Bunker Fuel Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

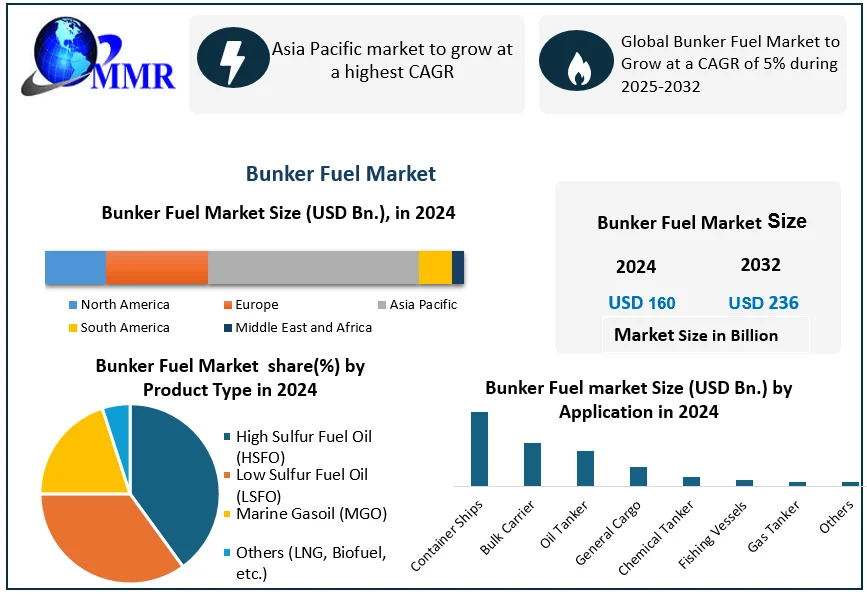

Global Bunker Fuel Market size was valued at USD 160 Bn. in 2024, and the total Bunker Fuel revenue is expected to grow by 5% from 2025 to 2032, reaching nearly USD 236 Bn.

Bunker Fuel Market Overview:

Bunker fuel, also known as marine fuel, refers to the heavy, residual fuel oil used by ships and large marine vessels for propulsion and auxiliary engines. It is primarily categorized into residual fuel oil (like IFO, HFO) and distillate fuel oil (like MGO, MDO).

The bunker fuel market encompasses the production, storage, trading, and supply of these fuels to the global shipping industry, which is vital for international trade. Availability of bunker fuel depends on global crude oil production and refining capacity, with major bunkering hubs located near busy ports such as Singapore, Rotterdam, Fujairah, and Houston. The market faces fluctuating supply and demand due to varying shipping activity, geopolitical tensions, and environmental regulations like IMO 2020, which mandate low-sulphur fuels, pushing demand toward cleaner marine gasoil and low-sulphur fuel oil.

Asia-Pacific dominates the bunker fuel market due to heavy maritime traffic and major ports in China, Singapore, and South Korea. Major key players include BP Marine, Royal Dutch Shell plc, ExxonMobil Corporation, TotalEnergies SE, and Chevron Corporation. End users mainly consist of container ships, bulk carriers, oil tankers, and general cargo ships, with container ships contributing the largest share due to the high volume of global trade. The market is rapidly evolving with a shift toward LNG bunkering and alternative fuels to meet decarbonization goals, driving technological advancements and cleaner fuel adoption worldwide. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Bunker Fuel Market Dynamics

Escalating Maritime Trade and Seaborne Tourism Fueling to Drive Bunker Fuel Market Growth

One of the primary drivers for the Bunker Fuel Market is the continuous growth of global maritime trade. As international shipping remains the backbone of global commerce, the increased movement of commodities and goods boosts the demand for bunker fuel, which powers commercial fleets worldwide. Additionally, the expanding cruise tourism industry further propels bunker fuel consumption, as cruise liners and passenger vessels require significant fuel volumes for long voyages, luxurious onboard facilities, and uninterrupted operations.

Industrialization in Emerging Economies to Create Bunker Fuel Market Opportunity

Economic development and rapid industrialization in emerging economies present lucrative opportunities for the bunker fuel market. Growth in export-import activities, industrial output, and infrastructural development drive shipping demands in regions such as Asia-Pacific, the Middle East, and Africa. This industrial surge necessitates reliable maritime transport, thereby expanding the need for bunker fuel. Moreover, the globalization of supply chains ensures that efficient, large-scale shipping solutions remain critical, reinforcing market opportunities in developing markets.

Technological Shifts and Energy Transition Impacting Traditional Demand to Create Bunker Fuel Market Challenge

Technological advancements in vessel design and propulsion systems aim to enhance energy efficiency and lower emissions, presenting a challenge to traditional bunker fuel consumption. As ships become more fuel-efficient and the maritime sector increasingly explores LNG, biofuels, and alternative energy sources to comply with stricter emissions norms, the market faces pressure to adapt. This shift requires industry players to invest in cleaner fuel technologies and innovative distribution solutions to maintain competitiveness.

