Application Container Market Size by Service, Deployment Mode, Organization Size, Application Area, End User, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

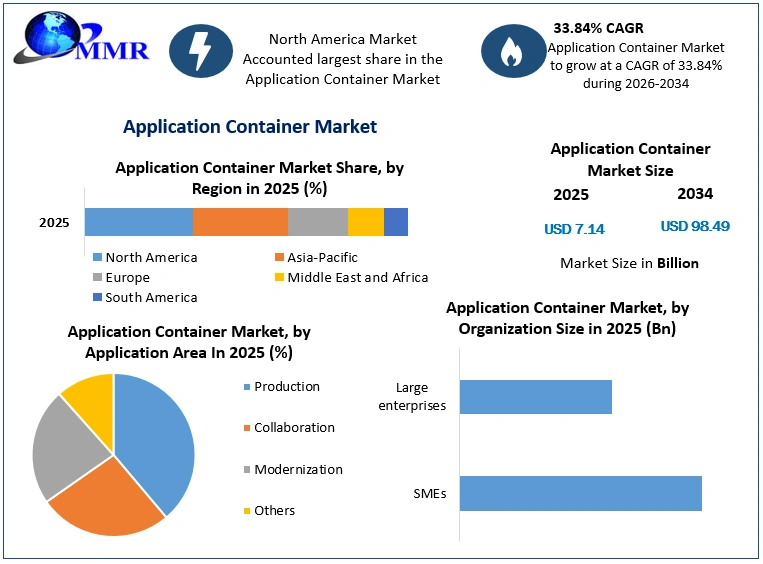

The Application Container Market size was valued at USD 7.14 Billion in 2025 and the total Application Container revenue is expected to grow at a CAGR of 33.84 % from 2026 to 2034, reaching nearly USD 98.49 Billion by 2034.

Application Container is self-contained software units containing application code, libraries, and dependencies, designed for universal execution across diverse environments, including desktops, traditional IT systems, and cloud platforms.

The Application Container Market is expected rapid growth, driven by the escalating demand for efficient and scalable software deployment solutions across diverse industries. With the increasing adoption of cloud computing and the need for agile application development, the market is witnessing a surge in prominence. The current scenario reflects a dynamic landscape, with Application Container Market key players such as Docker Inc., Red Hat, Inc., Google LLC, and Microsoft Corporation leading the charge. These industry giants are actively contributing to the Application Container Market growth through innovations and strategic collaborations. The Application Container Market growth is driven by factors such as the rising trend of microservices architecture, which emphasizes modular and independent components for application development, enhancing scalability and flexibility. The containerization technology's ability to streamline the deployment process, improve resource utilization, and facilitate seamless integration across various platforms has boosted its adoption globally. Organizations are increasingly recognizing the benefits of container orchestration tools like Kubernetes, contributing to the market's upward trajectory.

The Application Container Market competitive landscape is characterized by continual advancements and partnerships, exemplified by Docker Inc.'s introduction of Docker Enterprise 3.0, focusing on enhanced security and scalability features, reinforcing its position as a key player. Similarly, Red Hat, Inc. has made significant strides with OpenShift, a comprehensive Kubernetes platform, to address the evolving needs of enterprises in deploying and managing containerized applications. Google LLC, through Google Kubernetes Engine (GKE), and Microsoft Corporation, with Azure Kubernetes Service (AKS), are also pivotal in shaping the market dynamics. Recent developments indicate a shift towards containerization in edge computing and serverless architectures, expanding the market's reach. As the Application Container Market continues to evolve, the emphasis on container security, compliance, and management solutions is becoming more pronounced. The market is poised for sustained growth as businesses across sectors increasingly recognize the pivotal role of containerization in achieving operational efficiency, cost-effectiveness, and accelerated application delivery, solidifying the position of key players and fostering innovation in the rapidly advancing landscape.

Application Container Market Size, Growth & Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Application Container Market Dynamics:

The growing adoption of microservices architecture boost the use of containers for modular and independent application development

The increasing shift to cloud computing, where application containers play a pivotal role in meeting the dynamic resource scaling demands of businesses driving the growth of Application Container Market, for instance, Netflix harnesses the power of Docker containers to efficiently manage its extensive streaming services on the cloud. By optimizing resource utilization and enhancing scalability, Netflix exemplifies the transformative impact of application containers in addressing the challenges posed by large-scale cloud-based operations.

