Automotive Chip Market Size by Component Type, Vehicle Type, Application Type, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

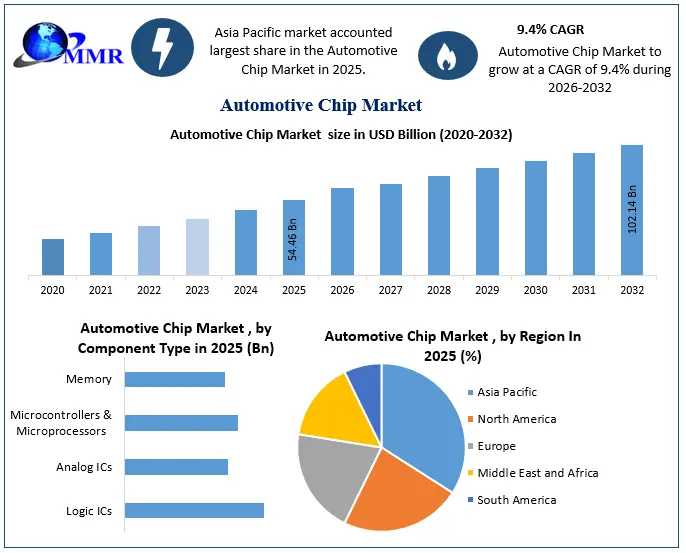

Automotive Chip Market size was valued at USD 54.46 billion in 2025, and the total Automotive Chip revenue is expected to grow at a CAGR of 9.4% from 2026 to 2032, reaching nearly USD 102.14 billion.

Automotive Chip Market Overview

Automotive chips are particularly semiconductors designed for vehicles, which enable tasks such as engine control, security system (ADAS), infotainment, and electric powertrain. They include microcontroller (MCU), power management ICs, sensors, and connectivity modules, strict automotive-grade reliability (AEC-Q100) and security (ISO 26262) standards. These chips ensure excessive temperature, vibration and long-life cycle (10–15 years).

Automotive chip markets increase demand from electric vehicles (EVS), ADAS and connected cars, which increases the annual growth up to 12%+. However, the supply remains forced by limited semiconductor FAB capacity, geopolitical stress and prolonged lead time (6+ months). While new fabs are planned (e.g., TSMC in Arizona, Infineon in Germany), a lack of deficiency remains in Legacy Nodes (40NM-90NM), keeping prices high. Long-term contracts are secured for stabilizing automakers' supply chains. The expansion of capacity is expected to reduce the imbalance by 2026–2027.

The Asia-Pacific (APAC) dominated the demand of the Automotive Chip Market, led by China, Japan, and South Korea, fueled by EV adoption. Top players include Renesas (Japan), Samsung (Korea), and HiSilicon (China), driving innovation in power and AI chips.

To Know About The Research Methodology :- Request Free Sample Report

To Know About The Research Methodology :- Request Free Sample Report

To Know About the Research Methodology

The automotive chip market is not only benefiting from the growth of the electric and autonomous vehicle market but also from the increased connectivity features in modern cars. As cars become more connected, they require more advanced chips to handle the data processing and communication needs. The chips are used in various applications such as telematics, wireless charging, and advanced navigation systems. With the rise of 5G networks, the demand for automotive chips that can handle the increased data transfer speeds is also on the rise. The automotive chip market is expected to continue growing at a significant rate throughout the forecast period. The automotive industry is becoming increasingly dependent on chips to power the cars of the future.

Tesla had an internal chip design team as early as five years ago. The original focus was on MCUs. Later, the car manufacturer shifted chip design to power modules. For example, Hyundai Motor announced the establishment of a chip design team on September 4, while CRRC and BYD directly included the wafer factory in the scope of vertical integration.

A CPU chip for the automotive system called the Snapdragon Ride Flex SoC was introduced by Qualcomm Technologies, Inc. It manages assisted driving as well as cockpit features like entertainment. Taiwan Semiconductor Manufacturing Co. launched new software to make it easier for customers developing high-tech computer chips for automotive to benefit from its most recent innovations. The largest contract maker of semiconductors in the world is TSMC. Many of the largest chip manufacturers serving the automotive sector, including NXP Semiconductor and STMicroelectronics NV (STM.DE), use TSMC to produce their components.

