Global Automotive Engineering Services Market Size by Service Type, Vehicle Type, Location, Application, Propulsion, and Nature Type – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2034

Overview

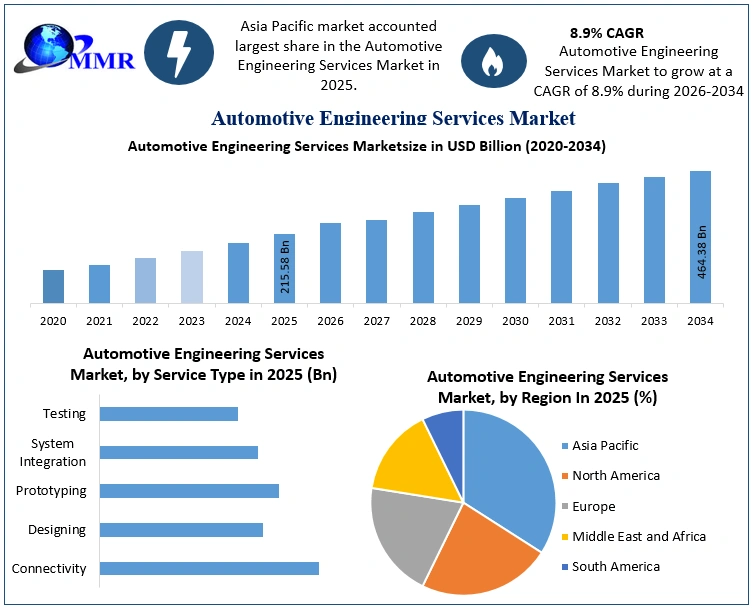

The Automotive Engineering Services Market size was valued at USD 215.58 Billion in 2025 and the total Automotive Engineering Services revenue is expected to grow at a CAGR of 8.9% from 2026 to 2034, reaching nearly USD 464.38 Billion.

Automotive Engineering Services Market Overview:

Automotive engineering services assist original equipment manufacturers (OEMs) and their suppliers in digitizing the product value chain, lowering development costs, and growing up the time to market. Vehicle engineering, vehicle electronics, manufacturing IT, and product lifecycle management are some of the automotive engineering services.

Designing and testing brake systems, engines, safety mechanisms, fuel technologies, and transmission are all examples of automotive engineering services. Growing competition in the car sector among auto OEMs and increased focus on improving key capabilities among auto OEMs are the major factors driving the global automotive engineering services market.

Other factors influencing the market's growth include growing sales of electric vehicles, rising R&D expenditures in the automotive sector, and strict government laws and regulations governing vehicles powered by internal combustion engines (ICEs). Thanks to the development of autonomous vehicles, growth potential for automotive engineering services have been increased. However, intellectual property (IP) and a changing business model are some of the growth hurdles for automotive engineering services market growth. Additionally, weak economic conditions worldwide brought on by the spread of COVID-19 provide serious challenges to the growth of the market. The report has covered dynamics related to the patents and intellectual property rights and how the companies from both the sides are working on it.

Automotive Engineering Services Size, Growth & Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Automotive Engineering Services Market Dynamics:

R&D investment made by the automobile industry

The key factors driving the market growth are the consistently rising consumer trust in engineering services and the significant RD investments made by the automobile industry. Top users of automotive engineering services include some of the world's leading manufacturers, including Renault, Volkswagen, BMW AG, Daimler AG, and Ford Motor Company. The increasing focus on autonomous driving systems would require OEMs to incorporate more cruise control features and advanced safety systems for semi-autonomous vehicles.

Additionally, other automakers are seriously considering using automotive engineering services to increase quality, increase safety, save development costs, and adhere to strict norms set by governments. These are key driving factors of the automotive engineering service market.

Development in autonomous vehicles

Driverless vehicles that can drive themselves by sensing their environment are known as autonomous vehicles. Advanced automotive engineering services are used by autonomous vehicles to respond to their environment and adjust their driving. These cars assist in enhancing traffic safety and decreasing vehicle collisions brought on by human mistakes. Automated cars have the potential to reduce the frequency of accidents because the software utilized is expected to make fewer errors than humans. Additionally, the rate of accidents equals fewer traffic issues, and less human behavior means fewer roadblocks.

For instance, autonomous vehicles assist those who are unable to drive due to a disability or old age because they offer a more convenient mode of transportation. For example, Ford is one of the leading businesses globally focused on the development of driverless automobiles. By the end of 2025, it plans to roll out completely autonomous vehicles. Therefore, the market for automotive engineering services is expected to grow significantly as demand for autonomous vehicles increases

IP restrictions hamper the market growth

Outsourcing is currently common practice among OEMs, Tier 1 suppliers, and system integrators in the automotive sector. Before final manufacturing, a typical engineering service begins with concept/research and progresses through the design and testing phases. In some circumstances, the OEM owns the intellectual property of new technologies or processes that arise during the process. However, service providers may be working with numerous OEMs for comparable criteria or standards, with the limitation of employing existing patented technology from different OEMs. As a result, service providers must exercise extreme caution when it comes to IP violations. Innovation in the automotive sector necessitates a significant investment of both resources and time. IP restrictions prohibit service providers from reusing the same technology, which may limit its utilization.

