Commercial Vehicle Driver Information System Market Size by Component, Vehicle Type, Sales Channel, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

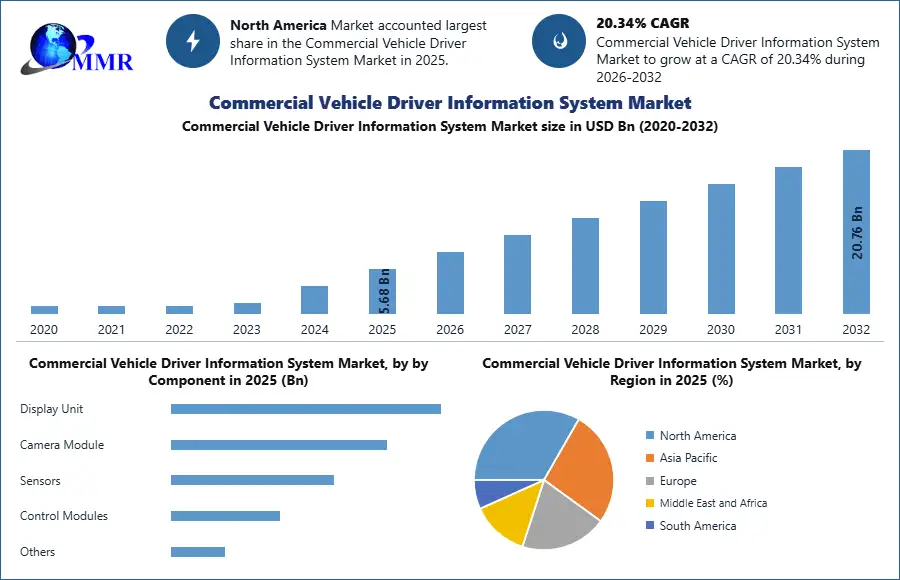

Commercial Vehicle Driver Information System Market size was valued at USD 5.68 billion in 2025, and the total revenue is expected to grow at CAGR of 20.34 % from 2025 to 2032, reaching nearly USD 20.76 billion.

Commercial Vehicle Driver Information System Market: Market Overview

In today’s transportation ecosystem, Commercial Vehicle Driver Information Systems (CVDIS) are transforming fleet operations by enhancing road safety, operational visibility, and driver behavior monitoring. With increasing regulatory pressure and the need for safer logistics infrastructure, these systems are seeing widespread adoption across both long-haul and regional transport fleets.

OEMs and fleet operators are leveraging these technologies to comply with safety mandates, reduce accidents, and improve driver efficiency. As advanced driver-assistance features such as forward collision warnings, automatic emergency braking, and lane departure alerts become standard, the CVDIS market is rapidly evolving toward smarter, AI-enabled platforms.

The MMR report provides comprehensive coverage of this transformation, including in-depth consumer and fleet operator insights, ADAS penetration comparisons between commercial and passenger vehicles, global and regional adoption rates, pricing and cost structure analyses, emerging innovation trends such as HUDs, AR interfaces, and biometric driver IDs, and the evolving manufacturing landscape impacted by supply chain disruptions. It also explores ESG considerations like CO₂ reductions through eco-driving tools, recent investments and M&A activity in the driver tech space, and the shifting regulatory landscape across key geographies, including mandates from EU, US, and India related to driver monitoring, alerts, and connected safety systems.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Commercial Vehicle Driver Information System Market: Market Dynamics

Pricing Trends of Commercial Vehicle Driver Information System Cluster Type

In 2025, the Display Unit segment dominates the Commercial Vehicle Driver Information System market, as it serves as the primary interface for delivering real-time vehicle data, navigation, and driver alerts. Increasing demand for advanced dashboards and digital cockpits in commercial vehicles is driving this segment. Sensors and Camera Modules are also witnessing strong growth due to their critical role in enhancing driver awareness, safety, and ADAS integration. Meanwhile, Control Modules remain essential for system processing and integration but are comparatively mature, while other components support niche and auxiliary functionalities.

Based on Cluster Type, Digital Clusters represent the fastest-growing and most demanded segment in 2025. Their ability to provide customizable displays, real-time analytics, and integration with telematics and infotainment systems makes them highly preferred by fleet operators and OEMs. Hybrid Clusters are gaining traction as a transitional solution combining analog reliability with digital flexibility. In contrast, Analog Clusters continue to decline in adoption due to limited functionality and lack of advanced features.

By Propulsion Type, ICE Vehicles currently hold the largest market share in 2025, owing to their dominant presence in the global commercial vehicle fleet. However, Electric Vehicles (EVs) are the fastest-growing segment, driven by increasing electrification trends, regulatory support, and the need for advanced driver information systems tailored to battery monitoring, energy efficiency, and range optimization.

| Commercial Vehicle Driver Information System Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 5.68 USD Bn |

| Forecast Period 2026-2032 CAGR: | 20.34% | Market Size in 2032: | 20.76 USD Bn |

| Segments Covered: | by Component | Display Unit Camera Module Sensors Control Modules Others |

|

| By Cluster Type | Analog Digital Hybrid |

||

| By Propulsion Type | ICE Vehicles Electric Vehicles |

||

| by Vehicle Type | Light Commercial Vehicles (LCVs) Small Vans Pickup Trucks Others Heavy Commercial Vehicles (HCVs) Freight Trucks Long Haul Trucks Articulated Trucks Others Buses & Coaches City Buses Luxury Coaches Others |

||

| by Sales Channel | OEMs Aftermarket |

||

Commercial Vehicle Driver Information System Market: Regional Analysis

The objective of the report is to present a comprehensive analysis of the Global Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that includes market leaders, followers, and new entrants.

PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Global Market dynamics, structure by analyzing the market segments and projects the Global Market size. Clear representation of competitive analysis of key players by Provider type, price, financial position, Product portfolio, growth strategies, and regional presence in the Global Market make the report investor’s guide.

Scope of the Global Commercial Vehicle Driver Information System Market: Inquire before buying

Global Commercial Vehicle Driver Information System by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Commercial Vehicle Driver Information System Key Companies are:

- Bosch Automotive Technologies

- Continental AG

- HARMAN International

- IAC Group

- Luxoft

- Nippon Seiki Co., Ltd.

- NVIDIA Corporation

- Panasonic Corporation

- Pricol Ltd.

- Renesas Electronics Corporation

- Simco Ltd.

- Spark Minda

- Stoneridge Inc.

- Valeo SA

- Visteon Corporation

- Yazaki Corporation

- Infineon Technologies

- NXP Semiconductors

- Mobileye

- Autoliv Inc.

- Daimler

- Ford

- Denso Corporation

- Japan Display Inc.

- Aisin Corporation

- Aptiv Plc

- EDGE3 Technologies

- Gentex Corporation

- Omron Corporation

- Texas Instruments Incorporated

- Toyota Industries Corporation