Automotive Adhesives And Sealants Market Size by Resin Type7., Application, Vehicle Type, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

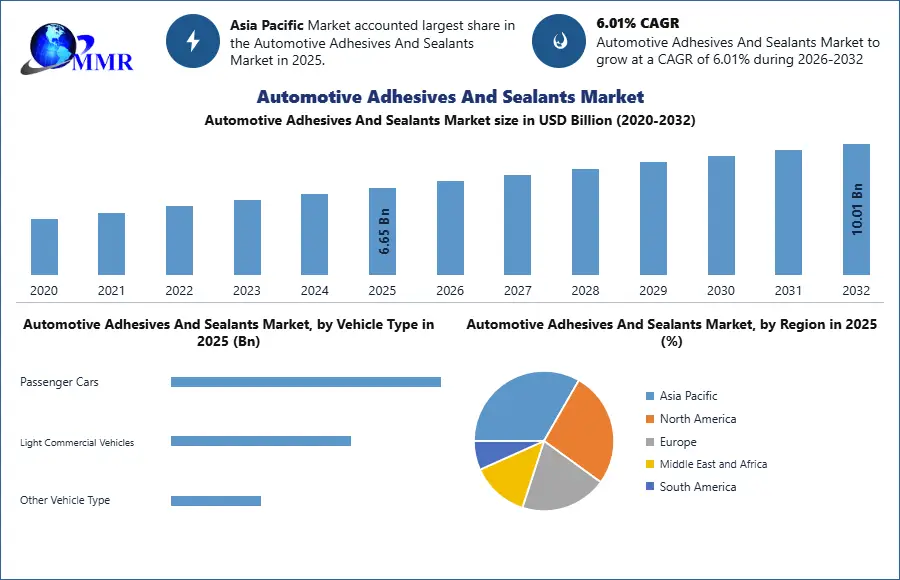

Automotive Adhesives And Sealants Market size was valued at US$ 6.65 Bn. in 2025 and the total revenue is expected to grow at 6.01% of CAGR through 2026 to 2032, reaching nearly US$ 10.01 Bn.

Automotive Adhesives And Sealants Market Overview:

Automotive adhesives and sealants are widely used, from as little as a sensor to as large as a car chassis. To reduce the weight of the vehicle to a minimum, lightweight composite materials are used in the production of many high-performance automobiles. Because these composite materials cannot be welded, mechanical fasteners must be used, which increases the weight of the car, is unattractive, and runs the danger of vibrating loose. and increase performance to drive market growth. Professionals in the automobile sector enjoy structural adhesives because they make it simple to link various types of material together (such as composite to metal where welding would not be suitable). The rubber toughening found in structural adhesives, which helps in absorbing vibration and impact stresses, is an extra benefit and boosts the market growth.

A wide variety of adhesive products, including formed-in-place gaskets, adhesive for sealing core plugs, automobile hose bonding, heat exchanger sealing, and filter end cap bonding, are available from Permabond that are suited for under-the-hood applications. Various adhesives are also used in the electronic systems of cars for a variety of purposes, including connecting electric motors, potting and sealing electrical components, sensors, switches, and relays. Permabond provides adhesives to the automobile industry on a global scale, with many of its products being designated by top automakers and Tier 1 auto suppliers, who benefit from premium, cutting-edge goods at extremely affordable costs, these increase competition in auto manufacturers and create new opportunities. The report addresses development policies and plans, manufacturing procedures, and cost structures are also analyzed. Additionally, this report includes data on supply and demand, import/export consumption, cost, price, income, and gross margins. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Automotive Adhesives And Sealants Market Dynamics:

