DNA Forensic Market by Technology, Source, Application, and End‑User – Global Market Size Estimation, Industry‑Wide Analysis, Competitive Landscape Assessment & Long‑Term Forecast to 2032

Overview

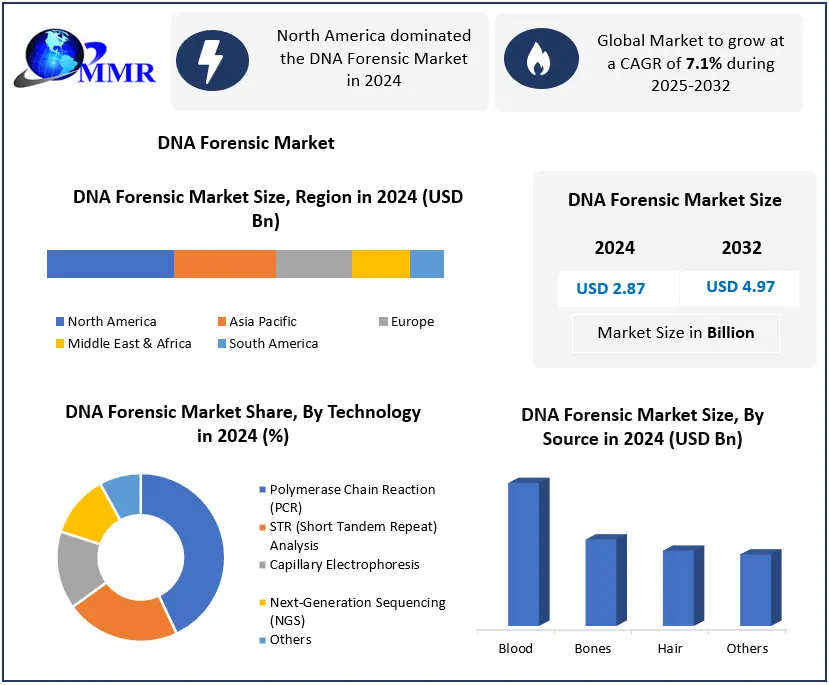

The DNA Forensic Market was valued at USD 2.87 Bn in 2024, and the total revenue of the DNA Forensic Market is expected to grow at a CAGR of 7.1% from 2025 to 2032, reaching nearly USD 4.97 Bn by 2032. Growth driven by rising crime rates, next-generation sequencing (NGS), rapid DNA technologies, and government investments in forensic infrastructure.

Global DNA Forensic Market Overview:

DNA forensics, also known as forensic DNA analysis or DNA profiling, is a branch of forensic science that involves the identification and analysis of DNA (deoxyribonucleic acid) samples to provide information for legal and investigative purposes. DNA is a molecule found in the cells of living organisms, carrying genetic information unique to each individual. In the context of forensics, DNA analysis is commonly used to establish biological relationships, identify individuals, and link suspects to crime scenes.

The DNA forensic market is experiencing robust growth globally, driven by increasing demand for advanced forensic technologies, rising awareness about DNA profiling, and a surge in criminal investigations. The market's current scenario is characterized by a growing emphasis on technological advancements, such as next-generation sequencing (NGS) and rapid DNA analysis techniques. Factors contributing to the DNA Forensic Market growth include the rising incidence of crime, advancements in forensic science, and the increasing need for accurate and rapid identification of suspects. Key players such as Thermo Fisher Scientific, QIAGEN, and Promega Corporation are at the forefront of innovation, constantly introducing new products and technologies to enhance DNA analysis capabilities.

