Anti-Drone Market by RF Jamming Systems, Directed Energy Weapons, Radar Detection, Acoustic Sensors, Electro-Optical/IR Systems, Fixed Installation, Mobile & Portable Units, AI-Powered Analytics, Drone Interception, Swarm Defense, Counter-UAS Software, Military-Grade, Commercial-Grade - Global Forecast to 2032

Overview

Global Anti-Drone Market Size and Growth Potential

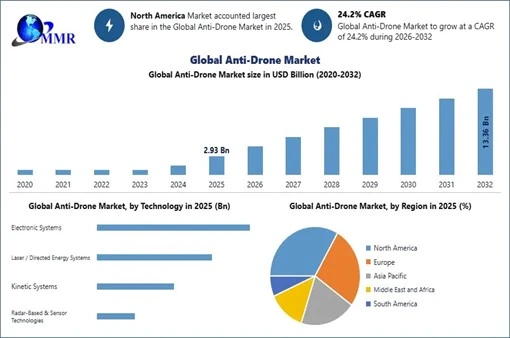

The Global Anti-Drone Market was valued at USD 2.93 billion in 2025 and is projected to reach USD 13.36 billion by 2032, registering a robust CAGR of 24.2% during the 2026–2032 forecast period. This rapid expansion is driven by an unprecedented surge in commercial and weaponized drone incidents globally, rising defense modernization budgets, and growing critical infrastructure protection mandates. North America dominated the market at USD 1.12 billion in 2025, fueled by heightened military deployments and Federal Aviation Administration (FAA)-aligned regulatory frameworks. The Asia Pacific region is the fastest-growing market, projected at a CAGR of 27.3%, with India, China, and South Korea driving state-level counter-unmanned aircraft system (C-UAS) investments. Globally, over 1,200 unauthorized drone incursions were reported at airports and government facilities in 2024 alone, reinforcing the urgency of scalable anti-drone infrastructure investments.

Anti-Drone Market Key Highlights

| Market Parameter | Value / Insight | Trend |

| Global Market Size (2025) | USD 2.93 Billion | ↑ Strong |

| Forecast Market Size (2032) | USD 13.36 Billion | ↑ Accelerating |

| Forecast CAGR (2026–2032) | 24.20% | ↑ High Momentum |

| Largest Regional Market (2025) | North America – USD 1.12 Bn (38%) | ↑ Dominant |

| Fastest Growing Region | Asia Pacific – CAGR 27.3% | ↑ Emerging Leader |

| Leading Product Segment | Hybrid / Integrated Systems | ↑ Rising Adoption |

| Top End-User Segment | Military & Defense | ↑ Expanding Budget |

| Key Enabling Technology | RF Detection + AI-Based Tracking | ↑ Converging |

| Number of Airport Incursions (2024) | 1,200+ Unauthorized Incidents Globally | ↑ Threat Escalating |

| Regulatory Framework Milestone | NATO C-UAS Strategy Framework (2023) | → Policy Shaping |

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Anti-Drone Market Ecosystem Map

The Anti-Drone Market ecosystem comprises a structured, multi-layered value chain spanning technology developers, system integrators, defense contractors, regulatory authorities, and end-user verticals. The following illustrative map represents the key participants and information flows across the ecosystem:

| Raw Material / HW Suppliers | Technology Developers | System Integrators | Service Providers | Regulatory Bodies | End Users |

| RF Chips, IR Sensors, Radar Modules | RF Jamming, Laser, AI/ML Platforms | Defense Prime Contractors | MRO, Training & Consulting | FAA, EASA, NATO, MoD | Military & Defense |

| Optical Sensors, EO/IR Cameras | Acoustic, Lidar, Net Guns | C-UAS Software Vendors | Cloud Analytics, SaaS | National Aviation Regulators | Critical Infrastructure |

| High-Power Microwave (HPM) Components | GPS Spoofing, Command & Control | Telecom & IT Integrators | R&D Labs, Testing Agencies | DHS, Homeland Security Depts. | Airports & Aviation |

Anti Drone Market DROCT Analysis (Drivers, Restraints, Opportunities, Challenges, and Trends)

Anti-Drone Market Driver: Escalating Drone Threat Incidents

A rapid rise in unauthorized drone incursions at airports, military installations, and public events is the primary demand catalyst for the Anti-Drone Market. In 2024, over 1,200+ unauthorized drone incidents were documented globally, with an estimated 40% increase in weaponized drone use in conflict zones. Governments and defense agencies are committing multi-year C-UAS procurement budgets, directly accelerating Anti-Drone Market revenues.

