Carbon Fiber Prepreg Market Size by Resin Type, End-use Industry, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2034

Overview

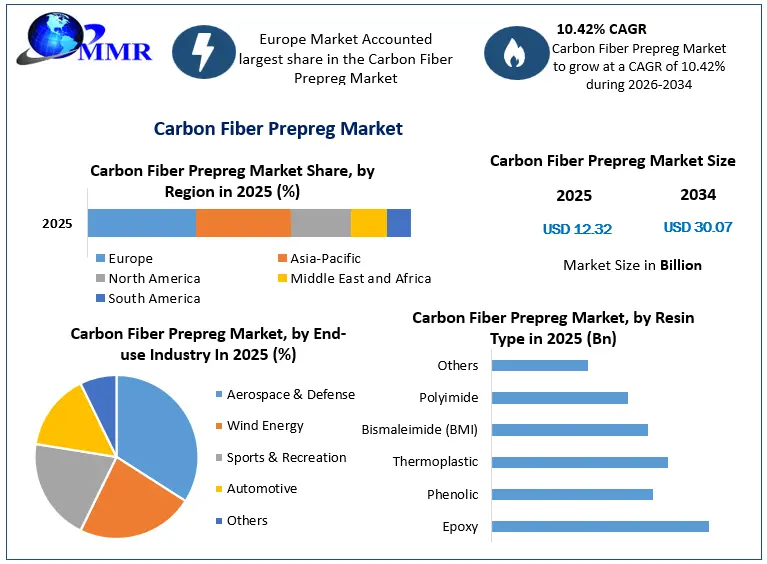

The Carbon Fiber Prepreg Market size was valued at USD 12.32 Billion in 2025 and the total Carbon Fiber Prepreg revenue is expected to grow at a CAGR of 10.42% from 2026 to 2034, reaching nearly USD 30.07 Billion.

Carbon Fiber Prepreg Market Overview:

In comparison to conventional prepregs, carbon fiber prepregs have superior performance and a host of benefits, including good weight reduction, a high strength-to-weight ratio, high tensile and compressive strengths, a low coefficient of thermal expansion, and high fatigue resistance. Rapidly shifting carbon fiber prepreg market dynamics and an increase in demand for lightweight and durable materials are likely to result in increasing demand for lightweight materials from major industries like aerospace and defense and automotive, which will likely open up new revenue opportunities for preggers in this product category and drive carbon fiber prepreg market.

In , a significant decline is expected in the market for carbon fiber prepreg. The short-term impact on the carbon fiber prepreg market is visible in the H1 results of the key players, which show a dramatic decline in sales, enormous losses, staff layoffs, cash burnouts, production halts, etc. However, the long-term view is still encouraging due to a slow recovery in the manufacturing of cars and airplanes, which will finally have a beneficial effect on the carbon fiber prepreg market.

Carbon prepreg accounts for almost 80% of the overall prepreg market. According to forecasts, the market will probably accelerate in the years to come, reaching an expected value of US$ 4.9 billion in . One of the factors contributing to the decline in manufacturing of composite-rich aircraft like the B787 and A350XWB is acting as one of the prime reasons behind the market’s delayed recuperation.

Carbon Fiber Prepreg Market Snapshot

To know about the Research Methodology:-Request Free Sample Report

Carbon Fiber Prepreg Market Dynamics:

The supply chain analysis of the Carbon Fiber Prepreg Market

Today, five major large-tow carbon fiber manufacturers mostly serve the restricted wind blade industry, with Zoltek being the leading supplier, In addition to Vestas and Gamesa, Zoltek now has about 44.1 million lbs of carbon fiber deployed in wind turbine blades globally (Wood ) and plans to have many more contracts with other large turbine manufacturers (Lucintel ). SGL Rotec, which the SGL Group sold to an unnamed investor in December, has been producing lighter-weight, thinner, and more stable rotor blades for offshore applications and low-wind environments by combining materials such as carbon fiber with semi-automatic milling technologies creating a huge demand for carbon fiber prepreg market.

