Airline Technology Integration Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

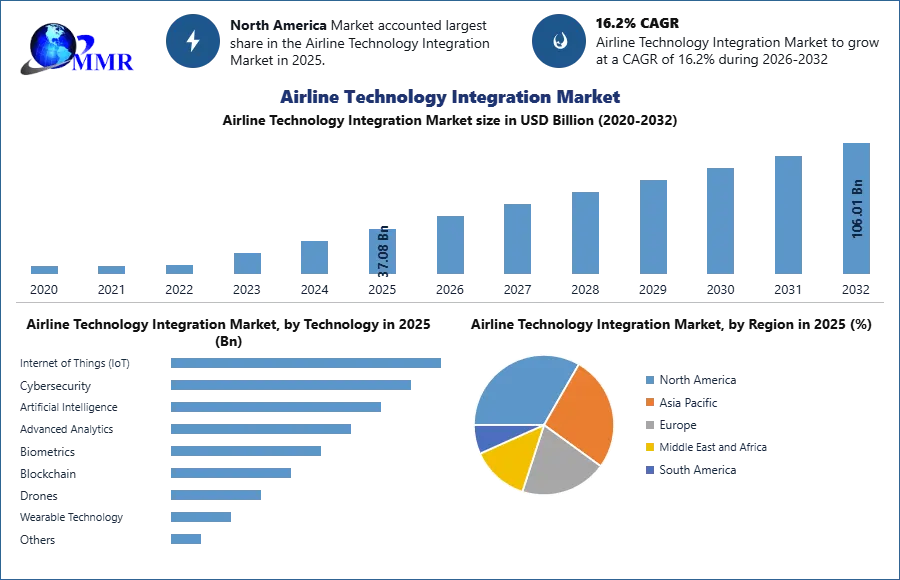

The Global Airline Technology Integration Market size was valued at USD 37.08 Billion in 2025 and the total Airline Technology Integration revenue is expected to grow at a CAGR of 16.2% from 2025 to 2032, reaching nearly USD 106.01 Billion.

Airline Technology Integration refers to the process of integrating various technologies and systems used in the aviation industry to enhance operational efficiency, improve customer experience, and optimize overall airline operations. It involves integrating software, hardware, and data systems to enable seamless communication, coordination, and automation across airline functions, such as reservations, ticketing, check-in, boarding, baggage handling, flight operations, and maintenance.

The Airline Technology Integration market is driven by several factors, including the increasing need for operational efficiency and cost optimization in the highly competitive airline industry, the growing demand for enhanced customer experience, the rising adoption of digitalization and automation, and the need for improved safety and security measures. Airlines are constantly seeking ways to streamline their operations, optimize resources, and enhance their services to gain a competitive edge, and technology integration plays a crucial role in achieving these goals.

The Airline Technology Integration market is characterized by a wide range of players, including technology providers, system integrators, software vendors, and service providers. These players offer a diverse array of solutions, including software platforms, hardware systems, data integration tools, connectivity solutions, analytics and business intelligence tools, and consulting and professional services related to technology integration in the aviation industry.

The Airline Technology Integration market is expected to grow steadily in the coming years, driven by increasing digitalization, automation, and connectivity trends in the aviation industry. The market is also expected to be influenced by emerging technologies such as the Internet of Things (IoT), artificial intelligence (AI), and data analytics, which have the potential to transform airline operations and customer experience. However, the high cost of integration, increasing security breaches, cyber-attacks, data breaches, and other security incidents are expected to restrict the market growth.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Airline Technology Integration Market Dynamics:

Increasing air travel demand across the world

The increasing demand for air travel is driven by various factors such as growing economic growth, rising disposable incomes, changing demographics, globalization of businesses, and increasing tourism. The increasing demand for air travel is placing a significant demand on airline technology integration. As more people travel for business or leisure purposes, there is a growing need for advanced technology solutions to enable seamless and efficient operations across various aspects of the aviation industry, including reservations and ticketing, flight operations, passenger services, baggage handling, security, etc. As a result, the growing demand for air travel all across the world is driving the need for advanced technology solutions to manage increasing passenger volumes, optimize capacity utilization, and improve operational efficiency, thereby driving the airline technology integration market.

