B2B Mobility Sharing Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

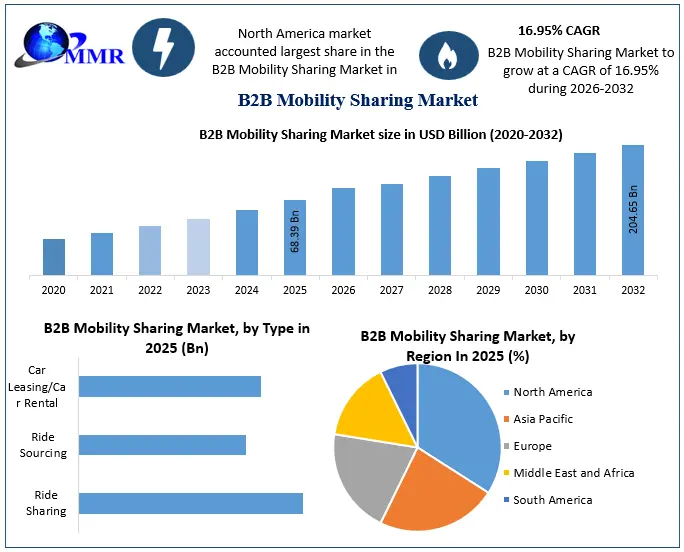

Global B2B Mobility Sharing Market size was valued at USD 68.39 Bn. in 2025, and the total Global B2B Mobility Sharing Market revenue is expected to grow by 16.95% from 2026 to 2032, reaching nearly USD 204.65 Bn.

The B2B mobility sharing market has emerged as a pivotal sector in modern urban transportation, offering diverse services such as ride-sourcing, car sharing, and micromobility. This market has seen exponential growth, driven by technological advancements, evolving consumer preferences, and substantial investments.

• According to MMR analysis, the global B2B mobility-sharing market is projected to reach significant revenue milestones, reflecting its robust expansion and adoption across various regions. Companies are continuously innovating to improve service efficiency and user experience, which in turn boosts market revenue and growth.

The extensive use of ride-sourcing services has created a significant demand for B2B mobility sharing in North America. The development of these services is aided by the region's sophisticated infrastructure as well as a high rate of smartphone and mobile internet usage. Market leaders Uber, Lyft, and Via are able to retain and increase their market share by taking use of large user populations and technical developments.

Qualitative data indicates that the rise of autonomous vehicles and AI-powered solutions is set to further transform the B2B mobility sharing landscape. These innovations promise to reduce operational costs and enhance service efficiency, driving higher profit margins. Additionally, environmental sustainability trends are pushing companies to adopt greener technologies, aligning with consumer demand for eco-friendly transportation options. Overall, the B2B mobility sharing market is poised for continued growth, supported by a dynamic ecosystem of technological innovation, consumer demand, and strategic investments.

To know about the Research Methodology :- Request Free Sample Report

B2B Mobility Sharing Market Dynamics

The Forces Steering Shared Mobility

B2B shared mobility has revolutionized urban transportation by providing a variety of options, including e-hailing, car sharing, and micro-mobility. E-hailing, where riders use a mobile app to book rides, dominates the marketplace with more than 40 million daily trips. This segment, led by companies like Uber and Lyft, showcases significant profit margins due to its high volume and efficient service models.

By optimizing routes depending on passenger pickups, dynamic shuttle services like Via increase operational effectiveness and profitability. The practice of pooling rides among strangers, or pooled e-hailing, lowers expenses and boosts efficiency, both of which support market growth. Car owners may now hire out their vehicles thanks to the growth of peer-to-peer car-sharing services like Turo, which increases asset utilization and opens up new revenue sources. This particular model not only meets a wide range of customer demands, but it also increases profit margins by reducing vehicle idle time.

• Shared micromobility options like Lime and Bird scooters and bicycles cater to short-distance travel, addressing the last-mile connectivity issue and contributing to market expansion. These services are particularly popular in densely populated urban areas, driving market growth through high usage rates.

Initiatives by the government

Almost every country's government cares about population growth, which have serious effects on ecosystems. Governments encourage individuals to use vehicles and other forms of transportation as little as possible. Furthermore, one of the administration's important ideas to encourage people to pick shared rides over personal trips is to share rides among families, relatives, and friends, which is expected to stimulate the expansion of the B2B Mobility Shared Industry. Consumers prefer affordable & luxury modes of transportation to individual driving. Furthermore, clients who previously rented a personal driver for their vehicle because it was more cost-effective have altered their preferences to using shared transportation. As a result, these initiatives are expected to propel the global B2B Mobility Shared Market forward over the forecast period. Alarmism about the environment and efficient modes of transportation is on the rise.