Hexcel and the top three Japanese producers (Toray, Toho Tenax, and Mitsubishi Rayon), as well as their production capacity predictions. Toray's claim of 50,000 tonnes per year is particularly noteworthy since it almost equals the whole world's combined small- and large-tow CF production capacity in , and drives the carbon fiber prepreg market.

A closer look at Toray's supply chains indicates that they comprise finished CFRP component production in Japan, France, and Germany, as well as vertically integrated manufacturing from precursors to prepregs or final parts in Japan, France, and the United States. Toray also intends to build a new $1 billion plant on 400 acres in Spartanburg, South Carolina. These facilities will be vital to Toray's ability to fulfill important aerospace contracts, including a 15-year agreement signed with Airbus.

| CF Suppliers | Capacity (Tonnes/yr) | Prepreg | Customer |

| Toray | 18,900-50,000 | Tacoma, WA, US, Japan | Boeing 787 airbag |

| Toho Tenax | 15,100 -. 18,900 | Shizuoka, Japan | Bombardier CSeries, A380 |

| Mitsubishi Rayon | 10,600 -. 14,300 | Irvine, CA, United States | A380 |

| Hexcel | 7,250 -. 10,000 | US; Europe; Tianjin, China | Airbus A350, A380 |

| Cytec | 2,400 -. 6,000 | Tempe, AZ, US; Greenville, TX, United States | Bombardier, F-35, COMAC C919 |

The BMW i3 program, which is supplied with carbon fiber through a joint venture founded in 2009 between SGL and BMW (termed SGL Automotive Carbon Fibers and abbreviated ACF), is the most important of these supply networks. ACF produced the world's first carbon fiber. A factory geared to supplying fiber to the automobile sector. BMW just SGL Carbon SE, a carbon fiber company, plans to invest more than 100 million euros. ($137 million) to increase joint carbon fiber production from 3,000 to 6,000 tonnes per year. tonnes per year 33 The investment will allow the firms to increase manufacturing in Germany and elsewhere. the United States in response to increased demand for BMW's electric i3 and i8 vehicles.abd drive the carbon fiber prepreg market during the forecast period.

Crude oil is converted into propylene, then acrylonitrile, then polyacrylonitrile (PAN), and lastly spun into 50K tow precursor at Node 1 in Otake, Japan. Mitsubishi Rayon Corporation (MRC), situated in Japan, is responsible for all Node 1 processes. SGL will provide exclusively through a joint venture called Mitsubishi Rayon-SGL Precursor Ltd. Co. ACF's forerunner. Two PAN precursor spin plants, each with a capacity of 3,500 tonnes per year and with huge demand from the carbon fiber prepreg market also, have been installed. And drive the carbon fiber prepreg market in the automotive industry also, offer Node 1 a total annual capacity of 7,000 tonnes PAN precursor 34 Otake's ancestor, more details of each application and their carbon fiber prepreg supply chain are detailed and covered in the report.

Automotive OMEs and carbon fiber prepreg suppliers’ partnerships

| CF/CFRP supplier | OEM | Notes |

| SGL | BMW | Life cabin of i3 and i8 electric vehicles; BMW 18.4 % ownership stake in SGL |

| Toray-Plasan | GM | Body panels Corvette; Toray 20% ownership stake in Plasan |

| Toray-Plasan | Ford | Body panels Mustang; Toray 20% ownership stake in Plasan |

| Toray-Plasan | Chrysler | Body panels Viper; Toray 20% ownership stake in Plasan |

| SGL | Volkswagen | Volkswagen Group owns many of the luxury brands that were leaders in adopting CF for automotive applications; brands include Lamborghini, Porsche, Bentley, Bugatti, and Ducati. Volkswagen has 8% ownership stake in SGL. |

| Toho Tenax | GM | Investigating carbon fiber thermoplastic reinforced polymer manufacturing having a cycle time of less than one minute for high-volume part production |

| Dow AkSA | Ford | Investigating low-cost, high-production volume CFRP for automotive applications; Dow AkSA is a joint venture of Dow Chemical Company and the world’s largest producer of acrylic fiber, AkSA, based in Turkey. Carbon fiber production assets are located in Turkey |

| Toray | Daimler | Manufacturing and marketing of CFRP for automotive applications using a rapid RTM process |

| Toho Tenax | Toyota | Cabin and other components for Lexus LFA |

| Cytec | Jaguar Land Rover | Develop composite materials for high-volume serial automotive vehicles |

