Automotive Software Market Size by Vehicle type, Application, Software layer,EV application, and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

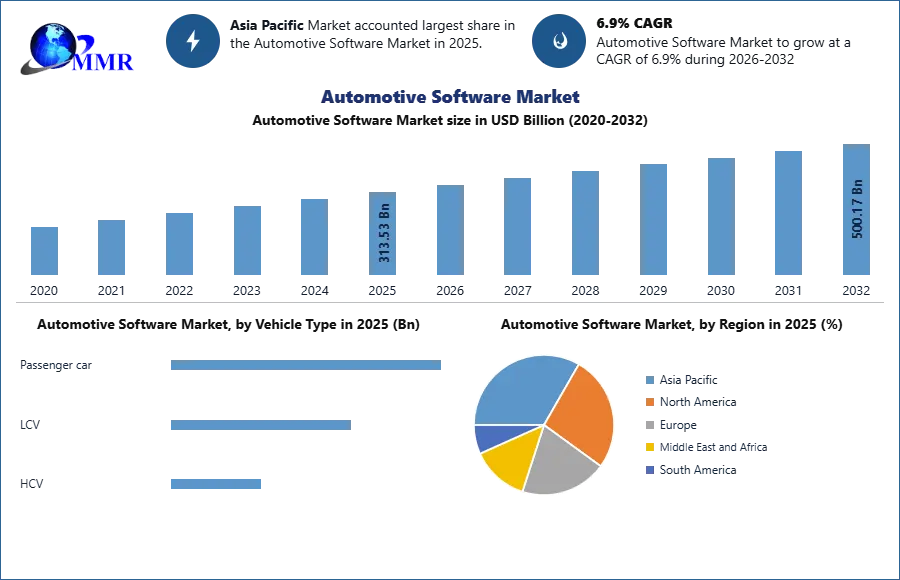

The Automotive Software Market size was valued at USD 313.53 Billion in 2025 and the total Automotive Software revenue is expected to grow at a CAGR of 6.9% from 2026 to 2032, reaching nearly USD 500.18 Billion.

Automotive Software Market Overview:

Advanced Driver Assistance Systems (ADAS), safety and communication applications, and other applications that use automotive software. The growing need for car-to-car communication is expected to drive the automotive software market in the coming years, and the popularity of such applications has grown in recent years.

The Automotive software is a collection of programmable instructions that are used in performing various operations of computer-based in-vehicle applications.. This advance automotive software installed in car’s system. The software is used in applications such as infotainment, body control, comfort, and telematics.

Autonomous driving (AD), connected vehicles, powertrain electrification, and shared mobility (ACAS) are all mutually reinforcing trends in the automotive industry. They are not only disrupting the automotive value chain and affecting all stakeholders, but they are also a significant driver of the expected 6.9 per cent compound annual growth rate. CAGR for the automotive software market, i.e., between and , from USD 240 billion to USD 409.29 billion.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Research Methodology

Primary and secondary data collection methods were used to collect data. primary interviews with experts from automotive & IT industries and suppliers have been carried out to take the key inputs about the trends in industry in particular regions and specific companies. Primary respondents include representatives from manufacturing TIER 1, TIER 2 companies, and OEMs. Some of the industry experts are also interviewed to validate the key findings. From secondary sources such as the International Organization of Motor Vehicle Manufacturers (OICA), the China Association of Automobile Manufacturers (CAAM), and others. Details list of sources is given in the report in case internal data is not used.

Automotive Software Market Dynamics:

Connected car service Derive the market

The growing number of connected cars has created new revenue-generating opportunities for the ecosystem's stakeholders. Many non-automotive players have entered the race of connected cars and autonomous driving to capitalize on the revenue opportunity.

Vehicles today are no longer hardware-based moving machines. They currently account for nearly 40% of electronic content, and this figure is expected to rise to more than 60% in the coming decades.

Domain controllers, consolidated ECUs, HMI, and AI will dominate the majority of electronic content for advanced vehicle applications such as ADAS, telematics, engine management systems, and so on. For proper operation, these applications must be programmed with a large number of lines of code. Vehicles become more technologically advanced, the complexity of these applications grows.