The increased adoption of microservices architecture further driving the Application Container Market growth. For example, Amazon's utilization of containerization through AWS Fargate underscores the advantages of microservices, showcasing how it achieves flexibility and efficient resource allocation. This exemplifies the pivotal role that application containers play in facilitating modern software development practices, aligning seamlessly with the growing emphasis on microservices. Containers streamline agile development methodologies, exemplified by Google's continuous integration and delivery platform, Google Cloud Build. Leveraging containers, Google Cloud Build enables organizations to execute rapid and reliable software development cycles. The Application Container Market is driven by the indispensable role that application containers play in DevOps practices, fostering collaboration between development and operations teams. Kubernetes, embraced by industry leaders like Spotify, stands out as an efficient container orchestration tool that facilitates seamless DevOps integration for continuous deployment, marking a critical milestone in the evolution of software development and deployment practices. Containers also optimize resource utilization, enabling more applications to run on a single host. Facebook's strategic use of Docker for containerization showcases how this approach enhances resource efficiency, reducing the infrastructure footprint and operational costs. Furthermore, the market is characterized by the inherent portability of containers, ensuring consistent application execution across diverse environments. Microsoft Azure's container service, AKS, is a prime example, allowing the seamless deployment and management of containerized applications across both on-premises and cloud infrastructures, providing organizations with unmatched flexibility and consistency. As the market continues to expand, the integration of containers into edge computing architectures and their seamless deployment across hybrid cloud environments, as demonstrated by Docker Edge and IBM Cloud Kubernetes Service, respectively, are pivotal factors driving the sustained growth of the Application Container Market.

Overcoming Container Networking Challenges for Seamless Communication in Service Discovery and Load Balancing for Market Growth

Security concern is emerging as a paramount challenge to the Application Container Market growth, as vulnerabilities within these containers pose the potential threat of exposing sensitive data. For instance, The Equifax breach in 2017, underlining the critical need for fortifying container security measures. This incident prompted the industry to reevaluate its approach, emphasizing the imperative of addressing potential threats and bolstering security frameworks to safeguard against unauthorized access and data breaches. Orchestrating and managing overabundance of containers introduces complexities, particularly evident in large-scale deployments. Instances of security lapses due to misconfigured Kubernetes settings underscore the challenge of streamlining orchestration practices. As organizations increasingly adopt containers, the industry grapples with a shortage of skilled professionals proficient in container technologies. This talent gap, observed during the initial stages of container adoption, necessitates focused training initiatives and educational programs to bridge the divide and ensure effective implementation. The scarcity of expertise presents a hurdle for businesses striving to maximize the benefits of containerization, hindering widespread adoption and the realization of full potential.

Compatibility issues across various container runtimes and orchestration platforms hinders the growth of Application Container Market. Docker and Kubernetes compatibility challenges underscore the importance of standardized practices and rigorous compatibility testing to ensure a cohesive and interoperable container ecosystem. Managing software licenses within containerized environments introduces complexities, as seen in instances of open-source license violations in containerized applications. Robust license management strategies become imperative to prevent legal ramifications and ensure compliance with licensing agreements. Containers may introduce resource overhead, impacting performance. Instances of resource contention due to excessive container proliferation underscore the importance of optimizing containerized applications for efficient resource utilization, striking a balance between performance and resource consumption. Ensuring regulatory compliance in containerized environments remains complex, particularly in industries such as finance and healthcare, where stringent regulatory requirements demand careful consideration of compliance frameworks and container security measures.

Application Container Market growth driven by Escalating Demand for Business Agility and Swift Time-to-Market

The accelerating demand for business agility and expedited time-to-market is a pivotal driver of market growth trends. In the competitive landscape, enterprises are increasingly recognizing the imperative of adopting cutting-edge technologies for developing and delivering modern applications, fostering coordination and growth. Legacy environments, acting as impediments to technological evolution, necessitate transformations in applications, platforms, and technology. Application containers emerge as catalysts in expediting the application development lifecycle, curtailing testing time, and simplifying testing processes to enhance agility. Container orchestration further facilitates the deployment of applications across diverse environments, encompassing physical or virtual, as well as public, private, or hybrid cloud infrastructures. This not only furnishes enterprises with a competitive edge but also translates into heightened efficiency, diminished application-related costs, and a more favorable Return on Investment (ROI), thereby propelling the market's Compound Annual Growth Rate (CAGR).