The fluctuating cost of Carbon fiber prepreg becoming more challenging for OMEs

The two most significant growth challenges are the high cost of carbon fiber production and the requirement for improved technology. Furthermore, it cannot be used in small manufacturing units because it requires a heat source and vacuum bagging at a low temperature during the molding process. Because prepreg is nonrecyclable after molding, it contributes to the pollution problem. Furthermore, the negative environmental repercussions of the resins used in production impede Carbon fiber prepreg market growth.

Carbon fiber composites are widely employed in industries such as aerospace, wind energy, automotive, industrial, marine, and oil & gas. Advanced carbon fiber composites are more costly than metals. The use of composites represents a "tradeoff between cost and performance." As a result, carbon composites have made an effect in high-performance vehicles such as jet fighters, spaceships, racing boats, and exotic sports automobiles. In , the global composites materials market was worth $288 million and was increasing at a rate of 15- 20% each year. This market will grow more if the cost of composites is decreased. The cost under consideration is essentially the cost of composite manufacture.

However, in order to provide an accurate estimate, the complete life cycle cost, including maintenance and operation, must be included. Composites offer a cost advantage, particularly in terms of operation and maintenance which form a sizable percentage of direct operating costs in the carbon fiber prepreg market

Carbon Fiber Prepreg Market Segment Analysis:

Based on Resin Type, the Carbon Fiber Prepreg Market is segmented into Epoxy, Phenolic, Thermoplastic, Bismaleimide (BMI), Polyimide, and Others. Epoxy is expected to dominate the carbon fiber prepreg market during the forecast period. Epoxy is highly in demand thanks to its extreme strength and lightweight, carbon fiber-reinforced polymer (CFRP) composites are utilized in a wide range of products, including vehicles, body armor, and sports equipment.

Drive the carbon fiber prepreg market. A poor interfacial connection with the polymeric matrix is caused by the integration of an untreated, pristine carbon fiber surface, which causes the catastrophic breakdown of the composite material. Because it tends to enhance surface area and has been used between the fiber and matrix, graphene oxide, a 2D macromolecule with various polar functional groups on the basal planes and edges, such as hydroxyl, carboxyl, and carbonyl, has helped to improve CFRP characteristics.

Carbon fiber-based polymer epoxy composites can play a significant role in the aerospace and automotive industries because they are ideal for applications that consider lightweight materials with exceptional mechanical performance, high stiffness, corrosion resistance, a low coefficient of thermal expansion, chemical resistance, and excellent electrical and thermal conductivity. The designed composite materials must be able to withstand temperature variations and unfavorable weather conditions, such as high winds and salinity in the ocean. In this situation, multifunctional composites could be very intriguing; thus, combining the excellent mechanical properties of CF/epoxy composites with additional embedded functionalities like temperature management, energy storage, and sensing properties would result in a technological advance in the usability of carbon-based composites and drive the carbon fiber prepreg market during the forecast period.

The possibility of devastation from the impact was widely known while designing aircraft and spacecraft. The use of CFRP composites is growing quickly as a way to reduce these effects; for example, an A-320 aircraft uses 21.5% composite material in its total weight, and a Boeing 787 and Airbus A350 use 50% CFRP in their total weight for various parts like the tail cone, center wing box, vertical and horizontal tails, and pressure bulkheads. However, due to their exceptional performance and superior strength-to-weight ratio, CFRP composites have also begun to be used in the field of military aircraft driving the carbon fiber prepreg market globally.