As a result, systems must be programmed with more codes, increasing the demand for embedded software. As a result, the growing number of connected cars is propelling the automotive software market.

Advancements in 5G and AL technology drive the Automation software market

The revolution in design requirements and architectures is influencing software requirements. Wireless connectivity is critical to the user experience of automotive software. To find a solution, various telecom companies are focusing on the development of 5G to improve the safety and efficiency of automotive software. Automobiles are becoming network-aware, software-defined, and ultra-connected data transmitting vehicles, necessitating the use of a high-tech connectivity platform.

Understanding these implications, as well as the challenges for the automotive industry, can help to accelerate the adoption of connected cars. Thanks to autonomous vehicles and automotive software expected to communicate instantly, 5G will be a critical enabler.

For example, South Korea and the EU have agreed to collaborate on 5G development, with both investing USD 1.8 billion and USD 790 million, respectively, in funding local 5G projects. The United Kingdom has approved USD 77 million in funding for the 5G research facility 5 GIC.

Working with automotive software generates massive amounts of data, which has led to the expansion of AI in the automotive sector. Speech and gesture recognition enhanced HMI, eye tracking, driver monitoring, radar-based detection units, virtual assistance, and engine control units all use artificial intelligence in automotive software. Deep learning is expected to grow at the fastest rate in the automotive industry when compared to other technologies, which will drive the market.

Lack of connected infrastructure

The high-priced infrastructure required for 5G and wireless connectivity is having an impact on the growth of the automotive software market. A significant amount of capital will be required to build the necessary software interaction platforms, which include IoT, data analytics, and the cloud.

Connected cars and ADAS solutions require quick, agile, and accessible methods of updating software to incorporate new content. The difficulty has grown even more apparent as the updates necessitate fast connectivity solutions, which developing countries are still struggling to develop.

Over-the-air (OTA) software updates have been given first priority. Furthermore, without proper connectivity solutions, manufacturers are adding new apps and services ranging from emergency calling services to traffic alert notifications.

Automotive Software Market Segment Analysis

Based on Vehicle Type: The strong demand for highly advanced applications such as ADAS and connected services is driving up demand for automotive software in passenger cars in developed countries. The increase in demand for advanced applications for the automotive industry prompted the major player to implement the strategy.

Software services are more prevalent in passenger cars than commercial vehicles, the passenger car segment is expected to dominate the automotive software market during the forecast period.

For example, Harman International (US) acquired Savari Inc (US) in February , an automotive technology company that develops vehicle-to-everything communication technology for 5G Edge and automotive devices. The increasing disposable income in Asia Pacific developing countries has fueled demand for passenger cars with technologically advanced services.

In , China's car production is expected to be around 21.5 million units, while Japan's production is expected to be around 6.7 million units. It accounted for approximately 3.1 million units in South Korea and approximately 3.5 million units in India in the same year.

Toyota Kirloskar Motor announced a USD 272.5 million investment in electric components and technology development in . In , Hyundai Motor will invest USD 500 million to increase its market share in India.

Tesla Inc invested USD 187 million in November to optimize the production line at its Shanghai factory (China).

China is quickly becoming one of the most important global export hubs for US electric vehicle manufacturers. Furthermore, the region's demand for automotive software is expected to rise as a result of the advent of autonomous driving and IoT and prominent growth in demand for high-end services further.

Passenger vehicles have more software content than commercial vehicles. A luxury-class passenger car has more electronic content than a passenger car in the economy or middle class. Software controls these modern electronic applications.

The connected passenger car represents a watershed moment in the automotive industry. They gather massive amounts of data from a variety of sources. The passenger vehicles communicate with one another, exchange data, and warn drivers of potential hazards.

Furthermore, the rise of vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communications, as well as the introduction of semi- and fully autonomous driving, would result in the greatest value repositioning in the automotive software industry. Therefore, it is essential that passenger cars have sophisticated software with a high V2V and V2I data transfer capability.

Based on the Application: the power train segment will be the fastest-growing application in the automotive software market during the forecast period. Powertrain technology improves fuel efficiency and performance in conventional internal combustion engines, electric and hybrid vehicles with software and data by leveraging onboard sensing and external connectivity via vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I) and vehicle-to-everything (V2X) technologies.

