Bio-implant Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2030

Overview

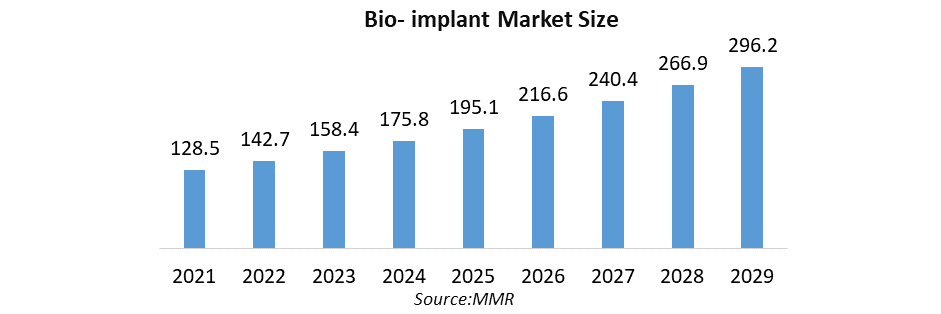

The Bio-implant Market size was valued at USD 158.31 Billion in 2023 and the total Bio-implant revenue is expected to grow at a CAGR of 11% from 2024 to 2030, reaching nearly USD 328.69 Billion.

Bio-implant Market Overview:

Bioimplants are bioengineered products used to restore the physiological function of a damaged biostructure. The approach entails replacing, supporting, or enhancing a missing, damaged, or existing biological structure. Growing occurrences of bone degradation in the geriatric population, rising demand for minimally invasive procedures, increasing prevalence of lifestyle disorders such as obesity, diabetes, and infections, and technological innovation in the healthcare industry are all expected to drive bio-implant market growth. Growing R&D efforts and aggressive strategies used by major competitors are propelling the bioimplants market forward. The increasing cost of bioimplant operations and the proper use of bioimplant goods to hamper Bio-implant market growth.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Continuous technical improvement in the manufacturing of bio-implants, such as 3D printing, increased government investment in the healthcare sector is likely to give the significant push to market growth during the forecast period.

An increasing development of healthcare infrastructure in both developed and emerging countries is driving the Bio-implants Market. The rising frequency of chronic conditions such as cardiovascular disease, osteoarthritis, and congenital and neuropathic disorders is a growing demand for biological implants. Globally, the aging population is steadily growing. A considerable portion of the elderly population requires dental implants, which increases the need for biological implants. Additionally, advancements in bioengineering technology and growing awareness of aesthetic implants are propelling the market forward.

Report Scope:

The report on Bio-implant provides a quantitative analysis of market size, price, M&A, demand, supply chain, investment and expansion plans by key competitors, and predictions. Porter's five forces study explains how buyers and suppliers build supplier-buyer networks and make profit-driven decisions. The present Bio-implant Market potential is assessed through detailed analysis and segmentation. The analysis will provide investors with a full insight into the industry's future, as well as the elements likely to affect the firm favorably or adversely.

The research offers a complete understanding of the market for those investors and current players in the industry. The study contains scenarios for the Bio-implant Market from the past and present, along with projected market numbers. The report's thorough analysis of important competitors, including market leaders, followers, and new entrants, covers every aspect of the market. The research contains strategic profiles of the top market participants, a full examination of their key competencies, and their company-specific plans for the introduction of new products, growth, partnerships, joint ventures, and acquisitions. With its clear portrayal of competitive analysis of significant companies by product, pricing, financial condition, product portfolio, growth strategies, and regional presence in the domestic as well as the local market, the research acts as an investor's guide.

Bio-implant Market Dynamics:

Global need for bio-implants

The growing use of bio-implant surgeries over arthroscopy and other therapeutic treatments such as physiotherapy is a significant driver driving the bio-implant market. This preference is ascribed to associated benefits such as increased success rates and biocompatibility. Other factors driving the market include increased incidence of cardiovascular diseases (CVD) and orthopedic disorders, a large senior population base, lifestyle changes, and rising acceptance of aesthetic operations. Rising awareness of aesthetic implants and improvements in bioengineering technologies are also driving the bio-implant market.

Non-surgical or minimally invasive bio-implants are becoming increasingly popular in a variety of medical fields. For example, a growing number of dental patients are opting for bio-implants as a less invasive and more successful alternative to root canal therapy. The alarming rise in oral healthcare issues drives even more demand for the bio-implants market. For example, the World Health Organization's 2016 Global Burden of Disease Study (GBDS) expected that oral disorders impacted about half of the global population. Dental caries and other tooth diseases were reported to afflict almost 3.58 billion people. In the foreseeable future, this will create a larger addressable market.

