Artificial Intelligence in Agriculture Market Size by Technology, Component, Deployment Mode, Enterprise Type, Application, End User and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

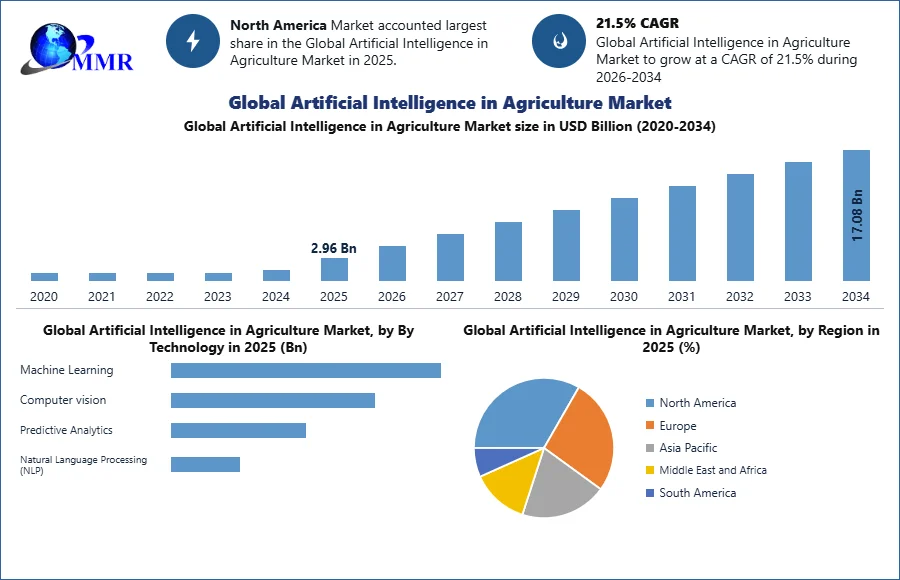

The Artificial Intelligence in Agriculture Market size was valued at USD 2.96 Billion in 2025, and the total revenue is expected to grow at a CAGR of 21.5 % from 2025 to 2034, reaching nearly USD 17.08 Billion.

The MMR report provides analysis of the Artificial Intelligence in Agriculture market by covering the regulatory and policy landscape, including global regulations, data privacy, cybersecurity, regional policy support, and certification standards for AI solutions. It evaluates pricing and market economics, with detailed pricing trends by technology, ROI and value proposition assessment, total cost of ownership, regional price comparisons, and the impact of government incentives and subsidies on adoption. The report further examines AI adoption and maturity levels across farm sizes and regions, highlighting readiness, barriers, productivity impacts, and sustainability outcomes. In addition, it delivers deep insights into the technological and innovation landscape, tracking emerging AI advancements, R&D initiatives, and strategic collaborations shaping agricultural productivity. The study also analyzes investment and funding trends, including venture capital, private equity, government funding, and M&A activity. Finally, it presents real-world use cases and implementation insights, showcasing practical applications, ROI outcomes, best practices, and challenges associated with deploying AI solutions across farming and agro-tech ecosystems.

The use of advance technological solutions to make cultivation more efficient, remains one of the greatest requirements. While, AI sees many direct use across sectors, i.e. AI-powered solutions will not only empower farmers to do better with less, it will also increase quality and assure faster go to market for crops. The report directed towards how AI can transform the agriculture landscape, the use of drone-made image processing techniques, exactitude farming landscape, the future of agriculture, challenges and overall Artificial Intelligence in Agriculture market position in forecast period.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Artificial Intelligence in Agriculture Market Scope

Agriculture is seeing prompt implementation of AI and Machine Learning (ML) both in terms of agricultural products and in-field agriculture techniques. Intellectual computing in specific, is all set to become the most disruptive technology in agriculture service sector as it can understand, learn, and respond to different circumstances to rise efficacy. Providing some of these solutions as a service such as chatbot or other conversational platform to all the farmers will help them keep pace with technological innovations as well as apply the same in their day-to-day farming to obtain the benefits of this service. Now, Microsoft is working with 175 farmers in India to deliver counselling services for sowing, land and fertilizer. This initiative has previously resulted in 30% higher yield per hectare on an average compared to last year.

Artificial Intelligence in Agriculture Market Industry Dynamics

Drivers

Growth driven by IOT

Large volumes of data get produced every day together with structured and unstructured format. These re-count to data on historic weather pattern, soil reports, new research, rainfall, pest invasion, images from drones and cameras. Intellectual IOT solutions can sense all this data and deliver strong perceptions to increase yield. Proximity Sensing and Remote Sensing are two technologies which are mainly used for intelligent data fusion. This supports in soil characterization based on the soil below the surface in a specific place. Hardware solutions like Rowbot are already coupling data collecting software with robotics to formulate the best fertilizer for growing corns as well to other activities to maximize output.