Automotive Chip Market Recent Technology Trend

Possibility to mitigate yield limitations by combining several node sizes

In recent years, after decades of successful development toward smaller node sizes, semiconductor players appear to have reached physical limitations, especially in ensuring economic yields. Since monolithic SoCs are designed as fully integrated chips, all parts need to be on the same small node size. For chip designers, this leads to a trade-off, as small node sizes are beneficial for HPC but not ideal for certain other parts, such as analog functions. By disaggregating the monolithic chip into Chiplets, this need for one node size is removed, as each Chiplet’s node size can be chosen individually. From a yield perspective, this is very interesting: One small defect on a large, fully integrated monolithic SoC leads to the waste of the entire chip. Whereas in Chiplet Systems, the defect will only impact the single Chiplet where the defect is located, while other Chiplets are not affected. Overall, Chiplet Systems come with yield and cost benefits due to the disaggregation into different node sizes.

High scalability and modularity

High scalability and modularity

For monolithic SoCs, changes to parts of a chip lead to a redesign (at least partly) of the whole SoC, which results in high R&D costs. In Chiplet Systems, a single Chiplet can be interchanged and replaced. This step is possible without a re-design of the architecture as long as the architecture was designed correctly and the modifications/changes stay within certain limits. The development effort for modular solutions addressing scalability or customization requests from OEMs might be significantly reduced in this way. Chiplet Systems can therefore serve as a bridging technology in hybrid E/E architectures and also as an alternative alongside monolithic SoCs in future centralized compute architectures.

Automotive Chip Market Dynamics

Growing shift towards the use of electric and hybrid vehicles reduces vehicle emissions, to Drive Market Automotive Chip Growth

Motor vehicles not running on fossil fuels, such as electric vehicles, hybrid electric vehicles,Solar-powered vehicles are the primary choice for alternative technologies of powering an engine that does not involve petroleum. Increasing the use of electric and hybrid vehicles will help reduce fuel costs for consumers, minimize air pollution due to a reduction in greenhouse gases (GHGs), improve air quality in urban areas, and lower dependence on fossil fuels. The adoption of electrified vehicles will lead to a significant rise in demand for new automotive ICs, microprocessors, and sensors.

Global Automotive Chip Shortage Slows Market Growth Amid Supply Chain Disruptions to Restrain the Automotive Chip Market

The automotive chip market faces significant restraints due to persistent supply chain disruptions, hampering production and delaying vehicle deliveries. Despite rising demand for electric and connected vehicles, production bottlenecks limit market expansion. Efforts to ramp up chip fabrication capacity are underway, but long lead times and high investment costs delay relief. As a result, the automotive chip market growth is projected to slow in the near term, with recovery dependent on stabilized supply chains and increased semiconductor manufacturing resilience.

Temperature Sensitivity and High Entry Costs to Create Automotive Chip Market Challenge

The wide variety in temperatures inside and outside cars is the largest issue with automobile electronics. Lack of cooling prevents chips from malfunctioning and aging too quickly. Performance chips raise emissions, harm the engine, and result in misfires when they are exposed to higher temperatures. Developing automotive chip applications requires significant investment in research, development, and testing. The complexity of automotive systems and the strict requirements for reliability and safety contribute to the high cost of chip development. The cost barrier prevents smaller players from entering the market and limits innovation.