Airline technology integration is crucial to meet the rising expectations of travelers for a seamless travel experience, streamline operations for airlines, and enhance safety and security measures. Thus, driving the airline technology integration market growth. Advanced technologies such as artificial intelligence (AI), the Internet of Things (IoT), data analytics, biometrics, and blockchain are being increasingly integrated into airline operations to improve efficiency, enhance the passenger experience, and optimize resources. For example,

1. AI-powered chatbots and virtual assistants are being used for customer service and support, helping airlines handle increasing volumes of inquiries and providing personalized assistance to travelers.

2. IoT sensors are being deployed in aircraft and airports to collect and analyze data in real time, enabling predictive maintenance, optimizing fuel consumption, and improving overall operational efficiency.

3. Biometric authentication technologies such as facial recognition and fingerprint scanning are being used for secure and seamless passenger identity verification at various touchpoints, including check-in, boarding, and security screening.

High Cost and Security Concerns

The high cost of airline technology integration is expected to restrain the growth of the airline technology integration market. Implementing and integrating new technologies in the airline industry involves significant costs, including software development, hardware infrastructure, system integration, training, and ongoing maintenance and support. This poses challenges for airlines, particularly those with budget constraints or limited financial resources, in justifying the investment in technology integration and may delay or limit the adoption of new technologies.

In addition, security concerns in the airline technology integration market are expected to be a potential threat to the growth and adoption of new technologies in the airline industry. The aviation industry is highly regulated and faces significant security challenges due to the sensitive nature of its operations, including passenger safety, cargo security, and protection of critical systems and data. Security breaches, cyber-attacks, data breaches, and other security incidents result in financial losses, reputational damage, operational disruptions, and legal and regulatory consequences, restraining the airline technology integration market.

The supply chain of technology solutions used in the airline industry can also pose security concerns. This includes software and hardware components provided by third-party vendors, suppliers, or partners. Vulnerabilities or compromises in the supply chain can potentially result in security breaches or compromise the integrity and security of the integrated technology solutions.

Insider threats, such as unauthorized access, misuse of privileges, or malicious activities by employees or contractors, are further expected to pose significant security risks to airline technology integration, thereby restraining the airline technology integration market growth. Insiders with privileged access to critical systems or sensitive data can potentially cause intentional or unintentional harm, resulting in security breaches or disruptions to operations. Proper access controls, monitoring, and auditing of privileged users are essential to mitigate insider threats.

Airline Technology Integration Market Segment Analysis:

Based on Technology, the Internet of Things (IoT) segment dominated the global airline technology integration market with the highest market share in terms of revenue in 2025. The Internet of Things (IoT) is a rapidly growing technology in the airline technology integration industry, as it has significant implications for the airline industry. IoT refers to the connection of physical devices, such as sensors, actuators, and other smart devices, to the Internet, allowing them to exchange data and communicate with each other.

In the airline industry, IoT is being used for various applications that enhance operational efficiency, improve safety, and enhance customer experience. IoT is rapidly transforming the airline industry by enabling real-time data collection, analysis, and decision-making, resulting in improved operational efficiency, enhanced safety, and enhanced customer experience. As technology continues to evolve, it is expected to play an increasingly significant role in the airline technology integration market, driving innovation and shaping the future of the industry.

The cybersecurity segment is expected to grow significantly and offer lucrative growth prospects for the airline technology integration market players. As airlines continue to embrace digitalization and leverage advanced technologies, the need for robust cybersecurity measures becomes paramount to safeguard against potential cyber threats and attacks. The airline industry is highly reliant on technology for various operations, including flight operations, reservations, passenger data management, and financial transactions.