Based on the End-use Industry, the Carbon Fiber Prepreg Market is segmented into Aerospace & Defense, Wind Energy, Sports & Recreation, Automotive, and Others. The Aerospace & Defense industry held the largest market share in . For the majority of their existence, the carbon fiber (CF) and carbon fiber reinforced polymers (CFRP) industries have been primarily driven by aerospace projects. Despite the fact that the aerospace industry presently purchases less CF by weight than the industrial sector, mostly due to the increasing demand for carbon fiber prepreg market. The high cost per weight of CFRP elements for airplanes and spacecraft implies wind turbine blades. And drive the demand for the carbon fiber market.

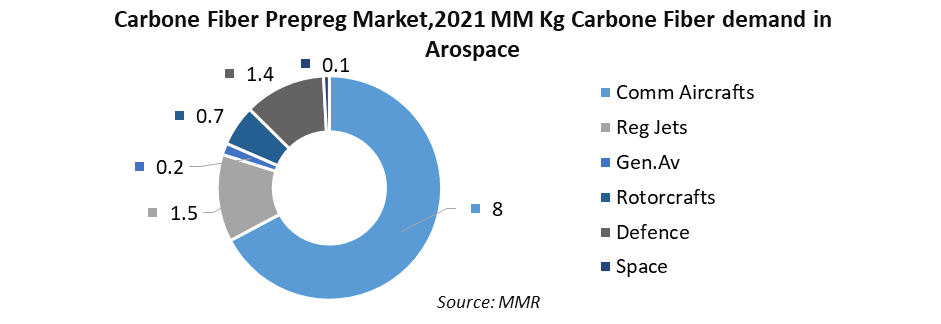

By , aerospace applications will still account for a sizable portion of the global carbon fiber prepreg market (about 65%) monetary worth. In , the aerospace sector generated roughly $700 billion in sales. The construction and sale of around 4,390 airplanes and rotorcraft contributed $152 billion of that sum to the aerospace industry's most visible product, aircraft. This needed production effort, as well as older craft upkeep, repair, and overhaul. Approximately 544,000 tonnes of raw materials the majority of which are CFRP composites 16,300 tonnes, or 3% of that total, were accounted for.

By , aerospace applications will still account for a sizable portion of the global carbon fiber prepreg market (about 65%) monetary worth. In , the aerospace sector generated roughly $700 billion in sales. The construction and sale of around 4,390 airplanes and rotorcraft contributed $152 billion of that sum to the aerospace industry's most visible product, aircraft. This needed production effort, as well as older craft upkeep, repair, and overhaul. Approximately 544,000 tonnes of raw materials the majority of which are CFRP composites 16,300 tonnes, or 3% of that total, were accounted for.

This provides a sizable source of demand given the scale of the entire carbon fiber prepreg market. Considering that Boeing and Airbus control the majority of the aerospace CF composites industry, it makes sense that Europe and North America would have the highest demand for the aerospace-grade Carbon fiber prepreg market. In fact, this is the situation right now, according to the forecast period. In , Europe accounted for 49% of the demand for aerospace CF, compared to 32% for the rest of the world.

North America In , these ratios are expected to remain the same, although demand quantities will change. estimated to be over 290% of the values. The geographic distribution of demand for and manufacturing capability of small-tow carbon fiber is typically required for aeronautical applications. Asia has the majority of the small-tow capacity, as is clear, and drives the carbon fiber prepreg market. More details about each region are detailed covered in the report.

Carbon Fiber Prepreg Market Regional Insights:

The Europe region dominated the market with a 49 % share in 2025. Europe now leads the globe in CF and CFRP demand, and this position is expected to be maintained. North American demand growth is expected to keep pace with Europe and outpace that of Asia and Japan. There is now excess production capacity, particularly in small-tow capacity and in North America and Asia, but recent estimates indicate strong demand growth in large-tow areas such as wind and automotive applications, necessitating capacity increases to satisfy demand. This opens up the possibility of export opportunities for North American producers. The requirement for a ready supply of precursor and carbon fiber, the unique nature of process technology, and U.S. export controls have resulted in an industry with extensive vertical integration, even across continents.