Automotive Chip Market Segment Analysis

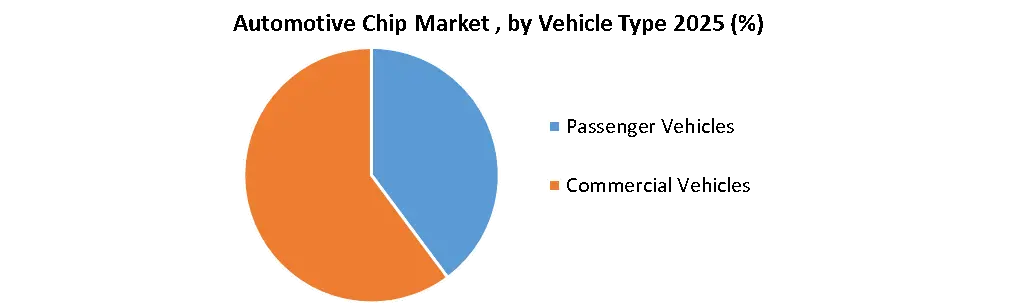

Based on Vehicle Type, the Passenger Vehicles Segment has dominated the Automotive Chip Market in 2024 and is expected to hold the largest market share over the forecast period. Dominance due to the larger share compared to commercial vehicles. The surge in demand for advanced driver-assistance systems (ADAS), infotainment, and electric vehicles (EVs) in passenger cars drove higher semiconductor consumption. Rising consumer preference for connected and autonomous features further boosted chip usage. In contrast, commercial vehicles, though increasingly adopting telematics and automation, had lower production volumes and slower tech integration rates. Additionally, stringent emissions norms and fleet electrification in some regions supported growth, but passenger vehicles remained the primary driver due to higher sales volumes and faster adoption of advanced electronic systems.

Automotive Chip Market Recent Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 20 May 2026 | Infineon Technologies AG | The company officially launched the Moore4Power project, an ambitious €91 million EU flagship research initiative with 62 partners focused on heterogeneous integration of Si, SiC, and GaN technologies for power electronics. | The initiative will significantly shorten automotive development cycles and unlock up to 99% efficiency architectures with near-lossless bidirectional charging capabilities for next-generation e-mobility platforms. |

| 21 May 2026 | Qualcomm Technologies, Inc. | The company announced an expanded multi-year strategic technology collaboration with Stellantis to integrate its Snapdragon Digital Chassis and Snapdragon Ride Pilot platforms across next-generation vehicle architectures. | The integration establishes a common, high-performance computing foundation that drives massive cost efficiency through platform standardization across millions of production vehicles. |

| 15 April 2026 | Silicon Box | The semiconductor packaging specialist formally joined imec's Automotive Chiplet Program (ACP) to deliver end-to-end expertise in high-density chiplet interconnection protocols. | This alliance helps de-risk production pipelines and establishes standardized, interoperable packaging standards required to lower costs for software-defined vehicles. |

| 17 February 2026 | Renesas Electronics Corporation | The company expanded its manufacturing partnership with GlobalFoundries (GF) to secure long-term capacity for its advanced automotive microcontrollers across global foundry footprints. | This strategic shift drastically enhances supply chain resilience and guarantees production flexibility to meet growing microchip volume demands in connected automotive segments. |

| 04 February 2026 | Mythic | The artificial intelligence hardware specialist signed a definitive agreement with Honda Motor Co. to co-develop analog compute-in-memory (CiM) system-on-chip systems for software-defined vehicles. | The resulting neuromorphic architecture is targeted to deliver up to a 100x improvement in energy efficiency for high-compute automated driving algorithms within power-constrained vehicular platforms. |

| 22 April 2025 | Intel Corporation | At Auto Shanghai 2025, the company unveiled its second-generation AI-enhanced Software-Defined Vehicle (SDV) system-on-chip featuring the industry’s first automotive chiplet architecture. | The platform accelerates digital cockpit innovation by unlocking centralized high-performance computing capabilities like localized large language models (LLMs) and advanced 3D human-machine interfaces. |

Automotive Chip Market Regional Analysis

The Asia Pacific region held the largest share of 40 % in 2025. Thailand, India, Japan, South Korea, China, and the Rest of Asia-Pacific are evaluated for the Asia-Pacific automotive Chip market growth analysis. Japan leads in terms of raw materials, small active-passive components, and equipment regarding semiconductors in the region. Also, the country has a significant advantage in upstream semiconductor materials along the semiconductor value chain. In addition, the country is capable of meeting the high standards of purity required for semiconductor materials. The rising demand for electric vehicles and government measures encouraging the adoption of electric vehicles are the main factors driving the growth of the automotive chip market in the area. Also, the region is experiencing a marked increase in vehicle production, which is projected to support the growth of the automotive chip industry in the area. TSMC and Samsung competed for dominance in the wafer foundry sector, stemming from the growing popularity of smartphones. The winner was determined by securing orders for application processors from tech giants like Apple, Qualcomm, and MediaTek. TSMC's outperformance showcased Taiwan's aggressive investments in semiconductor equipment.