As a result, airlines are vulnerable to cybersecurity risks, such as data breaches, ransomware attacks, and system disruptions, which have severe consequences, including financial losses, reputational damage, and disruption to operations. In recent years, there have been several high-profile cybersecurity incidents in the airline industry, which have highlighted the importance of robust cybersecurity measures. For instance,

In addition, the Artificial Intelligence (AI) segment is expected to witness lucrative growth through the forecast period. Artificial Intelligence (AI) is a rapidly growing technology that is being widely adopted in the airline industry for various applications within the realm of airline technology integration. AI has the potential to revolutionize the way airlines operate and provide services to their passengers. With continued advancements in AI technologies such as machine learning, deep learning, and natural language processing, airlines are expected to leverage AI to optimize their operations, enhance customer experiences, and drive revenue growth in the airline technology integration market.

AI-powered applications such as predictive maintenance, virtual assistants, personalized recommendations, and demand forecasting enable airlines to streamline their operations, improve decision-making, and deliver personalized and efficient services to passengers. Moreover, the use of AI in areas such as safety and security, risk management, and fraud detection helps airlines enhance safety measures and mitigate risks. As a result, AI in the airline technology integration market is expected to be transformative, with AI-driven solutions shaping the industry's landscape and driving innovation for improved operational efficiency and enhanced passenger experiences.

Airline Technology Integration Market Regional Insights:

North America dominated the Airline Technology Integration Market in 2025 and is expected to continue its dominance over the forecast period. The North American airline technology integration market is highly competitive and diverse, with a mix of global and regional providers offering a wide range of solutions to cater to the needs of the airlines in the region. Airlines in North America leverage technology to streamline their operations, enhance their revenue management, optimize distribution, and improve the overall customer experience to stay competitive in the dynamic airline industry landscape.

Major global providers such as Sabre, Amadeus, and Travelport have a strong presence in this region, serving both full-service and low-cost airlines, supporting the Airline Technology Integration market growth. Additionally, there are also smaller regional and specialized providers catering to the unique needs of the North American airline industry. The North American market has a significant presence of low-cost carriers (LCCs), and some specialized providers offer technology solutions tailored to the unique requirements of LCCs. For example,

Navitaire, a subsidiary of Amadeus, is a prominent provider of reservation, ancillary revenue, and revenue accounting solutions for LCCs in North America.

The United States is expected to lead the market with the highest market share by 2029. The United States, being one of the largest aviation markets in the world, has seen significant action and developments in the field of airline technology integration, supporting the airline technology integration market growth during the forecast period. The U.S. airline industry has been at the forefront of adopting and leveraging technology to enhance operations, improve customer experience, and optimize revenue management. For instance,

Adoption of Artificial Intelligence (AI) and Machine Learning (ML) technologies: U.S. airlines have been leveraging AI and ML technologies for various use cases, such as predictive maintenance of aircraft, demand forecasting, revenue optimization, personalized customer service, and baggage tracking. These technologies enable airlines to analyze vast amounts of data and derive insights for better decision-making and operational efficiency.

Implementation of Next Generation Air Transportation System (NextGen): The Federal Aviation Administration (FAA) has been leading the NextGen initiative, which aims to modernize the U.S. air traffic control system using advanced technologies to improve the safety, efficiency, and capacity of the national airspace. This includes the deployment of advanced avionics, communication, and navigation technologies on aircraft, as well as ground-based infrastructure for more efficient air traffic management.

Europe is another significant region for the airline technology integration market, with a mix of global and regional providers offering solutions to airlines. The European market is characterized by diverse airline business models, including legacy carriers, low-cost carriers, and regional airlines, which drive the demand for a wide range of technology solutions. Providers such as Amadeus, SITA, and Hitit Computer Services have a significant presence in Europe, along with local providers catering to specific regional markets.