Growing elderly population is boosting the Bio-implant Market

Current market trends indicate that the elderly population will grow. The effects are more evident in nations with a high HDI, such as Korea and the United States. According to a recent US CDC estimate, the old and younger populations will equalize by 2036, with the former growing rapidly thereafter. Researchers think that the senior population, particularly those over the age of 65, is more likely to undergo hip replacement surgery, knee replacement surgery, shoulder replacement surgery, or spinal surgery.

Bio-implants are frequently utilized in orthopedic treatments, therefore this development helps the market. Hip fractures are among the most common catastrophic injuries among the elderly, necessitating immediate surgery and anesthesia. Patients spend several weeks in the hospital, resulting in 1.5 million hospital bed days used each year. According to NICE recommendations, surgery should be undertaken on the same day as hospital admission or the next day.

This is owing to the fact that being confined to a bed with a hip fracture is unpleasant, embarrassing, and stressful, and patients are unable to get out of bed until the procedure is over. As a result, the growing geriatric population is propelling the market for Bio-implant Market.

Osteoporosis and cardiovascular diseases are becoming more common

According to the World Health Organization (WHO), cardiovascular diseases (CVDs) be the main cause of death in 2023, killing an estimated 18 million people each year. CVDs include coronary heart disease, cerebrovascular disease, rheumatic heart disease, and various heart and blood vessel issues. Heart attacks and strokes cause for more than four out of every five CVD fatalities that necessitate surgery. According to the International Osteoporosis Foundation, osteoporosis cause more than 9 million fractures globally in 2020, with an osteoporosis fracture happening every three seconds. According to the World Health Organization, osteoporosis affects around 6.4 % of men over the age of 50 and 22.2 % of women in the same age range globally.

Based on the worldwide male and female populations, this might affect 500 million men and women. Osteoporosis is expected to affect 32 million persons aged 50 and up in Europe (European Union plus Switzerland and the United Kingdom) in 2019, accounting for 5.6 % of the overall European population aged 50 and up, or around 26.5 million women. An estimated 9.5 million new osteoporosis fractures were recorded in the year 2000, including 1.6 million hip fractures, 1.7 million forearm fractures, and 1.4 million clinical vertebral fractures.

Based on the worldwide male and female populations, this might affect 500 million men and women. Osteoporosis is expected to affect 32 million persons aged 50 and up in Europe (European Union plus Switzerland and the United Kingdom) in 2019, accounting for 5.6 % of the overall European population aged 50 and up, or around 26.5 million women. An estimated 9.5 million new osteoporosis fractures were recorded in the year 2000, including 1.6 million hip fractures, 1.7 million forearm fractures, and 1.4 million clinical vertebral fractures.

The majority of the remaining fractures were found in the Western Pacific and Southeast Asia, with Europe and the Americas accounting for 51% of all fractures. As a result, the increased frequency of osteoporosis and cardiovascular disorders is increasing the usage of implants, as most ailments need surgery. Owing to all of these reasons, the bio implant market is expected to grow.

Market Restraints

Bio-implant Caused Adverse Effects

Metal sensitivity is the most common form of immune reaction to implants. The most common metals used in orthopedic and dental implants are stainless steel (with nickel), cobalt, chromium, and titanium. Nitinol is utilized in the manufacture of cardiac stents and patches (an alloy of titanium and nickel). Metal allergies are becoming increasingly widespread in the general population as a result of increased metal exposure through piercings, jewelry, internal medical devices, and dental restorations. Medical implants frequently employ metal alloys such as nickel, cobalt, chromium, molybdenum, zirconium, and titanium.

Nickel, cobalt, and chromium sensitivity afflict up to 13% of the population; nickel allergy affects 17% of women and 3% of men, while 1-2% of the population is sensitive to cobalt, chromium, or both. Immunological reactions to medical implants, such as hypersensitivity to pacemakers or other cardiovascular devices, cranial endovascular stents and coils, dental implants, and orthopedic hardware, are commonly recorded in the literature (eg, joint replacement prostheses, fracture fixation devices, and pain-relief stimulators). When implants corrode or disintegrate, the immune system responds to surface changes and breakdown products.

According to Huber et al, the detection of corrosion products and a hypersensitive reaction in patients shows a relationship between corrosion and implant-related hypersensitivity. As a result, adverse effects caused by resorbable implants are stifling the market.

Bio-implant Market Opportunity

A sedentary lifestyle has been linked to a variety of chronic diseases, including CVD, congenital and neuropathic problems, and osteoarthritis. This has increased the demand for bio-implants throughout the world. According to the National Spinal Cord Injury Statistical Center, over 54.2% of the population in the United States suffered from a spinal cord injury in 2019. These occurrences are expected to affect over 60% of the US population by 2020, resulting in market growth potential.