Stringent Environmental Regulations and Oil Price Volatility to Create Restraint for Bunker Fuel Market

Stringent global environmental regulations, including IMO 2020 and upcoming decarbonization targets, constrain the use of high-sulfur fuels and force ship operators to either switch to low-sulfur alternatives or invest in expensive emission control technologies like scrubbers. This regulatory push increases compliance costs and affects profit margins. Additionally, bunker fuel prices remain closely tied to global crude oil price volatility, exposing market players to unpredictable operational costs and profit uncertainties, which can deter investments and complicate long-term planning.

Bunker Fuel Market Segment Analysis

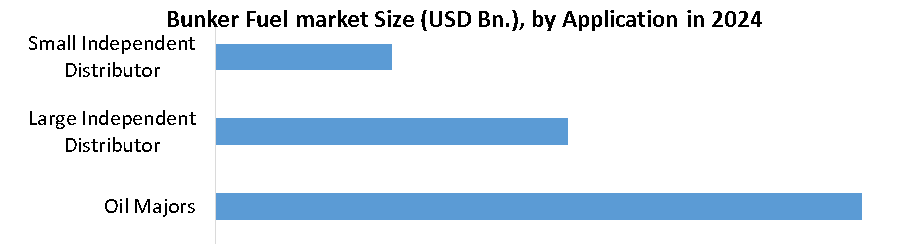

Based on Commercial Distributor, Oil majors maintain a dominant position in the Bunker Fuel Market, leveraging their extensive infrastructure and global presence. These companies offer a wide spectrum of bunker fuel types, providing comprehensive solutions to meet the diverse needs of shipping companies globally. Large independent distributors have expanded their market share, providing a competitive alternative to oil majors. They often concentrate on specific regions or markets, providing flexibility and customized services to cater to the evolving demands of shipping companies. Small independent distributors play a crucial role in serving local markets and niche segments with their specialized knowledge. Their agility and ability to provide personalized services make them essential for certain regions or specialized shipping operations.

Based on Type, historically, HSFO has held a substantial share in the Bunker Fuel Market, but its dominance is diminishing due to environmental regulations favouring lower Sulphur alternatives. The segment is currently undergoing a significant decline, driven by the International Maritime Organization's (IMO) regulations mandating a reduction in Sulphur content, leading to a shift towards low Sulphur alternatives. LSFO has emerged as a dominant segment propelled by environmental concerns and stringent regulatory requirements. The increasing adoption of LSFO is fuelled by the imperative for regulatory compliance, meeting the Sulphur content limits set by the IMO. This positions LSFO as a major player in the transitioning bunker fuel market.

MGO, with its lower Sulphur content compared to HSFO, occupies a niche market catering primarily to vessels preferring cleaner fuels. Its popularity is pronounced in regions with stricter emission standards, positioning MGO as a key player in specific geographical areas or for vessels with stringent emission requirements. The other category introduces a diverse range of specialty fuels and blends tailored to specific vessel requirements or market niches. Ongoing research and development activities play a pivotal role in introducing innovative fuel types within this category, addressing specific needs and compliance requirements.

Bunker Fuel Market Regional Analysis

Asia-Pacific — The Leading Hub for Bunker Fuel Demand

Asia-Pacific is the undisputed leader in the bunker fuel market, commanding over 50% of the global share. This dominance stems from the region’s position as the core of global manufacturing and export activities, fuelling massive maritime trade volumes. Major ports like Singapore (the world’s largest bunkering port), Shanghai, Hong Kong, and Busan act as vital refuelling hubs for thousands of container ships, bulk carriers, and tankers traversing major sea routes such as the Strait of Malacca and the South China Sea. Rapid industrialization, the rise of emerging economies like China and India, and strong regional infrastructure investments continue to drive bunker fuel consumption, reinforcing Asia-Pacific as the primary growth engine for the market.

Europe — Strong Regulatory Push Toward Cleaner Fuels

Europe accounts for approximately 24% of the market. The region is anchored by major ports including Rotterdam, Antwerp, and Gibraltar, serving busy North Sea and Atlantic trade routes. European dominance is also shaped by stringent environmental policies, such as the European Union’s push for carbon-neutral shipping and emission control areas (ECAs) in the Baltic and North Seas. This regulatory framework accelerates the shift from traditional high-sulphur bunker fuels to cleaner alternatives like low-sulphur fuel oil (LSFO), marine gasoil (MGO), and LNG bunkering, transforming Europe into a key adopter of sustainable marine fuel solutions.

Bunker Fuel Market Competitive Landscape

The bunker fuel market in 2025 is highly competitive and dominated by major global oil companies, integrated energy firms, and large independent bunker suppliers that ensure consistent supply and compliance with evolving marine fuel standards. Leading players such as BP Marine, Royal Dutch Shell plc, ExxonMobil Corporation, Chevron Corporation, and TotalEnergies SE hold significant market shares due to their extensive global bunkering infrastructure, robust supply chains, and investments in low-sulphur and alternative fuels to meet IMO 2020 and decarbonization targets. Large independent distributors like World Fuel Services Corporation, Bunker Holding A/S, and PetroChina International compete aggressively by offering flexible pricing, regional expertise, and value-added services such as fuel quality testing and digital bunkering solutions.

