Automated Fare Collection Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2034

Overview

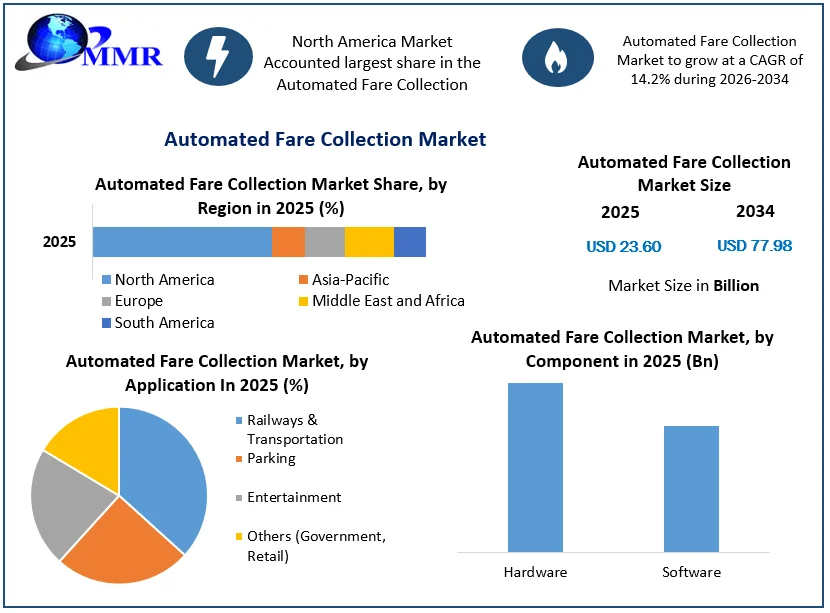

The Automated Fare Collection Market size was valued at USD 23.60 Billion in 2025 and the total Automated Fare Collection revenue is expected to grow at a CAGR of 14.2% from 2026 to 2034, reaching nearly USD 77.98 Billion.

Automated Fare Collection (AFC) refers to a comprehensive system used in public transportation networks to automate the fare payment process for passengers. The primary objective of AFC systems is to streamline and simplify the collection of fares, making it more efficient, convenient, and secure. Typically implemented in buses, trains, subways, and other modes of public transportation, AFC systems utilize advanced technologies such as contactless smart cards, near field communication (NFC), mobile applications, and other electronic payment methods.

The Automated Fare Collection (AFC) market is experiencing significant growth and transformation, driven by advancements in technology, urbanization, and the increasing emphasis on efficient public transportation systems. The current scenario is marked by a rising demand for seamless and contactless fare payment solutions, fueled by the need for enhanced passenger convenience and operational efficiency. Factors such as the integration of near field communication (NFC) and smart card technologies, coupled with the widespread adoption of mobile-based payment systems, are shaping the market landscape.

Automated Fare Collection Market Growth and Share Analysis

To know about the Research Methodology :- Request Free Sample Report

The growth of smart cities and the expansion of public transportation networks are contributing to the increased deployment of AFC systems globally. Key players in the mar Automated Fare Collection Market, such as Thales Group, Cubic Corporation, and NXP Semiconductors, are actively involved in strategic developments, including product launches and partnerships, to stay competitive. For instance, Thales Group's expertise in contactless payment solutions and Cubic Corporation's innovations in fare collection technologies showcase the industry's commitment to providing cutting-edge solutions. The ongoing trend towards digitalization and the integration of advanced analytics for data-driven insights further underline the dynamic nature of the Automated Fare Collection Market, positioning it as a pivotal component in shaping the future of modern urban mobility.

