Agrochemicals Market by Pesticide Type, Fertilizer Type, Crop Type and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

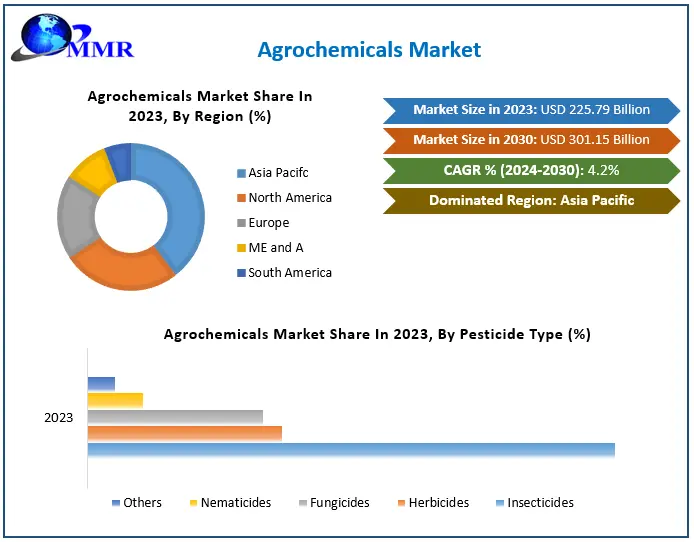

The Global Agrochemicals Market size was valued at USD 225.79 Billion in 2023 and the total Agrochemicals revenue is expected to grow at a CAGR of 4.2 % from 2024 to 2030, reaching nearly USD 301.15 Billion by 2030.

Agrochemicals Market Overview

Agricultural productivity is a key metric for assessing the performance of agricultural businesses, and these businesses have become increasingly open to employing agrochemicals. The scientific community is working nonstop to create high-quality agrochemicals that boost agricultural output. The agriculture industry is undeniably under regular surveillance by national and state authorities. The requirement to maintain agricultural integrity is expected to play a significant role in increasing sales in the global agrochemicals market. The overall revenue volume in the worldwide market is expected to rise by a significant amount. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Agrochemicals Market Trends:

The future of agrochemicals looks bright considering the global population growth rate, the growing need for more crop protection agents to protect against crop losses and increase yields, rising consumer demand for sustainably produced food, and agrochemicals’ role in tackling climate change through reducing the need to convert forests to farmlands, and thereby reducing potential greenhouse gas (GHG) emissions. However, several challenges stifle the growth potential of agrochemical companies.

Agrochemicals Market Dynamics:

The imperative to enhance agricultural efficiency and protect crops drives demand for agrochemicals worldwide.

The imperative to enhance agricultural efficiency and safeguard crops against pests, weeds, and diseases stands as a pivotal driver for the global agrochemicals market. 40% of global crop yields succumb to pests and diseases annually, with weeds alone slashing yields by nearly 34%. Agrochemical solutions such as herbicides, fungicides, and insecticides emerge as indispensable tools in curbing these losses and shielding crops. Climate change exacerbates crop stresses like drought, heat, cold, and salinity, further imperiling yields. Agrochemicals offer a means to bolster crop resilience in the face of such climatic challenges. Regions with tropical climates face heightened risks of insect infestations, fungal infections, and rampant weed proliferation, fueling demand for pesticides and other crop protection agents.

Moreover, unsustainable agricultural practices like reduced crop rotations and continuous cropping degrade soil health and foster the emergence of resistant pests and weeds, intensifying the necessity for diverse agrochemical interventions and advanced fertilizers. As agriculture increasingly shifts towards high-value horticultural crops, which demand heightened plant protection, the need for agrochemicals remains unabated. Therefore, the persistent quest to enhance agricultural productivity and shield crops against evolving threats from pests, diseases, and weeds serves as a paramount driver propelling growth in the global agrochemicals market.

Increasing stringency of regulatory requirements

Stringent regulatory laws, especially in Europe, are challenging to agrochemicals market with the further development of new, innovative technologies like gene-editing in plants, and the use of some types of crop protection agents like glyphosate. The number of glyphosate-related cases for a major agrochemical company crossed 11,000, impacting its stock price performance. A ban on a prevalent crop protection chemical like glyphosate could potentially remove up to 40% of the revenues for a few companies—most agrochemical companies being highly dependent upon glyphosate to drive their revenues and margins.

Government farm subsidy reduction with expectations of government subsidy cuts in the United States, farmers are likely to have less of a safety net in case of any weather-related disaster, pay more crop insurance premiums from their own pockets, and have less financial incentive to buy new and more effective crop protection products and seeds which affects to agrochemicals market.

Capturing value from increasing interest in sustainable agricultural practices and precision farming:

Sustainable agricultural practices include components like Integrated Pest Management (IPM), which involves proactive monitoring of pest populations, and preventing them from growing to unprecedented, damaging levels without causing irreversible soil toxicity or environmental harm all are included in the Agrochemicals Market. It comprises an integrated approach wherein the use of nonchemical tools and digital technologies is encouraged. Rigid focus on minimizing the use of agrochemicals, and greater adoption of IPM practices lead to long-term demand agrochemical market and a decline in major classes of crop protection chemicals including herbicides.