Thanks to its renewable energy goals and utilization of offshore wind power, Europe will continue to hold a large share of total global wind energy carbon fiber demand (about 65% in ). Although Zoltek is the principal manufacturer of carbon fiber used in wind turbine blades, firms in Taiwan, Japan, Germany, and others are participating in the supply chain for CFRP parts. As the wind industry tries to expand the size of turbines and blades for either onshore or offshore installations, performance concerns may overcome the present limiting factor for CF usage, cost. Europe is believed to be progressing faster on manufacturing procedures, owing to increased investment in R&D and technology.

Second, due to advantageous pricing and material availability, Korean enterprises are rapidly expanding and competing more effectively in nondedicated contract markets. Third, there are no domestic policies or tax incentives to manufacture carbon fiber composites. According to some global industry officials, the US sector benefits from "substantial" financial support for fiber and composite R&D, as well as vertical integration of key production companies. It is commonly expected that China would position itself to fill manufacturing gaps and compete effectively with the US industry.

Carbon Fiber Prepreg Market Recent Industry Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2026 | Toray Industries | Launched a new high-speed curing carbon fiber prepreg designed for automotive mass production. | Reduces cycle times by 40%, enabling wider adoption of lightweight composites in commercial vehicles. |

| 03 March 2026 | Hexcel Corporation | Opened a new automated prepreg manufacturing line at its facility in France. | Increases regional production capacity by 25% to meet rising demand from aerospace OEMs. |

| 12 May 2026 | Solvay | Formed a strategic partnership with a leading wind turbine manufacturer to supply recyclable thermoplastic prepregs. | Advances sustainability goals by offering a fully recyclable composite solution for offshore wind blades. |

| 22 June 2026 | Mitsubishi Chemical | Commercialized a cost-effective PAN-based carbon fiber prepreg optimized for industrial applications. | Lowers material costs by 15%, facilitating the transition from metal components to composites in heavy industry. |

Carbon Fiber Prepreg Market Scope: Inquire before buying

| Carbon Fiber Prepreg Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 12.32 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 10.42% | Market Size in 2034: | USD 30.07 Bn. |

| Segments Covered: | by Resin Type | Epoxy Phenolic Thermoplastic Bismaleimide (BMI) Polyimide Others |

|

| by End-use Industry | Aerospace & Defense Wind Energy Sports & Recreation Automotive Others |

||

Carbon Fiber Prepreg Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Carbon Fiber Prepreg Market Key Players

1. Mitsubishi Rayon Co. Ltd.

2. PRF Composite Materials

3. Barrday Corporation

4. GMS Composites

5. Hankuk Carbon

6. ABC Composites

7. Solvay

8. Teijin Limited

9. Park Electrochemical Corporation

10. Axiom Materials

11. Hc Composite

12. Kineco

13. Taiwan First Li-Bond Co., Ltd.

14. North Thin Ply Technology

15. TCR Composites

16. Toray Industries Inc.

17. Hexcel Corporation

18. Gurit Holding Ag

19. Royal Tencate N.V.

20. SGL Group

Frequently Asked Questions:

1] What segments are covered in the Global Carbon Fiber Prepreg Market report?

Ans. The segments covered in the Carbon Fiber Prepreg Market report are based on Product Type and End User.

2] Which region is expected to hold the highest share in the Global Carbon Fiber Prepreg Market?

Ans. The Europe region is expected to hold the highest share in the Carbon Fiber Prepreg Market.

3] What is the market size of the Global Carbon Fiber Prepreg Market by 2034?

Ans. The market size of the Carbon Fiber Prepreg Market by 2034 is expected to reach USD 30.07 Bn.

4] What is the forecast period for the Global Carbon Fiber Prepreg Market?

Ans. The forecast period for the Carbon Fiber Prepreg Market is 2026-2034.

5] What was the market size of the Global Carbon Fiber Prepreg Market in 2025?

Ans. The market size of the Carbon Fiber Prepreg Market in 2025 was valued at USD 12.32 Bn.