Anti-Drone Market Restraint: Regulatory Fragmentation Across Jurisdictions

The Anti-Drone Market faces significant deployment friction due to inconsistent national and regional regulations governing jamming, spoofing, and physical interception. In civilian airspace, electronic countermeasures are prohibited without explicit government authorization in many jurisdictions, including the EU and parts of Asia Pacific. This regulatory ambiguity delays commercial deployments at airports, stadiums, and industrial facilities, limiting total addressable market expansion for non-defense end-users.

Anti-Drone Market Opportunity 1: Critical Infrastructure Protection Mandates

Power grids, nuclear facilities, oil & gas pipelines, and water treatment plants are increasingly mandated by national security frameworks to implement drone detection perimeters. The US NDAA (2023), EU NIS2 Directive, and similar legislations are creating procurement obligations for infrastructure operators. This presents a substantial non-defense revenue stream within the Anti-Drone Market, estimated at USD 780 million by 2028.

AI-Integrated Autonomous C-UAS Platforms

The integration of AI/ML into C-UAS platforms — enabling autonomous threat classification, multi-drone swarm tracking, and real-time decision support — is creating a high-margin product tier within the Anti-Drone Market. AI-enabled platforms command 25–40% pricing premiums over conventional detection systems and are increasingly preferred by both military and commercial buyers seeking low human-intervention security architectures.

Anti-Drone Market Challenge: Rapid Drone Technology Evolution Outpacing C-UAS Capabilities

Commercial drones are advancing faster than countermeasure technologies, with FPV (First Person View) racing drones, encrypted control signals, and AI-assisted autonomous flight increasingly evading conventional RF-based detection and jamming systems. The Anti-Drone Market faces the persistent challenge of technology obsolescence cycles, requiring continuous R&D investment and platform upgradability to maintain operational effectiveness against next-generation drone threats.

Anti-Drone Market Trend: Shift Toward Layered Multi-Sensor C-UAS Architectures

The Anti-Drone Market is transitioning from single-sensor deployments to multi-layered, sensor-fused C-UAS architectures that combine radar, RF detection, EO/IR cameras, acoustic sensors, and AI command platforms into unified operational systems. NATO-aligned nations are standardizing on layered C-UAS frameworks, reinforcing demand for modular, interoperable, and upgradable system platforms from prime contractors and specialist integrators.

Anti-Drone Market Segment Analysis

By Product / System Type

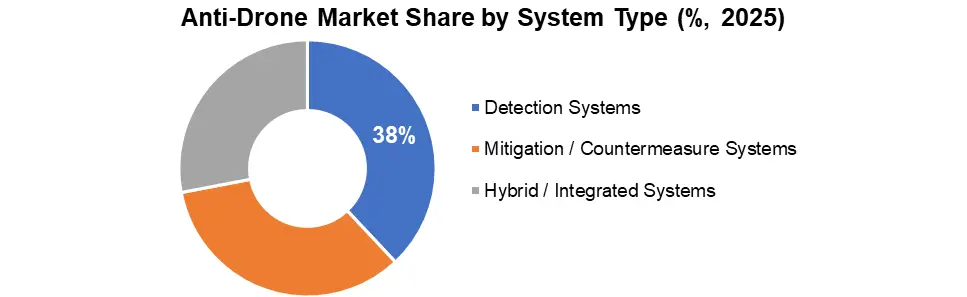

Detection Systems represent the foundational layer of the Anti-Drone Market, accounting for approximately 38% of total market revenue in 2025. These systems comprising RF analyzers, radar arrays, acoustic sensors, and EO/IR cameras are deployed as the first line of defense, providing essential situational awareness and enabling threat classification prior to countermeasure activation. Detection systems are experiencing strong adoption across both military and commercial segments, with AI-augmented detection platforms commanding significant price premiums.

Mitigation / Countermeasure Systems, including RF jammers, GPS spoofers, HPM weapons, directed energy (laser) platforms, and net-gun/interceptor drones, represent xx% of the Anti-Drone Market share and are projected to exhibit the highest growth potential. This sub-segment is expected to experience a CAGR of 26.8% through 2032, driven by the increasing need for active defense solutions against drone threats.

Hybrid / Integrated Systems, which combine detection and mitigation capabilities within unified command-and-control architectures, are the fastest-growing product category. These integrated platforms are projected to surpass USD XX billion by 2032. They are increasingly favored by defense agencies and critical infrastructure operators, who seek streamlined C-UAS operations with minimal manual intervention and greater operational efficiency.

