General Surgery Devices Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

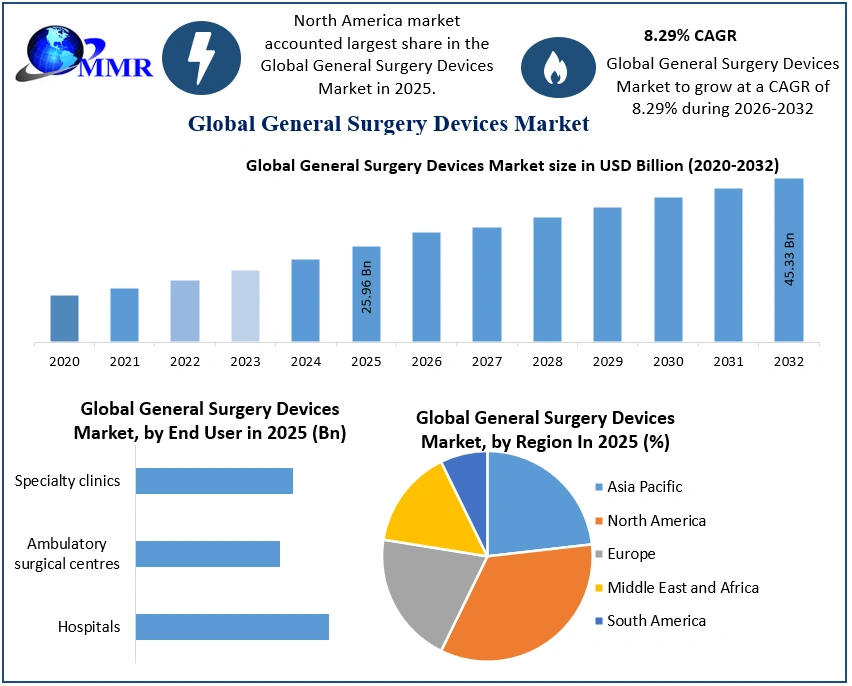

The General Surgery Devices Market size was valued at USD 25.96 Billion in 2025 and the total General Surgery Devices revenue is expected to grow at a CAGR of 8.29% from 2026 to 2032, reaching nearly USD 45.33 Billion by 2032.

General Surgery Devices Market Overview

The general surgery devices market is witnessing significant growth driven by factors such as increasing surgical procedures, technological advancements, and the growing geriatric population. With a rising number of surgical interventions performed globally, there is a higher demand for general surgery devices. The prevalence of chronic diseases that need surgical treatments is a major factor in this. Thanks to technological improvement, more precise and successful surgical procedures are now possible thanks to equipment for minimally invasive and robotic surgery. The growing geriatric population, being more susceptible to chronic diseases, necessitates a higher number of surgical interventions. This demographic trend has significantly boosted the demand for general surgery devices.

Increased healthcare expenditure by governments and healthcare organizations worldwide has improved medical infrastructure and promoted advanced surgical procedures, creating a favourable environment for the market's growth. Moreover, improving healthcare awareness and enhanced access to healthcare services, especially in developing regions, have led to a surge in surgical procedures, driving the demand for general surgery devices.The general surgery devices market is segmented based on product type, application, end-user and geography. The essential product types in this industry are surgical instruments, disposable surgical supplies, sutures and staplers, electrosurgical devices, laparoscopic equipment and wound closure tools.

Gynaecology, urology, orthopaedic, cardiovascular and gastrointestinal surgery are among the surgical specialities that employ this technology. The primary end-users of general surgery equipment are hospitals, ambulatory surgical centres and speciality clinics. Geographically, Asia Pacific is predicted to grow at the fastest rate due to rising healthcare spending and bettering medical facilities, while North America has historically had a sizable General Surgery Devices market share. Medtronic, Johnson & Johnson, Stryker Corporation, B. Braun Melsungen AG and Olympus Corporation are a few of the market's top players.

