Cold Storage Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

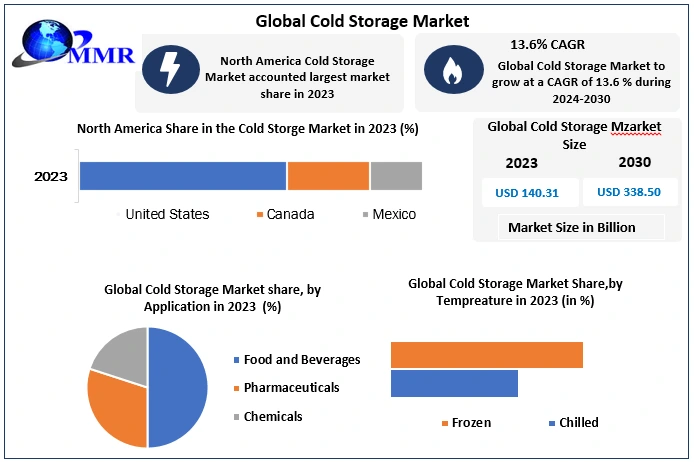

The Cold Storage Market size was valued at USD 181.07 Billion in 2025 and the total Cold Storage revenue is expected to grow at a CAGR of 13.6% from 2025 to 2032, reaching nearly USD 442.07 Billion.

Cold Storage Market Overview

Cold storage refers to the preservation of food or other items in a freezer or other cold location. Food stored in freezers is maintained for a longer period. Also, storing or moving temperature-sensitive products is an important aspect of the supply chain management system. Cold storage technology office benefits include modern refrigeration technology, as well as maintaining and before including for diverse products such as fruits and vegetables, which significantly reduces the potential of air temp product waste.

The cold storage industry offers refrigeration for various requirements and has a range of services spanning several sectors. However, the most significant usage of cold storage is in the food & and beverage industry.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Cold Storage Market Dynamics

Increasing Demand for Perishable Goods to Drive the Market Growth

The growth of the cold storage market is driven by the rising demand for perishable goods, including fresh fruits, vegetables, dairy products, and pharmaceuticals. As global supply chains expand and consumers seek diverse and fresh products year-round, there is a growing need for efficient cold storage solutions. Cold storage facilities help maintain the quality and safety of perishable items, extending their shelf life and reducing wastage. With a rising global population and changing consumer preferences, the demand for cold storage is expected to increase significantly.

In U.S. agricultural exports, moving away from bulk commodities like wheat and soybeans towards non-bulk items, specifically perishable products such as meats and fruits. This transformation is primarily attributed to income growth, trade liberalization in high- and middle-income markets in East Asia, North America, and the European Union, and advances in transportation technology. Perishable products now constitute approximately 20% of total U.S. food and agricultural exports. Technological advancements in transportation have facilitated the delivery of perishable goods over long distances at lower costs, reducing the wedge between exporting and importing country prices.

Innovations in packaging, coatings, and bioengineering have further extended the marketing reach of U.S. perishable products, allowing them to reach high- and middle-income Cold Storage Market in East Asia, North America, and Europe. The ocean and overland trades now accommodate a wider range of perishable products, enabling U.S. exports to cover greater distances, particularly in horticultural and livestock categories.

E-commerce and Online Grocery Retail Surge to Boost the Market

The rapid growth of e-commerce and online grocery retail is another key driver for the cold storage market. As consumers increasingly turn to online platforms for their shopping needs, there is a surge in the demand for quick and reliable delivery of perishable goods. Cold storage facilities play a crucial role in the e-commerce supply chain by ensuring that temperature-sensitive products are stored and transported under optimal conditions. This trend is expected to intensify with the ongoing digitalization of retail and the expansion of online grocery services, driving the need for more sophisticated and expansive cold storage infrastructure.

Technological Advancements and Automation in Cold Storages to Create Lucrative Opportunity for Market Growth

The cold storage market is poised for substantial growth through the integration of advanced technologies and automation. Pioneering innovations such as IoT sensors, RFID systems, and AI-driven analytics offer a transformative opportunity by enhancing operational efficiency and precision. Real-time monitoring capabilities ensure optimal conditions for stored goods, a crucial aspect for industries such as pharmaceuticals, food and beverages, and biotechnology. Automation in material handling, inventory tracking, and order fulfillment emerges as a cost-effective solution, minimizing errors and streamlining processes.