The imperative for collaboration in response to intensified competition mandates the adoption of new technologies and contemporary application design. Legacy settings, posing as obstacles to technology adoption, require comprehensive upgrades in applications, systems, and technology. Application containers play a pivotal role in expediting software development, mitigating complexity, reducing validation time, and enhancing overall agility. The streamlined process of installing applications through container orchestration, adaptable to various settings including physical, virtualized, public, private, and hybrid clouds, not only augments ROI but also confers a competitive advantage, ultimately reducing application costs.

In tandem with these market dynamics, numerous innovations are emerging as frontline technologies for businesses globally. The gradual integration of diverse technologies across the world underscores the pivotal role of the application container platform in harnessing the benefits of the Internet of Things (IoT). Application containers facilitate seamless application mobility across IoT devices, host switching, service registration, and accelerated application setup and upgrades. With minimal assistance and limited resource requirements for lightweight operating systems, application containers can efficiently run programs on IoT edge devices. The escalating need for frequent and efficient updates of IoT applications at scale propels the demand for application containers, thereby driving the revenue of the Application Container market.

Application Container Market Segment Analysis:

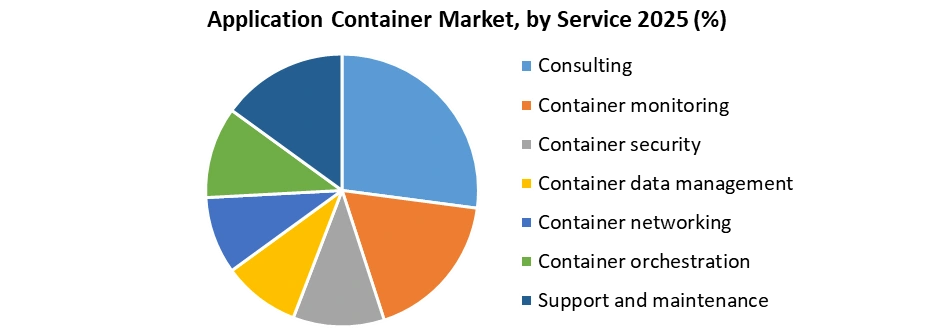

Based on Services, Consulting services segment dominated the Application Container Market in 2025 and is expected to maintain its dominance over the forecast period. It plays a pivotal role in guiding enterprises through the adoption and implementation of container technologies. Container monitoring services ensure the seamless operation of applications, tracking their performance and identifying potential issues. Container security services address the critical need for safeguarding containerized applications against cyber threats. Container data management services focus on efficiently handling and storing data within containers, enhancing overall data accessibility. Container networking services facilitate communication between containers, optimizing data flow. Container orchestration services streamline the deployment and management of containerized applications, promoting scalability and efficiency. Additionally, support and maintenance services are crucial for sustaining the continuous functionality of containerized environments. The comparative analysis of these services reveals their diverse applications and varying degrees of adoption, underscoring the multifaceted landscape of the Application Container Market.

Application Container Market Regional Insights:

The North American region dominated the Application Container Market in 2025 and is expected to maintain its dominance over the forecast period. The adoption of microservices architecture by enterprises stands out as a primary catalyst, providing a framework for scalable and agile application development. Simultaneously, the ongoing transformation of business-critical applications further propels market growth, as organizations pivot towards container technology to modernize and optimize their software infrastructure. This strategic shift is complemented by a steady influx of financial investments in container technology, fostering innovation and development within the ecosystem. Notably, the presence of a diverse array of small and large players in North America contributes to a dynamic landscape, offering myriad opportunities for market growth.

Cloud adoption has become a cornerstone of North America's influence on the application container market. The region has swiftly embraced cloud and related services, establishing an extensive network facilitated by major cloud service providers. This robust cloud infrastructure serves as a linchpin for the growth of containerized applications. Additionally, the heightened demand for DevOps practices in North America significantly contributes to market proliferation. DevOps adoption serves as a driving force behind the seamless integration and deployment of application containers, aligning with the region's tech-savvy landscape. As startups, including Bluedata, ClusterHQ, CoreOS, Docker, Sysdig, and Twistlock, thrive in the North American ecosystem, they inject innovation and competitiveness into the market. The region's commitment to developing and adhering to standards and guidelines for securing containerized infrastructure further solidifies its role as a trendsetter, shaping the trajectory of the global application container market.

