Caps & Closures Market by Raw Material, Type, Product Type, End-User, and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Forecast to 2032

Overview

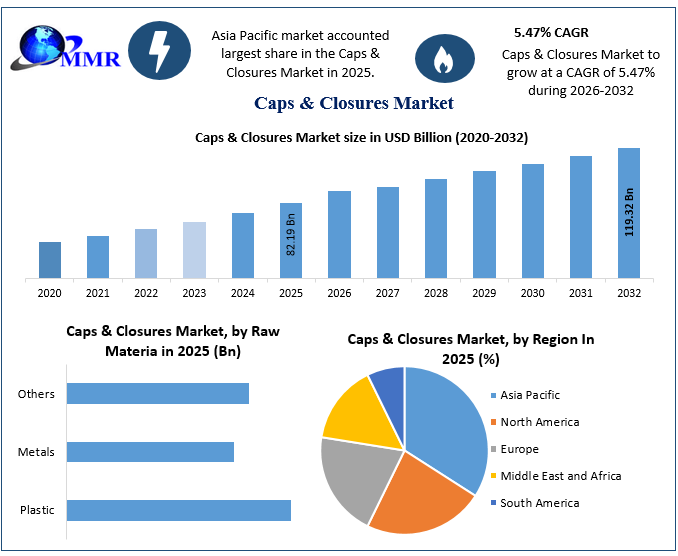

Global Caps & Closures Market was valued at USD 82.19 Billion in 2025, and it is projected to touch USD 119.32 Billion by 2032, exhibiting a CAGR of 5.47 % during the forecast period (2026-2032).

Caps & Closures Market Overview:

Caps and closures provide easy-to-open packaging, that help to achieve the ideal product packaging. With the use of effective caps and closures, customers can easily open and close a bottle, clamshell package, blister pack, or other types of packaging. There are various other reasons which are major drivers of caps and closures market other than accessibility, such as easy dispensing of products, improvement in the longevity of products, and protection from contamination and dirt. Increasing demand in the food and beverage sector and growing awareness of food safety fuels innovation in cap and closure solutions to extend product shelf life. The pharmaceutical industrial adherence to stringent regulatory requirements to propel the adoption of secure and tamper-proof closures for medical products.

The North America cups and closures market held the second-largest revenue share in 2023 and is expected to continue to grow at the fast CAGR over the forecast period. Silgan Holdings Inc. and Amcor PLC, two major cup and closure manufacturers, account for the majority of this region's market share

The market is also influenced by a growing focus on sustainability, with manufacturers exploring eco-friendly materials and designs to align with consumer preferences. Technological advancements, such as child-resistant closures and 3D printing, contribute to the dynamism of the market, positioning it for continued expansion to meet evolving industry needs globally. Regulatory mandates regarding food safety, product integrity, and environmental sustainability are driving manufacturers to adopt advanced caps and closures technologies.

This report gives a brief idea of the pricing strategies that key manufacturers of cups and closures in the in the market employ to gain the maximize market share, profitability, and competitive advantage. For instance, Closure Systems International, Inc., one of the leading manufacturers, employs skimming strategies to target early adopters and segments willing to pay a premium for advanced features and benefits.

For instance,

1. In 2023, Silgan Holdings Inc. leading worldwide manufacturer and supplier of speciality closures business had net sales of $2.2 billion (approximately 37.1 percent of their consolidated net sales) and EBIT of $281.0 million (approximately 45.2 percent of their consolidated EBIT excluding corporate expense).

2. In 2023, Amcor PLC manufacturer of caps and closures had net sales of USD 14,694 million, in line with the prior year and GAAP Net Income of USD 1,048 million and adjusted EBIT of USD 1,608 million

3. The Guala Closures Group is a global leader in the production of closures for spirits, wine, water, edible oil and a wide range of other beverages. In the first quarter 2024, the Group sold around 3.6 billion closures across its 3 product lines (safety, luxury, roll-on) and across 5 destination markets (spirits, wine, water, other non-alcoholic beverages, edible oil & condiments).