Adhesives and sealants have a huge future in the automotive industry

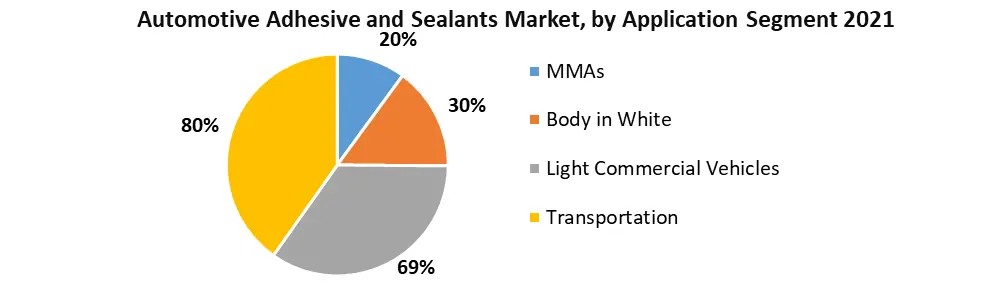

As automakers continue to look for methods to make cars lighter and more fuel-efficient, the usage of adhesives in automotive assembly is growing. Numerous vehicle assembly applications are gaining from automotive adhesives. According to a forecast from the Automotive Adhesives Market, the body in white application accounted for the biggest volume share of the global automotive adhesives market in 2022. (A stage in automotive design or vehicle manufacture known as "body in white" or "BIW" refers to the point at which the sheet metal components of a car body have been joined together.) The use of automotive adhesives in BIW has advantages in terms of increased durability, increased strength, and decreased weight. According to the study, the assembly application.

Due to their superior surface adherence, high shear strength, and temperature tolerance, double-sided adhesive tapes account for a sizable percentage i.e (80%) of the market. Automotive manufacturers are drawn to these components' biodegradable qualities due to rising environmental responsibility concerns. The weight of adhesive materials, which can weigh up to 40 pounds in some finished cars, is small compared to the weight of metal rivets, screws, and welds, which are no longer necessary to successfully connect components.

Adhesives create huge demand thanks to as vehicle ages, heat-affected regions near spot welds may experience microcracking. Squeaks and rattles may eventually result from this cracking. Adhesives do not have this issue since they disperse the tension of a bond across a larger surface than a spot weld. In comparison to conventional reinforcing elements that would be inserted during manufacture, they are also much lighter and less costly.

Future Growth of the Automotive Adhesives and Sealants Market

What does the utilization of automotive adhesive hold for the future? Growth. Global megatrends continue to be important factors from the viewpoint of adhesive makers or applicators, and these include:

Adhesive assembly techniques with added value reduce or eliminate the need for mechanical fixing and labor expenses. To create new baseline formulations with combined benefits, novel product chemistries integrate the advantages of many already used chemistries.

The continued and expanded usage of mixed materials requires taking into account joining techniques that address specific D/a difficulties and the removal of BLRT on Class A surfaces. Technologies that enable complete cure on demand as well as quick fixing similar to spot welding. De-bond on demand for serviceability, especially for parts of electric vehicles that require service. Due to the lack of traditional engine and transmission noise and new frequencies in noise transmission, new methods of acoustic solutions are needed for electric cars. Due to the lack of traditional engine and transmission noise and new frequencies in noise transmission, new methods of acoustic solutions are needed for electric cars.

By design, where heat does not fully penetrate metals, or as a result of manufacturer sustainability measures, lower bake temperatures are achieved (utility savings) Regulations of chemical formulations and substances will continue, and there will be regional trends toward "odor-free" adhesive goods (e.g., Europe and China).

Improved "virtual" examination of adhesive performance to forecast performance and failure concurrently with or before prototype construction levels.There is no question that the utilization and adaptability of adhesive chemistries will continue to flourish in permitting the outcomes of the megatrends that transform our business on a regular basis. The market for adhesives is equipped to take on the upcoming significant design difficulties.

Challenges face by OMEs

Strict regulatory requirements create an obstacle to the automotive adhesives market. Manufacturers of automotive adhesives are required to adhere to VOC emission guidelines established by several national and regional organizations. As a result, many glue suppliers are forced to make significant financial investments to modernize their businesses, raising the final product's price. Low- and no-VOC adhesives have been developed as concern about the negative effects of formaldehyde and other VOCs on human health has grown. Given the growing prevalence of adhesives in our daily lives, this technical advancement is quite important. Any brand-new low-VOC adhesive in the US must meet the performance requirements set out by ASTM International in order to be accepted on the market. Standard criteria are created by ASTM Technical Committee 014 for compounding adhesives and engages in research on adhesives, including clarification on the nature of adhesion.