The competitive landscape is witnessing strategic alliances, mergers, and sustainability-driven innovation, with many suppliers expanding their portfolios to include LNG bunkering, biofuels, and carbon offset solutions to address stringent environmental norms. The Asia-Pacific region remains the most competitive market due to intense port traffic in Singapore, China, and South Korea, while Europe and North America focus strongly on transitioning to greener marine fuels. Players that effectively balance cost-efficiency, regulatory compliance, and technological advancements are expected to maintain a competitive edge in this evolving industry landscape.

Bunker Fuel Market Recent Development

• April 2024: Oman, TotalEnergies

Development: TotalEnergies formed a joint venture with the Oman National Oil Company to supply liquefied natural gas (LNG) as a marine fuel through Marsa LNG Gas, covering upstream gas production and downstream liquefaction, with production expected to start in Q1 2028.

• May 2024: Singapore, NYK Line

Development: NYK Line collaborated with the Global Centre for Maritime Decarbonization for a six-month project to trial a marine biofuel blend (24% fatty acid methyl esters and very low sulphur fuel oil) on a short-sea vehicle carrier, stopping at various ports.

• April 2024: Georgia, USA, JAX LNG and Seaside LNG

Development: JAX LNG and Seaside LNG conducted the inaugural liquefied natural gas (LNG) bunkering operation in the Port of Savannah, supplying fuel to CMA CGM’s SYMI vessel at the Garden City Terminal.

Bunker Fuel Market Key Trends

• Shift to Low-Sulphur Fuels

Driven by IMO 2020 regulations mandating a 0.5% sulphur cap, the bunker fuel market in 2025 sees a significant shift toward very-low sulphur fuel oil (VLSFO) and marine gas oil (MGO) to reduce emissions, with VLSFO expected to witness substantial growth due to its compliance with environmental standards.

• Adoption of Alternative Fuels

Increasing environmental concerns and sustainability goals are boosting the adoption of liquefied natural gas (LNG) and biofuels, with initiatives like NYK Line's biofuel trials and TotalEnergies' LNG ventures in Oman reflecting the industry's move toward cleaner fuel solutions.

Bunker Fuel Markets Scope: Inquire before buying

| Global Bunker Fuel Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 160 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5 % | Market Size in 2032: | USD 236 Bn. |

| Segments Covered: | by Type | High Sulfur Fuel Oil Low Sulfur Fuel Oil Marine Gasoil Others |

|

| by Commercial Distributor | Oil Majors Large Independent Distributor Small Independent Distributor |

||

| by Application | Container Bulk Carrier Oil Tanker General Cargo Chemical Tanker Fishing Vessels Gas Tanker Others |

||

Bunker Fuel Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe), Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A), South America (Brazil, Argentina, Rest of South America)

Bunker Fuel Market Key Players are:

Major Global Key Players:

• Shell (Singapore)

• Bunker Holding A/S (Denmark)

Leading Key Players in North America:

• Aegean Marine Petroleum Network Inc. (United States)

• BP PLC (United Kingdom)

• World Fuel Services (United States)

• Exxon Mobil (United States)

Market Follower Key Players in Europe:

• Chemoil Energy Ltd. (United Kingdom)

• Gazprom Neft PJSC (Russia)

• AC Bunker Fuels Ltd. (United Kingdom)

• KPI Bridge Oil A/S (Denmark)

• Royal Dutch Shell PLC (Netherlands)

• Total Marine Fuel (France)

• Bright Oil (United Kingdom)

• Lukoil-Bunker (Russia)

• Alliance Oil Company (Sweden)

Prominent Key Player Asia Pacific:

• Bomin Bunker Oil Corp. (Singapore)

• China Marine Bunker (China)

• Bunker Holding (Singapore)

• Sinopec (China)

• GAC (United Arab Emirates)

• China Changjiang Bunke (China)

• Southern Pec (Singapore)

• Shanghai Lonyer Fuels (China)

FAQ’s:

1. What is the Bunker Fuel Market?

Ans: The Bunker Fuel Market refers to the global industry involved in the production, distribution, and sale of fuel to power ships and vessels. It plays a crucial role in maritime transportation.

2. What types of fuels are used in the Bunker Fuel Market?

Ans: Common fuels include IFO 380, IFO 180, MGO, and MDO. IFO (Intermediate Fuel Oil) and MGO/MDO (Marine Gas Oil/Marine Diesel Oil) are primary choices for various vessels.

3. What drives the demand for bunker fuel?

Ans: Growing maritime trade, rising seaborne tourism, emerging economies, and the globalization of supply chains are key drivers fueling demand in the Bunker Fuel Market.

4. How does the market cope with environmental regulations?

Ans: Stringent environmental regulations pose challenges, requiring compliance with emission standards. This often involves costly fuel modifications or the adoption of alternative, cleaner fuels.

5. What impacts bunker fuel prices?

Ans: Bunker fuel prices are closely tied to crude oil prices. Volatility in oil prices can lead to unpredictable and increased operational costs for shipping companies.