Cold storage providers embracing these technological advancements position themselves as industry leaders, offering reliability and cost efficiency. This strategic investment not only caters to existing demands but also expands their clientele across diverse sectors. The adoption of cutting-edge technologies becomes the key to competitiveness, providing a pathway to meet the dynamic needs of clients in the ever-evolving landscape of cold storage services.

Cold storage technologies offer useful features, such as advanced refrigeration technologies and monitoring and tracking systems of various products like fruits and vegetables, significantly lessening the possibility of wastage of temperature-sensitive goods. However, the major challenge for industry players is to expand the cold storage market. Due to a lack of infrastructure, it is hard to maintain the cold storage market. Also, the lack of reliable power supply for cold warehouses further increases the operation costs. However, this also opens opportunities for the industry players to develop unique solutions that can overcome the unreliable power supply in emerging markets. Rising alertness about hygiene is causing consumer preferences to shift toward ready-to-cook meals.

Consumers are favoring frozen food due to the ease of use in terms of packing technique and support for microwave cooking. However, the lack of refrigeration facilities in retail stores and inadequate distribution facilities to serve the rural areas pose major challenges to the frozen food market in developing economies. The major driving growth factors for the cold storage market are increasing demand for healthy food, import and export of refrigerated foods, and increasing private sector participation.

Abuse of temperature and duration is a significant impediment to market progress. Additionally, a lack of experienced staff and insufficient cold chain management are putting a brake on the cold storage industry.

Cold Storage Market Segment Analysis

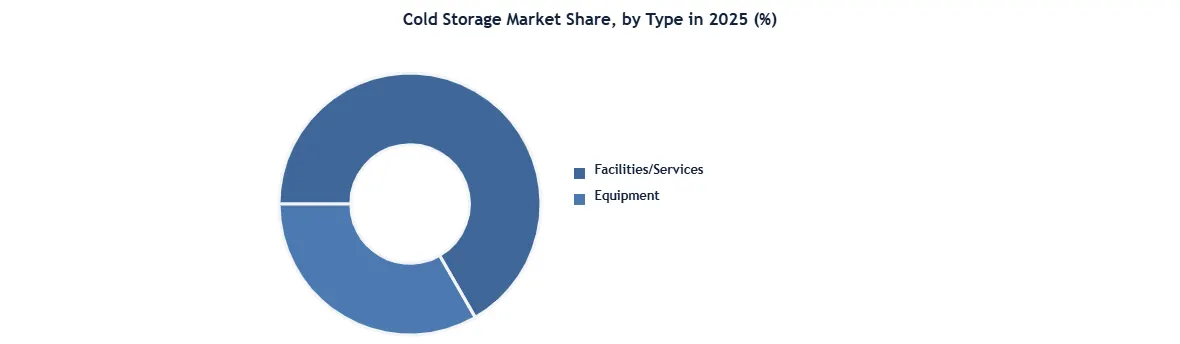

Based on Type In the global cold storage market, the facilities/services segment dominates and accounts for the major revenue share, primarily because large-scale refrigerated warehouses and integrated cold chain services are essential for storing perishable food, pharmaceuticals, and chemicals. This segment includes public and private refrigerated warehouses, cold rooms, and value-added services such as inventory handling, transportation, and monitoring. The expansion of organized food retail, online grocery platforms, and frozen food consumption has increased demand for outsourced cold storage facilities. In 2025, facilities/services held roughly 89% of market revenue, supported by investments in automated warehouses, energy-efficient systems, and AI-based monitoring.

Based on construction type, the bulk storage segment held the largest Cold Storage Market share in 2025. Bulk Storage facilities are designed for large-scale storage, accommodating high volumes of perishable goods, making them suitable for industries with substantial inventory requirements. Production Stores are tailored for manufacturing environments, offering controlled conditions for processing and preserving goods during production. Ports represent specialized cold storage facilities located at maritime hubs, facilitating efficient import and export of temperature-sensitive commodities. Each construction type addresses specific operational demands, ensuring the preservation of perishables across various industries. This segmentation underscores the adaptability and versatility of cold storage solutions in meeting the unique requirements of bulk storage, production, and port logistics.