By End-User / Industry Vertical

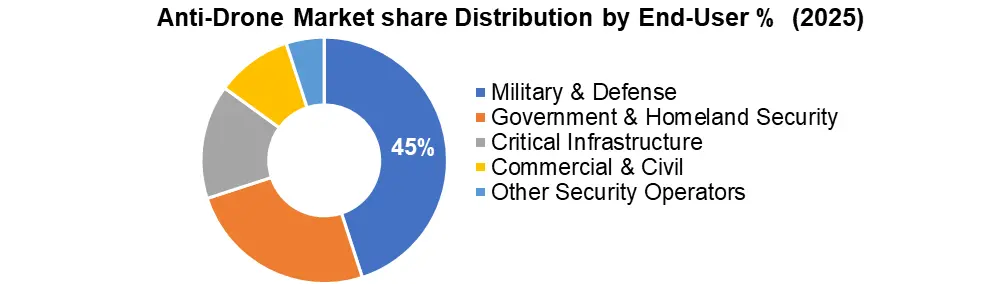

Military & Defense is the dominant end-user vertical in the Anti-Drone Market, representing approximately 45% of market revenue in 2025, driven by active military deployments in conflict zones, border protection mandates, and national defense modernization programs across the US, EU, India, South Korea, and Israel. Government & Homeland Security is the second-largest vertical, fueled by counter-terrorism imperatives, airport security requirements, and critical event protection. Critical Infrastructure including energy grids, nuclear plants, oil & gas facilities, and water utilities is the fastest-growing end-user category, supported by legislative mandates and insurance-linked risk mitigation requirements, with an estimated CAGR of 28.4% through 2032.

Commercial & Civil applications including stadium security, corporate campuses, and high-security logistics hubs represent an emerging growth frontier, projected to reach USD xx billion by 2032 as regulatory clarity improves. Other Security Operators, including private security firms and law enforcement agencies, are adopting portable, cost-effective C-UAS solutions at an accelerating pace.

Anti-Drone Market Technology Analysis

| Technology | Detection / Mitigation | Key Capability | Market Maturity |

| RF / Signal Detection | Detection | Identifies drone RF signatures; passive & active scanning | Mature – High Deployment |

| Radar (Primary / Secondary) | Detection | Tracks micro-drones at range; integrates with command systems | Mature – Defense Standard |

| Electro-Optical / IR Cameras | Detection & Tracking | Visual/thermal identification; AI-augmented classification | Growing – AI Integration Phase |

| Acoustic Sensors | Detection | Passive sound pattern recognition; ideal for urban environments | Niche – Complementary |

| RF Jamming / Spoofing | Mitigation | Disrupts C2 signal; forces return-to-home or landing | Regulated – Defense Authorized |

| High-Power Microwave (HPM) | Hard Kill / Mitigation | Disables drone electronics; effective for swarm defense | Emerging – R&D Phase |

| Directed Energy (Laser) | Hard Kill | Precision physical neutralization; low cost-per-shot | Emerging – Field Testing |

| Net Guns / Interceptor Drones | Physical Capture / Soft Kill | Non-destructive neutralization; recovery of drone forensics | Growing – Commercial Uptake |

| AI / ML Platform Integration | Cross-Functional | Automated threat classification; multi-sensor data fusion | Rapid Growth – Key Differentiator |

| GPS Spoofing / Navigation Denial | Electronic Countermeasure | Misdirects drone navigation; geo-fencing enforcement | Specialized – Government Use |

Anti-Drone Market Regional Analysis (2025–2032)