Automotive Engineering Services Market Segment Analysis:

By Service type, based on service type prototype service segment held the largest market shear in 2025 thanks to automotive industry's increased use of 3D printing technology to create models of entire cars as well as prototypes of assemblies and individual parts. With the use of 3D printing technology, producers may easily spot defects in the prototype and quickly fix them, supporting a cost-effective strategy. Companies are using 3D CAD software more frequently to enhance design quality, increase productivity, establish a database for manufacturing, and improve communications through documentation.

As ESPs invest in the development of new test centers in an effort to grow and satisfy the rising demands for automotive testing, the testing category is expected to experience the fastest growth over the next eight years, with a CAGR of almost 30.0%. For instance, Bertrandt AG invested USD 17.0 million in March to expand its high-voltage test facility in order to meet the expanding demand for high-voltage test resources.

Based on Location Type, the outsource engineering service segment held the largest market share in 2025. The constant pressure to quickly design, prototype, manufacture, and launch new products in the marketplace, in response to ever-decreasing product lifecycle and greater demand, is placing a strain on the in-house engineering workforces and processes of companies, and as a result, the companies are now gradually shifting towards outsourcing of engineering services. Outsourcing is expected to be the fastest location segment in the forecast period.

The market for outsourcing will be boosted during the forecast period by the rising customer demand for more advanced car connectivity services. As they desire the flexibility to satisfy customers' individual demands in all regional markets, OEMs are expected to focus on boosting their outsourcing of automotive engineering services.

Cybersecurity and connected car research and testing are two significant issues that have led to a lot of software updates and software management services. Therefore, the OEMs who stand to benefit the most from their partnerships with engineering service providers will be the ones to choose their outside partners and ensure that projects proceed as planned. All of these advantages of outsourcing will be advantageous for the market as a whole. The majority of the major EV battery manufacturers are constantly innovating in battery design and chemistry to increase the range of EVs and go ahead with the need for regular charging. Additionally, ongoing developments in the field of EV batteries are focused on enhancing the range of electric vehicles. Additionally, this is in favor of outsourcing automotive engineering services for battery management.

{kind=link}

The top companies in the global market for outsourcing automotive engineering services are Bertrandt, Altran Technologies S.A., Alten GmbH, HORIBA, Ltd., and AVL List GmbH. The industry also includes a number of other well-known companies that provide outsourcing for automotive engineering services, including IAV GMBH, FEV Group, MBTECH GROUP GMBH, EDAG ENGINEERING GMBH, and KISTLER INSTRUMENTE AG. Top, mid-level, and a number of domestic businesses compete in the global market for automotive engineering services. Additionally, the established players in the market have developed a number of strategies and research and development projects to compete with other competitors in the regional and international markets.

Based on Application Type, the connectivity service segment is expected to highest growing segment in the forecast period. The global 5G infrastructure is expanding quickly. Next-generation cellular technology, or 5G, is expected to be able to deliver high-speed, reliable communication at extremely low latency levels. Currently, three primary categories of connected services. By giving them new capabilities, the new wireless technology is expected to support the growth of various reducing digital industries.

The adoption of 5G services, for instance, is expected to be driven by the requirement to ensure reliable, seamless, and continuous connectivity with autonomous vehicles. Additionally, it is expected that the rapid adoption of 5G network infrastructure would increase operational efficacy in a number of IoT use cases, including smart homes, smart cities, and industry 4.0. On the other hand, it is also expected that the industry will benefit from the future adoption of 5G services for applications such as remote patient monitoring and remote surgery.

Today, electronic systems are used by millions of automobiles for emergency services, linked entertainment, and real-time navigation. However, future wireless networks like 5G will allow for more uses, including communications between vehicles, infrastructure, networks, and passengers (V2P), as well as autonomous driving. New safety-sensitive applications, collectively referred to as V2V/V2I, will be made possible by 5G's higher throughput, dependability, availability, and decreased latency (V2X, or Vehicle-to-Everything).

Automotive Engineering Services Market Regional Insights:

The automotive engineering service market was dominated by the Asia Pacific area in 2025, with a revenue share of about 42.0%, and it is expected that this trend would continue during the next eight years. This is explained by China's quick adoption of electric vehicles for personal transportation. The market is expected to grow throughout the forecast period due to government regulations that aim to minimize or reduce emissions and use green technologies. The Asia Pacific automotive engineering services market is being driven by factors including increased vehicle production, rising luxury vehicle demand, rising sales of electric automobiles, and technological advancement.