To Know About The Research Methodology :- Request Free Sample Report

To Know About The Research Methodology :- Request Free Sample Report

Global Caps & Closures Market Dynamics:

The Utilization of Biodegradable & Recyclable Plastics is a Developing Supportability Pattern

The increasing focus on sustainability is positively influencing the industry, with manufacturers looking at eco-friendly materials and plans that align with market preferences. Biodegradable caps and closures, for example, are constructed from materials that naturally degrade in the environment, such as synthetic plastics made from plants or biodegradable polymers. They can be treated in the soil or recycled after use, reducing their natural effect. Caps and closures, however, are made of recyclable materials such as aluminium or PET polymers that can be recycled alongside other residences and modern garbage.

Stringent environmental laws, particularly those defined by ISO standards, provide substantial challenges to the expansion of the caps and closures market. ISO regulations prioritize sustainability, requiring producers to limit environmental effect throughout the product's lifecycle, from raw material sourcing to end-of-life disposal. Compliance entails using recyclable materials, reducing carbon footprints, and ensuring that packaging is environmentally friendly. These tight standards can result in higher manufacturing costs and require investments in novel technology and procedures. While customers seek sustainable products, producers struggle to strike a balance between compliance, profitability, and market demand. As a result, companies in the caps and closures industry must proactively adapt to regulatory frameworks, incorporate sustainable practices into their operations, and innovate to fulfil environmental regulations as well as customer expectations for eco-friendly packaging solutions.

1. ISO 18604: Packaging Reuse: This standard focuses on packaging reuse, including reusable caps and closures. It provides guidelines for designing packaging that can be reused multiple times, which aligns with sustainability goals by reducing waste and resource consumption.

2. ISO 20380: Packaging Sustainability Optimization of the packaging system: This standard provides guidelines for optimizing the sustainability of packaging systems, including caps and closures. It covers aspects such as material selection, energy consumption, and environmental impact assessment, promoting the use of biodegradable and recyclable materials.

For instance, In October 2023, Berry Worldwide Inc. presented lightweight cylinder conclusion arrangements that are produced utilizing virgin plastics, including polyethylene (PE) and polypropylene (PP), and can also be made utilizing post-customer reused plastics (rPE and rPP) from Berry Worldwide Inc.'s. internal closed loop recycling facility.

Market Growth for Caps and Closures is Driven by an Upsurge in Consumer Demand for Packaged Food and Beverages as Urbanization Increases

The increasing demand for caps and closures is strongly linked to urbanization. Urban customers demand simple, fast packaging solutions for food and beverage items. Caps and closures are widely used in the beverage packaging industry since they help to preserve the freshness, flavour, and surface of refreshments. Recently, there has been an increase in the use of packaging options such as containers and pockets to extend the shelf life of beverages. Caps and closures play an important role in providing comfort by making products easy to open and close while preventing spillage. Caps and closures provide a resistant seal, preventing microorganisms from entering the object and keeping it fresh for longer. They address growing concerns about the safety and cleanliness of food and beverage goods by preventing breakdown. With a focus on sanitation and cleanliness, as well as an increase in demand for bundled items, the caps and closures business is likely to grow significantly. Manufacturers also provide a few customisation options that are more relevant to the product, assisting them in retaining customers and expanding their global market.

For instance,

1. In 2022, Tetra Pak introduced smart cap technologies for beverage packaging, integrating QR codes and NFC (Near Field Communication) capabilities. These smart caps enable consumer engagement, product traceability, and enhanced supply chain transparency.

2. Coca-Cola collaborated with Aptar, a global leader in dispensing systems and packaging solutions, to develop sustainable closures for beverage bottles. This collaboration focused on designing closures using recycled materials and enhancing recyclability. By integrating sustainable practices into closure manufacturing, Coca-Cola and Aptar aimed to reduce environmental impact and meet consumer expectations for eco-friendly packaging solutions.