Image-based insight generation

Exactitude farming is one of the maximum discussed areas in farming today. Drone-based images can support in in-depth field analysis, crop observing and scanning of fields. Computer vision technology, IOT and drone data can be collective to assure rapid actions by farmers. Feeds from drone image data can create alerts in real time to increase the speed of precision farming. Companies such as Aerialtronics have employed IBM Watson IoT Platform and the Visual Recognition APIs in commercial drones for image analysis in real time. More or less areas where computer vision technology can be put to utilization in Disease detection, Crop readiness identification, Field management, etc.

Health monitoring of crops

Remote sensing techniques together with hyper spectral imaging and 3d laser scanning are crucial to create crop metrics thru thousands of acres. It has the likely to lead in a revolutionary change regarding of how farmlands are observed by farmers both from time and effort outlook. This technology will also be utilized to monitor crops along their complete lifecycle containing report generation in case of anomalies.

Automation techniques in irrigation and enabling farmers

With regard to human intensive processes in farming, irrigation is one of the process. Machines trained on historic weather pattern, soil quality and kind of crops to be grown, can automate irrigation and amplify overall yield. With close to 65-75% of the world’s fresh water being utilized in irrigation, automation can assist to farmers for better management of their water problems.

Artificial Intelligence in Agriculture Market Challenges

Lack of familiarity with high tech machine learning solutions

However, AI offers huge opportunities for application in agriculture, there still exists a lack of awareness with high tech machine learning solutions in farms across most of the region in a globe. Introduction of farming to external factors like weather conditions, soil situations and existence of pests is relatively high. Similarly, AI systems also require a lot of data to train machines and to make accurate predictions.

Artificial Intelligence in Agriculture Market Segment Analysis

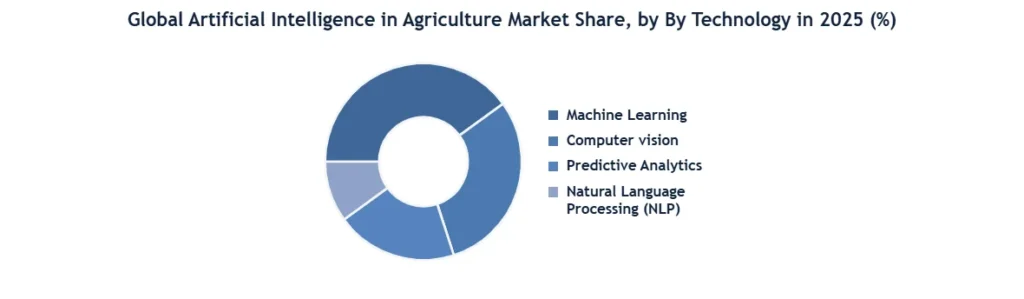

Based on the Technology, in 2025, Machine Learning dominates the Artificial Intelligence in Agriculture Market due to its widespread use in yield prediction, crop health monitoring, and precision farming decision-making. Computer Vision follows, driven by applications in crop disease detection, weed identification, and automated harvesting through drones and smart imaging systems. Predictive Analytics is gaining strong adoption for weather forecasting, demand planning, and resource optimization, supporting risk mitigation in farming operations. Natural Language Processing (NLP) plays a growing role in voice-enabled advisory platforms, farm management software, and multilingual farmer support systems, particularly in emerging economies. The Others segment, including robotics intelligence and expert systems, contributes to niche applications such as autonomous farm equipment and smart irrigation, supporting the gradual expansion of advanced AI capabilities across the agricultural value chain.

Based on Application, In 2025,Precision Farming segment dominated the AI in Agriculture Market. This is driven by the increasing adoption of AI-powered technologies for crop monitoring, precision irrigation, soil analysis, and yield optimization. Farmers are leveraging AI-based analytics and predictive insights to improve productivity, reduce input costs, and support sustainable farming practices.

Artificial Intelligence in Agriculture Market Trends

Agricultural Drones to Amplify the Growth of the Market

As global population anticipated to reach over 9.8 billion by 2050, agricultural consumption is anticipated to rise by a massive 75%, where drones have now been mainstreamed for smart farming supporting farmers in a range of tasks from analysis and planning to the real planting of crops, and the ensuing observing of fields to determine health and growth. Also, drones prepared with hyperspectral, multispectral, or thermal sensors are capable to detect areas that need changes in irrigation. Once crops have started growing, these sensors are capable to estimate their vegetation index, and indicator of health through AI, by determining the crop’s heat signature.

Artificial Intelligence in Agriculture Market Geographic Overview

North America dominated Artificial Intelligence in Agriculture Market in 2025. The growth of the market is attributed to the high selection of trend setting innovations and item in agriculture part. Asia Pacific is estimated to have high growth rate in the forecast period due to the rising demand from emerging nations, for instance, India and China. Also, rising adoption of mechanical technology and IoT devices in agriculture is additionally evaluated to drive the Artificial Intelligence in Agriculture market.