Challenges Facing Shared Mobility

Distinct regulatory obstacles frequently impede the growth and harmonization of services. A vulnerability exposed by the COVID-19 pandemic was the sharp decline in demand for shared transportation due to lockdowns and social isolation. Additional obstacles include consumer worries regarding data privacy, cleanliness, and safety. A lot of businesses are finding it difficult to turn a profit in the face of increasing operating expenses and competitive pressure, raising concerns about the financial viability of shared mobility models. Infrastructure investments, such as shared car parking spaces and dedicated lanes, are crucial but frequently underfunded, which hinders service effectiveness and adoption rates.

B2B Mobility Sharing Market Segment Analysis

Based on Type, according to MMR analysis, the ride-sourcing segment has been the largest B2B mobility-sharing market in 2025 and is expected to dominate during the forecast period, characterized by its substantial market share and rapid growth.

According to the International Transport Forum (ITF), ride sourcing services, such as those provided by Uber and Lyft, facilitate over 40 million trips daily worldwide. This high usage rate translates to significant profit margins and sustained market growth.

Ride sourcing optimizes routes, cuts down on wait times, and raises client happiness by utilizing cutting-edge algorithms and real-time data. The National Renewable Energy Laboratory (NREL) emphasizes that ride-sourcing platforms' success in the industry is a result of these efficiencies as well as their adaptable scalability. In addition, the U.S. Department of Transportation (DOT) states that the ride-sourcing industry has been growing steadily year over year due to rising urbanization and shifting customer preferences for on-demand and convenient transportation options. The leadership of this market is upheld by ongoing technical advancements and significant investments, guaranteeing its crucial position in urban mobility's future.

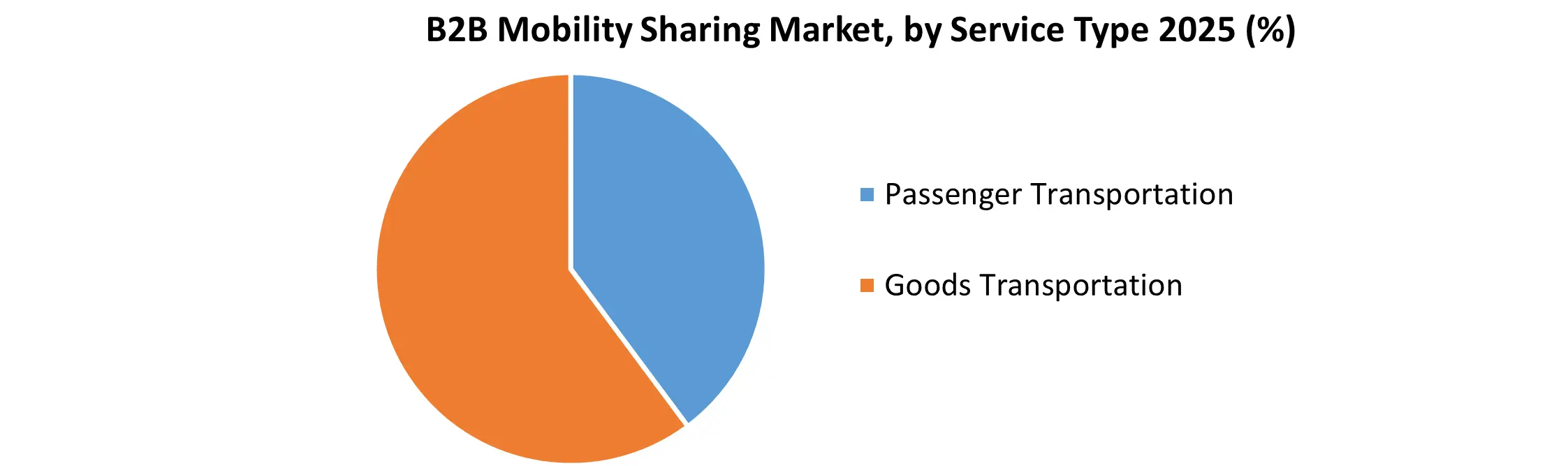

Based on service type, the Global B2B Mobility Sharing Market comprises goods transportation and passenger transportation. Among these, passenger transportation held the dominant share, accounting for 65% of the B2B Mobility Sharing Market. This dominance is primarily attributed to the growing demand for employee commute solutions, especially in urban and corporate hubs. Additionally, businesses are increasingly adopting shared mobility options to reduce operational costs, ease parking concerns, and support sustainability goals, making passenger transportation the preferred service type in the B2B mobility ecosystem.

Industry Development Factors:

As traffic congestion worsens, the market for shared mobility is gaining traction. According to an MMR Report study, travel times in Mexico Metropolis during peak traffic are 52 % higher in the year 2021, making this the most congested city in North America. Although this figure refers to extra average travel time during the day, traveling during peak evening hours takes 87 % longer on average. On the West Coast, Los Angeles and Vancouver are the most congested cities in the U.S & Canada, respectively. An increase in demand for ride-sharing services, along with a loss in parking space, is driving the industry. Car-sharing systems are used by businesses to commute their employees daily, decreasing fleet time and parking costs.