Leverage connected powertrain information from neighbouring vehicles (V2V) and traffic signals (V2I) to minimize accelerations and generate an energy-efficient speed profile. Fuse powertrain dynamics layer on top of existing off-the-shelf navigational services to present energy optimal routes specific to vehicle powertrain and driver behaviour.

Advanced powertrain control for electrified powertrains, engine control, transmission control and ultra-low NOx solutions for heavy-duty trucks. Within the powertrain domain, a shift toward EVs is expected to drive market growth at a CAGR of 5%. (i.e., PHEV, HEV, BEV).

This is due to the high ASP of EV ECUs, which is up to ten times higher than that of ICEs when accounting for their complexity. ICE vehicles contribute only a minor portion of the powertrain ECU/DCU market growth. domain, as the ASP of ICE ECUs, is expected to remain relatively stable over time. In total, the market size is Because the take rate of powertrain ECUs/DCUs engine, transmission, or battery control is nearly 100 per cent.

Based on the Software Layer: an operating system (OS) serves as a bridge between computer hardware and application programmes. This limits an application's ability to use hardware by requiring it to adhere to rules and procedures programmed into the operating system.

Based on the Software Layer: an operating system (OS) serves as a bridge between computer hardware and application programmes. This limits an application's ability to use hardware by requiring it to adhere to rules and procedures programmed into the operating system.

The operating system also includes services that make app development and execution easier. These services include managing all of the hardware resources that the app will use, such as loading the programme into memory, communicating with sensors and actuators, storing results, and performing a variety of other functions.

Many other software capabilities, such as middleware, libraries, and other system software, are also considered part of the OS.

The capabilities and ecosystem of the operating system are also important for developing the apps and software platforms required by software-defined vehicles. To put it another way, the best operating system requires a large ecosystem and infrastructure to support the growing software-defined vehicles of the future.

Recent Development: Automotive Software Market

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 05 January 2026 | NVIDIA | NVIDIA launched its Alpamayo open AI models, a suite of foundation models designed to enable contextual reasoning in autonomous vehicles using multimodal perception. | The release accelerates the transition to Level 4 autonomy by providing a high-fidelity simulation-trained framework for complex real-world decision-making. |

| 06 January 2026 | Siemens | Siemens introduced a specialized digital twin software platform for Software-Defined Vehicles (SDVs) that facilitates continuous virtual validation of hardware-software integration. | This tool drastically reduces development lifecycle risks and integration time, supporting the automotive industry's pivot toward centralized zonal architectures. |

| 07 January 2026 | Lucid, Nuro, and Uber | The companies debuted a collaborative robotaxi platform at CES 2026, integrating proprietary autonomous stack software with an electric vehicle chassis. | The joint venture commercializes a scalable Level 4 software solution, marking a significant milestone for urban mobility-as-a-service deployment in major metropolitan hubs. |

| 18 December 2025 | Siemens | Siemens officially unveiled PAVE360™ Automotive, a pre-integrated software category designed to address the complexity of ADAS and Infotainment integration. | The platform empowers OEMs and Tier-1 suppliers to perform early full-system virtual integration, effectively shortening time-to-market for advanced vehicle features. |

| 23 February 2026 | Fortune Business Insights | Market auditors confirmed that Application Software reached a 50.97% dominant share of the total automotive software market valuation in early 2026. | This data reflects the massive industry investment in connected services and telematics, projecting the global market value to reach $41.12 billion within the fiscal year. |

Automotive Software Market Regional Insights:

Asia Pacific is expected to hold the largest share during the forecast period. Increased demand for connected services, particularly in Japan, China, and South Korea, is driving the Asia Pacific market. It is the largest market because it produces the majority of vehicles. Despite the fact that automotive software penetration in the region is very low when compared to Europe and North America, the market size is larger due to higher vehicle production.

Increased demand for connected services, particularly in Japan, China, and South Korea, is driving the Asia Pacific market. It is the largest market because it produces the majority of vehicles. Despite the fact that automotive software penetration in the region is very low when compared to Europe and North America.

This region's key automotive manufacturers, as well as software providers and system integrators, are focusing on developing and innovating advanced software solutions to support reliable, safe, and performance-oriented automotive applications.