To know about the Research Methodology :- Request Free Sample Report

General Surgery Devices Market Dynamics

The General Surgery Devices Market is driven by several key factors. A significant factor is the rise in surgical procedures performed all around the world. This can be ascribed to the rise in chronic illness prevalence and the need for surgical procedures in an ageing population. To fulfil the demands of healthcare practitioners, there is a rising demand for general surgery devices, such as surgical instruments and equipment. Technology development is a key factor in the market's growth. Robotic aided surgery, minimally invasive methods and advanced imaging systems are just a few examples of the general surgery gadget advancements that have dramatically increased surgical precision, decreased invasiveness and improved patient outcomes.

Because they provide greater efficiency and efficacy in surgical procedures, these developments have expanded the popularity of general surgery devices. The ageing population is a big additional factor. As people get older, they are more likely to develop chronic disorders that call for surgical treatment, like orthopedic and cardiovascular issues. As healthcare providers meet the needs of this demographic group, the need for general surgery equipment is growing as the older population increases globally. There has been a significant shift towards minimally invasive surgery in terms of General Surgery Devices market trends.

Smaller incisions, less tissue stress and quicker patient recovery times are all benefits of this method. As a result, there is a significant need for specialized equipment that makes minimally invasive operations possible, such as endoscopic tools, robotic surgical systems and laparoscopic instruments. These products' increased market acceptance is a result of their improved patient results and comfort. In terms of opportunities, emerging General Surgery Devices markets present significant growth potential for general surgery device manufacturers. Developing regions, particularly in Asia Pacific and South America, are witnessing improvements in healthcare infrastructure, rising healthcare expenditure and increasing awareness of surgical treatments.

These factors create favorable General Surgery Devices market conditions for expansion and penetration in these regions. The market for general surgery devices also benefits from the shift towards personalized medicine. Tailoring devices to meet individual patient needs, such as patient-specific implants or surgical tools, has the potential to improve surgical outcomes and patient satisfaction. The customization of general surgery devices offers opportunities for market players to cater to the specific requirements of patients, leading to better clinical outcomes. However, there are certain threats and challenges that need to be considered.

Stringent regulatory requirements can pose challenges for general surgery device manufacturers. Meeting regulatory standards and obtaining necessary approvals can be time-consuming and costly, hindering market entry and the development of new products. Reimbursement issues can impact market growth. Limited or inadequate reimbursement policies for general surgery devices in certain regions may restrict their adoption.

The high costs associated with these devices, coupled with reimbursement limitations, can limit access to advanced surgical technologies, affecting market penetration. Cost constraints also pose a challenge in the General Surgery Devices market. The affordability of general surgery devices and consumables is crucial, especially for healthcare facilities with limited budgets or patients in regions with lower income levels.

Finding solutions to address cost constraints and improve affordability is necessary to enhance market penetration and ensure equitable access to these devices. Maintaining device accuracy and reliability remains a challenge. Consistent and accurate performance of general surgery devices, such as precision instruments and implantable devices, is vital for successful surgical outcomes. Manufacturers need to continuously focus on improving device accuracy and reliability through stringent quality control measures and ongoing research and development efforts.

General Surgery Devices Market Regional Analysis

The General Surgery Devices Market exhibits regional variations in terms of market size, growth rates and key market players. In North America, the market is dominated by the United States, which benefits from advanced healthcare infrastructure, high healthcare expenditure and a strong presence of key market players. The region's well-established reimbursement system facilitates the adoption of advanced general surgery devices and government initiatives coupled with a high prevalence of chronic diseases contribute to market growth.

Another significant General Surgery Devices market is Europe, which is driven by nations like Germany, the United Kingdom, France and Italy. The need for general surgical instruments is supported by the region's top hospitals, regulated healthcare system and focus on patient safety. The market expansion in Europe is further fuelled by the use of minimally invasive surgical techniques and cutting-edge surgical technology. The Asia Pacific region is experiencing significant growth in the General Surgery Devices Market. Rapid economic growth, rising healthcare costs and a big patient base all support market expansion.

