Autonomous Vehicle Market: by Application (Transportation, Defence, Civil), by Vehicle Type (Passenger, Commercial), by Propulsion Type (Semi & Fully Autonomous) - Forecast to 2030

Overview

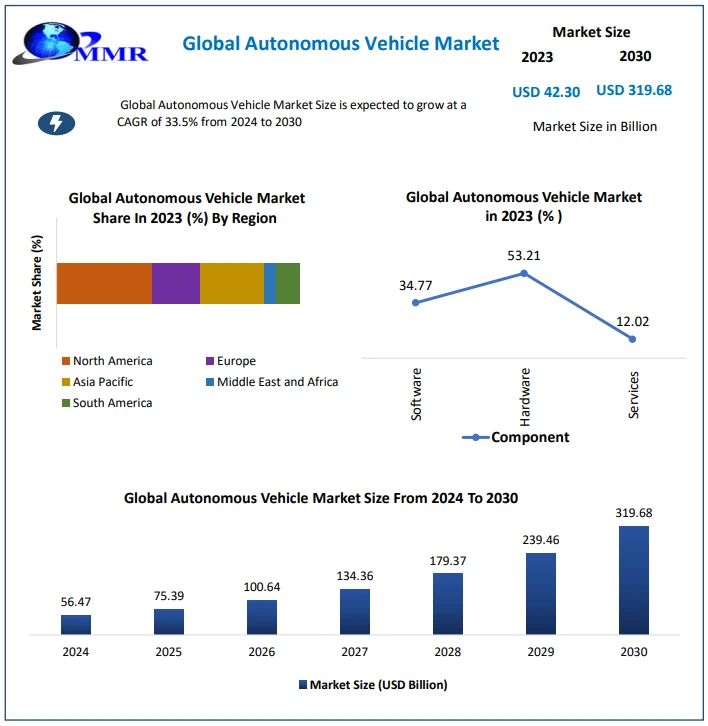

The Autonomous Vehicle Market size was valued at USD 42.30 billion in 2023 and the total Autonomous Vehicle Market Size is expected to grow at a CAGR of 33.5% from 2024 to 2030, reaching nearly USD 319.68 billion in 2030.

The Autonomous Vehicle Industry Overview:

Autonomous vehicles also commonly known as driverless or self-driving vehicles, are automobiles that require no human involvement for operating or controlling them. Automated vehicles have been generating significant attention and discussion, recently with almost every automobile company trying to develop their respective Autonomous vehicle concept and are successful in achieving some levels of autonomy and are planning to start production of driverless vehicles. The emergence of the new-age automotive industry with the onset of connected, Autonomous, shared, and electric vehicles, is expected to accelerate the growth of the sector, which has been moving at a slow year-on-year growth rate owing to a gradually decreasing rate of car sales. As companies attempt to expand their businesses across the new ancillary services for Autonomous vehicles, new players with innovative business models are also emerging.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The concept of self-driving cars, once considered science fiction, is rapidly Increasing Autonomous Vehicle Market. Consumers are increasingly intrigued by the convenience, safety, and potential cost savings offered by autonomous vehicles. With advancements in technology, vehicles are becoming more reliable, and capable of navigating complex traffic situations and adapting to various weather conditions. The market has also witnessed the emergence of innovative business models, such as ride-sharing and autonomous taxi services, which are transforming the traditional car ownership model.

Major automotive companies (Audi, BMW, Daimler, Ford, GM, Nissan, Toyota, Volkswagen, Volvo, etc.) and Vehicle Type companies (Google, Induct, etc.) have already demonstrated Autonomous driving through working prototypes and pilots. Several advanced driver assistance systems (ADAS) such as active lane keep assist, adaptive cruise control, and self-parking are already available as combined functions on current-generation cars. Additional functionality is expected to be rolled out in the Forecast Period. Furthermore, significant efforts are being made to advance existing Vehicle Types and to address cost-side challenges. Both the availability and affordability of key technologies to enable Autonomous driving are expected to greatly increase in the forecast Period.

1. Omniq, a company specializing in providing artificial intelligence-based solutions, has introduced an innovative in-car face detection feature capable of identifying and recognizing faces within a vehicle.

Autonomous Vehicle Market Dynamics:

Promoting Safety, Reducing Pollution, and Enhancing Infrastructure

The rise in the development of smart cities is a key factor driving the growth of Autonomous vehicles helps reduce air pollution in smart cities and also helps to fight climate change. Driverless vehicles decrease 90 % the chances of accidents, by significantly improving the safety of roads. Countries such as the United States, Canada, and Mexico, are deploying digital infrastructure to promote communication between vehicles and networks to collect essential information, thereby reducing traffic congestion and improving road safety. Government funding, supportive regulatory framework, and investment in digital infrastructure are pretended to positively drive the demand for Autonomous cars during the forecast period.