Asia Pacific countries are concentrating their efforts on the production of automobile components as well as vehicles. For example, the Chinese government is working on "Made in China 2025," which will help domestic automakers compete with global automakers.

This will enable the incorporation of cutting-edge technology such as ADAS, connected services, autonomous driving, infotainment, powertrain management, V2X, vehicle diagnostics, and telematics, among others. The services fuel the region's demand for automotive software.

A few global players dominate the automotive software market, which also includes several regional players. Robert Bosch (Germany), NVIDIA (US), NXP (Netherlands), BlackBerry (Canada), Elektrobit (US), Renesas Electronics (Japan), Airbiquity (US), Wind River Systems (US), and Green Hills Software are some of the key players in the automotive software industry (US).

These companies have extensive global distribution networks. On top of that, these companies have a diverse product portfolio of software solutions for a variety of applications. These major players' primary strategies for maintaining their market position are new product development, contracts and agreements, and collaborations.

Robert Bosch Gmbh is a market leader in the automotive software market due to its strong distribution network and diverse product portfolio. For the automotive industry, it provides remote device management, software updates, gateway software, and data management. Significant investments in the software service would result in a larger footprint in the automotive software market.

Automotive Software Market Scope: Inquire before buying

| Automotive Software Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 313.53 USD Billion |

| Forecast Period 2026-2032 CAGR: | 6.9% | Market Size in 2032: | 500.17 USD Billion |

| Segments Covered: | by Vehicle Type | Passenger car LCV HCV |

|

| by Application | ADAS & Safety Systems Body Control & Comfort System Powertrain System Infotainment System Communication System Others |

||

| by Software Layer | Operating System Middleware Application Software |

||

| by EV End-Use | Charging Management Battery Management V2G Others |

||

Automotive Software Market, by region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Netherlands, Ukraine, Austria and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Myanmar,Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina and Rest of South America)

Automotive Software Market Leading Competitors are:

The automotive software industry is characterized by intense competition among key players, including established companies and emerging tech firms. Major manufacturers like NVIDIA and Tesla lead with innovative solutions focused on autonomous driving and advanced driver assistance systems (ADAS). Strategic partnerships, such as those between automotive giants and technology firms, enhance market penetration and product offerings. Financial performance reflects this rivalry, with companies investing heavily in research and development to drive innovation. As consumer demand for connected and autonomous vehicles grows, the competitive landscape will continue to evolve, necessitating agility and continuous improvement from all market participants.

- Robert Bosch GmbH

- Continental AG

- BlackBerry Limited QNX

- Google LLC Alphabet

- Microsoft Corporation

- NVIDIA Corporation

- NXP Semiconductors N.V.

- Intel Corporation

- Infineon Technologies AG

- Renesas Electronics Corporation

- Aptiv PLC

- DENSO Corporation

- Panasonic Automotive Systems

- LG Electronics Vehicle Solutions

- HARMAN International

- Wind River Systems

- Green Hills Software

- Elektrobit

- TTTech Auto AG

- Vector Informatik GmbH

- KPIT Technologies Ltd.

- Tata Elxsi Ltd.

- Airbiquity Inc.

- MontaVista Software LLC

- OpenSynergy GmbH

- Sonatus Inc.

- Autodata Ltd.

- Intellias Ltd.

- PATEO Connectivity Technology

- Qualcomm Technologies Inc.

Frequently Asked Questions:

1. What is the forecast period considered for the Automotive Software Market report?

Ans. The forecast period for the Automotive Software Market is 2026-2032.

2. Which key factors are hindering the growth of the Automotive Software Market?

Ans. Lack of connected infrastructure hindering the growth of the automotive software market growth.

3. What is the compound annual growth rate (CAGR) of the Automotive Software Market for the forecast period?

Ans. 6.9% CAGR is the annual growth rate of the automotive software market for the forecast period

4. What are the key factors driving the growth of the Automotive Software Market?

Ans. Advancements in 5G and AL technology drive the Automation software market

5. What was the Global Automotive Software Market size in 2025?

Ans: The Global Automotive Software Market size was USD 313.53 Billion in 2025.