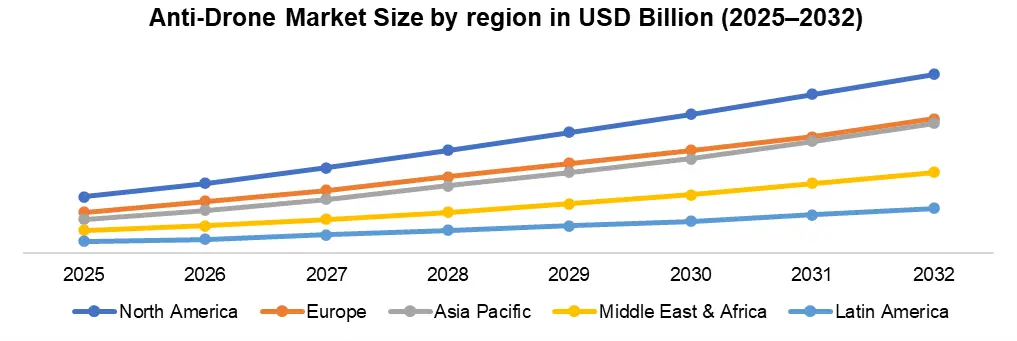

The Anti-Drone Market is expected to experience significant growth across various regions, driven by heightened security concerns and regulatory developments. North America was held a dominant position in the market, accounted 38% of the global market share in 2025. The United States, with its extensive military deployments, homeland security initiatives, and commercial sector investments, is the leading driver of this growth. The U.S. government's commitment to countering drone threats at military bases, airports, and critical infrastructure continues to fuel market expansion. Canada and Mexico are also expected to see increasing demand, particularly for commercial anti-drone solutions in airports and high-security venues. North America’s market is projected to grow steadily, driven by defense budgets and regulatory support.

In Asia Pacific (APAC), countries like China, India, and Japan are rapidly adopting anti-drone technologies due to growing concerns over national security and critical infrastructure protection. China's regulatory framework and India's expanding defense needs are contributing to strong demand, with the region expected to see robust market growth in the coming years.

Europe, including Germany, France, the UK, and Italy, is also experiencing growth due to the EU's regulatory focus on unmanned traffic management and critical infrastructure protection, driving demand for anti-drone solutions. The Middle East & Africa (MEA), led by UAE, Saudi Arabia, and Israel, is characterized by state-led defense procurements. Meanwhile, South America, with Brazil and Argentina, is in the early stages of adoption but is showing gradual market expansion.

Anti-Drone Market Competitive Landscape

The Global Anti-Drone Market is characterized by an intensely competitive landscape dominated by a blend of defense prime contractors, specialized C-UAS technology firms, and emerging AI-driven startups. Leading players in the Anti-Drone Market include Dedrone (US), DroneShield (Australia), Thales Group (France), Raytheon Technologies (US), L3Harris Technologies (US), Lockheed Martin (US), HENSOLDT AG (Germany), SRC Inc. (US), Rohde & Schwarz (Germany), and Blighter Surveillance Systems (UK).

Defense primes such as Raytheon and Lockheed Martin leverage deep integration with national defense procurement frameworks, long-term contracts, and established classified system delivery capabilities. Specialist firms like Dedrone and DroneShield are gaining market share through SaaS-based C-UAS platforms, cloud-connected sensor networks, and rapid deployment architectures suited for critical infrastructure and commercial security.

The Anti-Drone Market is witnessing a clear trend toward vertical integration, with hardware manufacturers acquiring software analytics capabilities and AI platform providers embedding sensor fusion layers into their offerings. Strategic partnerships between defense contractors and airport authorities, energy companies, and government agencies are becoming a key competitive moat. Mergers, acquisitions, and joint development agreements are reshaping market consolidation, with an estimated 12+ notable transactions recorded in the Anti-Drone Market between 2022 and 2024.

Top 10 Companies Anti-Drone Market

| Sr. No. | Company | Headquarters | Core C-UAS Solution |

| 1 | Dedrone | USA | DedroneTracker AI Platform |

| 2 | DroneShield | Australia | DroneSentry, RfPatrol, DroneGun |

| 3 | Raytheon Technologies | USA | Coyote UAS, FAAD System |

| 4 | Thales Group | France | Squire Radar, Gamekeeper |

| 5 | L3Harris Technologies | USA | Paladyne E1000MP Jammer |

| 6 | Lockheed Martin | USA | Morfius C-UAS, HELIOS Laser |

| 7 | HENSOLDT AG | Germany | Xpeller Multi-Sensor System |

| 8 | Rohde & Schwarz | Germany | ARDRONIS RF Detection System |

| 9 | Blighter Surveillance Systems | UK | A400 Series Air Security Radar |

| 10 | SRC Inc. | USA | Silent Archer C-UAS System |

Anti-Drone Market Regulatory, Legal & Compliance Landscape

The regulatory landscape governing the Anti-Drone Market is complex and rapidly evolving, as it operates at the intersection of national security law, aviation safety regulations, spectrum management, and civil liberties frameworks, each imposing distinct compliance requirements across jurisdictions. In the United States, the FAA Reauthorization Act (2018) and the National Defense Authorization Act (NDAA 2023) grant explicit authority to DHS, DoD, and authorized federal agencies to detect and counter hostile drones.

