Cloud Kitchen Market Size by Type, Product, Nature, Deployment, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2030

Overview

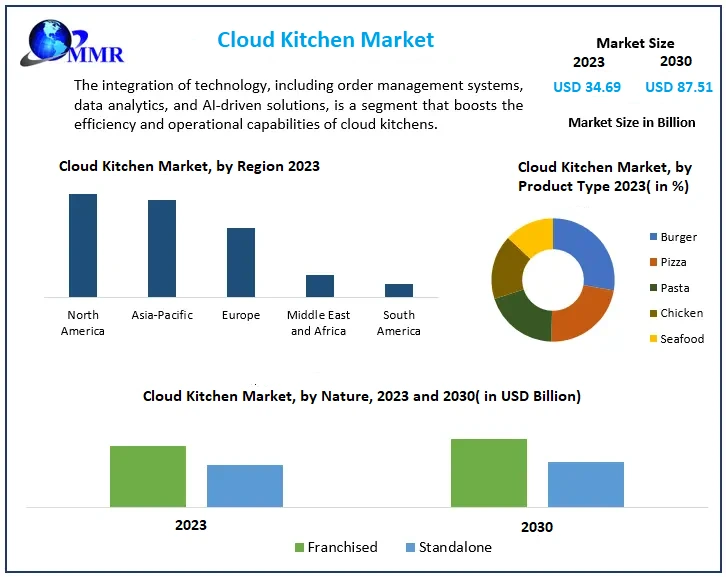

Global Cloud Kitchen Market size was valued at USD 34.69 Bn in 2023 and Cloud Kitchen Market revenue is expected to reach USD 87.51 Bn by 2030, at a CAGR of 14.13% over the forecast period.

Cloud Kitchen Market Overview

In the global food industry, a virtual kitchen is known as “Cloud Kitchen.” It is a commercial kitchen that provides the food business with the facilities and services needed to prepare food items for delivery and takeout.

The increasing preference for convenient and quick meal options fulfils the demand for cloud kitchens. Growing dependence on online platforms for various services, including food ordering, is reshaping consumer behavior and driving the demand for virtual kitchens.

Cloud kitchens operate with lower overhead costs as they eliminate the need for physical dining spaces, reducing expenditures related to rent, utilities, and decor. It offers a cost-effective solution for food entrepreneurs and established restaurant chains.

They eliminate the need for a physical shop, reducing overhead costs associated with traditional brick-and-mortar establishments. Cloud kitchens have been hosting multiple virtual restaurants or brands under one physical roof. This allows for a diverse range of cooking options to be offered from a single location. In urban areas with socially diverse populations, cloud kitchens have been provided to various tastes and preferences.

The integration of advanced technologies, including artificial intelligence (AI), data analytics, and kitchen management software, is a key trend in Cloud Kitchen Market. Cloud kitchens leverage technology to optimize operations, enhance efficiency, and improve the overall customer experience.

Data analytics tools enable cloud kitchens to gather insights into customer preferences, ordering patterns, and popular menu items. This data-driven approach allows for informed decision-making regarding menu optimization, pricing strategies, and marketing initiatives, contributing to better overall business performance.

The integration of advanced technologies positively impacts the cloud kitchen market by driving operational efficiency, enhancing customer experiences, and providing operators with valuable insights to adjust to Cloud Kitchen market trends. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Cloud Kitchen Market Dynamics

Increasing demand for food delivery services

Customers' convenience is the main factor behind the increase in demand for meal delivery services. The need for hassle-free meal options, urbanization, and busy lifestyles have all contributed to a notable movement toward online food ordering.

Online meal delivery is growing due to several variables, including changing lifestyles, faster smartphone adoption rates, and easier access to e-banking systems, better food-service logistics, and higher internet penetration rates.

The MMR Analysis indicates that Indian meal delivery services such as Zomato and Swiggy have set goals to reach 200 million users over the next five years, with 83 million monthly active users in 2023. The increasing demand for food delivery services has reshaped the cloud kitchen market, driving innovation and the evolution of business models.

Adoption of Digital Technologies

The adoption of digital technologies in the food industry, particularly within the context of cloud kitchens, has been a transformative factor that significantly enhances the efficiency and customer experience.

Food ordering and consumption have undergone significant changes as a result of technological advancements and integration. Through online meal-ordering apps, cloud kitchens are revolutionizing the food sector today.

Compared to the brick-and-mortar business model and restaurant setup, the cost of starting a cloud kitchen business is comparatively quite inexpensive. A cloud kitchen has a minimal capital expenditure (Capex) and can be put up for about one-third of what it costs to open a restaurant.

Unlike typical dine-in restaurants, cloud kitchen businesses do not have to worry about exorbitant rental costs, restaurant interiors, or guest facilities. The majority of investment in cloud kitchen businesses, however, goes toward supply chain management, well-equipped kitchen infrastructure, workforce training, delivery fleet, and technology.