The Availability of Alternatives to Packaging Methods Hinders the Expansion of the Caps & Closures Market

Plastic packaging substitutes such as pouches, blisters, and others offer several benefits, comprising flexibility, lightweight, and cost-efficiency, which are more preferred by consumers. These adaptable packaging options give distinctive branding, such as contoured pouches and blisters with custom graphics, allowing firms to stand out and boost brand identification. Rigid packaging solutions cost more to manufacture and transport than flexible packaging alternatives. The time-consuming and labour-intensive process of designing customized products, as opposed to other packaging methods, is a major obstruction to worldwide market growth.

Global Caps & Closures Market Segment Analysis:

Based on Raw Material type, caps & closures market is sub-segmented into Plastic, Metals and Others (glass, wood, rubber, elastomers and paperboard). Plastic segment held the largest revenue share in 2023 and is expected to continue to dominate the market in forecast period. Plastic material poses environmental concerns due to lower degradability as well as occurrence of CO2 emissions during its production. The trend of recycling is therefore emerging in manufacturing of caps and closures with numerous companies making use of recycled content as raw material to minimize dependence on virgin plastic. Metal is sustainable and durable as compared to plastic material and therefore has gained traction in the market. Metal closures are widely used for covering beverage glass bottles, metal cans of food products, as well as bottles of pharmaceuticals. The others segment contains materials, such as glass, cork, and rubber, which are gaining popularity as these offer robust sealing solutions as well as provide aesthetic appeal to packaging. Therefore, glass and corks or stoppers are used for wine bottles and for perfumery glass bottles that can retain perfume fragrance for a longer time.

For instance,

1. Menshen and Borealis AG launched 10 packaging closures in September 2020, which are manufactured using 50% PCR polypropylene. These are intended to be used for laundry and home care products.

2. BERICAP, a leading manufacturer of plastic closures, launched child-resistant closures (CRC) for pharmaceutical and certain beverage products. This innovation demonstrated BERICAP’s commitment to product safety and compliance, influencing adoption in relevant industries.

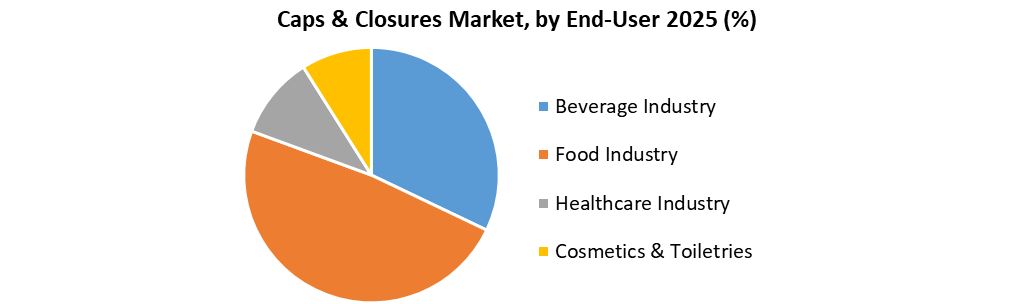

Based on the Application, the market is further classified by application into beverage, food, healthcare, cosmetics & toiletries, and others. Beverage packaging is a significant end-use industry for caps & closures. Drink packaging fills in as a vehicle for expanding time span of usability while keeping up with the taste and surface of the drinks. Pockets and containers are turning out to be progressively famous packaging choices in the drink business. The demand for focus on segregated closures from major beverage companies throughout the world is driving the market for premium caps in the beverage industry. There are different caps & closures that can be utilized to seal or pack non-alcoholic drinks, such as energy and sports drinks, probiotic drinks, meal replacements, and leafy food-based drinks in glass and plastic jugs, will help promote caps and closures demand.

The rising utilization of packaged food items, Prepared To-Eat (RTE) dinners, and in a hurry snacks is supposed to fuel class development all through the forecast period. Besides, in the medical care industry, caps & closures are utilized to seal jugs and jars containing meds, nutrients, saline jugs, and antibody vials, in addition to other things. Developing interest in senior-friendly and child-safe terminations that reduce the risk of accidental over the counter (OTC) drug use by infants and children will certainly increase demand in caps and closures in this section.