South Korea, China, Japan, India and other nations play a critical role in the expansion of the regional market. Ageing population, shifting lifestyle habits and rising prevalence of chronic diseases are the demand drivers for general surgical devices.The ongoing development of healthcare infrastructure and increasing awareness of advanced surgical treatments provide growth opportunities for market players in the region. South America represents a growing market for general surgery devices, with countries like Brazil, Mexico and Argentina contributing to market growth.

The region benefits from a growing healthcare infrastructure, expanding private healthcare sector and increasing investments in healthcare. The rising prevalence of chronic diseases and the adoption of advanced surgical techniques drive the demand for general surgery devices in South America. While challenges related to limited access to advanced healthcare technologies, affordability and reimbursement may exist, the General Surgery Devices market offers growth potential for market players willing to address these obstacles.

General Surgery Devices Market Segment Analysis

Based on Application, the market is segmented based on applications into orthopedic surgery, cardiology, ophthalmology, wound care, audiology, thoracic surgery, urology and gynecology surgery, plastic surgery, neurosurgery, and others. The orthopedic surgery segment held the largest General Surgery Devices Market share in 2025 and is expected to retain its dominance during the forecast period. This is attributed to the increasing incidences of bone diseases and a burgeoning geriatric population worldwide. Factors such as product advancements, favorable reimbursement policies, and enhancements in diagnostic techniques and orthopedic surgical imaging technology are also anticipated to propel this segment forward.

Based on End User, the General Surgery Devices Market serves hospitals, ambulatory surgical centres and specialty clinics. Hospitals represent the largest segment due to their comprehensive range of surgical services and patient volume. Ambulatory surgical centres are gaining popularity as they offer convenient, cost-effective alternatives to traditional hospital-based surgeries. Specialty clinics cater to specific surgical specialties and provide specialized treatments.

General Surgery Devices Market Competitive Landscape

A number of major manufacturers are contending for market share in the general surgery devices industry, which is characterised by a fiercely competitive environment. Offering a variety of surgical tools, imaging systems and surgical navigation technology, Medtronic PLC is a market leader. The business actively participates in strategic partnerships and acquisitions to diversify its product offering and market presence in addition to focusing on ongoing product innovation to preserve its competitive edge. Johnson & Johnson, through its subsidiary Ethicon, is also a major player in the General Surgery Devices market, specializing in surgical devices such as sutures, staplers and advanced energy devices.

The company emphasizes research and development to introduce innovative surgical solutions and engages in strategic collaborations and partnerships to enhance its product offerings and global reach. Another significant competitor in the market for general surgery devices is Stryker Corporation, which produces orthopaedic surgical tools and equipment. The business concentrates on technology development and product innovation to give doctors cutting-edge equipment for successful surgical procedures. Stryker regularly seeks out acquisitions to increase the scope of its product offering and solidify its position in the General Surgery Devices market. Olympus Corporation, known for its expertise in endoscopy and visualization systems, offers advanced endoscopes, imaging systems and energy devices for minimally invasive surgeries.

The company invests in research and development to introduce innovative products and collaborates with healthcare professionals and institutions to drive advancements in endoscopic procedures. Other notable players in the General Surgery Devices Market include B. Braun Melsungen AG, Boston Scientific Corporation, Conmed Corporation, Zimmer Biomet Holdings Inc. and Intuitive Surgical Inc. These companies compete through product innovation, geographic expansion, strategic collaborations and mergers and acquisitions to strengthen their market positions.

Continuous innovation is what keeps the market dynamic, with firms vying to provide technologically cutting-edge goods that meet patients' and healthcare professionals' changing needs. These businesses use strategic alliances and acquisitions as key tactics to diversify their product lines and penetrate new markets. The General Surgery Devices Market's competitive landscape is dynamic and driven by a focus on innovation, collaboration and market expansion.

Continuous innovation is what keeps the market dynamic, with firms vying to provide technologically cutting-edge goods that meet patients' and healthcare professionals' changing needs. These businesses use strategic alliances and acquisitions as key tactics to diversify their product lines and penetrate new markets. The General Surgery Devices Market's competitive landscape is dynamic and driven by a focus on innovation, collaboration and market expansion.

