1. Fiberglass Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Fiberglass Market: Dynamics

2.1. Fiberglass Market Trends by Region

2.1.1. North America Fiberglass Market Trends

2.1.2. Europe Fiberglass Market Trends

2.1.3. Asia Pacific Fiberglass Market Trends

2.1.4. Middle East and Africa Fiberglass Market Trends

2.1.5. South America Fiberglass Market Trends

2.2. Fiberglass Market Dynamics by Region

2.2.1. North America

2.2.1.1. North America Fiberglass Market Drivers

2.2.1.2. North America Fiberglass Market Restraints

2.2.1.3. North America Fiberglass Market Opportunities

2.2.1.4. North America Fiberglass Market Challenges

2.2.2. Europe

2.2.2.1. Europe Fiberglass Market Drivers

2.2.2.2. Europe Fiberglass Market Restraints

2.2.2.3. Europe Fiberglass Market Opportunities

2.2.2.4. Europe Fiberglass Market Challenges

2.2.3. Asia Pacific

2.2.3.1. Asia Pacific Fiberglass Market Drivers

2.2.3.2. Asia Pacific Fiberglass Market Restraints

2.2.3.3. Asia Pacific Fiberglass Market Opportunities

2.2.3.4. Asia Pacific Fiberglass Market Challenges

2.2.4. Middle East and Africa

2.2.4.1. Middle East and Africa Fiberglass Market Drivers

2.2.4.2. Middle East and Africa Fiberglass Market Restraints

2.2.4.3. Middle East and Africa Fiberglass Market Opportunities

2.2.4.4. Middle East and Africa Fiberglass Market Challenges

2.2.5. South America

2.2.5.1. South America Fiberglass Market Drivers

2.2.5.2. South America Fiberglass Market Restraints

2.2.5.3. South America Fiberglass Market Opportunities

2.2.5.4. South America Fiberglass Market Challenges

2.3. PORTER’s Five Forces Analysis

2.4. PESTLE Analysis

2.5. Technology Roadmap

2.6. Regulatory Landscape by Region

2.6.1. North America

2.6.2. Europe

2.6.3. Asia Pacific

2.6.4. Middle East and Africa

2.6.5. South America

2.7. Key Opinion Leader Analysis For Fiberglass Industry

2.8. Analysis of Government Schemes and Initiatives For Fiberglass Industry

2.9. Fiberglass Market price trend Analysis (2023-24)

2.10. Fiberglass Market Trade Analysis

2.10.1. Global Import Analysis

2.10.1.1. Top Importer of Fiberglass

2.10.2. Global Export Analysis

2.10.2.1. Top Exporter of Fiberglass

2.11. Fiberglass Production Analysis

2.12. The Global Pandemic Impact on Fiberglass Market

3. Fiberglass Market: Global Market Size and Forecast by Segmentation by Demand and Supply Side (by Value and Volume) 2025-2032