For Instance,

1. In 2022, Reynolds Group Holdings, parent company of Reynolds Consumer Products, acquired Closure Systems International (CSI), a leading global manufacturer of plastic closures for beverages, food, and personal care products. The acquisition allowed Reynolds Group to expand its portfolio in closures and packaging solutions, leveraging CSI’s expertise in innovative closure designs and technologies. This strategic move aimed to strengthen market position and offer enhanced closure solutions to customers globally.

2. In 2024, Nestle Waters launched smart packaging solutions featuring NFC (Near Field Communication) technology integrated into beverage caps.

Global Caps & Closures Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 11 February 2025 | European Parliament / Council | The EU Packaging and Packaging Waste Regulation (PPWR) officially entered into force, updating rules across member states to reduce packaging waste and mandate full recyclability. | The law applies starting August 2026, driving massive regional market demand for mono-material and waste-reducing closure systems ahead of 2030 sustainability milestones. |

| 11 August 2025 | BERICAP | The company announced the full industrial availability of its easyconnect cap solution, an innovative closed transfer system (CTS) developed for the European agricultural sector. | The product milestone establishes localized compliance in the Netherlands and Denmark by 2026, providing operators with drip-free, contamination-free liquid chemical transfer. |

| 19 November 2025 | Wisecap Group / Corvaglia Group | Both companies formed a strategic industrial partnership, integrating Corvaglia's cap manufacturing activities in Switzerland into Wisecap's broad European production network. | The transaction strengthens collective innovation by combining Corvaglia's injection-molding technology with Wisecap's industrial scale, expanding their product portfolio of beverage closures across the EMEA region. |

| 09 April 2026 | Amcor Plc | The company unveiled its next-generation 55 mm Flava Flip Top Closure (38/400 neck finish) designed specifically for the sauce and condiment market. | The mono-material cap achieves an 18.7% absolute weight reduction (saving 1.9g) to optimize recycle-readiness and help brand owners reach aggressive carbon reduction targets. |

Global Caps & Closures Market Regional Analysis:

Asia Pacific caps and closures market held the largest revenue share in 2023. The existence of extremely populated countries, such as China and India, combined with the growing food & beverage industry is projected to drive the regional market. Likewise, growing demand for cosmetics and home care products from countries, such as Japan and South Korea, is projected to boost caps and closures depletion. In North America, increased drinking of alcoholic and non-alcoholic beverages in countries, such as the U.S. and Canada are prompting demand for caps and closures in the beverage industry. The introduction of new types of beverages in the region is projected to further fast-track demand for its packaging products.

For instance,

1. In February 2022, Starbucks Coffee Company collaborated with PepsiCo to launch an energy drink known as Baya. The energy drink is available in three flavours, namely pineapple passion fruit, raspberry lime, and mango guava. This positive outlook for the beverage industry is anticipated to stimulate market growth during the forecast period.

2. In 2023, Amcor launched eco-friendly caps and closures made from recyclable materials across various markets in the Asia Pacific region. This initiative aimed to meet growing consumer and regulatory demands for sustainable packaging solutions. Amcor’s sustainable caps and closures contributed to reducing environmental impact and promoting circular economy practices in the region.

3. In 2024, Huhtamaki, a global packaging solutions provider, acquired a local closure manufacturer in Southeast Asia. This acquisition strengthened Huhtamaki’s presence in the Asia Pacific market for caps and closures. It enabled the company to expand its product portfolio and manufacturing capabilities, catering to increasing demand from the food and beverage industry in the region.

Competitive Analysis of Global Caps & Closures Market:

The competitive landscape of the cap and closure market is characterized by the presence of key companies aiming for market leadership. Regional and niche manufacturers contribute to the industry by providing specialized closure solutions. Collaborations and partnerships are frequent tactics for exchanging technological expertise and expanding into new markets. The market's dynamic nature stimulates ongoing innovation, guaranteeing that businesses can respond to changing customer needs, industry laws, and sustainability trends. Overall, the cap & closure market's competitive dynamics are shaped by a combination of global giants, regional competitors, and new innovators.