Manufacturers may find opportunity and difficulty in the global movement toward fully biodegradable materials. There is a market for such items since biodegradable materials are becoming more and more popular. The worldwide market for adhesives and sealants may be hampered by strict environmental restrictions from governing environmental organizations connected to VOC (Volatile Organic Compound) emission, which presents a problem for producers. This is due to the fact that manufacturers are only able to generate synthetic adhesives and sealants, as well as the growing price of the essential raw ingredients used to make them.

Automotive Adhesives And Sealants Market Segment Analysis:

Based on Resin Type, the Automotive Adhesives And Sealants Market are segmented into Type Epoxy, Acrylic, Polyurethane, Silicone, SMP, MMA Other Resins. MMAs held the largest market share in 2022. Adhesives made of methyl methacrylate are now commonly used in the automotive and transportation industries. They combine the structural adhesive's strength with a special cure profile that enables them to be applied to big surfaces and a variety of materials. MMAs offer the best match in a sector that is always searching for lightweight and efficient solutions in the automotive adhesive sealant market.

For the automobile sector, MMAs' "snap-cure" capability is its most attractive feature. Unlike epoxies or other adhesives, which gradually gain strength during the curing process, MMAs stay usable for a short period of time before curing to a fixture strength. By altering the formulation and mixing ratios, that open workable time as well as curing time may be customized to the precise application. Large panels of heavy equipment or vehicles may now be covered with adhesive and fixtured as soon as feasible. By allowing for speedier adhesion and less waiting for cure, the use of MMAs in this fashion can drastically save manufacturing time. At room temperature, a full cure typically takes 4 to 24 hours to complete.

A number of additional characteristics of MMAs also make them well-suited for vehicle assembly. They are also largely immune to grease and oil, two frequent pollutants in the manufacturing of automobiles. Production may be streamlined even further by allowing components to be adhered without first going through a thorough cleaning procedure. Because MMAs can adhere to a variety of surfaces, including metal, certain plastics, and composites, they may be used in a wide range of automotive applications. A lighter vehicle with lower fuel and material costs can be made by using adhesive in place of metal rivets. Additionally, it disperses tension across the bond region as opposed to concentrated areas. In comparison to rivets or certain other adhesives, MMAs can lessen bond-line read-through (BLRT), giving surfaces a smoother appearance.

Based on the Application, the Automotive Adhesives And Sealants Market are segmented into Body in White, Paint Shop, Assembly, and Power train. Body in white (BIW) is expected to dominate the market during the forecast period. Before painting and before to the assembly of the motor, chassis sub-assemblies, or trim (glass, door locks/handles, seats, upholstery, electronics, etc.) in the frame structure, BIW is termed. The term derives from an earlier time when automotive bodywork was constructed by independent companies on a unique chassis with a connected engine, suspension, and fenders. Body in white (BIW) parts make up approximately 20–30% of a vehicle's curb weight, which indicates significant income opportunity for component suppliers and other automotive accessories along the automotive value chain. Body in white (BIW) components are a dependable section of the automotive industry and are connected as the key industry segment in a sector where new technologies like electric and hybrid cars, the rise of autonomous and connected vehicles, and in the overall automotive industry.

The fundamental problem in the automobile industry is the growing need for fuel economy and lightweight solutions. For improved fuel efficiency, the automotive industry is constantly introducing innovative lightweight materials for applications in the body, chassis, interior, power train, and under the hood. However, the cost of the lighter materials is more than that of the older components. Although the new materials boost the buyer's fuel economy, they also raise the cost of automobiles. This might affect both the organization's ability to make a profit and the size of the next buy lot of lighter cars, both of which are necessary for efficient operation. However, improvements in high-strength material production techniques and component weight reduction are predicted to give lucrative opportunities in the upcoming years.