Automated Fare Collection Market Dynamics:

Government Initiatives and Investments Driving Automated Fare Collection Market Evolution

Technological advancements, exemplified by the integration of contactless smart cards and mobile-based payment systems, such as London's Oyster card or Hong Kong's Octopus card, enhance user experience and stimulate Automated Fare Collection Market growth. The rise of smart cities and increasing urbanization initiatives worldwide fuels the demand for efficient public transportation solutions, making AFC systems integral to optimizing fare collection processes, as seen in Singapore's comprehensive transport infrastructure. Additionally, the global shift towards contactless payment methods, accelerated by the COVID-19 pandemic, further drives AFC adoption, as illustrated by Transport for London's contactless payment system. Government initiatives and investments in public transportation infrastructure, like India's National Common Mobility Card (NCMC) in metro systems, play a pivotal role in fostering Automated Fare Collection Market development. Improved passenger experiences, facilitated by quick and hassle-free fare transactions, are evident in systems like Hong Kong's Octopus card, emphasizing the positive impact on Automated Fare Collection Market demand.

Data-driven decision-making, supported by AFC systems providing valuable insights, is exemplified by London's analytics-driven optimizations in route planning and infrastructure investments. The integration of AFC with multi-modal transportation, seen in Tokyo's Suica card system, responds to the demand for seamless fare solutions in diverse transportation environments. Security and fraud prevention features, as demonstrated by Chicago's Ventra system, contribute to the Automated Fare Collection Market growth by addressing concerns and building trust among users. The focus on environmental sustainability, such as Stockholm's Green Card initiative promoting eco-friendly travel through AFC, aligns with the industry's commitment to sustainable transport solutions and stimulates market growth. Additionally, global events and mega projects like the FIFA World Cup in Qatar drive the adoption of advanced fare collection solutions, highlighting the Automated Fare Collection Market responsiveness to large-scale transportation needs during such occasions.

Addressing Ticketing Abuse Strategies to Combat Fraud in Automated Fare Collection Market

One prominent obstacle is the persistent concern over security vulnerabilities and cyber threats. The digitization of payment methods in AFC systems increases the risk of unauthorized access and potential breaches. An illustrative example is the cyberattack on San Francisco's Municipal Transportation Agency in, highlighting the urgency for robust cybersecurity measures to safeguard AFC infrastructures and maintain the trust of both authorities and passengers. Another significant restraint lies in the high initial implementation costs associated with AFC systems. The substantial upfront investment required for hardware, software, and infrastructure development poses a financial barrier, impacting the swift adoption of these advanced fare collection technologies. A case in point is New York City's OMNY contactless payment system, which faced delays in its rollout due to financial constraints, emphasizing the challenges in overcoming the initial cost hurdle.

The integration of Automated Fare Collection Market systems with existing legacy infrastructure poses a complex challenge for many transportation networks. The coexistence of traditional fare collection methods and new AFC technologies, as observed in cities like Boston with the CharlieCard system, creates integration challenges. The transition from legacy systems to modernized AFC solutions demands meticulous planning and execution to ensure a seamless user experience and maintain operational efficiency.

Resistance to change and the need for extensive user education are additional hurdles in the AFC market. Both transportation authorities and passengers may resist the shift from conventional fare methods to automated systems. In Rome, for instance, the introduction of AFC systems faced public backlash, underscoring the importance of effective change management and user education strategies to facilitate a smooth transition and foster Automated Fare Collection Market growth.

Privacy concerns and data protection issues pose ethical challenges in the Automated Fare Collection Market. The collection of personal data through these systems raises privacy concerns among users. A notable example is the controversy surrounding London's Oyster card, where data usage practices were scrutinized, emphasizing the delicate balance needed between collecting operational data for efficiency and respecting user privacy.

Operational reliability and downtime issues present ongoing challenges. Events such as technical glitches experienced by Singapore's transit system, which affected the use of contactless payment cards, underscore the critical importance of system reliability. Continuous efforts are required to minimize disruptions and maintain seamless service, as operational issues can erode user confidence and hinder Automated Fare Collection Market growth.

Navigating diverse regulatory frameworks across regions and countries is an intricate challenge for AFC providers. Varying standards and compliance requirements, as seen in the European Union, demand constant adaptation. Regulatory compliance challenges can impede the seamless progression of AFC systems, necessitating a nuanced approach to navigate the intricate web of regional regulations in Automated Fare Collection Market.

