Bullet Train or High Speed Rail Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

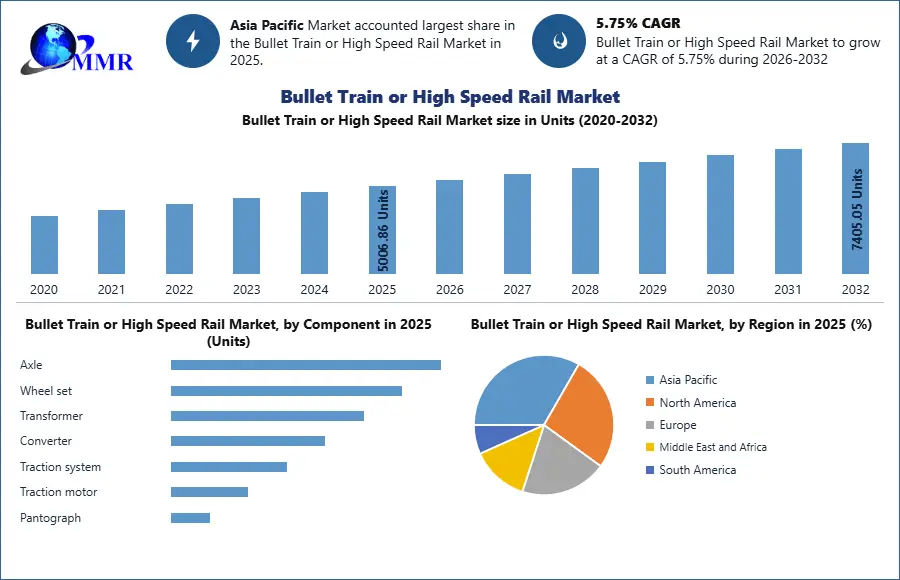

Global Bullet Train or High Speed Rail Market is expected to reach 7405.05 Units by 2032 from 5006.86 Units in 2025 at CAGR of 5.75%.

The report includes the analysis of impact of COVID-19 lock-down on the revenue of market leaders, followers, and disrupters. Since lock down was implemented differently in different regions and countries, impact of same is also different by regions and segments. The report has covered the current short term and long term impact on the market, same will help decision makers to prepare the outline for short term and long term strategies for companies by region.

To know about the Research Methodology :- Request Free Sample Report

Bullet Train or High Speed Rail Market, Dynamics:

Bullet train/High-speed rail market is an advanced railway transport that operates faster than traditional rail traffic. Worldwide, there is no single speed standard to term high-speed rail, new high speed train with speed of 250 kmph and above.

The report study has analyzed revenue impact of covid-19 pandemic on the sales revenue of market leaders, market followers and disrupters in the report and same is reflected in our analysis.

Rise in demand for bullet train/high-speed rail is largely, because of its accuracy and ability to cover large geographic distances in a short time. This is projected to be a major factor driving the bullet train/high-speed rail market throughout the forecast period. Growing government support across the world for incorporation of trains, as they are safe, economical, and a rapid means of transport, is anticipated to drive the bullet train/high-speed rail market during the forecast period. High-speed trains are projected to be operating in nearly 24 countries, such as France, Italy, Germany, Spain, China, Japan, , and the U.S., up from only 19 countries presently. Research across the globe has revealed that the number of countries incorporating the bullet train/high-speed rail is projected to approximately double over the next three years.

By technology, increasing demand for rapid mass transit to reduce traffic congestion is majorly responsible for the estimated growth of the wheel on rail technology. Moreover, the maglev technology is projected to record the fastest growth in the coming years for the bullet train/high-speed rail market. The high adoption rate of the maglev technology in the global bullet train/high-speed rail market is projected to make it the fastest growing segment.

Passenger segment led the bullet train/high speed rail market as compared to the freight segment, due to eco-friendly transport with high luxury and comfort. The passenger segment is expected to retain its dominant position in the market during the forecast period.

Bullet Train or High Speed Rail Market, Regional Analysis:

Region-wise, Asia Pacific is expected to be the xx % largest market share for global bullet train/high-speed rail. This can be generally attributed to the demand for high-speed trains for mass transit, thereby increasing the number of high-speed rail projects in the region.