3.1. Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

3.1.1. E-Glass

3.1.2. ECR-Glass

3.1.3. H-Glass

3.1.4. AR-glass

3.1.5. S-Glass

3.1.6. Others

3.2. Fiberglass Market Size and Forecast, by Product (2025-2032)

3.2.1. Glass Wool

3.2.2. Roving

3.2.3. Chopped Strand

3.2.4. Yarn

3.2.5. Others

3.3. Fiberglass Market Size and Forecast, by Application (2025-2032)

3.3.1. Transportation

3.3.2. Building & Construction

3.3.3. Electrical & Electronics

3.3.4. Pipe & Tank

3.3.5. Consumer Goods

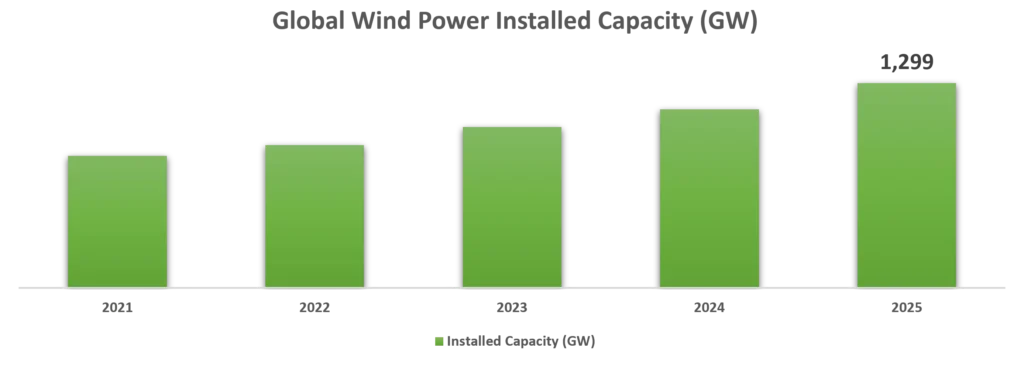

3.3.6. Wind Energy

3.3.7. Others

3.4. Fiberglass Market Size and Forecast, by Region (2025-2032)

3.4.1. North America

3.4.2. Europe

3.4.3. Asia Pacific

3.4.4. Middle East and Africa

3.4.5. South America

4. North America Fiberglass Market Size and Forecast by Segmentation (by Value and Volume) 2025-2032

4.1. North America Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

4.1.1. E-Glass

4.1.2. ECR-Glass

4.1.3. H-Glass

4.1.4. AR-glass

4.1.5. S-Glass

4.1.6. Others

4.2. North America Fiberglass Market Size and Forecast, by Product (2025-2032)

4.2.1. Glass Wool

4.2.2. Roving

4.2.3. Chopped Strand

4.2.4. Yarn

4.2.5. Others

4.3. North America Fiberglass Market Size and Forecast, by Application (2025-2032)

4.3.1. Transportation

4.3.2. Building & Construction

4.3.3. Electrical & Electronics

4.3.4. Pipe & Tank

4.3.5. Consumer Goods

4.3.6. Wind Energy

4.3.7. Others

4.4. North America Fiberglass Market Size and Forecast, by Country (2025-2032)

4.4.1. United States

4.4.1.1. United States Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

4.4.1.1.1. E-Glass

4.4.1.1.2. ECR-Glass

4.4.1.1.3. H-Glass

4.4.1.1.4. AR-glass

4.4.1.1.5. S-Glass

4.4.1.1.6. Others

4.4.1.2. United States Fiberglass Market Size and Forecast, by Product (2025-2032)

4.4.1.2.1. Glass Wool

4.4.1.2.2. Roving

4.4.1.2.3. Chopped Strand

4.4.1.2.4. Yarn

4.4.1.2.5. Others

4.4.1.3. United States Fiberglass Market Size and Forecast, by Application (2025-2032)

4.4.1.3.1. Transportation

4.4.1.3.2. Building & Construction

4.4.1.3.3. Electrical & Electronics

4.4.1.3.4. Pipe & Tank

4.4.1.3.5. Consumer Goods

4.4.1.3.6. Wind Energy

4.4.1.3.7. Others

4.4.2. Canada

4.4.2.1. Canada Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

4.4.2.1.1. E-Glass

4.4.2.1.2. ECR-Glass

4.4.2.1.3. H-Glass

4.4.2.1.4. AR-glass

4.4.2.1.5. S-Glass

4.4.2.1.6. Others

4.4.2.2. Canada Fiberglass Market Size and Forecast, by Product (2025-2032)

4.4.2.2.1. Glass Wool

4.4.2.2.2. Roving

4.4.2.2.3. Chopped Strand

4.4.2.2.4. Yarn

4.4.2.2.5. Others

4.4.2.3. Canada Fiberglass Market Size and Forecast, by Application (2025-2032)

4.4.2.3.1. Transportation

4.4.2.3.2. Building & Construction

4.4.2.3.3. Electrical & Electronics

4.4.2.3.4. Pipe & Tank

4.4.2.3.5. Consumer Goods

4.4.2.3.6. Wind Energy

4.4.2.3.7. Others

4.4.3. Mexico

4.4.3.1. Mexico Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

4.4.3.1.1. E-Glass

4.4.3.1.2. ECR-Glass

4.4.3.1.3. H-Glass

4.4.3.1.4. AR-glass

4.4.3.1.5. S-Glass

4.4.3.1.6. Others

4.4.3.2. Mexico Fiberglass Market Size and Forecast, by Product (2025-2032)

4.4.3.2.1. Glass Wool

4.4.3.2.2. Roving

4.4.3.2.3. Chopped Strand

4.4.3.2.4. Yarn

4.4.3.2.5. Others

4.4.3.3. Mexico Fiberglass Market Size and Forecast, by Application (2025-2032)

4.4.3.3.1. Transportation

4.4.3.3.2. Building & Construction

4.4.3.3.3. Electrical & Electronics

4.4.3.3.4. Pipe & Tank

4.4.3.3.5. Consumer Goods

4.4.3.3.6. Wind Energy

4.4.3.3.7. Others

5. Europe Fiberglass Market Size and Forecast by Segmentation (by Value and Volume) 2025-2032

5.1. Europe Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.2. Europe Fiberglass Market Size and Forecast, by Product (2025-2032)