Based on application, the food and beverages segment dominated the largest Cold Storage Market share in 2025. The Cold Storage industry, as reflected by Microlistics WMS, plays a pivotal role in maintaining food safety and brand integrity across the supply chain. With a focus on compliance, the system seamlessly integrates government-mandated regulations into its framework, ensuring adherence to critical parameters such as temperature control, batch, lot, use-by dates, and more. The segmentation of temperature zones acknowledges the unique storage needs of various perishable products, reflecting the industry's commitment to preserving freshness. The emphasis on track and traceability underscores the importance of thorough inventory management, essential for meeting regulatory requirements and swiftly responding to potential recalls.

Microplastics WMS not only addresses the challenges of recall execution but also facilitates cost accountability through detailed tracking of labor and materials. This technology-driven approach enhances efficiency, minimizes wastage, and fosters confidence in the safety and quality of stored goods. As the industry continues to evolve, leveraging automated systems, such as Microlistics WMS, becomes imperative for cold storage operators, retailers, and manufacturers seeking to optimize operations, ensure compliance, and uphold brand reputation.

Several industries use cold storage services to preserve food items. Restaurants, food outlets, supermarkets and grocery shops are a few of these industries. These industries may require domestic fridges, entire cold rooms or blast freezers based on the type of item being stored and the customers’ needs. Blast freezers are needed to keep a large number of food items for long periods.

Cold Storage Market Regional Analysis

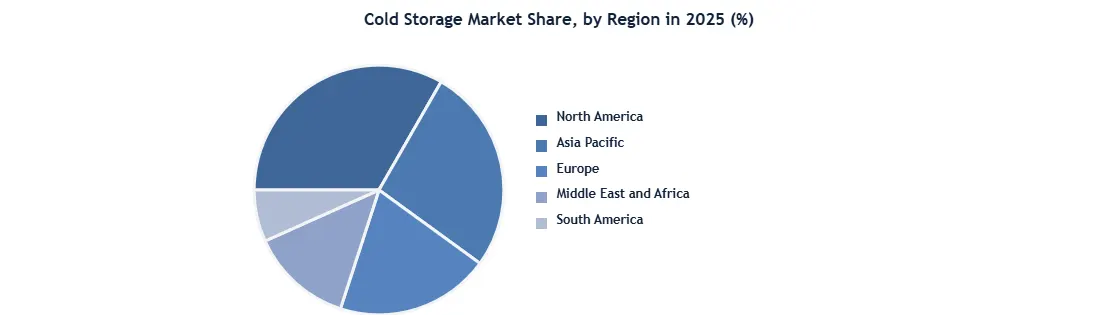

North America held the largest Cold Storage Market share in 2025 and the US has a major share. The U.S. cold storage market is influenced by growth, driven by an anticipated surge in e-commerce's share of grocery sales from 13% in 2021 to 21.5% by 2025. The speculative cold storage development in the U.S. has increased substantially to 3.3 million sq. ft., up from 300,000 sq. ft. in 2019. Despite this, new entrants face challenges such as high construction costs and complex user requirements. Investor interest in cold storage has risen, with 40% seeking assets in 2022 compared to 22% in 2021.

Third-party logistics providers represent 34% of leasing activity, reflecting outsourcing trends due to cost considerations and advanced technology systems. Consolidation is evident, with Lineage Logistics and Americold now commanding 71% of North America's cold storage space. While outsourcing is growing for the industrial market, cold storage sees a decline, with 72% outsourced to public refrigerated warehouses, down from 75% five years ago. This dynamic market shift indicates opportunities and challenges for both investors and operators in the evolving cold storage landscape.

Also, a growing demand for frozen and perishable goods, advanced infrastructure, and stringent quality standards propel the industry forward. The United States, with its robust supply chain and technological innovations, dominates the market. Rising consumer preferences for convenience foods and e-commerce trends further boost the demand for cold storage solutions.

The Asia Pacific cold storage market is expected to grow at a significant CAGR over the forecast period. With a surge in urbanization and changing lifestyles, there is a heightened demand for frozen and processed foods. Countries such as China and India play pivotal roles, witnessing substantial investments in cold chain infrastructure. The e-commerce boom and improving logistics contribute to the market's growth. The Asia Pacific region emerges as a key player in the global cold storage landscape, offering lucrative opportunities for industry participants.