Furthermore, governments in Europe & North America have enacted strict pollution control regulations, incentives provided by the US government to use car-sharing, automobile manufacturers in Germany are increasing their investments in car sharing, and heavy traffic congestion and pollution in China are driving people to choose urban mobility. The absence of suitable public transit infrastructure in India, as well as shifting restrictions in Malaysia and Singapore, are important drivers of industry expansion. Furthermore, consumers are choosing ride-sharing due to lower travel costs. The industry is also being aided by an increase in the usage of vehicles equipped with modern technologies.

People can employ solutions that allow users to share a range of forms of transportation due to rising automobile ownership costs. Furthermore, solutions enable users to make real-time reservations, changes, and cancellations. Especially in growing economies such As India & Mexico, ride-hailing services are commonly used. Over the forecast timeline, a lack of knowledge regarding the benefits of such application services may stymie market expansion. Furthermore, in the case of ride-sharing, people are afraid to share their cars with strangers, resulting in a decline in the number of vehicles participating in the segment.

B2B Mobility Sharing Market Regional Overview:

The B2B Mobility Sharing Market is divided into 5 primary segments based on the geographical study. North America, Latin America, Europe, Asia Pacific, the Middle East, and Africa are among them. Because of strict environmental regulations, North America leads the B2B Mobility Sharing Market. The strong market share of North America throughout the world is due to a combination of high disposable income and a significant number of adopters in the region. In the worldwide B2B Mobility Sharing market, Europe is considered to be the second-largest market.

Poor connectivity and high costs connected with internet technology growth are also impeding the market from reaching its maximum potential in some low-income countries in the Middle East and Africa. Various government measures encouraging resource sharing are attempting to restructure the industry. The European Commission, for example, and government bodies like the Center on Regulatory in Europe (CERRE), have begun to offer incentives to vehicle owners to encourage the usage of these services. As a result, several factors have contributed to the market's growth in recent years and thus are anticipated to continue indefinitely.

The objective of the report is to present a comprehensive analysis of the Global B2B Mobility Sharing Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include Market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Global B2B Mobility Sharing Market dynamics, structure by analyzing the Market segments and projecting the Global B2B Mobility Sharing Market size. Clear representation of competitive analysis of key players by Service Type, price, financial position, Service Type portfolio, growth strategies, and regional presence in the Global B2B Mobility Sharing Market make the report investor’s guide.

B2B Mobility Sharing Market Scope: Inquiry Before Buying

| B2B Mobility Sharing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 68.39 USD Billion |

| Forecast Period 2026-2032 CAGR: | 16.95% | Market Size in 2032: | 204.65 USD Billion |

| Segments Covered: | by Type | Ride Sharing Ride Sourcing Car Leasing/Car Rental |

|

| by Service Type | Passenger Transportation Goods Transportation |

||

| by Business Model | Subscription-Based Pay-as-You-Go Corporate Contracts |

||

| by Vehicle Type | Passenger Vehicle Light Commercial Vehicle Heavy Commercial Vehicle Shuttles Buses/Coaches Others |

||

| by End-User | IT & Technology Manufacturing & Industrial Logistics & Transportation Retail & E-commerce Hospitality & Travel Healthcare & Life Sciences Government & Public Sector Others |

||

B2B Mobility Sharing Market by region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest)

South America (Brazil, Argetina and Rest of South America)

B2B Mobility Sharing Market Key Players

Uber Technologies Inc.

Lyft Inc.

Ola Cabs

Bolt Technology

FREE NOW

Grab Holdings

DiDi Global

Car Sharing & Corporate Fleet Platforms

Zipcar

Getaround

Free2move

Zoomcar

Drivezy

Leasing, Rental & Fleet Management (B2B Focus)

Enterprise Mobility

Hertz Global Holdings

Sixt SE

Ayvens

Arval

Orix Corporation

Kinto

MaaS (Mobility-as-a-Service) & Aggregators

SkedGo Pty Ltd

Moovit

Citymapper

Ridecell

Shuttle / Corporate Transport Specialists

Shuttl

Zeelo

Liftango

Swvl

Micro-mobility / Niche B2B Sharing

Vogo

Yulu

Tier Mobility

Others

Frequently Asked Questions:

1. Which region has the largest share in Global B2B Mobility Sharing Market?

Ans: North America region held the highest share in 2025.

2. What is the growth rate of Global B2B Mobility Sharing Market?

Ans: The Global B2B Mobility Sharing Market is growing at a CAGR of 16.95% during forecasting period 2026-2032.

3. What is scope of the Global B2B Mobility Sharing market report?

Ans: Global B2B Mobility Sharing Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global B2B Mobility Sharing market?

Ans: The important key players in the Global B2B Mobility Sharing Market are – Ola, Zipcar, DriveNow, Zoomcar, Car2go, ParkatmyHouse, Lyft, Sixt, Spinlister, Uber, Drivezy, Volercars, SKedGo Pty Ltd, Tanzer, Rapido, and Jenzabar.

5. What is the study period of B2B Mobility Sharing Market?

Ans: The Global B2B Mobility Sharing Market is studied from 2025 to 2032.