NFC chip is one of the key NFC products available with various applications such as contactless mobile payments, information sharing, and information security. These chips produce a short-range radio signal used for sensitive financial and authentication data transmission. In Japan, several leading market players are actively developing NFC-based cashless payment devices and readers for the Japanese market, showing the rising adoption of NFC chips. Additionally, private organizations are also adopting NFC technology, which is expected to boost the growth of the near-field communication market in Japan. The government of South Korea approved a service that enables the consumer to authenticate mobile payment by tapping a contactless card, which helps increase the need for NFC chips in South Korea. The rising penetration of smartphones also drives the market through the forecast period. The uncertainties surrounding technological competition between China and the US have also interrupted the global supply chain; for example, smartphone and network device manufacturers have stocked up on semiconductor components. Multinational companies have also held inventory volumes above their normal levels to offset the potential loss owing to the uncertainty of the entire market.

Automotive Chip Market Competitive Landscape

The automotive chip market is fiercely competitive, in which NXP Semiconductor and Infineon Technologies dominate the sector. In 2024, NXP Semiconductor reported USD xx billion in automotive revenue, driven by the strong demand for ADAS, EV Powertrains and In-WHYCLE networking. Infineon Technologies recorded USD xx billion in automotive sales, affected by its leadership in electrical semiconductor and microcontroller solutions for electric and connected vehicles. Both companies continue to invest heavily in R&D and secure their positions as market leaders in a rapidly electrified and autonomous-operated industry to capitalize on the growing need for advanced automotive electronics.

Automotive Chip Market Scope: Inquire before buying

| Global Automotive Chip Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 54.46 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 9.4% | Market Size in 2032: | USD 102.14 Bn. |

| Segments Covered: | by Component Type | Logic ICs Analog ICs Microcontrollers & Microprocessors Memory |

|

| by Vehicle Type | Passenger Vehicles Commercial Vehicles |

||

| by Application Type | Chassis Powertrain Safety Telematics & Infotainment Body Electronics |

||

Automotive Chip Market, Key Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Automotive Chip Market, Key Players

North America Automotive Chip Market Key Players:

1. Texas Instruments (TI) - Dallas, Texas

2. Intel (Mobileye) - Santa Clara, California

3. ON Semiconductor - Phoenix, Arizona

4. Microchip Technology - Chandler, Arizona

5. Qualcomm - San Diego, California

Europe Automotive Chip Market Top Players

1. Infineon Technologies – Neubiberg, Germany

2. STMicroelectronics – Geneva, Switzerland

3. NXP Semiconductors – Eindhoven, Netherlands

4. Robert Bosch – Gerlingen, Germany

5. ams-OSRAM – Premstätten, Austria

APAC Automotive Chip Market Top Players:

1. Renesas Electronics – Tokyo, Japan

2. Samsung Semiconductor – Suwon, South Korea

3. ROHM Semiconductor – Kyoto, Japan

4. Huawei HiSilicon – Shenzhen, China

5. UNISOC – Shanghai, China

Frequently Asked Questions:

1] What segments are covered in the Automotive Chip Market report?

Ans. The segments covered in the Automotive Chip Market report are based on Component Type, Application Type, and Vehicle Type.

2] Which region is expected to hold the highest share in the Automotive Chip Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Automotive Chip Market.

3] What is the market size of the Automotive Chip Market by 2032?

Ans. The market size of the Automotive Chip Market by 2032 will be USD 102.14 billion.

4] What is the forecast period for the Automotive Chip Market?

Ans. The Forecast period for the Automotive Chip Market is 2026- 2032.