The cold storage market in Asia Pacific is experiencing significant growth, driven by factors such as increasing household incomes, urbanization, changes in consumer behavior, and the boom in e-commerce. The demand for cold storage facilities is expected to continue rising, supported by government initiatives, especially in countries with significant agricultural industries. Governments in several Asian countries have implemented policies and initiatives to boost the domestic pharmaceutical industry. These initiatives include the development of infrastructure, tax incentives, research and development funding, and streamlined regulatory processes.

Cold Storage Market Recent Development

April 2025 – Lineage, Inc. announced expansion of its U.S. cold-storage network through acquisition of four warehouses from Tyson Foods for about $247 million, adding 49 million cubic feet capacity and strengthening automated operations.

May 2025 – Americold Realty Trust expanded its North American network by acquiring a high-capacity cold warehouse in Houston to support food retail distribution and regional logistics expansion.

June 2025 – NewCold partnered with Walmart to establish a dedicated automated cold distribution center in the U.S., improving supply chain efficiency for frozen food distribution.

June 2025 – Americold Realty Trust announced a US$250 million investment for new cold storage facilities across the U.S., aimed at increasing warehouse capacity and serving growing demand from frozen and fresh food sectors.

July 2025 – Lineage, Inc. accelerated deployment of automation and AI-driven warehouse systems to improve energy efficiency, labor optimization, and inventory management across its global cold chain sites.

September 2025 – Americold Realty Trust strengthened international logistics through strategic cooperation with rail and port operators, expanding integrated refrigerated import-export transportation services in North America.

Cold Storage Market Scope: Inquire before buying

| Cold Storage Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 181.07 USD Billion |

| Forecast Period 2026-2032 CAGR: | 13.6% | Market Size in 2032: | 442.07 USD Billion |

| Segments Covered: | by Type | Facilities/Services Refrigerated Warehouse Private & Semi-Private Public Cold Room Equipment Blast freezer Walk-in Cooler and Freezer Deep Freezer Others |

|

| by Temperature Range | Frozen (-18°C to -25°C) Chilled (0°C to 15°C) Deep-frozen (Below -25°C) |

||

| by Storage Capacity | Small Scale (up to 5,000 pallets) Medium Scale (5,001–20,000 pallets) Large Scale (above 20,000 pallets) |

||

| by Construction | Bulk Storage Production Stores Ports |

||

| by Application | Food & Beverages Fruits & Vegetables Fruit Pulp & Concentrates Dairy Products Milk Butter Cheese Ice cream Others Fish, Meat, and Seafood Processed Food Bakery & Confectionary |

||

Cold Storage Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Cold Storage Market, Key Players

- Lineage, Inc.

- Americold

- NewCold Advanced Cold Logistics

- Nichirei Logistics Group

- United States Cold Storage

- Maersk

- DHL Supply Chain

- Kuehne + Nagel

- Constellation Cold Logistics

- Burris Logistics

- Agro Merchants Group

- Congebec Logistics

- VersaCold Logistics Services

- Conestoga Cold Storage

- Emergent Cold Latin America

- Frialsa Frigorificos

- SuperFrio Logistica

- STEF Group

- Interstate Warehousing

- Tippmann Group

- FreezPak Logistics

- Magnavale

- Arcadia Cold Storage & Logistics

- Vertical Cold Storage

- Agile Cold Storage

- Interport Cold Storage

- Oxford Cold Storage

- Frigoscandia

- Snowman Logistics

- ColdEX

- Nordic Logistics and Warehousing

- Coldman Logistics

- RINAC

- Confederation Freezers

- Chiltern Cold Storage Group

- Friozem Armazens Frigorificos

- Comfrio Logistica

- Localfrio

- RSA Cold Chain

- Sharjah Cold Stores

- Kerry Logistics Network

- Sinotrans

- NSSPL

- Frick India Limited

- GK Cold Chain Solutions

- Sical Logistics

- HSH Cold Storage

- ColdStar Logistics

- Inland Cold Storage

- Crystal Logistic Cool Chain