Thermo Fisher Scientific, for instance, has been actively involved in developing cutting-edge solutions for forensic DNA testing, including the Applied Biosystems Precision ID NGS System. QIAGEN, with its QIAcube and QIAseq technologies, has played a pivotal role in streamlining and automating DNA sample processing and analysis. The DNA Forensic Market has witnessed recent developments such as strategic collaborations, product launches, and expansions by key players to strengthen their market presence. As governments worldwide increasingly invest in forensic infrastructure, the DNA forensic market is poised for significant growth in the upcoming years.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

DNA Forensic Market Dynamics

Revolutionizing Cold Case Investigations with DNA Forensics Drives the DNA Forensic Market Growth

The DNA forensic market is experiencing dynamic growth driven by a confluence of factors shaping its landscape. One of the primary drivers is the alarming rise in crime rates globally. As criminal activities become more sophisticated, there is an increasing need for advanced forensic technologies to aid investigations. For instance, the prevalence of cybercrime has brought to the forefront the importance of DNA analysis in solving complex cases. The ability of DNA forensics to provide precise and irrefutable evidence is crucial in addressing the evolving nature of criminal activities, further fueling the market's expansion.

Advancements in forensic technologies constitute another significant growth driver for the DNA forensic market. The continuous evolution of techniques, such as next-generation sequencing (NGS) and rapid DNA analysis, has revolutionized the field. Companies like Thermo Fisher Scientific are at the forefront of innovation, exemplified by their Applied Biosystems™ Precision ID NGS System. This system showcases the industry's commitment to cutting-edge solutions for forensic DNA testing, enhancing the accuracy and efficiency of the analysis process. Technological progress not only meets the demands of evolving criminal methodologies but also establishes DNA forensics as a sophisticated and indispensable tool in modern investigative practices.

Government initiatives and funding play a pivotal role in propelling the DNA forensic market forward. Governments across the globe are increasingly recognizing the importance of investing in forensic infrastructure and crime prevention programs. These investments contribute to the growth of the market by supporting the establishment and enhancement of forensic laboratories. Funding for these initiatives accelerates the adoption of advanced DNA analysis technologies, thereby expediting investigations and ensuring justice is served efficiently.

The growing awareness and acceptance of DNA profiling among the general public are instrumental in driving market demand. As awareness about the accuracy and reliability of DNA forensics spreads, there is a corresponding increase in public trust in its applications. This heightened trust translates into a surge in demand for DNA forensic services in criminal investigations and legal proceedings. The growing recognition of DNA evidence as a powerful and conclusive tool further cements its position as a cornerstone of modern forensic science.

The globalization of DNA databases is another factor contributing to the expansion of the market. The collaboration and sharing of information on an international scale enable law enforcement agencies to solve cross-border crimes more effectively. Organizations like the European DNA Profiling Group (EDNAP) facilitate such cooperation, fostering advancements in forensic capabilities and harmonizing practices across borders. The globalization of DNA databases underscores the interconnected nature of crime and the need for a unified approach to forensic investigations.

The emphasis on solving cold cases through DNA analysis is a compelling growth driver for the market. Technological advancements have breathed new life into unsolved cases, offering hope to victims' families and bringing closure to long-standing mysteries. DNA forensics has played a pivotal role in reopening and reexamining cold cases, showcasing its potential to provide answers even years after the occurrence of a crime. The ability to bring justice to victims and their families in such cases enhances the credibility and societal value of DNA forensic technologies.

Collaborations between key market players and technology providers are contributing to the development of advanced DNA forensic solutions. Partnerships, such as the collaboration between Illumina and QIAGEN, aim to integrate sequencing technologies to create more comprehensive and efficient DNA analysis platforms. These collaborations harness the strengths of different entities, fostering innovation and ensuring that the DNA forensic market remains at the forefront of technological advancements.

Beyond criminal investigations, the increasing use of DNA forensics in civil applications is broadening the DNA Forensic Market scope. The technology's versatility makes it valuable in diverse scenarios, including immigration and disaster victim identification. The ability to establish identity and familial relationships through DNA analysis is crucial in situations where traditional identification methods may be challenging or impossible. This expanding range of applications enhances the DNA Forensic Market significance beyond its traditional role in solving criminal cases.

The growing demand for rapid DNA analysis is a testament to the evolving needs of law enforcement and emergency response scenarios. Companies like ANDE Corporation, with their Rapid DNA Analysis technology, cater to the need for swift and portable DNA profiling in field applications. This demand is driven by the necessity for quick and on-site DNA analysis solutions, enabling law enforcement agencies to expedite investigations and make informed decisions in real-time propel the DNA Forensic Market.