Accessibility and inclusivity concerns are significant challenges in the AFC market. Ensuring that AFC systems are accessible to individuals with disabilities or those without smartphones is crucial for widespread adoption. Instances where certain user groups, such as the visually impaired community in some cities, face challenges emphasize the need for inclusive design and accessibility features in AFC systems. Addressing fraudulent activities and ticketing abuse remains an ongoing battle for the AFC market. The potential for ticket cloning or misuse poses threats to the integrity of these systems. Incidents of fare evasion, as observed in cities like Sydney, underscore the continuous efforts required to implement advanced authentication measures and curb fraudulent practices effectively for Automated Fare Collection Market.

Smart Cities, Smart Transportation: AFC's Crucial Role in Urban Efficiency Drives Automated Fare Collection Market

One of the primary growth opportunities lies in the continued advancements in contactless technologies. The widespread adoption of Near Field Communication (NFC) and mobile-based payment solutions has transformed fare transactions, offering passengers a seamless and convenient payment experience. Examples like London's Oyster card and Hong Kong's Octopus card showcase the success of contactless systems in enhancing user convenience. The AFC market can further capitalize on this trend by innovating in contactless technologies, exploring possibilities such as wearables or biometric authentication to redefine the landscape of fare collection.

Integration with Mobility-as-a-Service (MaaS) platforms emerges as a strategic growth avenue. The concept of MaaS involves seamlessly connecting various modes of transportation under a unified platform, allowing users to plan, book, and pay for their entire journey through a single application. Cities like Helsinki have pioneered MaaS initiatives, providing a glimpse into the future of integrated urban mobility. AFC providers can align themselves with this trend by integrating their systems into MaaS platforms, becoming integral components of comprehensive urban transportation solutions.

Enhanced data analytics capabilities represent a growth frontier for AFC providers. The data generated by fare transactions holds immense potential for optimizing transportation operations. London's use of AFC data analytics to improve route planning and operational efficiency serves as a testament to the power of data-driven decision-making. AFC providers can further invest in advanced analytics tools to extract valuable insights, not only improving operational efficiency but also providing transportation authorities with actionable data for better planning and resource allocation.

The global embrace of smart city initiatives provides a fertile ground for AFC market growth. Smart cities leverage technology to enhance the efficiency and sustainability of urban services, including transportation. In smart cities like Singapore, AFC technologies play a crucial role in optimizing public transportation systems. As more cities worldwide transition towards becoming smart, AFC providers can position their solutions as indispensable components in the development of technologically advanced urban environments.

Innovations in fare pricing models offer a unique opportunity for market growth. Dynamic pricing strategies, where fares adjust based on demand and congestion levels, have been successfully implemented in cities like Stockholm. AFC providers can explore and introduce flexible pricing structures that respond to real-time conditions, aligning with the evolving needs of both transportation authorities and passengers. This flexibility not only improves revenue management but also enhances the overall user experience.

Collaborations with emerging technologies present avenues for innovation in the AFC market. Integrating technologies like blockchain and artificial intelligence (AI) can enhance security, transparency, and operational efficiency. Pilot projects, such as the one in Guangzhou, China, exploring blockchain in fare transactions, highlight the potential for increased security and trust. AI applications can optimize predictive maintenance, ensuring the continuous functionality of AFC systems. By staying at the forefront of technological advancements, AFC providers can drive innovation within the market.

Inclusive design for diverse user groups is a critical growth opportunity. Ensuring that AFC systems are accessible to individuals with disabilities or those without smartphones is essential for widespread adoption. Initiatives in cities like Barcelona, where inclusive design considerations are prioritized, serve as examples of creating solutions that cater to diverse user needs. This inclusivity not only broadens the user base but also positions AFC systems as integral components of accessible and equitable transportation solutions.

Expansion into emerging markets with evolving transportation infrastructures offers a strategic growth avenue. Regions like Latin America or Southeast Asia, where urbanization and transportation development are on the rise, present opportunities for AFC providers to establish their solutions as fundamental components of burgeoning transportation networks. By catering to the specific needs and challenges of emerging markets, AFC providers can penetrate new regions and contribute to the development of robust transportation ecosystems.

