providers to meet their evolving IT infrastructure demands. Colocation facilities boast state-of-the-art security measures, redundant power and cooling systems, and high-speed connectivity, making them an appealing choice for organizations seeking to outsource their data center requirements.

Furthermore, the escalating complexity of IT environments and the heightened emphasis on disaster recovery and business continuity planning are compelling organizations to leverage colocation services. By collocating their IT infrastructure in purpose-built data centers, businesses can ensure greater resilience and redundancy, thereby mitigating the risks associated with downtime and data loss. Additionally, colocation providers often extend managed services, encompassing network monitoring, maintenance, and support, thereby further enriching the value proposition for businesses.

Moreover, the ascent of cloud computing and hybrid IT environments is driving demand for colocation services. Many organizations are adopting a hybrid cloud strategy, blending on-premises infrastructure with cloud-based solutions. Colocation facilities serve as optimal environments for hosting private cloud deployments and connecting to public cloud providers, facilitating seamless integration and interoperability across diverse IT environments.

The expected growth in colocation facilities is poised to emerge as a significant catalyst for future data center construction. As businesses increasingly rely on colocation services to meet their evolving IT infrastructure needs, the demand for purpose-built data center facilities is expected to soar, presenting lucrative opportunities for construction companies and industry stakeholders.

Data Center Construction Market Segment Analysis

Based on Infrastructure Type, in 2025, the Electrical Infrastructure dominated the segment in the data center construction market. This is because uninterrupted power supply, power distribution units (PDUs), UPS systems, backup generators, and switchgears are the backbone of any data center facility. With the exponential rise in cloud computing, AI-driven workloads, and hyperscale data centers, power demand has surged significantly. Companies are investing heavily in advanced electrical infrastructure to ensure redundancy and energy efficiency, as downtime leads to massive financial losses. The growing adoption of renewable energy integration and smart power management systems also strengthens this segment’s dominance. Hence, electrical infrastructure holds the largest share in overall spending.

Based on Tier Standard, in terms of tier classification, Tier III data centers dominated the global market in 2025. These facilities offer an optimal balance of cost-effectiveness, reliability, and scalability, making them the preferred choice for enterprises and colocation providers. Tier III provides concurrent maintainability, meaning components can be replaced or repaired without downtime, ensuring 99.982% uptime. Unlike Tier I and II, which lack redundancy, Tier III ensures business continuity at a reasonable cost compared to Tier IV. With rising demand for hybrid IT environments and digital transformation initiatives, Tier III facilities remain the most widely adopted worldwide. Thus, Tier III leads the tier standard category in 2025.

Data Center Construction Market Regional Analysis:

In 2025, North America emerged as the dominant force in the data center construction market, commanding the largest revenue share of over 40.0%, followed closely by Asia Pacific. The substantial revenue share of North America can be attributed to its aggressive investments in hyperscale projects. As a developed economy, the United States boasts a well-established and sophisticated network infrastructure. Moreover, it serves as the headquarters for major cloud service providers, including Amazon.com, Inc., Google, and Facebook. These companies are actively investing in the construction of large-scale facilities to expand their processing capabilities and data storage capacity, thereby creating new avenues for growth in the data center construction market. Meanwhile, in the Asia Pacific region, the market for data center construction is poised to experience the swiftest growth throughout the forecast period, with notable contributions from China and India. This growth is fueled by continuous investments from cloud service providers and hyperscale entities, reflecting the region's increasing significance in the global digital landscape.

Key Companies and Market Share Overview

Favorable government initiatives aimed at reducing barriers for IT companies to operate across borders are yielding positive outcomes for the network infrastructure ecosystem. Consequently, companies are exhibiting aggressive investment behaviors in emerging economies across Latin America, the Middle East, Africa, and other regions to expand their operations. Numerous market players are forging partnerships with their clients to introduce innovative techniques geared towards enhancing the efficiency and sophistication of data centers. For instance, Nortek Air Solutions, a leading manufacturer of commercial HVAC systems, has collaborated with Facebook to develop a groundbreaking cooling technology. Known as State Point Liquid Cooling, this innovative approach utilizes direct evaporative cooling with outside air, resulting in a water-efficient and energy-efficient facility.

Data Center Construction Market Recent Industry Developments (2025–2026)

| Date | Company | Development | Impact |

|---|---|---|---|

| 21 January 2025 | Microsoft | Microsoft announced a massive $80 billion investment plan for new data center construction primarily focused on the United States. | The move aims to scale AI infrastructure footprint and meet the rising demand for generative AI workloads. |

| 15 January 2025 | Schneider Electric | Schneider Electric acquired APower, a provider of data center infrastructure solutions, for $1.2 billion. | This acquisition expands their capabilities in mission-critical electrical infrastructure and high-density power management. |

| 12 February 2025 | Compass Datacenters | Compass Datacenters broke ground on a $10 billion AI-ready campus in Mississippi. | The project introduces large-scale capacity in emerging regional markets to support distributed AI processing. |

| 24 February 2025 | Data4 | Data4, backed by Brookfield, committed $20 billion to construct specialized AI data center infrastructure in France. | The investment addresses sovereign data requirements and explosive demand for high-capacity facilities in Europe. |

| 18 June 2025 | Amazon (AWS) | Amazon announced a $13 billion investment plan through 2029 to expand and maintain data center infrastructure in Australia. | This initiative supports the surging demand for cloud computing and AI services across the Asia-Pacific region. |

| 05 January 2026 | KDDI | KDDI and partners launched the Osaka Sakai AI Data Center featuring NVIDIA Blackwell architecture. | The facility utilizes hybrid cooling systems to optimize energy efficiency for next-generation AI deployments. |

Data Center Construction Market Scope: Inquire before buying

| Data Center Construction Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 288.34 USD Billion |

| Forecast Period 2026-2032 CAGR: | 6.4% | Market Size in 2032: | 445.15 USD Billion |

| Segments Covered: | by Infrastructure Type | Electrical infrastructure UPS Power distribution units (PDUs) Backup generators Others Mechanical infrastructure Cooling systems Hvac Racks Ductwork Raised flooring Others Networking Infrastructure Others |

|

| by Tier Standard | Tier I Tier II Tier III Tier IV |

||

| by Data Center | Small-scale data center Medium data center Large data center |

||

| by End Use | BFSI Energy Government Healthcare Manufacturing IT & Telecom Media & Entertainment Retail Others |

||

Data Center Construction Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/Competitors profiles covered in the Data Center Construction Market report in strategic perspective

- Corgan Associates, Inc.

- Holder Construction

- Turner Construction

- DPR Construction

- Structure Tone

- Mortenson Construction

- Gilbane Inc.

- Balfour Beatty US

- Hensel Phelps

- Hoffman Construction

- HITT Contracting

- Fluor Corporation

- IMC Construction

- Pepper Construction

- FORTIS Construction Inc.

- A. Mortenson Company

- Brasfield & Gorrie, L.L.C.

- Rogers-OBrien Construction Company, Ltd

- AECOM

- Jacobs

- Clayco

- Skanska USA Building, Inc.

- The Whiting-Turner Contracting Company

- JE Dunn Construction

- McCarthy Building Companies

- Clark Construction Group

- Larsen & Toubro Limited