Opportunities in the Cloud Kitchen Market

In comparison to traditional kitchens in dine-in restaurants, cloud kitchens, also known as virtual or ghost kitchens, are far less expensive to operate because they do not need dine-in facilities or take into account expenditures connected to property and location. Customers' and company owners' perspectives on the restaurant industry have rapidly changed in response to the current shift in the times.

The restaurant's income has increased recently, although a few years ago the home delivery service only made up a small part of it. Restaurant owners might, for instance, employ cutting-edge techniques to gather consumer data to assess and update their menu based on consumer demand and swap out goods with better margin options.

Ghost kitchens are preferred by restaurant owners and operators who experiment with new food items and serve inventive fare to test and identify meals before serving them to customers or guests. Additionally, ghost kitchens give companies the chance to serve clients directly without being constrained by extra expenses or steadily growing real estate prices.

Compared to restaurants that accept dine-in customers, cloud kitchens have far greater potential for profitability and faster operational scaling. The Cloud kitchen Market has profit margins that typically range from 20% to 25%.

For example, how much money you make from a cloud kitchen business depends on how many orders you handle each day. A cloud kitchen requires an initial expenditure of between Rs. 7 Lacs and Rs. 8 Lacs to operate. However, it will vary based on the business's location, size, scope, food type provided, and technological setup.

Restraining Factors

The Cloud Kitchen Market's Growth Is Restricted by High Initial Costs and Intense Competition

Establishing and equipping a cloud kitchen with the necessary infrastructure, technology, and kitchen equipment can require a substantial initial investment. This financial barrier may limit entry for some potential players in the Cloud Kitchen market.

Setting up a cloud kitchen involves significant infrastructure costs, including the lease or construction of a commercial kitchen space. Outfitting the kitchen with essential equipment, ventilation systems, and safety measures adds to the initial financial investment.

The Cloud Kitchen Market is being hampered by low-profit margins and intense competition. Additional factors such as trust defects, and multiple brands come with multiple problems, hygiene & and working conditions, lack of pricing power no feedback loop, and the need to tightly monitor inventory.

The taste, distinctive product options, and accessibility of fast-food items, however, are typically what draw in target clients. Consuming these goods frequently, however, has a deleterious impact on users' health. For example, the majority of fast-food items including drinks and sides are high in carbs with minimal fibre content.

Consequently, eating a lot of carbohydrates might cause blood sugar to increase often. As a result, the risk of type 2 diabetes, weight gain, and insulin resistance is increased.

Cloud Kitchen Market Segment Analysis

By Type: The Independent Cloud Kitchen segment is expected to grow at the highest CAGR during the forecast period independent cloud kitchens heavily rely on third-party delivery channels and mostly serve customers who choose a certain food type.

The growing consumer taste for fast food, international cuisine, and online ordering is expected to fuel the segment's growth. The concept of shared kitchens is becoming more and more popular among restaurateurs, and there are many advantages to it.

This has led to an increase in the number of commissary kitchens. As an additional revenue stream, restaurants are renting out more and more of their cooking space to various food service companies.

Additionally, an increase in the number of food trucks and caterers using the storage space and open time slots provided by restaurant facilities is expected to fuel Cloud Kitchen's market growth.

By Product: Cloud kitchens focusing on specific products can tailor their marketing and branding strategies to target customer segments, creating a more personalized and appealing customer experience. Cloud Kitchen Market growth is being aided by a growth in the working population. The burger/sandwich sector, which accounted for around 32% of the total sales, held the biggest share of the Cloud Kitchen Market in 2023. With the growing emphasis on health and wellness, some cloud kitchens focus on offering nutritious and health-conscious menu options Salads, smoothies, and other foods that emphasize organic, fresh, or low-calorie components may fall under this category.

The demand for fast food services increased during the pandemic as a result of the availability of meal packages and delivery services. The demand for fast foods is also being driven by customers increasing tendency to snack.

By Nature: the acceptance of international Consumer interest in specialty foods and foods is encouraging business owners to invest in well-known brands. The franchisor also offers training and assistance, including marketing and staff training, supplies, and equipment, so opening such restaurants entails fewer risks.

As a result, advantages including the low risk of starting a cloud kitchen and receiving a sizable profit share are expected to fuel the segment's growth. The integration of technology in cloud kitchens can support sustainability initiatives.

For example, advanced inventory management systems can help reduce food waste by optimizing ingredient usage and minimizing overstock. Cloud kitchens, being delivery-centric, often invest in innovative and eco-friendly packaging solutions to minimize environmental impact. This includes the use of recyclable materials and packaging designs that minimize waste.

By Deployment Type: the deployment segments in the cloud kitchen market reflect the diverse approaches businesses take to enter and operate in the virtual kitchen space. The use of web-based platforms and mobile applications for online food ordering has significantly impacted the cloud kitchen market.

Consumers can easily browse menus, place orders, and track deliveries through user-friendly interfaces, contributing to the growth of the delivery-only model. Mobile deployment enhances the accessibility of cloud kitchens, allowing customers to place orders conveniently through mobile apps.

This accessibility caters to the on-the-go lifestyle of modern consumers who prefer the convenience of ordering food from their smartphones.