The Asia-Pacific area includes industrialized countries like Japan and South Korea as well as fast developing economies like China and India. These nations are recognized as the biggest markets for the production of automobiles, and in recent years, the region has also become a center for the industry. The region's automotive engineering services industry is expanding as a result of the region's high automotive demand and production as well as growing worries about rising CO2 emissions and traffic congestion. North America, on the other hand, is expected to experience rapid expansion throughout the forecast period.

The objective of the report is to present a comprehensive analysis of the Automotive Engineering Services Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

Automotive Engineering Services Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2025 | FEV Group | FEV Group launched an upgraded Software-Defined Vehicle (SDV) engineering framework integrated with AI-driven testing tools for next-generation electric mobility platforms. | The initiative reduces software validation cycles by up to 30%, significantly accelerating time-to-market for automotive original equipment manufacturers. |

| 18 March 2025 | Capgemini | Capgemini partnered with a major global automaker to deliver end-to-end cloud-based automotive engineering and digital twin simulation services. | This collaboration expands Capgemini's footprint in high-performance virtual prototyping while lowering vehicle development overheads. |

| 22 May 2025 | AVL List GmbH | AVL List GmbH expanded its engineering footprint by opening a state-of-the-art battery and e-drive validation facility dedicated to heavy-duty commercial EVs. | The expansion enhances testing throughput for 800V high-voltage architectures, addressing the global surge in zero-emission commercial transport requirements. |

| 10 September 2025 | L&T Technology Services | L&T Technology Services secured a multi-million dollar engineering services contract to design Level 3 and Level 4 Autonomous Driving Systems for a European OEM. | The win consolidates LTTS's leadership position in advanced driver-assistance systems (ADAS) software engineering and sensor fusion solutions. |

| 12 November 2025 | Horiba Mira | Horiba Mira unveiled a specialized automotive cybersecurity engineering suite compliant with updated ISO/SAE 21434 standards. | The platform enables vehicle manufacturers to effectively mitigate connected vehicle cyber threats and regulatory compliance risks. |

| 14 January 2026 | AKKA Technologies (Akkodis) | Akkodis announced a strategic joint venture to co-develop integrated lightweight vehicle architecture and thermal management systems for next-gen EVs. | This development significantly enhances electric powertrain efficiency and driving range through optimized thermal integration. |

Automotive Engineering Services Market Scope: Inquire before buying

| Automotive Engineering Services Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 215.58 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 8.9% | Market Size in 2034: | USD 464.38 Bn. |

| Segments Covered: | by Service Type | Connectivity Designing Prototyping System Integration Testing Others |

|

| by Vehicle Type | Passenger Cars Light Commercial Vehicles Heavy Commercial Vehicles Others |

||

| by location | In-house Out-source |

||

| by Application | ADAS and Safety Electrical, Electronics, and Body Controls Chassis Connectivity Services Interior, Exterior, and Body Engineering Powertrain and Exhaust Simulation Battery Development & Management Charger Testing Motor Control Others |

||

| by Propulsion | ICE Electric |

||

| by Nature Type | Body Leasing Turnkey |

||

Automotive Engineering Services Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Automotive Engineering Services Market, Key Players are:

1. Altair Engineering Inc. (US)

2. Pilot Systems International (US)

3. HARMAN International (US)

4. EPAM Systems (US)

5. GlobalLogic (US)

6. Belcan (US)

7. Hunter Engineering Company (US)

8. Alten Group (France)

9. Altran (Capgemini Engineering) (France)

10 ESI Group (France)

11. ASAP Holding Gmbh (Germany)

12. ESG Elektroniksystem- und Logistik-GmbH (Germany)

13. FEV Group GmbH (Germany)

14. Bertrandt AG (Germany)

15. EDAG Group (Germany)

16. ITK Engineering GmbH (Germany)

17. P3 group GmbH (Germany)

18. Robert Bosch GmbH (Germany)

19. IAV (Germany)

20. Continental AG (Germany)

21. L&T Technology Services Limited (India)

22. HCL Technologies Limited (India)

23. Onward Technologies Ltd. (India)

24. Horiba, LTD. (Japan)

25. Ricardo (UK)

26. Akka Technologies (Belgium)

27. Valmet Automotive (Finland)

28. Semcon (Sweden)

29. AVL List GmbH (Austria)

Frequently Asked Questions:

1. What is the forecast period considered for the Automotive Engineering Services Market report?

Ans. The forecast period for the Automotive Engineering Services Market is 2026-2034.

2. Which key factors are hindering the growth of the Automotive Engineering Services Market?

Ans. IP restrictions hamper the market growth.

3. What is the compound annual growth rate (CAGR) of the Automotive Engineering Services Market for the forecast period?

Ans. 8.9% of CAGR is the annual growth rate of the automotive engineering market.

4. What are the key factors driving the growth of the Automotive Engineering Services Market?

Ans. R&D investment made by the automobile industry.

5. What was the Global Automotive Engineering Services Market size in 2025?

Ans: The Global Automotive Engineering Services Market size was USD 215.58 Billion in 2025.