Europe is estimated to account for the largest market growth due to their farmers manage almost half of the land area for agriculture and it makes dominant industry in Europe. Trend in observing and reporting utensils for indoor and outdoor farms, and delivering a visualization of the farmer’s intact production using computer vision and AI are increasing the AI market in agriculture. The European Soil Data Centre (ESDAC) is the thematic center for soil associated data in Europe, where its goal is to be the single reference point for and to host all appropriate soil data and statistics at European level. AI firms are handling 'Internet of the Soil', which is a software and hardware solution for observing soil conditions like humidity, temperature, electrical conductivity, and more in European countries.

Their sensors connect wirelessly to a cloud-based platform where it can be retrieved by any internet connected device. Berlin-based InFarm has urbanized a vertical indoor farming system using IoT, Big Data, and cloud analytics, which can be employed in supermarkets, restaurants, local distribution warehouses, permitting businesses to grow their own fresh crop on site to deliver to customers. I The report covers the market leaders, followers and new entrants in the industry with the market dynamics by region. It will also help to understand the position of each player in the market by region, by segment with their expansion plans, R&D expenditure and organic & in-organic growth strategies. alliances and agreement in forecast period will give future course of action in the market to the readers. More than ten companies are profiled, benchmarked in the report on different parameters that will help reader to gain insight about the market in minimum time.

The objective of the report is to present a comprehensive analysis of the Global Artificial Intelligence in Agriculture Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that includes market leaders, followers and new entrants by Vehicle. PORTER, SWOT, PESTEL analysis with the potential impact of micro-economic factors by Vehicle on the market have been presented in the report.

External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers. The report also helps in understanding Global Artificial Intelligence in Agriculture Market dynamics, structure by analyzing the market segments and project the Global Artificial Intelligence in Agriculture Market size. Clear representation of competitive analysis of key players by Application, price, financial position, Product portfolio, growth strategies, and regional presence in the Global Artificial Intelligence in Agriculture Market make the report investor’s guide.

Recent Developments

- February 2025: John Deere continue to expand its AI-enabled precision agriculture portfolio by enhancing autonomous farming capabilities, integrating computer vision and machine learning to improve planting, spraying, and harvesting efficiency.

- January 2025: Google X spun out Heritable Agriculture, a startup using AI and machine learning to accelerate crop breeding, improve climate resilience, and optimize crop productivity through advanced genomic analysis.

- January 2025: Google Cloud partnered with the Government of Uttar Pradesh to launch an AI-powered Open Network for Agriculture, providing digital advisory, market access, financial services, and farm management solutions, demonstrating the growing adoption of AI-enabled agricultural ecosystems globally.

- July 2025: Farmers Business Network have received the funding of USD 50 million to expand its AI-powered digital agriculture platform and enhanced its "Norm" AI assistant with advanced crop marketing and agronomic decision-support capabilities.

Artificial Intelligence in Agriculture Market Scope : Inquire before buying

| Artificial Intelligence In Agriculture Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 2.96 USD Billion |

| Forecast Period 2026-2032 CAGR: | 21.5% | Market Size in 2034: | 17.08 USD Billion |

| Segments Covered: | by Component | Hardware Services Solution |

|

| by Technology | Computer Vision Machine Learning Predictive Analytics Natural Language Processing (NLP) Others |

||

| by Deployment Mode | Cloud On-premise Hybrid |

||

| by Enterprise Type | Large Small and Medium Enterprise (SMEs) |

||

| by Application | Agriculture Robot Crop and Soil Monitoring Weed Detection Livestock Health Monitoring Others |

||

| by End User | Farms & Agricultural Producers Agro-Tech Companies Agrochemical Companies Research Institutes Others |

||

Artificial Intelligence in Agriculture Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key players/Competitors profiles covered in the Artificial Intelligence in Agriculture Market report in strategic perspective

1. Deere Company

2. Microsoft Corporation

3. IBM Corporation

4. AWS

5. Global Agriculture

6. Bayer AG

7. Climate LLC.

8. Farmers Edge Inc.

9. Granular Inc.

10. AgEagle Aerial Systems Inc

11. Raven Industries Inc.

12. AGCO Corporation

13. Gamaya SA

14. Trimble Inc.

15. CropIn

16. Intello Labs

17.The Conservation Foundation

18. Fasal

19. Blue River Technology

20. Taranis

21. InData Labs

22. Itransition

23. Syngenta

24. Tule Technologies Inc.

25 EOS Data Analytics Ltd.

26 Agremo Ltd.

27 FarmWise Labs Inc.

28 Monarch Tractor Inc.

29 Evogene Ltd.

30. CropX Technologies

Others