Integrating Computer Vision and Hybrid Technologies

The rapid progress in Autonomous Vehicle Type is being driven by the integration of advanced computer vision Vehicle Type, which incorporates next-generation sensors, cameras, and sometimes biometric algorithms for various purposes such as driver assistance, surveillance, and entertainment. Within the field of in-car imaging systems, a wide range of hardware and software components are at play, and there has been significant growth in the development of semiconductor devices that embed advanced computer vision models at the edge.

The rise of hybrid technologies used in traditional cars and trucks currently, along with the use of pure electric and hybrid electric technologies in future autonomous cars and trucks, would together assist in saving energy and increasing the efficiency of the drive. The sharing economy would also increase energy savings with the use of Autonomous cars and trucks.

Challenges Hindering the Growth of the Autonomous Car Market

The high cost of Autonomous vehicles, rising concern for security & safety, and lack of proper infrastructure to support automated vehicles in developing countries restrict the growth of the market. Ambiguous laws and regulations regarding the use of Autonomous cars are expected to restrain the growth of the global Autonomous car market during the forecast period.

The main pillars of Autonomous vehicles are policies and regulations, technological innovation, infrastructure, and adoption by customers. The self-driving vehicle is dependent on factors such as continuously maintained road infrastructure, road signs, and updated maps or navigation systems. In many developing countries such as India, Mexico, and Brazil, the road infrastructure is not as developed as compared to developed countries such as the U.S., Singapore, and Sweden, which are causing a hindrance in the development of Autonomous vehicles.

Autonomous Vehicle Market Segmentation:

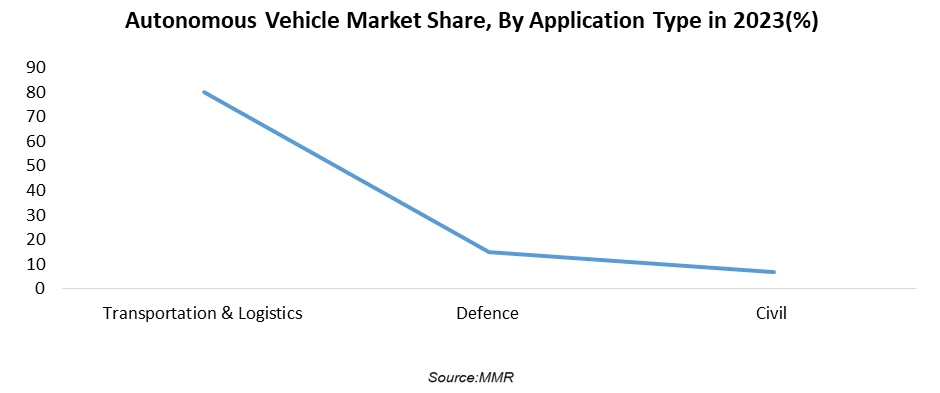

Based on Application, The Transportation and Logistics segment accounted for the largest market share in 2023 and is expected to grow with the highest CAGR of 17.4%% during the forecasted period. The rising adoption of electric and hybrid vehicles with various levels of automation has significantly triggered the demand for Autonomous vehicles in transportation applications. Public awareness and government support for shared mobility in the commercial sector have prominently boosted the trend of Autonomous vehicles in the segment. Autonomous vehicles have the potential to generate significant cost savings in transportation and logistics. By eliminating the need for human drivers, companies reduce labour costs associated with driver wages, benefits, and rest periods.

Companies in the transportation and logistics industry recognize the potential benefits of Autonomous vehicles in terms of cost savings, efficiency, and improved customer satisfaction. Consequently, there is a race among companies to develop and deploy Autonomous vehicle solutions to stay ahead of the competition and meet customers’ evolving demands.

Autonomous Vehicle Market Regional Insight:

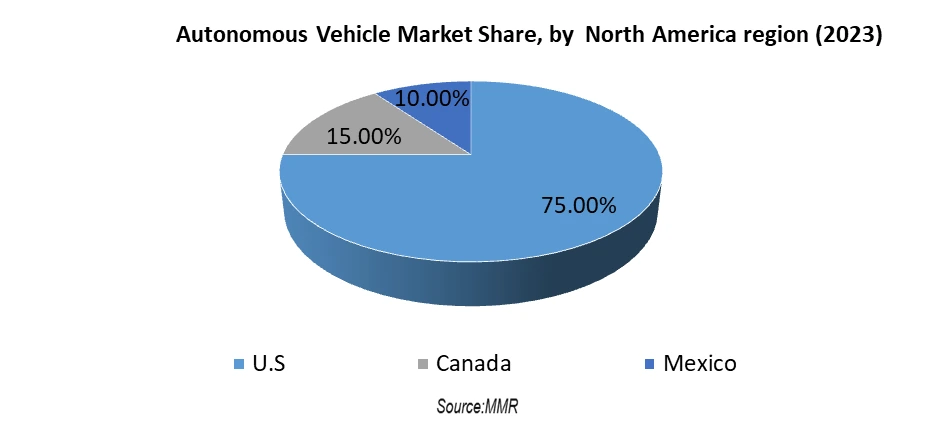

North America is a dominant region in the Autonomous Vehicle market and is expected to grow at a CAGR of 21.9 % through the forecast period. The prime factor supporting the accelerating growth of the North American region was amendments from the government in the traffic regulations to support Autonomous mobility on public roads. The region’s population is generally receptive to innovative technologies, creating a substantial market for autonomous vehicles, drones, and other autonomous systems. The consumer demand and acceptance drive further development in autonomous vehicles. The U.S. is expected to dominate the North American autonomous/self-driving cars market owing to increasing customer inclinations toward Autonomous cars.