Customization for multi-modal integration is another key growth opportunity. As cities increasingly adopt integrated multi-modal transportation systems, AFC solutions that seamlessly integrate with various modes of transportation become essential. Tokyo's Suica card system exemplifies the demand for customized AFC systems that offer passengers a unified and convenient payment experience across diverse transportation options. By focusing on multi-modal integration, AFC providers can address the evolving needs of modern urban commuters.

The focus on environmental sustainability presents an opportunity for AFC providers to align their solutions with global sustainability goals. Transitioning towards eco-friendly practices, such as the use of reusable smart cards in Vancouver, reflects a growing awareness of environmental impact. AFC providers can contribute to sustainability initiatives by implementing green practices, such as reducing the use of disposable tickets or cards, thereby appealing to environmentally conscious consumers and contributing to Automated Fare Collection Market growth.

Automated Fare Collection Market Segment Analysis:

Based on technology, the market has been divided into Smart Cards, Near Field Communication (NFC), and Magnetic Stripe. Among these, the Smart Cards sub-segment is projected to generate the maximum revenue. The Smart Cards sub-segment witnessed the highest revenue in 2025. The Smart Cards sub-segment, being the revenue leader in the Automated Fare Collection (AFC) Market in 2024, plays a pivotal role in revolutionizing public transportation systems globally. Smart cards are contactless payment methods embedded with secure chips, facilitating seamless fare transactions. These cards serve as digital wallets for commuters, allowing them to effortlessly access various modes of transportation, from buses and trains to subways. The importance of smart cards in AFC lies in their ability to streamline fare collection, enhance passenger convenience, and contribute to the overall efficiency of transportation networks. By providing a secure and efficient means of payment, smart cards significantly reduce boarding times, minimize cash handling, and contribute to the transition towards cashless and digitized public transit experiences, ultimately shaping the future of urban mobility which boost Automated Fare Collection Market.

Automated Fare Collection Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2025 | Conduent Incorporated | Conduent launched its next-generation cloud-based contactless Automated Fare Collection (AFC) platform designed for regional transit authorities. | The system significantly reduces hardware maintenance costs while offering seamless account-based ticketing (ABT) across multi-modal transit networks. |

| 12 May 2025 | Cubic Corporation | Cubic Transportation Systems partnered with a major European metropolitan transit operator to deploy an open-payment AFC gate architecture supporting cEMV cards and mobile wallets. | The deployment accelerates the transition to frictionless fare validation, expanding passenger throughput during peak hours by 25%. |

| 18 September 2025 | Thales Group | Thales integrated AI-driven biometric validation into its turnstile ticket barriers for high-density metro operations. | This advancement improves passenger processing speed and strengthens security measures against fare evasion. |

| 10 November 2025 | Scheidt & Bachmann | Scheidt & Bachmann unveiled its new FareGo suite expansion featuring real-time dynamic pricing and integrated Mobility-as-a-Service (MaaS) API modules. | It enables public transit operators to offer flexible, personalized fare structures and integrate seamlessly with third-party micromobility providers. |

| 20 February 2026 | NXP Semiconductors | NXP introduced its latest MIFARE DESFire EV3 smart card IC, tailored for secure and ultra-fast contactless AFC transaction processing. | The chip enhances cybersecurity protocols and guarantees interoperability across smart city transport infrastructures globally. |

Automated Fare Collection Market Scope: Inquire before buying

| Automated Fare Collection Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 23.60 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 14.2% | Market Size in 2034: | USD 77.98 Bn. |

| Segments Covered: | by Technology | Smart Cards Near Field Communication (NFC) Magnetic Stripe |

|

| by Component | Hardware Software |

||

| by System | Ticket Vending Machine (TVM) Ticket Office Machine (TOM) Fare Gates IC Cards |

||

| by Application | Railways & Transportation Parking Entertainment Others (Government, Retail) |

||

Automated Fare Collection Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Automated Fare Collection Market Key players

The Global Automated Fare Collection Market encompasses the ecosystem of hardware, software, and services used to automate ticketing and fee payments in public transportation networks (such as subways, buses, and trains).