Based on the Vehicle Type, the Automotive Adhesives And Sealants Market is segmented into Commercial vehicles, Passenger vehicles. The commercial vehicle held the largest market share in 2022. Commercial vehicles are increasingly using automotive adhesion materials as they are often custom-designed to meet a variety of needs, including utility operations, emergency services, trash collection, and others, necessitating high-performance solutions. In medium and large commercial vehicles, sealants are used to stop leaks and water penetration. They are used to bond the trailer bed, the wall skin, and the internal bracket to the frame.

Based on the Vehicle Type, the Automotive Adhesives And Sealants Market is segmented into Commercial vehicles, Passenger vehicles. The commercial vehicle held the largest market share in 2022. Commercial vehicles are increasingly using automotive adhesion materials as they are often custom-designed to meet a variety of needs, including utility operations, emergency services, trash collection, and others, necessitating high-performance solutions. In medium and large commercial vehicles, sealants are used to stop leaks and water penetration. They are used to bond the trailer bed, the wall skin, and the internal bracket to the frame.

Passenger automobiles dominated the whole sector as a result of high sales figures in significant economies around the globe. According to OICA figures, sales of passenger vehicles increased by 4.8% between 2021 and 2022. This increase may be ascribed to growing disposable income in emerging countries, increased production levels in developed markets that are recovering, and technical developments at the OEM level, leading to higher, more efficient production.

Recent Development: Automotive Adhesives And Sealants Market

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 16 January 2026 | Henkel AG & Co. KGaA | Signed an agreement to acquire Swiss-based ATP Adhesive Systems, a specialist in high-performance water-based specialty tapes. | The acquisition expands Henkel's portfolio into sustainable, low-VOC bonding solutions for the automotive and electronics sectors, aligning with its 2030 sustainability targets. |

| 12 December 2025 | Henkel | Launched Loctite MS 9650, a next-generation silane-modified polymer adhesive engineered specifically for automotive display components. | This silicone-free and isocyanate-free formula enables lightweight vehicle assembly with superior UV and vibration resistance for modern integrated cockpit interiors. |

| 09 October 2025 | Honeywell & Magna International | Formed a strategic partnership to develop advanced sealant systems tailored for Electric Vehicles (EVs). | The collaboration focuses on solving critical thermal management and high-voltage sealing challenges, improving battery safety and longevity in next-gen EV platforms. |

| 01 July 2025 | Henkel Adhesive Technologies | Opened a new specialized automotive adhesive warehouse in Chakan, Pune, to support the growing Indian mobility market. | The facility optimizes Just-in-Time (JIT) deliveries for regional OEMs, enhancing supply chain efficiency for structural bonding and sealing applications. |

| 12 June 2025 | Sika AG | Invested €50 million to expand its automotive adhesive manufacturing facility in Hungary. | This expansion boosts annual production capacity by 40,000 tons, directly addressing the surge in European demand for lightweighting materials in vehicle production. |

| 05 February 2025 | LG Chem & HL Mando | Entered a joint development collaboration to create specialized adhesives for automotive electronic components. | This partnership aims to secure a dominant position in the autonomous driving sensor and controller market through high-reliability bonding solutions. |

Automotive Adhesives And Sealants Market Regional Insights:

The Asia Pacific region dominated the market with 45% share in 2022. Applications including paper and packaging, health and hygiene, consumer goods and construction will all see growth in the global adhesives & sealants market from 2021 to 2022. This growth is due to a variety of factors, including the rising global population, technological development, and general increases in purchasing power. This is particularly true for the Asia Pacific region, which is expected to use adhesives & sealants the most over the forecast period. The market for adhesives and sealants in the Asia Pacific is expected to grow at the greatest rate during the next five years. The present global health crisis has led to an increase in demand for medical and hygiene items such as PPE, medical supplies, masks, ventilators, personal hygiene products, and paper goods.