However, because of IPM’s focus on natural pest control mechanisms, the demand for biologicals increases to a great extent and commands higher premiums than conventional crop protection chemicals. In fact, from 2020 to till the growth in biologicals (or biopesticides) has outpaced that of overall crop protection chemicals. For well-established innovators whose business models remain asset-heavy, leveraging the power of Machine Learning and Artificial Intelligence (AI) might help Agrochemicals Market a great deal. For instance, instead of testing the efficacy of seeds in a field, Bayer CropScience has made use of simulations and big data to test the same in a computer. This has reportedly shaved off one to two years’ worth of R&D efforts, improved the time-to-Agrochemicals Market for new seeds, and reduced its R&D expenditure.

Agrochemicals Market Segment Analysis:

Based on Crop Type, in 2023, the cereal and grains segment emerged as the dominant force in the market, commanding a substantial revenue share exceeding 47.0%. Agrochemicals play a pivotal role in the development of fruits and vegetables, ensuring their safety, quality, and cost-effectiveness. Pesticides support farmers in cultivating fruit and vegetable crops while fertilizers provide essential nutrients, nitrogen, phosphorus, and potassium (NPK), fostering optimal Agrochemicals Market growth. Asia Pacific stands as the primary consumer of cereal and grain products globally, boasting a significant portion of the world's cultivated land dedicated to grains and cereals. The widespread adoption of fertilizers has become imperative in grain cultivation to meet the escalating demand. This demand is primarily fueled by the increasing consumption of cereals and grains such as rice, wheat, rye, corn, oats, sorghum, and barley. Agrochemical utilization is particularly pronounced in the cultivation of staple crops like rice, wheat, and other cereals and grains.

Agrochemicals Market Regional Insights:

In 2023, the Asia Pacific region emerged as a dominant force in the agrochemicals market, capturing a substantial revenue share exceeding 27.0%. Renowned as the leading global producer of agricultural goods, the region benefits from major contributors such as India, China, and Japan. China, in particular, holds the title of the world's largest exporter and manufacturer of pesticides, as reported by the International Trade Center (ITC) and FAO. Following closely, India ranks as the world's fourth-largest producer of agrochemicals this robust presence of key agricultural nations in the region significantly influences its Agrochemicals market share.

China's prominence extends beyond production to the consumption and exportation of fertilizers and insecticides on a global scale. China leads in pesticide usage worldwide, consuming over 30% of the global supply and meeting more than 90% of the world's technical raw material requirements. The substantial utilization underscores the region pivotal role in shaping the dynamics of the agrochemicals industry, with implications for regional economic growth and per capita income.

Agrochemicals Market Scope: Inquiry Before Buying

| Agrochemicals Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 225.79 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 4.2% | Market Size in 2030: | US $ 301.15 Bn. |

| Segments Covered: | by Pesticide Type | Insecticides Herbicides Fungicides Nematicides Others |

|

| by Fertilizer Type | Nitrogenous Fertilizer Phosphatic Fertilizer Potassic Fertilizer |

||

| by Crop Type | Cereal & Grains Oilseeds & Pulses Fruits & Vegetables Others |

||

Global Agrochemicals Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, and Rest of ME&A)

South America (Brazil, Argentina, and Rest of South America)

Agrochemicals Market Key Players:

1. OCP GROUP (United States)

2. Nutrien Ltd. (United States)

3. FMC Corporation (United States)

4. DuPont de Nemours, Inc. (United States)

5. Marrone Bio Innovations, Inc. (United States)

6. Corteva Agriscience(United States)

7. Bayer AG (Germany)

8. Syngenta Group (Switzerland)

9. BASF SE (Germany)

10. Yara International ASA (Norway)

11. ADAMA Ltd. (Israel)

12. Israel Chemicals Ltd. (Israel)

13. UPL Limited(Mumbai, India)

14. Sumitomo Chemical Co., Ltd. (Japan)

15. Nufarm Limited (Australia)

16. Mitsubishi Chemical Corporation (Japan)

17. ChemChina (Syngenta Group) (Beijing, China)

18. Ihara Chemical Industry Co., Ltd. (Japan)

FAQs:

1. What makes the Asia Pacific a Lucrative Market for Agrochemicals Market?

Ans. Textiles, sugar, animal husbandry, and vegetable oil manufacture are among the emerging agro-based businesses that are driving this growth.

2. What are the top players operating in the Agrochemicals Market?

Ans. ADAMA LTD, BAYER, BASF SE, SYNGENTA AG, UPL, COMPASS MINERALS, EUROCHEM GROUP, and OCP GROUP.

3. What is the key driving factor for the growth of the Agrochemicals Market?

Ans. The requirement to maintain agricultural integrity is expected to play a significant role in increasing sales in the global agrochemicals market.

4. What is the market size of the Global Agrochemicals Market by 2029?

Ans. The Agrochemicals Market size was valued at USD 225.79 Bn. In 2023 the total Agrochemicals Market revenue is growing by 4.2 % from 2024 to 2030, reaching nearly USD 301.15 Bn.