Application Container Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 14 January 2025 | Red Hat | Red Hat launched OpenShift 4.17, featuring enhanced AI workload orchestration and optimized container management across hybrid cloud environments. | This upgrade accelerates enterprise AI deployment efficiency and reduces operational complexity for containerized cloud-native applications. |

| 18 March 2025 | Docker | Docker announced a strategic partnership with AWS to introduce Docker Build Cloud integrations for seamless developer container deployment. | The collaboration significantly boosts developer productivity by reducing local image build times by up to 39%. |

| 22 May 2025 | SUSE | SUSE unveiled Rancher Prime 3.1, delivering advanced multi-cluster management capabilities and strengthened zero-trust container security. | It enhances governance and security compliance for large-scale enterprise Kubernetes orchestration across edge and cloud environments. |

| 12 August 2025 | Mirantis | Mirantis acquired Shipa assets to expand its enterprise container ecosystem with automated application-centric deployment tools. | The acquisition simplifies developer workflows by decoupling application deployment from underlying Kubernetes infrastructure complexities. |

| 10 November 2025 | Google Cloud | Google Cloud deployed GKE Enterprise enhancements focusing on automated vulnerability scanning and real-time container runtime threat detection. | This roll-out elevates cloud security posture for enterprises running highly sensitive, containerized workloads at global scale. |

| 20 January 2026 | Microsoft | Microsoft launched Azure Container Apps Serverless GPU Support, enabling automated scaling for containerized deep learning and LLM inferencing. | The development optimizes compute cost efficiency by allowing companies to run containerized AI models without maintaining dedicated infrastructure. |

Application Container Market Scope: Inquiry Before Buying

| Application Container Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 7.14 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 33.84% | Market Size in 2034: | US $ 98.49 Bn. |

| Segments Covered: | by Service | Consulting Container monitoring Container security Container data management Container networking Container orchestration Support and maintenance |

|

| by Deployment Mode | Cloud On-premises |

||

| by Organization Size | SMEs Large enterprises |

||

| by Application Area | Production Collaboration Modernization Others |

||

| by End User | BFSI Healthcare and life science Telecommunication and IT Retail and e-commerce Education Media and entertainment Others |

||

Application Container Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Application Container Market Key Players:

Major Contributors in the Application Container Industry in North America:

1. Docker, Inc. - San Francisco, California, USA

2. Amazon Web Services (AWS) - Amazon ECS - Seattle, Washington, USA

3. Google Cloud Platform (GCP) - Google Kubernetes Engine (GKE) - Mountain View, California, USA

4. Microsoft Azure - Azure Kubernetes Service (AKS) - Redmond, Washington, USA

5. Red Hat, Inc. - OpenShift - Raleigh, North Carolina, USA

6. IBM - IBM Cloud Kubernetes Service - Armonk, New York, USA

7. VMware, Inc. - Tanzu - Palo Alto, California, USA

8. Rancher Labs, Inc. - Cupertino, California, USA

9. Mesosphere, Inc. (Now D2iQ) - Kubernetes - San Francisco, California, USA

10. Pivotal Software, Inc. (Acquired by VMware) - Palo Alto, California, USA

Leading players in the Europe Application Container Market:

1. Canonical Ltd. - Charmed Kubernetes - London, United Kingdom

2. SUSE - SUSE CaaS Platform - Nuremberg, Germany

3. SysEleven GmbH - Berlin, Germany

4. Amazic - Amsterdam, Netherlands

5. Storm Reply - Turin, Italy

6. Eficode - Helsinki, Finland

Key players driving the Asia-Pacific Application Container Market:

1. Alibaba Cloud (China)

2. Tencent Cloud (China)

3. Huawei Cloud (China)

4. Naver Cloud (South Korea)

5. NTT Communications (Japan)

6. SK Telecom (South Korea)

7. SAP Cloud Platform

8. Fujitsu Cloud (Japan)

9. NEC Corporation (Japan)

10. Infosys (India)

Frequently Asked Questions:

1] What Major Key players in the Global Application Container Market report?

Ans. The Major Key players covered in the Application Container Market report are Docker, Inc., Amazon Web series, Google Cloud, Red Hat, Inc., IBM.

2] Which region is expected to hold the highest share in the Global Application Container Market?

Ans. North America region is expected to hold the highest share in the Application Container Market.

3] What is the market size of the Global Application Container Market by 2034?

Ans. The market size of the Application Container Market by 2034 is expected to reach US$ 98.49 Billion.

4] What is the forecast period for the Global Application Container Market?

Ans. The forecast period for the Application Container Market is 2026-2034.

5] What was the market size of the Global Application Container Market in 2025?

Ans. The market size of the Application Container Market in 2025 was valued at US$ 7.14 Billion.