Financial Barriers in Forensic Laboratories High Costs of DNA Analysis Technologies Restrains the DNA Forensic Market Demand

One significant concern is the emergence of privacy issues and ethical dilemmas surrounding the collection and use of genetic information. The Golden State Killer case, which involved accessing public DNA databases without explicit consent, ignited debates on the ethical implications and privacy rights of individuals. High costs associated with advanced DNA analysis technologies pose a substantial restraint. The initial investment required for acquiring and implementing sophisticated equipment, such as next-generation sequencing (NGS) systems, can be prohibitive for smaller forensic laboratories. This financial barrier limits their capacity to conduct comprehensive DNA analysis, contributing to disparities in forensic capabilities.

Backlogs and extended turnaround times in forensic laboratories constitute another challenge. Despite technological advancements, the sheer volume of cases and the meticulous nature of DNA testing can lead to delays. This backlog impedes the timely resolution of cases, affecting the overall efficiency of the criminal justice system. Navigating complex legal and regulatory landscapes presents a hurdle to the DNA forensic market. Varying regulations across jurisdictions create challenges for standardization, hindering seamless collaboration between international law enforcement agencies. Legal and regulatory considerations are paramount, impacting the retention and use of DNA samples.

The limited adoption of DNA forensic technologies in developing regions poses challenges in implementation. Limited resources, infrastructure, and awareness hinder the accessibility of advanced DNA analysis tools, resulting in disparities in forensic capabilities on a global scale. The risk of contamination and sample quality issues during DNA sample analysis is a persistent challenge. Maintaining the integrity of DNA samples is crucial for accurate analysis, and instances of contamination underscore the importance of stringent quality control measures in DNA forensics.

AI Integration in DNA Analysis Enhancing Efficiency and Accuracy in Forensic Science

One key avenue lies in the expanded use of DNA forensics in healthcare, where the integration of genetic data for personalized medicine and disease risk assessment is gaining traction. Companies like 23andMe exemplify this trend, offering DNA testing services that provide valuable health insights to individuals. Additionally, the continuous advancements in rapid DNA analysis technologies create opportunities for on-site applications, especially in law enforcement and emergency response scenarios. ANDE Corporation's Rapid DNA Analysis technology stands as a notable example, catering to the pressing need for swift and portable DNA profiling.

The enhancement of forensic databases, such as the U.S. CODIS, presents another growth opportunity by facilitating more comprehensive and efficient matching of DNA profiles. Meanwhile, ongoing technological innovations in sample analysis, particularly addressing challenges with degraded or mixed DNA samples, broaden the scope of forensic applications. Improved DNA extraction methods exemplify these advancements, contributing to the market's expansion. The integration of Artificial Intelligence (AI) into DNA analysis processes offers prospects for increased efficiency and accuracy. Companies like Cybergenetics leverage AI algorithms for complex DNA interpretation, showcasing the potential synergy between technology integration and enhanced forensic capabilities.

International collaboration and standardization efforts in the field of DNA forensics create avenues for growth, with organizations like INTERPOL promoting global cooperation and harmonized practices. Expanding the application of DNA forensics in civil identification scenarios, such as disaster victim identification and immigration cases, reflects its versatility beyond criminal investigations. Public-private partnerships contribute to innovation, with collaborations between forensic laboratories and technology providers driving the development of advanced DNA forensic solutions. Supportive legislation and policies that allocate resources for research and development in DNA forensics, as seen in the U.S. and European countries, create a conducive environment for market growth. The expansion of education and training programs in forensic science ensures a skilled workforce, driving the continued adoption and advancement of DNA analysis technologies in the field.