Cloud Kitchen Market Regional Insights

North America: Particularly the United States, has a mature and well-established cloud kitchen market. The presence of major food delivery platforms and a tech-savvy consumer base has fuelled the growth of cloud kitchens.

The United States held the largest share of the North American food service market. Food delivery platforms' services and the convenience they offer to customers and restaurants are the main drivers of market growth in North American countries.

These distribution systems have increased across the US in recent years, surpassing the competition in Silicon Valley. In North America, these platforms now boast over 20 million daily active users and have grown to become significant industry players. DoorDash, GrubHub, Uber Eats, Foodpanda, Instacart, Deliveroo, Postmates, Seamless, and Gopuff are a few of the prominent platforms in North America.

Europe: Rich and diverse culinary landscape provides a significant opportunity for cloud kitchens. Operators can cater to the varied tastes and preferences of European consumers by offering a wide range of cuisines.

The ability to provide diverse menu options allows cloud kitchens to attract a broad customer base and adapt to local tastes. The ongoing trend of urbanization in European cities is a key driver for the growing demand for food delivery services.

Cloud kitchens strategically located in urban centers can tap into this trend by catering to the needs of busy urban dwellers seeking convenient and diverse dining options.

Asia-Pacific: This region has witnessed rapid growth in the cloud kitchen market. Rising urbanization, changing lifestyles, and a strong emphasis on food delivery contribute to the growth of cloud kitchen operations.

The convenience of mobile payments aligns with the tech-savvy nature of consumers in the region. Cloud kitchens can integrate secure and user-friendly mobile payment options into their platforms to streamline the ordering and payment processes.

Many of the countries in this area are going through a rapid digitalization process, which is expected to create opportunities for growth for the regional market participants. To obtain a competitive advantage in the market, more restaurateurs are setting up their cloud kitchens due to changing customer preferences and the rising popularity of international cuisine.

The use of cloud kitchens can also assist restaurateurs in testing out their new products without detracting from the in-game experience.

Competitive Landscape of Cloud Kitchen Market

The intense competition encourages cloud kitchens to innovate in terms of menu offerings. To stand out, operators often develop unique and diverse menus, introducing new culinary concepts and catering to specific dietary preferences. This innovation contributes to meeting varied consumer demands.

In November 2021 - Auntie Anne's and Cinnabon declared a deal with franchise group Fresh Dining Concepts to bring 10 co-branded Auntie Anne's and Cinnabon locations to the five New York City boroughs over the next four years. The agreement between Fresh Dining Concepts and Auntie Anne's and Cinnabon will help the brands accelerate ongoing efforts to become more accessible to guests by adding locations outside the traditional mall setting.

Starbucks entered into a strategic partnership with Alibaba's food delivery platform Ele. Me in China to expand its delivery services. This collaboration enhances Starbucks' reach in the Chinese market.

Cloud Kitchen Market Scope: Inquiry Before Buying

| Cloud Kitchen Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 34.69 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 14.13% | Market Size in 2030: | US $ 87.51 Bn. |

| Segments Covered: | by Type | Independent Cloud Kitchen Commissary/Shared Kitchen Kitchen Pods |

|

| by Product | Burger/Sandwich Pizza Pasta Chicken Seafood Mexican/Asian Food Others |

||

| by Nature | Franchised Standalone |

||

| by Deployment | Web Mobile |

||

Cloud Kitchen Market, by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Cloud Kitchen Key Players are:

1. Auntie Anne’s Franchisor SPV LLC

2. Domino’s Pizza, Inc.

3. CKE Restaurants Holdings, Inc.

4. Firehouse Restaurant Group, Inc.

5. Jack in the Box, Inc.

6. McDonald’s

7. Restaurant Brands International, Inc.

8. Yum Brands Inc.

9. Inspire Brands, Inc.

10. Innobliss Solutions Private Limited

11. Kitchen United

12. Rebel Foods

13. Doordash Kitchen

14. Zuul Kitchen

15. Keatz

16. Kitopi

17. Ghost Kitchen Orlando

18. Dahmakan

19. Starbucks

Frequently Asked Questions:

1] What is the growth rate of the Cloud Kitchen Market?

Ans. The Cloud Kitchen Market is growing at a significant rate over the forecast period.

2] Which region is expected to dominate the Cloud Kitchen Market?

Ans. North America region is expected to dominate the Cloud Kitchen Market over the forecast period.

3] What is the expected Cloud Kitchen Market size by 2030?

Ans. The market size of the Cloud Kitchen Market is expected to reach USD 87.51 Bn by 2030.

4] Who are the top players in the Cloud Kitchen Industry?

Ans. The major key players in the Cloud Kitchen Market from the GHOST KITCHEN ORLANDO, Kitopi, STARBUCKS (STAR KITCHEN), Rebel Food, Zomato, KEATZ, KITCHEN UNITED, ZUUL KITCHEN, DAHMAKAN, DOORDASH KITCHEN.

5] Which factors are expected to drive the Cloud Kitchen Market growth by 2030?

Ans. Rising Demand for Online Food Delivery and Cost Efficiency is a growing demand for market Cloud Kitchen market.