Technological breakthroughs in bio-implant production, such as 3D printing, laser technology, and nanotechnology, have considerably improved these products' biocompatibility. These initiatives are bolstered by increased healthcare financing from governments throughout the world. Several government agencies are collaborating with healthcare research and manufacturing firms to bring novel and more effective products to market. For example, in June 2019, the Government of Kazakhstan indicated an interest in collaborating with MIDHANI, an Indian bio-implant producer, to commercialize titanium bio-implants.

Bio-implant Market Segment Analysis:

Based on Product, In terms of product, orthopedic implants had the largest market share in 2023. This can be ascribed to variables such as increased implant use in orthopedic procedures, an increase in the prevalence of orthopedic disorders, and advantageous reimbursement schemes implemented by various governments. According to the Centers for Disease Control and Prevention (CDC), about 54.4 million persons in the United States suffered from arthritis in 2020.

Dental implants, on the other hand, are expected to rise faster throughout the forecast period owing to reasons such as an aging population with more tooth abnormalities and increased demand for dental and aesthetic operations. In 2017, the American Academy of Implant Dentistry expected that more than 70.0% of Americans aged 35 to 44 had one missing tooth. Additionally, sedentary lifestyles and growing cigarette and nicotine intake are expected to exacerbate tooth problems in the forecast years. This has an effect on the total demand for bio-implants in the dentistry sector.

Bio-implant Market, by Product in 2023 (%)

Based on the Material, The biomaterial metal category grabbed the highest share of the bio-implant market in 2023 and is likely to retain its position during the forecast period. Advantages such as better tensile strength and corrosion resistance when compared to other materials such as ceramics and alloys are important development drivers for this category. Dental implants, joint replacement implants, and pacemaker cases are examples of biomaterial metal applications.

Based on the Material, The biomaterial metal category grabbed the highest share of the bio-implant market in 2023 and is likely to retain its position during the forecast period. Advantages such as better tensile strength and corrosion resistance when compared to other materials such as ceramics and alloys are important development drivers for this category. Dental implants, joint replacement implants, and pacemaker cases are examples of biomaterial metal applications.

Ceramic implants, on the other hand, are expected to develop at a rapid pace throughout the projection period. Ceramics have sparked a lot of attention, owing to their capacity to provide a crucial mechanical function for tissue repair. Additionally, bio-ceramics are expected to gain traction in the coming years due to their capacity to stimulate bone regeneration tissues.

Based on the Origin, In terms of origin, xenografts led the market in 2018, owing to their biological origin, which makes them more compatible with the human body. Allografts, on the other hand, is predicted to expand at a faster rate throughout the projection period. This is due to advantages such as a decreased risk of harvest site morbidity, less postoperative discomfort, and a shorter surgery and recuperation time. According to LifeLink Tissue Bank data from 2018, about 1.7 million allografts are implanted in the United States each year. These grafts are used in practically every surgical specialty, including orthopedics, gynecology, heart surgery, and neurology.

Bio-implant Market, by Origin in 2023 (%)

Based on the End-use, The market is divided into three segments based on end use: hospitals, clinics, and specialized centers. Hospitals dominated the market in 2018 and will continue to do so during the projected period. This is due to high patient traffic and favorable payment arrangements for pricey devices like pacemakers at government institutions. Clinics accounted for the second-highest revenue share in 2018 and will continue to rise steadily through 2026.

Based on the End-use, The market is divided into three segments based on end use: hospitals, clinics, and specialized centers. Hospitals dominated the market in 2018 and will continue to do so during the projected period. This is due to high patient traffic and favorable payment arrangements for pricey devices like pacemakers at government institutions. Clinics accounted for the second-highest revenue share in 2018 and will continue to rise steadily through 2026.

However, there has been a rising preference for specialty facilities in recent years for the treatment of numerous cardiac and orthopedic ailments. This can be linked to increased awareness of various ailments and treatment alternatives, as well as increased disposable money. Because these environments are tailored to specific medical diseases, these specialist facilities help to achieve the objective of improved clinical outcomes at lower costs. These factors are projected to drive the segment's growth throughout the forecast period.

Bio-implant Market, by End Use in 2023 (%)

Bio-implant Market Regional Insights:

Bio-implant Market Regional Insights:

North America dominated the Bio-Implants Market. North America is observed to have a considerable proportion of the bio-implants market and is expected to maintain this trend during the forecast period, with no noteworthy variations. The growing incidence of chronic illnesses and the availability of enhanced healthcare infrastructure are the primary factors driving the market growth.