General Surgery Devices Market Scope: Inquire before buying

| Global General Surgery Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 25.96 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 8.29% | Market Size in 2032: | USD 45.33 Bn. |

| Segments Covered: | By Type | Disposable Surgical Supplies Open Surgery Instrument Energy-based & Powered Instrument Minimally Invasive Surgery Instruments Medical Robotics & Computer Assisted Surgery Devices Adhesion Prevention Products |

|

| By Application | Orthopedic Surgery Cardiology Ophthalmology Wound Care Audiology Thoracic Surgery Urology and Gynecology Surgery Plastic Surgery Neurosurgery Others |

||

| By End User | Hospitals Ambulatory surgical centres Specialty clinics |

||

General Surgery Devices Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

General Surgery Devices Market, Key players

The captured list of leading manufacturers of General Surgery Devices industry has been compiled after an analysis of multiple factors. It is not an exhaustive list based only on market share ranking. After a regional analysis, a competitive analysis and other such considerations, the company profiles were selected based on a variety of factors. The comprehensive report contains information on the position of each company in the market from a local and global perspective.

North America:

1. Medtronic PLC (United States)

2. Johnson & Johnson (United States)

3. Stryker Corporation (United States)

4. Boston Scientific Corporation (United States)

5. Intuitive Surgical Inc. (United States)

6. Baxter International Inc. (United States)

7. Becton, Dickinson and Company (United States)

8. Abbott Laboratories (United States)

9. Zimmer Biomet Holdings Inc. (United States)

Europe:

1. B. Braun Melsungen AG (Germany)

2. Karl Storz GmbH & Co. KG (Germany)

3. Siemens Healthineers AG (Germany)

4. Smith & Nephew PLC (United Kingdom)

Asia Pacific:

1. Olympus Corporation (Japan)

2. Terumo Corporation (Japan)

3. Fujifilm Holdings Corporation (Japan)

4. Nihon Kohden Corporation (Japan)

5. Hitachi Ltd. (Japan)

6. Hoya Corporation (Japan)

7. Mindray Medical International Limited (China)

8. Nipro Corporation (Japan)

9. Wipro GE Healthcare Pvt. Ltd. (India)

10. Asahi Kasei Corporation (Japan)

FAQs

Q: What factors are driving the growth of the General Surgery Devices Market?

A: The growth of the general surgery devices market is driven by factors such as the increasing prevalence of general surgical conditions, advancements in technology, rising awareness about surgical management and higher healthcare expenditure. The demand for personalized surgical solutions and the development of user-friendly devices also contribute to market growth.

Q: What are the key trends in the General Surgery Devices Market?

A: Some key trends in the market include the adoption of continuous glucose monitoring systems, integration of artificial intelligence and data analytics in surgical devices and the focus on developing user-friendly and convenient surgical devices. These trends aim to improve patient outcomes, enhance surgical precision and provide personalized solutions for surgical management.

Q: What are the opportunities in the General Surgery Devices Market?

A: Emerging markets, such as Asia Pacific and South America, present significant growth opportunities for general surgery device manufacturers due to the increasing prevalence of surgical conditions and improving healthcare infrastructure in these regions. The demand for personalized surgical management and the development of innovative surgical devices and digital health platforms offer opportunities for market expansion and penetration.

Q: What are the challenges and threats in the General Surgery Devices Market?

A: Challenges in the general surgery devices market include product affordability, ensuring device accuracy and reliability, stringent regulatory requirements and reimbursement issues. The high cost of surgical devices and associated consumables can limit access to surgical management technologies, while regulatory and reimbursement hurdles can hinder market entry and slow down product development.

Q: Who are the key players in the Market?

A: The general surgery devices market includes several key players, such as Medtronic PLC, Johnson & Johnson, Stryker Corporation, Boston Scientific Corporation, Olympus Corporation, B. Braun Melsungen AG and Siemens Healthineers AG. These companies, along with others, contribute to the competitive landscape of the market by offering a wide range of surgical devices and technologies.