The region has been a pioneer of Autonomous vehicles owing to factors like strong and established automotive company clusters and being home to the world's biggest Vehicle Type companies like Google, Microsoft, Apple, etc. Particularly in the US, self-driving cars have already been tested and used in California, Texas, Arizona, Washington, Michigan, and other states of the US. However, their mobility is currently restricted to specific test areas and driving conditions.

Automotive Carbon Wheel Market Competitive Landscape:

1. In Feb. 2024, Ryder System, a supply chain, dedicated transportation and fleet management Solutions Company, and Kodiak Robotics, an autonomous trucking company, announced a collaboration to leverage Ryder’s service network to enable the commercialization and scaling of Kodiak’s autonomous truck solution.

2. December 2023, Kodiak and Ryder established their first truck port in Houston, strategically located at an existing Ryder fleet maintenance facility. The truck port enables Kodiak to launch and land autonomous trucks as well as transfer freight to serve routes between Houston, Dallas and Oklahoma City.

3. In July 2023, HCL Tech., the Noida-headquartered IT services company announced that it had signed a definitive agreement to acquire a 100 per cent equity stake in ASAP Group, an automotive engineering services provider.

4. In August 2023, Pony.ai, a U.S.-based software company, partnered with Toyota Motor (China) Investment Co., Ltd. and GAC Toyota Motor Co., Ltd. to create a joint venture aimed at advancing fully driverless robotaxis for mass production and deployment. The initiative combines Pony.ai's autonomous driving tech, Toyota's branded electric vehicles, and GTMC's production expertise. Together, they'll offer safe and convenient robotaxi services, propelling the industry towards commercialized autonomous mobility.

Autonomous Vehicle Market Scope: Inquire before buying

| Global Autonomous Vehicle Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 42.30 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 33.5% | Market Size in 2030: | US $ 319.68 Bn. |

| Segments Covered: | by Application | Transportation & Logistics Defence Civil |

|

| by Vehicle Type | Passenger Car Commercial Vehicle |

||

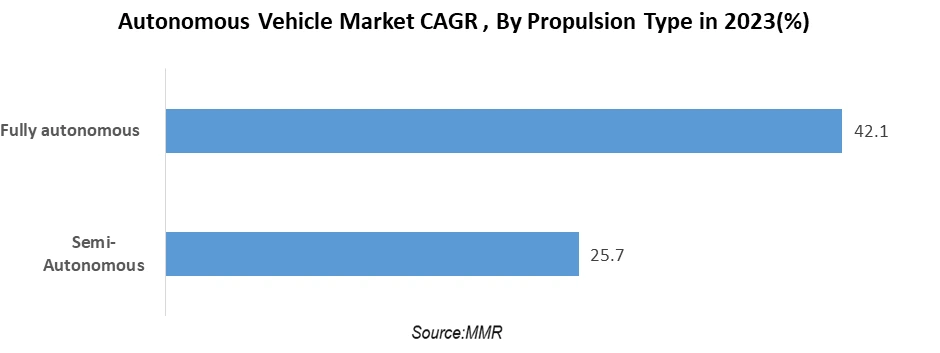

| by Propulsion Type | Semi-Autonomous Fully Autonomous |

||

Autonomous Vehicle Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players in the Autonomous Market Industry:

1. Delphi

2. Ford Motors

3. Tesla

4. Alphabet

5. Intel

6. Daimler Group

7. Baidu

8. Google

9. Volkswagen

10. Jaguar

11. BMW

12. General Motors

13. Toyota

14. AB Volvo

15. Autoliv

16. Bosch

17. Renault-Nissan-Mitsubishi alliance

18. Audi AG

19. General Motors Company

20. Honda Motor Co., Ltd.

21. Nissan Motor Company

Frequently Asked Questions:

1] What segments are covered in the Autonomous Vehicle Market report?

Ans. The segments covered in the Autonomous Vehicle Market report are based on Application, Vehicle Type, and Propulsion Type.

2] Which region is expected to hold the highest share in the Autonomous Vehicle Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Autonomous Vehicle Market.

3] What is the market size of the Autonomous Vehicle Market by 2030?

Ans. The market size of the Autonomous Vehicle Market by 2030 is US$ 319.68 Billion.

4] What is the forecast period for the Autonomous Vehicle Market?

Ans. The Forecast period for the Autonomous Vehicle Market is 2024- 2030.

5] What is the expected growth rate and market size of the Autonomous Vehicle Market by 2030?

Ans. The Autonomous Vehicle Market is expected to grow at a CAGR of 33.5 % from 2024 to 2030, reaching nearly USD 319.68 Billion.