DNA Forensic Market Segment Analysis:

Based on Technology, the DNA Forensic Market has been divided into Polymerase Chain Reaction (PCR), Capillary Electrophoresis, Next-Generation Sequencing (NGS), Short Tandem Repeat (STR) Analysis and others. Among these, the Polymerase Chain Reaction (PCR) sub-segment is projected to generate the maximum revenue. The Polymerase Chain Reaction (PCR) sub-segment witnessed the highest market share in the global DNA Forensic Market in 2024. Polymerase Chain Reaction, a DNA amplification technique, revolutionized the field of DNA forensics by allowing the generation of millions of copies of a specific DNA segment. This capability is crucial in forensic investigations where the quantity of DNA from crime scenes is often limited. The efficiency and precision of PCR in selectively amplifying target DNA make it an indispensable tool for forensic laboratories.

The PCR sub-segment's dominance can also be attributed to its established track record in producing reliable and reproducible results. The robustness of PCR technology ensures that forensic laboratories can trust the accuracy of the obtained DNA profiles, crucial for the legal validity of the evidence presented in court. This reliability has led to the widespread acceptance and preference for PCR in forensic DNA analysis. Ongoing innovations in PCR techniques, such as real-time PCR and digital PCR, contribute to improved sensitivity, specificity, and speed in DNA analysis. These advancements align with the growing demands of forensic investigations for rapid and precise results, further solidifying PCR's position as a cornerstone technology in the DNA forensic market.

The adoption of PCR in forensic investigations extends beyond crime scene analysis. It plays a pivotal role in paternity testing, missing person identification, and disaster victim identification. The sub-segment's versatility and applicability across various forensic scenarios contribute to its sustained market dominance. Forensic laboratories, technology providers, and research institutions collaborate to enhance PCR technologies, resulting in more efficient DNA analysis solutions. These collaborations contribute to the continuous improvement and innovation within the PCR sub-segment, reinforcing DNA Forensic Market leadership.

Based on Application, the DNA Forensic market is segmented into criminal investigations, paternity testing, disaster victim identification, biodefense and others. The criminal investigations segment dominated the DNA forensic market in 2024 due to the increasing reliance of law enforcement agencies on DNA evidence for solving crimes. Rapid advancements in DNA sequencing and profiling technologies enhanced accuracy and reduced processing time, boosting adoption. Paternity testing and disaster victim identification followed, but their market share was smaller because of limited use cases. Biodefense applications remained niche, driven by government and military programs.

DNA Forensic Market Regional Insight:

North America region dominated the DNA Forensic Market in the year 2023, and is expected to continue its dominance during the forecast period. In North America, the DNA Forensic Market stands as a dynamic and influential sector, characterized by technological advancements, widespread adoption, and a robust legal framework supporting forensic investigations. The region has been a pioneer in the development and application of DNA forensic technologies, and its dominance in this market is evident through several key insights.

The United States, as a major contributor to North America's DNA forensic market, has consistently showcased leadership in the adoption and advancement of DNA analysis technologies. The Federal Bureau of Investigation's (FBI) Combined DNA Index System (CODIS) stands as a flagship example of successful DNA database implementation. CODIS facilitates the sharing of DNA profiles among federal, state, and local forensic laboratories, enhancing collaboration and aiding in the resolution of criminal cases. The United States' commitment to expanding and optimizing forensic databases contributes significantly to the region's dominance in the global DNA forensic market.

Canada, another key player in North America, has also made substantial contributions to the DNA forensic landscape. The Royal Canadian Mounted Police (RCMP) National DNA Data Bank, exemplifies Canada's commitment to leveraging DNA technology in solving crimes. The DNA Data Bank includes crime scene DNA profiles and profiles from individuals convicted of designated offenses, contributing to the effectiveness of forensic investigations across the country.

The North American region's dominance in the DNA forensic market is further underscored by the region's early adoption of innovative technologies. Next-Generation Sequencing (NGS) technologies, which have revolutionized DNA analysis, find widespread application in North American forensic laboratories. Companies like Illumina, a leader in genomic sequencing, have played a pivotal role in driving the adoption of NGS in forensic applications.