According to Centers for Disease Control and Prevention (CDC) data updated in July 2022, coronary heart disease is the most frequent kind of heart disease, affecting roughly 21.1 million persons aged 20 and older in the United States. Moreover, according to CDC data, someone has a heart attack every 40 seconds, and about 815,000 people in the United States experience a heart attack each year. The growing prevalence of chronic illnesses is likely to drive up overall demand in the bio-implant market.

As a result of the aforementioned reasons, the market is likely to develop at a rapid pace during the forecast period. Additionally, increased product releases are likely to boost market growth throughout the projection period. For example, in June 2022, ZimVie received FDA clearance for the T3 pro tampered implant and Encode emergence healing augmentation in the United States.

Europe is the second biggest market for bio-implants, thanks to government funding and support, an increase in the prevalence of orthopedic illnesses, and increased R&D efforts. Many pacemaker manufacturers, for example, are focused on creating MRI-conditional and leadless pacemakers. Additionally, as the prevalence of CVD rises, so does the number of CVD procedures, fueling market expansion.

Asia Pacific is expected to be the fastest-growing market throughout the forecast period, owing to the increasing prevalence of spinal cord injuries. This might be ascribed to an alarming increase in the number of traffic accidents. According to a 2019 paper from Tokyo's Keio University, more than 100,000 individuals in Japan are paralyzed owing to spinal cord injury. However, the country's recent approval of iPS technology is likely to aid such patients in the future years, creating a new market potential for bio-implants. Thus, the aforementioned factors are expected to boost the market growth in this area during the forecast period.

Bio-implant Market Scope: Inquire before buying

| Bio-implant Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | USD 158.31 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 11% | Market Size in 2030: | USD 328.69 Bn. |

| Segments Covered: | by Product | Cardiovascular Implants Spinal implants Orthopedic Implants Dental Implants Ophthalmic Implants Other Implants |

|

| by Material | Ceramics Polymers Alloys Biomaterial Metal |

||

| by Origin | Autograft Allograft Xenograft Synthetic |

||

| by End-Use | Hospitals Clinics Specialty Centers |

||

Bio-implant Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Bio-implant Market, Key Players are

1. Abbott Laboratories (US)

2. Bausch & Lomb Incorporated (US)

3. BIOTRONIK Inc. (US)

4. Edwards Lifesciences Corporation (US)

5. LifeNet Health (US)

6. MiMeDX (US)

7. Arthrex, Inc (US)

8. Integra LifeSciences (US)

9. Medtronic (US)

10. Wright Medical Group N.V. (US)

11. Cook Group (US)

12. Induce Biologics (US).

13. Danaher Corporation (US)

14. Cardinal Health (US)

15. Zimmer Biomet (US)

16. Boston Scientific Corporation (US)

17. Stryker Corporation (US)

18. Endo International Plc (US)

19. Dentsply Sirona (US)

20. Johnson & Johnson Services, Inc. (US)

21. Invibio Ltd. (UK)

22. Smith & Nephew PLC (UK)

23. aap Implantate AG (Germany)

24. B. Braun Melsungen (Germany)

25. KLS Martin (Germany)

26. Alpha Bio Tec (Israel)

Frequently Asked Questions:

1] Which is the most preferred Bioimplant material?

Ans. Metal-based materials often outperform other materials in terms of strength and toughness. Because magnesium (Mg) and its alloys are inherently biocompatible materials with low density and excellent mechanical qualities, they have been studied for biomedical applications.

2] What is BioImplant?

Ans. The bio-implant is made out of a titanium screw covered in hydroxyapatite and encased in cell sheets generated from immortalized human periodontal cells. A tooth-extraction mouse model had bio-implants implanted into the upper first molar area.

3] What is the best material for teeth implants?

Ans. Titanium is the greatest dental implant material since it is biocompatible. This suggests it is correct and closely matches the human body. It may also merge with human bone. The two-piece device allows for a customized implant that addresses low bone deficits.

4] Which crown is best for implant?

Ans. Ceramics and porcelain have the most natural appearance, while gold is the most lasting form of crown available. Crowns are distinguished not just by the materials from which they are created. The manner in which a crown is affixed to an implant also makes a visible impact.

5] What type of crown lasts the longest?

Ans. Metal crowns are the least likely to crack or shatter, last the longest in terms of wear, and need just a minimal portion of your tooth to be removed. They are also resistant to biting and chewing pressures. The biggest disadvantage of this sort of crown is its shiny tint. Metal crowns are an excellent option for hidden molars.