1. In July 2022, Guala Closures a global leading producer of closures for spirits, wines, beverages and oil bottles has reached an agreement to acquire Labrenta.

2. In February 2023, Berry Global Inc. introduced a comprehensive packaging solution specifically designed for pharmaceutical and herbal markets, targeting syrup and liquid medicines. This solution includes child-resistant and tamper-evident PET bottles and closures. The product range consists of seven different sizes, ranging from 20ml to 1l, all featuring a 28mm neck. Notably, certain bottles and closures within this range have undergone rigorous testing and certification processes, meeting child-resistant standards set by the EU's ISO8317 and US' 16CFR1700.20 regulations.

3. In January 2023, Aptar Pharma, part of AptarGroup, Inc., launched APF Futurity™, its first metal-free and highly recyclable, multidose nasal spray pump developed to deliver nasal saline and other comparable over-the-counter (OTC) formulations.

4. In March 2023, UNITED CAPS Launched 23 H-PAK, a new cap for carton packaging. The company's latest innovation 23 H-PAK is tethered to outstanding value and performance instead of expensive line changes.

5. In October 2021, Silgan Holdings has acquired Easytech Closures S.p.A. which manufactures and sells easy-open and sanitary metal ends used with metal containers primarily for food applications in Europe.

Caps & Closures Market Scope: Inquire before buying

| Global Caps & Closures Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 82.19 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 5.47% | Market Size in 2032: | US $ 119.32 Bn. |

| Segments Covered: | by Raw Material | Plastic Metals Others |

|

| by Type | Plastic Caps & Closures Metal Caps & Closures Other Caps & Closures |

||

| by Product Type | Easy-Open Can End Metal Lug Closures Peel-Off Foils Screw Closures Metal Crowns Corks Others |

||

| by End-User | Beverage Industry Food Industry Healthcare Industry Cosmetics & Toiletries Others |

||

Global Caps & Closures Market, by Region:

North America (United States, Canada, Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (India, China, Japan, South Korea, Australia, ASEAN, and Rest of APAC)

Middle East and Africa (South Africa, GACC, Egypt, Nigeria, and Rest of ME & A)

South America (Brazil, Argentina, Columbia, and Rest of South America)

Global Caps and Closures Market, Key Manufactures:

1. Silgan Holdings Inc. (US)

2. Plastics Corporation,

3. Crown Holdings Incorporation (US)

4. Reynolds Group Holdings, (US)

5. Aptar Group Incorporated (US)

6. Pact Group Holdings.

7. Alpha packaging

8. Berry Global Inc. (US)

9. Amcor Limited Plc (Australia)

10. BERICARP Holding GmbH (Germany)

11. Guala Closures S.P.A (Italy)

12. RPC Group PLC (UK)

13. Rexam PLC (UK)

14. United Caps (Luxembourg)

15. Nippon Closures Co. Ltd. (Japan)

16. Mold-Rite Plastics LLC (US)

17. O.Berk Company, LLC (US)

18. Pelliconi & C. Spa. (Italy)

19. Weener Plastics (Netherlands)

20. Blackhawk Molding Co. Inc. (US)

21. C.L. Smith Company (US)

22. Elmoris, Jsc (US)

Frequently Asked Questions:

1. Which region has the largest share in Global Caps & Closures Market?

Ans: Asia-Pacific Caps & Closures market held the largest share in 2025.

2. What is the growth rate of Global Caps & Closures Market?

Ans: The Global Caps & Closures Market is growing at a CAGR of 5.47% during forecasting period 2026-2032.

3. What is scope of the Global Caps & Closures market report?

Ans: Global Caps & Closures Market report helps with the PESTEL, PORTER, analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. What are the upcoming hot bets for the caps & closures market?

Ans: Rise in demand from caps and closures from emerging economics and growing demand for packaged food & beverage products.