5.3. Europe Fiberglass Market Size and Forecast, by Application (2025-2032)

5.4. Europe Fiberglass Market Size and Forecast, by Country (2025-2032)

5.4.1. United Kingdom

5.4.1.1. United Kingdom Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.4.1.2. United Kingdom Fiberglass Market Size and Forecast, by Product (2025-2032)

5.4.1.3. United Kingdom Fiberglass Market Size and Forecast, by Application (2025-2032)

5.4.2. France

5.4.2.1. France Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.4.2.2. France Fiberglass Market Size and Forecast, by Product (2025-2032)

5.4.2.3. France Fiberglass Market Size and Forecast, by Application (2025-2032)

5.4.3. Germany

5.4.3.1. Germany Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.4.3.2. Germany Fiberglass Market Size and Forecast, by Product (2025-2032)

5.4.3.3. Germany Fiberglass Market Size and Forecast, by Application (2025-2032)

5.4.4. Italy

5.4.4.1. Italy Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.4.4.2. Italy Fiberglass Market Size and Forecast, by Product (2025-2032)

5.4.4.3. Italy Fiberglass Market Size and Forecast, by Application (2025-2032)

5.4.5. Spain

5.4.5.1. Spain Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.4.5.2. Spain Fiberglass Market Size and Forecast, by Product (2025-2032)

5.4.5.3. Spain Fiberglass Market Size and Forecast, by Application (2025-2032)

5.4.6. Sweden

5.4.6.1. Sweden Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.4.6.2. Sweden Fiberglass Market Size and Forecast, by Product (2025-2032)

5.4.6.3. Sweden Fiberglass Market Size and Forecast, by Application (2025-2032)

5.4.7. Austria

5.4.7.1. Austria Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.4.7.2. Austria Fiberglass Market Size and Forecast, by Product (2025-2032)

5.4.7.3. Austria Fiberglass Market Size and Forecast, by Application (2025-2032)

5.4.8. Rest of Europe

5.4.8.1. Rest of Europe Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

5.4.8.2. Rest of Europe Fiberglass Market Size and Forecast, by Product (2025-2032)

5.4.8.3. Rest of Europe Fiberglass Market Size and Forecast, by Application (2025-2032)

6. Asia Pacific Fiberglass Market Size and Forecast by Segmentation (by Value and Volume) 2025-2032

6.1. Asia Pacific Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.2. Asia Pacific Fiberglass Market Size and Forecast, by Product (2025-2032)

6.3. Asia Pacific Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4. Asia Pacific Fiberglass Market Size and Forecast, by Country (2025-2032)

6.4.1. China

6.4.1.1. China Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.1.2. China Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.1.3. China Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.2. S Korea

6.4.2.1. S Korea Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.2.2. S Korea Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.2.3. S Korea Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.3. Japan

6.4.3.1. Japan Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.3.2. Japan Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.3.3. Japan Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.4. India

6.4.4.1. India Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.4.2. India Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.4.3. India Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.5. Australia

6.4.5.1. Australia Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.5.2. Australia Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.5.3. Australia Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.6. Indonesia

6.4.6.1. Indonesia Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.6.2. Indonesia Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.6.3. Indonesia Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.7. Malaysia

6.4.7.1. Malaysia Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.7.2. Malaysia Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.7.3. Malaysia Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.8. Vietnam

6.4.8.1. Vietnam Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.8.2. Vietnam Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.8.3. Vietnam Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.9. Taiwan

6.4.9.1. Taiwan Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.9.2. Taiwan Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.9.3. Taiwan Fiberglass Market Size and Forecast, by Application (2025-2032)