Commercial operators remain constrained by FCC spectrum regulations, which restrict the use of jamming technologies unless specifically authorized for defensive operations. In the European Union, the U-Space Regulation (2021/664) and the NIS2 Directive are shaping the Anti-Drone Market by mandating the integration of Unmanned Traffic Management (UTM) systems and critical infrastructure drone security protocols. NATO’s C-UAS Strategy Framework (2023) is also harmonizing defensive doctrines among member states, influencing procurement standards across the market.

In Asia Pacific, India’s DGCA regulations and China’s CAAC drone management rules are setting domestic compliance frameworks, restricting the deployment of foreign C-UAS systems without bilateral defense agreements. In the Middle East, the Anti-Drone Market is largely driven by state-directed procurement, which often operates outside civilian regulatory constraints. As the Anti-Drone Market expands into commercial sectors such as airports, stadiums, and energy facilities, its growth remains contingent on each country’s willingness to extend counter-drone authorization beyond defense agencies.

Anti-Drone Market: Investment & Funding Analysis

The Anti-Drone Market has attracted significant institutional and governmental investment, emphasizing the strategic importance of counter-UAS capabilities across both defense and commercial security sectors. Between 2021 and 2024, the market received over USD 3.2 billion in cumulative venture capital, private equity, and government-backed research funding globally, signaling strong investor interest in counter-drone technologies.

Dedrone, a leading company in the market, raised over USD 60 million in Series C funding in 2021. It was later acquired by Axon Enterprise for USD 250 million in 2024, marking one of the largest M&A transactions in the Anti-Drone Market. DroneShield, another key player, expanded its manufacturing and R&D capacity with an AUD 75 million capital raise in 2023, driven by increasing defense orders from the US and European markets.

US Department of Defense (DoD) investment in C-UAS technologies under the Joint C-UAS Office (JCO) surpassed USD 700 million in FY2023, with additional multi-year allocations under MDAP (Major Defense Acquisition Program) and rapid acquisition pathways to enhance anti-drone capabilities. DARPA's ALIAS and RACER programs continue to direct high-value R&D funding toward autonomous drone threat detection, ensuring ongoing investment in innovation.

In Europe, the European Defence Fund (EDF) allocated over EUR 130 million toward collaborative C-UAS R&D programs from 2023–2025, further solidifying Europe’s commitment to advancing drone defense technologies. In addition, Israel's BIRD Program and India's iDEX initiative are channeling early-stage government grants to domestic C-UAS startups, broadening the investment base and promoting innovation beyond established industry players. Multilateral investment in AI-integrated C-UAS platforms is expected to grow at a CAGR of over 30% through 2028, reflecting the increasing focus on advanced, autonomous drone defense technologies.

Anti-Drone Market Scope: Inquire before buying

| Anti-Drone Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 2.93 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 24.2% | Market Size in 2032: | USD 13.36 Bn. |

| Segments Covered: | by Product / System Type | Detection Systems Mitigation / Countermeasure Systems Hybrid / Integrated Systems |

|

| by Component | Hardware Software |

||

| by Technology | Electronic Systems Laser / Directed Energy Systems Kinetic Systems Radar-Based & Sensor Technologies |

||

| by Range | Short-Range Systems Medium-Range Systems Long-Range Systems |

||

| by Platform / Deployment Mode | Ground-Based Fixed Systems Ground-Based Mobile Systems Handheld / Portable Systems UAV / Drone-Based Counter-Drone Systems |

||

| by Application | Detection Only Detection & Disruption Tracking & Identification |

||

| by End-User / Industry Vertical | Military & Defense Government & Homeland Security Critical Infrastructure Commercial & Civil Other Security Operators |

||

Key players profiles covered in the Anti-Drone Market report in strategic perspective

1. Dedrone (Axon Enterprise)

2. DroneShield Ltd.

3. Thales Group

4. Lockheed Martin Corporation

5. Raytheon Technologies (RTX)

6. Northrop Grumman

7. Boeing Defense

8. Leonardo S.p.A.

9. Elbit Systems

10. Rafael Advanced Defense Systems

11. Airbus Defence & Space

12. Rohde & Schwarz

13. D-Fend Solutions

14. Fortem Technologies

15. Detect Inc.

16. Liteye Systems

17. Blighter Surveillance Systems

18. MyDefence

19. Sentrycs

20. Aaronia AG

21. L3Harris Technologies

22. HENSOLDT AG

23. Saab AB

24. IAI (Israel Aerospace Industries)