| Company | Headquarters | Core Competencies |

| Cubic Corporation | San Diego, California, USA | Automated fare collection systems, transit ticketing, smart mobility solutions |

| Conduent, Inc. | Florham Park, New Jersey, USA | Automated fare collection, transit payment systems, tolling |

| Scheidt & Bachmann GmbH | Mönchengladbach, Germany | Fare collection systems, validators, ticket vending machines |

| Thales Group | Meudon, France | Smart ticketing, AFC, transport payment solutions |

| Siemens AG | Munich, Germany | Rail automation, fare collection, intelligent transport systems |

| Indra Sistemas, S.A. | Alcobendas, Spain | AFC platforms, intelligent transport systems |

| INIT SE | Karlsruhe, Germany | Public transport IT, fare collection, fleet management |

| Flowbird Group | Besançon, France | Ticketing, contactless fare collection, parking payment systems |

| Vix Technology | Sydney, Australia | AFC software, ticketing, transit payment platforms |

| Masabi Ltd. | London, United Kingdom | Mobile ticketing, cloud-based fare collection |

| Littlepay | Melbourne, Australia | Open-loop contactless fare payment |

| Genfare (SPX Technologies) | Elk Grove Village, Illinois, USA | Fareboxes, validators, AFC equipment |

| AEP Ticketing Solutions | Soest, Netherlands | Smart ticketing, AFC software |

| Omron Corporation | Kyoto, Japan | Automatic fare gates, ticket validators |

| Nippon Signal Co., Ltd. | Tokyo, Japan | AFC gates, railway ticketing systems |

| NEC Corporation | Tokyo, Japan | Smart ticketing, AFC, biometric transport systems |

| Hitachi Rail | London, United Kingdom | Rail ticketing, AFC, mobility solutions |

| Huawei Technologies Co., Ltd. | Shenzhen, China | Smart transportation, AFC infrastructure |

| LG CNS Co., Ltd. | Seoul, South Korea | Smart mobility, AFC integration |

| Samsung SDS | Seoul, South Korea | Smart transportation platforms, digital fare systems |

| GMV Innovating Solutions | Madrid, Spain | Public transport ticketing, AFC software |

| Xerox Transportation Solutions (Conduent) | Florham Park, New Jersey, USA | Transit fare collection systems |

| TransCore | Nashville, Tennessee, USA | Electronic tolling, transit payment systems |

| NXP Semiconductors N.V. | Eindhoven, Netherlands | NFC chips, secure transit payment ICs |

| STMicroelectronics N.V. | Geneva, Switzerland | Secure microcontrollers, contactless payment ICs |

| HID Global | Austin, Texas, USA | Smart cards, ticketing credentials, secure access |

| Visa Inc. | San Francisco, California, USA | Open-loop transit fare payments |

| Mastercard Incorporated | Purchase, New York, USA | Contactless transit payment solutions |

| CPI Card Group Inc. | Littleton, Colorado, USA | Contactless transit smart cards |

| Calypso Networks Association | Brussels, Belgium | Open fare collection standards and interoperable ticketing |

Frequently Asked Questions:

1] What segments are covered in the Global Automated Fare Collection Market report?

Ans. The segments covered in the Automated Fare Collection Market report are based on Technology, Component, System, and Application.

2] Which region is expected to hold the highest share in the Global Automated Fare Collection Market?

Ans. The North America region is expected to hold the highest share in the Automated Fare Collection Market.

3] What is the market size of the Global Automated Fare Collection Market by 2034?

Ans. The market size of the Automated Fare Collection Market by 2034 is expected to reach USD 77.98 Billion.

4] Who are the top key players in the Automated Fare Collection Market?

Ans. Thales Group (France), Cubic Corporation (United States), and NXP Semiconductors (Netherlands)are the top key players in the Automated Fare Collection Market.

5] What was the Global Automated Fare Collection Market size in 2025?

Ans: The Global Automated Fare Collection Market size was USD 23.60 Billion in 2025.