The precision and efficiency offered by NGS contribute to the region's reputation for cutting-edge forensic capabilities. Moreover, the region's dominance is reinforced by continuous research and development initiatives undertaken by academic institutions, forensic laboratories, and private enterprises. For instance, the National Institute of Justice (NIJ) in the United States consistently funds research projects aimed at advancing forensic technologies, including DNA analysis methods. This commitment to research ensures that North America remains at the forefront of technological innovation in the DNA forensic market.

The legal framework supporting DNA forensic investigations in North America also contributes to its dominance. Stringent regulations and standardized practices ensure the integrity and reliability of DNA evidence presented in courts. The utilization of DNA evidence in high-profile cases, such as the O.J. Simpson trial in the United States, has further emphasized the credibility and impact of DNA forensics in the region's legal landscape.

Competitive Landscape:

In January 2023, Life sciences firm Qiagen declared the acquisition of DNA-biometrics company Verogen in a $150-million cash deal, further bolstering its position in the forensics market. This move builds upon the existing partnership between the two companies established in 2021, where Qiagen holds the distribution rights for some of Verogen's products, including next-generation gene sequencing panels and the genetic code analyzing technology GEDmatch. Qiagen anticipates generating approximately $20 million in sales from the Verogen portfolio in the current year. While the deal is expected to have a dilutive impact of about 3 cents on Qiagen's adjusted profit per share for 2023, it is projected to be neutral to the firm's profit in 2024. This strategic acquisition underscores Qiagen's commitment to expanding its forensics portfolio and leveraging advanced DNA technologies to strengthen its position in the life sciences market.

DNA Forensic Market Scope : Inquire before buying

| Global DNA Forensic Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 2.87 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 7.1% | Market Size in 2032: | USD 4.97 Bn. |

| Segments Covered: | by Technology | Polymerase Chain Reaction (PCR) Short Tandem Repeat (STR) Analysis Capillary Electrophoresis (CE) Next-Generation Sequencing (NGS) Others |

|

| by Source | Blood Bones Hair Others |

||

| by Application | Criminal Investigations Paternity Testing Disaster Victim Identification Biodefense Others |

||

| by End-User | Law Enforcement Agencies Healthcare Providers Government Laboratories Private Forensic Laboratories Others |

||

Global DNA Forensic Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

DNA Forensic Market Key Players:

North America

1. Thermo Fisher Scientific Inc. (United States)

2. Illumina, Inc. (United States)

3. Promega Corporation (United States)

4. Agilent Technologies, Inc. (United States)

5. Bode Cellmark Forensics, Inc. (United States)

6. NEB (New England Biolabs, Inc.) (United States)

7. Forensic Analytical (United States)

8. Hamilton Company (United States)

9. IntegenX Inc. (United States)

10. Orchid Cellmark, Inc. (United States)

11. Bioscience Laboratories, Inc. (United States)

12. DNA Diagnostics Center (DDC) (United States)

13. Macy Technologies, Inc. (United States)

14. NMS Labs (United States)

15. Zymo Research Corporation (United States)

Europe

1. Qiagen N.V. (Netherlands)

2. Eppendorf AG (Germany)

3. Genomic Vision (France)

4. Microgenetics Ltd. (United Kingdom)

Asia Pacific

1. Genetic Technologies Group (Australia)

FAQ:

1] What segments are covered in the Global DNA Forensic Market report?

Ans. The segments covered in the DNA Forensic Market report are based on Technology, Source, Application, and End-User.

2] Which region is expected to hold the highest share in the Global DNA Forensic Market?

Ans. The North America region is expected to hold the highest share in the DNA Forensic Market.

3] What is the market size of the Global DNA Forensic Market by 2032?

Ans. The market size of the DNA Forensic Market by 2032 is expected to reach USD 4.97 Bn.

4] Who are the top key players in the DNA Forensic Market?

Ans. Thermo Fisher Scientific Inc. (United States), Illumina, Inc. (United States), and Promega Corporation (United States) are the top key players in the DNA Forensic Market.

5] What was the market size of the Global DNA Forensic Market in 2024?

Ans. The market size of the DNA Forensic Market in 2024 was valued at USD 2.87 Bn.