DOC DPF Market by Type and Application – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

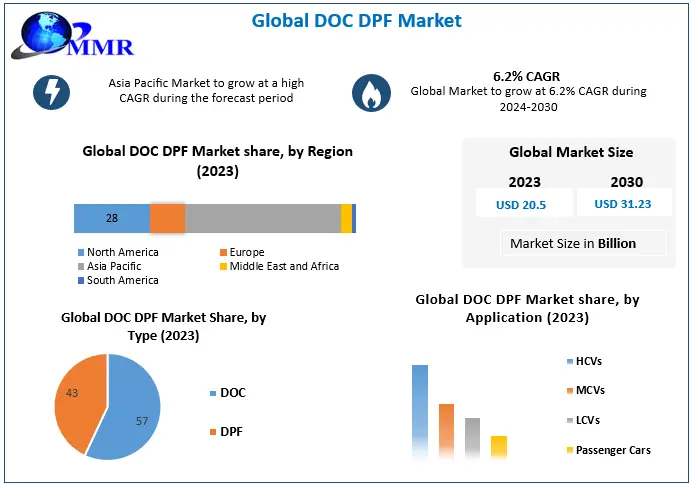

Global DOC DPF Market size was valued at USD 20.5 Bn. in 2023 and is expected to reach USD 31.23 Bn. by 2030, at a CAGR of 6.2% over the forecast period (2024-2030).

DOC DPF Market Overview

The DOC DPF is a combination of two emission control technologies used in diesel engines i.e. DOC (Diesel Oxidation Catalyst) and DPF (Diesel Particulate Filter). DOC is a component of the exhaust system that helps to reduce harmful emissions from diesel engines. It helps to oxidize pollutants such as carbon monoxide. DPF helps to remove harmful particles from diesel exhaust. It helps to improve engine performance and economy of fuel.

DOC DPF is used in modern diesel engines to comply with stringent emission regulations that help to reduce gaseous pollutants by improving air quality in the environment. Technological advancement by DOC DPF manufacturers to improve system performance at lower temperatures significantly contribute to the DOC DPF Market growth. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

DOC DPF Market Dynamics

Emission Regulations by government to boost the DOC DPF market growth

Stringent emission regulations by government and other regulatory bodies are expected to drive the DOC DPF market growth. These regulations aim to reduce harmful pollutants emitted by diesel vehicles and machinery, such as particulate matter (PM), nitrogen oxides (NOx), and hydrocarbons (HC). The implementation of emission standards encourages the adoption of DOC DPF systems to ensure compliance. Growing environmental awareness and concerns about air quality and public health significantly contribute for the growth of DOC DPF growth. These systems help reduce the emission of particulate matter and other pollutants, leading to cleaner air and a healthier environment. The increasing emphasis on sustainability and reducing carbon footprints is expected to adopt of DOC DPF technologies by DOC DPF key player.

Diesel engine emissions, have linked to various health issues, including respiratory problems, cardiovascular diseases, and cancer. As the awareness of the health impacts of diesel emissions increases, there is a greater emphasis on reducing these pollutants with the use of DOC DPF systems. Continuous advancements in DOC DPF technologies have improved their effectiveness, efficiency, and durability. Enhanced catalyst formulations, improved filter materials, and optimized regeneration strategies have made DOC DPF systems more reliable and efficient in reducing emissions. Technological advancements presents lucrative opportunities for market growth by offering better performing and cost-effective solutions. Government incentives, subsidies, and support programs is expected to boost the DOC DPF market growth. Financial incentives, tax benefits, and grants provided by governments encourage vehicle owners and fleet operators to invest in emissions control technologies.

High cost of DOC DPF to restrain the DOC DPF market growth

High cost of DOC DPF which involve advanced technologies, catalysts, and materials, which increases their overall cost and is expected to restrain the DOC DPF industry growth. The initial investment and ongoing maintenance expenses associated with DOC and DPF systems is a barrier for vehicle owners, especially for smaller businesses and individual consumers. Retrofitting existing vehicles with DOC DPF is challenging, particularly for older vehicle models. Retrofitting requires modifications to the exhaust system and engine calibration, which can be complex and costly. Limited retrofitting options are expected to limit the DOC DPF market potential for DOC DPF systems, as some vehicles are not feasible or cost-effective to retrofit.

Fuel Consumption and Trade-offs to hamper DOC DPF market growth

DOC DPF systems can introduce backpressure into the exhaust system, which can slightly increase fuel consumption and affect vehicle performance. Advancements in technology have minimized these impacts, and concerns among vehicle owners about the potential trade-offs in terms of fuel efficiency and overall vehicle performance is expected to restrain the DOC DFP market share. DOC DPF systems require regular maintenance and periodic regeneration to ensure their optimal performance. This includes cleaning or replacing filters, monitoring ash accumulation, and performing regeneration cycles to burn off trapped particulate matter. The maintenance and regeneration processes is time-consuming and require additional resources, which can be perceived as a restraint for vehicle owners and significantly restraint the market growth.