The Asia Pacific region is experiencing rapid growth in the airline industry, with a significant increase in air travel demand. This has led to a growing need for airline technology integration solutions in the region, offering lucrative growth potential for the airline technology integration market players. Major global providers such as Sabre, Amadeus, and Travelport have a strong presence in Asia Pacific, along with regional providers such as Radixx International, Intelisys Aviation Systems, and Crane PAX. Local providers are also emerging to cater to the specific requirements of the diverse markets in the Asia Pacific region.

The APAC region has become a major hub for air travel, with increasing passenger volumes, growing airline fleets, and emerging low-cost carriers (LCCs) driving the demand for advanced technology solutions to streamline operations, optimize revenue management, and enhance customer experience, thereby driving the airline technology integration market growth.

Recent Developments

On September 2024 , Raytheon continued investing in advanced systems engineering and secure software platforms. Strategically, the company focuses on real-time operational systems and secure data environments. Its expertise in mission-critical computing and system reliability supports complex enterprise software ecosystems requiring high assurance and regulatory adherence.

On 10 October 2024, Accenture expanded digital transformation and AI consulting services. The firm emphasized cloud migration, system integration, and managed services. Strategically, Accenture supports enterprises through modernization of legacy systems and deployment of scalable digital platforms. Its advisory-led approach strengthens operational agility and data-driven decision-making.

November/December 2025, Amazon and Google launched a multicloud connectivity service to provide faster, private network links between cloud platforms. This development aids enterprise SaaS providers by improving cross-cloud performance and reliability, which supports sophisticated management platforms such as yacht management systems hosted in the cloud. Enhanced multicloud networking helps ensure uptime and data exchange across distributed services.

Airline Technology Integration Market Scope: Inquire before buying

| Airline Technology Integration Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 37.08 USD Billion |

| Forecast Period 2026-2032 CAGR: | 16.2% | Market Size in 2032: | 106.01 USD Billion |

| Segments Covered: | by Technology | Internet of Things (IoT) Cybersecurity Artificial Intelligence Advanced Analytics Biometrics Blockchain Drones Wearable Technology Others |

|

| by Offering | Software Hardware |

||

| by Deployment | On-Premise Cloud |

||

Airline Technology Integration Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key players/Competitors' profiles covered in the Yacht Management Software Market report in a strategic perspective

1.PERLE

2.Amadeus IT Group SA

3.SITA (Société Internationale de Télécommunications Aéronautiques)

4.Amazon Web Services, Inc.

5.Microsoft Corporation

6.Thales Group, Sabre

7.Honeywell International Inc.

8.Palo Alto Networks, Inc.

9.Raytheon Technologies Corporation

10.Accenture Plc.

11.Awery Aviation

12.Sabre Corporation

13.ForeFlight

14.Rusada

15.Swiss Aviation Software

16.Travelport

17.Radixx International

18.Hitit Computer Services

19.Intelisys Aviation Systems

20.Crane PAX

21.HitchHiker GmbH

FAQs:

1. What are the growth drivers for the Airline Technology Integration market?

Ans. The increasing need for operational efficiency and cost optimization in the highly competitive airline industry, the growing demand for enhanced customer experience, the rising adoption of digitalization and automation, and the need for improved safety and security measures are expected to be the major driver for the Airline Technology Integration market.

2. What is the major restraint for the Airline Technology Integration market growth?

Ans. High cost of integration, increasing security breaches, cyber-attacks, and data breaches are expected to be the major restraining factor for the Airline Technology Integration market growth.

3. Which region is expected to lead the global Airline Technology Integration market during the forecast period?

Ans. North America is expected to lead the global Airline Technology Integration market during the forecast period.

4. What is the projected market size & growth rate of the Airline Technology Integration Market?

Ans. The Global Airline Technology Integration Market size was valued at USD 37.08 Billion in 2025 and the total Airline Technology Integration revenue is expected to grow at a CAGR of 16.2% from 2025 to 2032, reaching nearly USD 106.01 Billion.

5. What segments are covered in the Airline Technology Integration Market report?

Ans. The segments covered in the Airline Technology Integration market report are Technology, Offering, Deployment, and Region.