6.4.10. Rest of Asia Pacific

6.4.10.1. Rest of Asia Pacific Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

6.4.10.2. Rest of Asia Pacific Fiberglass Market Size and Forecast, by Product (2025-2032)

6.4.10.3. Rest of Asia Pacific Fiberglass Market Size and Forecast, by Application (2025-2032)

7. Middle East and Africa Fiberglass Market Size and Forecast by Segmentation (by Value and Volume) 2025-2032

7.1. Middle East and Africa Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

7.2. Middle East and Africa Fiberglass Market Size and Forecast, by Product (2025-2032)

7.3. Middle East and Africa Fiberglass Market Size and Forecast, by Application (2025-2032)

7.4. Middle East and Africa Fiberglass Market Size and Forecast, by Country (2025-2032)

7.4.1. South Africa

7.4.1.1. South Africa Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

7.4.1.2. South Africa Fiberglass Market Size and Forecast, by Product (2025-2032)

7.4.1.3. South Africa Fiberglass Market Size and Forecast, by Application (2025-2032)

7.4.2. GCC

7.4.2.1. GCC Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

7.4.2.2. GCC Fiberglass Market Size and Forecast, by Product (2025-2032)

7.4.2.3. GCC Fiberglass Market Size and Forecast, by Application (2025-2032)

7.4.3. Nigeria

7.4.3.1. Nigeria Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

7.4.3.2. Nigeria Fiberglass Market Size and Forecast, by Product (2025-2032)

7.4.3.3. Nigeria Fiberglass Market Size and Forecast, by Application (2025-2032)

7.4.4. Rest of ME&A

7.4.4.1. Rest of ME&A Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

7.4.4.2. Rest of ME&A Fiberglass Market Size and Forecast, by Product (2025-2032)

7.4.4.3. Rest of ME&A Fiberglass Market Size and Forecast, by Application (2025-2032)

8. South America Fiberglass Market Size and Forecast by Segmentation (by Value and Volume) 2025-2032

8.1. South America Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

8.2. South America Fiberglass Market Size and Forecast, by Product (2025-2032)

8.3. South America Fiberglass Market Size and Forecast, by Application(2025-2032)

8.4. South America Fiberglass Market Size and Forecast, by Country (2025-2032)

8.4.1. Brazil

8.4.1.1. Brazil Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

8.4.1.2. Brazil Fiberglass Market Size and Forecast, by Product (2025-2032)

8.4.1.3. Brazil Fiberglass Market Size and Forecast, by Application (2025-2032)

8.4.2. Argentina

8.4.2.1. Argentina Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

8.4.2.2. Argentina Fiberglass Market Size and Forecast, by Product (2025-2032)

8.4.2.3. Argentina Fiberglass Market Size and Forecast, by Application (2025-2032)

8.4.3. Rest Of South America

8.4.3.1. Rest Of South America Fiberglass Market Size and Forecast, by Glass Type (2025-2032)

8.4.3.2. Rest Of South America Fiberglass Market Size and Forecast, by Product (2025-2032)

8.4.3.3. Rest Of South America Fiberglass Market Size and Forecast, by Application (2025-2032)

9. Global Fiberglass Market: Competitive Landscape

9.1. MMR Competition Matrix

9.2. Competitive Landscape

9.3. Key Players Benchmarking

9.3.1. Company Name

9.3.2. Business Segment

9.3.3. End-user Segment

9.3.4. Revenue (2023)

9.3.5. Production of 2023

9.3.6. Company Locations

9.4. Leading Fiberglass Market Companies, by market capitalization

9.5. Analysis of Organized and Unorganized Key Players in Fiberglass Industry

9.6. Market Structure

9.6.1. Market Leaders

9.6.2. Market Followers

9.6.3. Emerging Players

9.7. Mergers and Acquisitions Details

10. Company Profile: Key Players

10.1. China Jushi Co., Ltd. (China)

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Scale of Operation (small, medium, and large)

10.1.7. Details on Partnership

10.1.8. Regulatory Accreditations and Certifications Received by Them

10.1.9. Awards Received by the Firm

10.1.10. Recent Developments

10.2. Xingtai Jinniu Fiberglass (China)

10.3. Glasstex Fiberglass (China)

10.4. Chongqing polycomp International Corporation (China)

10.5. Jushi Group Co., Ltd (China)

10.6. Taishan Fiberglass (China)

10.7. Hexcel Corporation (U.S.)

10.8. Fibre Glast Developments Corp. (U.S.)

10.9. PPG Industries (US)

10.10. Owens Corning (US)

10.11. Phelps Industrial Products LLC. (US)

10.12. Agy Holdings Corp. (US)

10.13. CertainTeed Corporation (US)

10.14. Auburn Manufacturing, Inc. (U.S.)

10.15. BGF Industries, Inc. (U.S.)

10.16. Dupont (U.S.)

10.17. Johns Manville Corp. (US)

10.18. Nitto Boseki Co., Ltd. (Japan)

10.19. Nippon Electric Glass (Japan)

10.20. Asahi Fiberglass Co (Japan)

10.21. PFG Fiber Glass (Taiwan)

10.22. Taiwan Glass Ind. (Taiwan)

10.23. 3B-The Fiberglass Company (Belgium)

10.24. Knauf Insulation (Belgium)

10.25. Gurit (Switzerland)

10.26. Chomarat (France)

10.27. Saint-Gobain (France)

10.28. Saertex GmbH & Co.KG. (Germany)

11. Key Findings

12. Industry Recommendations

13. Fiberglass Market: Research Methodology

14. Terms and Glossary