Market Challenges

Emission standards and regulations changes in every regions and countries, making it challenging for DOC DPF manufacturers to meet various requirements. Adapting emission standards and complying with multiple regulations increase complexity and costs for DOC DPF key players, and is expected to impact market growth. The increasing adoption of electric vehicles poses a long-term challenge for the DOC DPF market. As more regions prioritize electrification and promote EV adoption, the demand for diesel vehicles and associated emission control technologies decline over time and restrains the market growth.

DOC DPF Market Regional Insight

Asia Pacific region held the largest DOC DPF market share in 2023 and is expected to dominate the market over the forecast period. Growing automotive industry in China, India, Japan, and South Korea increases the demand for DOC DPF system in the region and is expected to fuel the market growth. Regulations implemented by the regional government contributes for the growth of market. In 2020, China has 372 Mn motor vehicles and from them PM emission from diesel vehicles account 99% of emissions from motor vehicles. Due to this consumers realize the importance of environmental protection in the region, which is expected to boost the DOC DPF market growth.

In North America, is expected to dominate the market over the forecast period. Use of DOC DPF helps to reduce the fuel efficiency and reduces the ownership cost, which is expected to boost the regional market growth. The United States is the country with most stringent emission requirements in the world. Brazil, Mexico, Argentina, and Colombia are the major countries contributing for the growth of market.

In European region, motor vehicle emission has been limited and is updated to sixth generation, which is expected to drive the regional DOC DPF market growth.

DOC DPF Market Segment Analysis

Based on Type: The market is segmented into DOC and DPF. The DOC segment held the largest DOC DPF market share in 2023 and is expected to grow rapidly during the forecast period. The Diesel Oxidation Catalyst (DOC) plays a crucial role in transforming detrimental emissions into less harmful compounds. It effectively reduces nitrogen oxides (NOx) and particulate matter (PM), contributing to a cleaner environment. Furthermore, the DOC enhances engine performance and promotes fuel efficiency by facilitating the conversion of harmful exhaust gases. In summary, the diesel oxidation catalyst is instrumental in mitigating environmental impact, enhancing overall engine functionality, and optimizing fuel economy.

DOC DPF Market Competitive Landscape

The competitive landscape of the market is characterized by the presence of several established players and a growing number of new entrants. The competitive landscape of the DOC DPF industry is shaped by strategic partnerships, collaborations, and acquisitions. The strategies adopted by the DOC DPF key player, such as expansion of product portfolio, mergers & acquisitions, geographical expansion, and collaborations, to enhance the DOC DPF Market penetration. The DOC DPF key players include Roadwarrior Inc., DPFXFIT By GESi, Dinex, DPF Regeneration, European Exhaust & Catalyst Ltd, DPF Sales Australia, and Cummins Inc.

In April, 2022, Red Fox Resources has announce the partnership with Volvo and Mack Trucks. They held Extended Emission Parts Recycling Program to provide sustainability and revenue opportunity for Volvo and Mack Truck Dealers. The program allows Volvo and Mack dealers to recycle scrap emission cores such as DPF and DOC. Red Fox Resources purchases used emission control systems from the dealer and reclaims the catalyst material for re-use.

DOC DPF Market Scope: Inquire before buying

| Global DOC DPF Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 20.5 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 6.2% | Market Size in 2030: | US $ 31.23 Bn. |

| Segments Covered: | By Type | DOC DPF |

|

| By Application | HCVs MCVs LCVs Passenger Cars |

||

DOC DPF Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

DOC DPF Market Key Players

1. Sud-Chemie India Pvt. Ltd.

2. Umicore Automotive Catalysts

3. Roadwarrior Inc.

4. DPFXFIT By GESi

5. Dinex

6. DPF Regeneration

7. European Exhaust & Catalyst Ltd

8. DPF Sales Australia

9. Cummins Inc.

1. Tenneco Inc

2. Nett Technologies Inc.

3. Tata AutoComp Katcon Exhaust Systems Pvt. Ltd

4. Perkins Engines Company Limited

5. Skyline Emissions

6. OTOMATIC

7. ESW Group

Frequently Asked Questions:

1] What is the growth rate of the Global DOC DPF Market?

Ans. The Global Market is growing at a significant rate of 6.2% over the forecast period.

2] Which region is expected to dominate the Global DOC DPF Market?

Ans. Asia Pacific region is expected to dominate the DOC DPF Market over the forecast period.

3] What is the expected Global Market size by 2030?

Ans. The market size of the DOC DPF Market is expected to reach USD 31.23 Bn by 2030.

4] Who are the top players in the Global DOC DPF Industry?

Ans. The major key players in the Global Market are Dinex, DPF Regeneration, European Exhaust & Catalyst Ltd, DPF Sales Australia, and Cummins Inc.

5] Which factors are expected to drive the Global DOC DPF Market growth by 2030?

Ans. Emission Regulations by the government is expected to drive the Market growth over the forecast period.