The use of automotive adhesives and sealants is growing in the area as a result of the rise in demand for lightweight automobiles and the sizable automotive manufacturing industry in countries such as China, India, and Japan.

The Organization Internationale des Constructeurs d'Automobiles (OICA) estimates that China produced 18,242,588 vehicles in the first nine months of 2022 compared to 16,976,248 in 2020.

On the plus side, the Chinese government is placing a lot of emphasis on expanding the nation's manufacturing and sale of electric cars. As a result, the nation intends to raise EV manufacturing to 2 million annually by 2020 and 7 million annually by 2025. Such patterns are anticipated to fuel the expansion of the Chinese automobile sector throughout the forecast period. Additionally, India's first-quarter vehicle production grew from 2,148,638 units in 2020 to 3,289,683 units in 2022. Additionally, the automotive sector has been observing a sustained movement in vehicle preferences, from two- to four-wheelers, which serves to increase the demand for passenger vehicles in the nation. This shift has been attributed to ongoing economic growth and growing salaries.

In terms of e-mobility, the Japanese government has increased EV subsidies and wants to install 150,000 EV charging stations by 2030. e-Mobility Power, a joint company created to build, manage, and run charging stations and related electrical infrastructure, has the support of the major OEMs. In order to address technical challenges, joint ventures and mergers among smaller suppliers are expected to increase in the future years. and raise more funding for R&D investment to boost the market growth. more micro-level analyses are covered in the report.

Automotive Adhesives And Sealants Market Scope: Inquire before buying

| Automotive Adhesives And Sealants Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 6.65 USD Billion |

| Forecast Period 2026-2032 CAGR: | 6.01% | Market Size in 2032: | 10.01 USD Billion |

| Segments Covered: | by Resin Type | Epoxy Acrylic Polyurethane Silicone SMP MMA Other Resins |

|

| by Application | Body in White Paint Shop Assembly Power train |

||

| by Vehicle Type | Passenger Cars Light Commercial Vehicles Other Vehicle Type |

||

| by End-Use | OEM (Original Equipment Manufacturer) Aftermarket |

||

Automotive Adhesives And Sealants Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Automotive Adhesives And Sealants Market, Key Players are:

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- B. Fuller Company

- The Dow Chemical Company

- PPG Industries Inc.

- Arkema S.A. (Bostik)

- DuPont de Nemours Inc.

- LORD Corporation

- Illinois Tool Works Inc.

- BASF SE

- Huntsman Corporation

- Wacker Chemie AG

- Jowat SE

- Permabond LLC

- Hernon Manufacturing Inc.

- Evonik Industries AG

- Solvay

- RPM International Inc.

- Covestro AG

- Unitech Limited

- Hubei Huitian New Materials Co. Ltd

- Yokohama Rubber (Hamatite)

- ThreeBond Holdings

- Ashland Global Holdings Inc.

- Delo Industrial Adhesives LLC

- Dymax Corporation

- Uniseal

- Avery Dennison Corporation

Frequently Asked Questions:

1] What segments are covered in the Global Automotive Adhesives And Sealants Market report?

Ans. The segments covered in the Automotive Adhesives And Sealants Market report are based on Product Type and End User.

2] Which region is expected to hold the highest share in the Global Automotive Adhesives And Sealants Market?

Ans. The Asia Pacific region is expected to hold the highest share in the Automotive Adhesives And Sealants Market.

3] What is the market size of the Global Automotive Adhesives And Sealants Market by 2032?

Ans. The market size of the Automotive Adhesives And Sealants Market by 2032 is expected to reach US$ 10.01 Bn.

4] What is the forecast period for the Global Automotive Adhesives And Sealants Market?

Ans. The forecast period for the Automotive Adhesives And Sealants Market is 2026-2032.

5] What was the market size of the Global Automotive Adhesives And Sealants Market in 2025?

Ans. The market size of the Automotive Adhesives And Sealants Market in 2025 was valued at US$ 6.65 Bn.