The objective of the report is to present comprehensive analysis of Global Bullet Train or High Speed Rail Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of industry with dedicated study of key players that includes market leaders, followers and new entrants by region.

PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors by region on the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give clear futuristic view of the industry to the decision makers. The report also helps in understanding Global Bullet Train or High Speed Rail Market dynamics, structure by analyzing the market segments, and project the Global Market size. Clear representation of competitive analysis of key players by Global Bullet Train or High Speed Rail Type, price, financial position, product portfolio, growth strategies, and regional presence in the Global Bullet Train or High Speed Rail Market make the report investor’s guide.

Bullet Train or High Speed Rail Market, Key Highlights:

1. Global Bullet Train or High Speed Rail Market analysis and forecast, in terms of value.

2. Comprehensive study and analysis of market drivers, restraints and opportunities influencing the growth of the Global Market

3. Global Market segmentation on the basis of type, source, end-user, and region (country-wise) has been provided.

4. Global Bullet Train or High Speed Rail Market strategic analysis with respect to individual growth trends, future prospects along with the contribution of various sub-market stakeholders have been considered under the scope of study.

5. Global Bullet Train or High Speed Rail Market analysis and forecast for five major regions namely North America, Europe, Asia Pacific, the Middle East & Africa (MEA) and Latin America along with country-wise segmentation.

6. Profiles of key industry players, their strategic perspective, market positioning and analysis of core competencies are further profiled.

7. Competitive developments, investments, strategic expansion and competitive landscape of the key players operating in the Global Market are also profiled.

Scope of the Global Bullet Train or High Speed Rail Market: Inquire before buying

| Bullet Train or High Speed Rail Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 5006.86 Units |

| Forecast Period 2026-2032 CAGR: | 5.75% | Market Size in 2032: | 7405.05 Units |

| Segments Covered: | by Propulsion | Diesel Electric Dual power |

|

| by Speed | 200–299 km/h 300–399 km/h 400–499 km/h Above 500 km/h |

||

| by Application | Passenger Freight |

||

| by Technology | Wheel-on rail Maglev |

||

| by Component | Axle Wheel set Transformer Converter Traction system Traction motor Pantograph |

||

Bullet Train or High Speed Rail Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Bullet Train or High Speed Rail Market Key Players

1. RRC Corporation Limited

2. Alstom SA

3. Siemens AG

0. Hitachi Ltd.

5. Kawasaki Heavy Industries Ltd.

6. Hyundai Rotem Company

7. Talgo S.A.

8. Stadler Rail AG

9. Construcciones y Auxiliar de Ferrocarriles (CAF)

10.Mitsubishi Heavy Industries Ltd.

11.Wabtec Corporation

12.Thales Group

13.ABB Ltd.

14.Toshiba Corporation

15.Voith GmbH & Co. KGaA

16.Knorr-Bremse AG

17.Mitsubishi Electric Corporation

18.China Railway Construction Corporation (CRCC)

19.China Railway Group Limited

20.Larsen & Toubro Limited

21.Gammon India Limited

22.Bechtel Corporation

23.Bouygues Travaux Publics

24.East Japan Railway Company (JR East)

25.Central Japan Railway Company (JR Central)

26.SNCF Group

27.Deutsche Bahn AG

28.BEML Limited

29.Medha Servo Drives Pvt. Ltd.

Frequently Asked Questions:

1. Which region has the largest share in Global Bullet Train or High Speed Rail Market?

Ans: Asia Pacific region held the highest share in 2025.

2. What is the growth rate of Global Bullet Train or High Speed Rail Market?

Ans: The Global Market is growing at a CAGR of 5.75% during forecasting period 2026-2032.

3. What is scope of the Global Market report?

Ans: Global Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors& Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Market?

Ans: The important key players in the Global Market are – Denso Corporation, Hanon Systems, Sanden Holding Corporation, Mitsubishi Heavy Industries Ltd, MAHLE GmbH, Valeo SA, Keihin Corporation, Calsonic Kansei Corporation, SamvardhanaMotherson Group, Subros Limited, SMAC Auto Air, TransAir Manufacturing, Eberspacher Group, Marelli Corporation.

5. What is the study period of this Market?

Ans: The Global Market is studied from 2025 to 2032.