Global DNA Data Storage Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

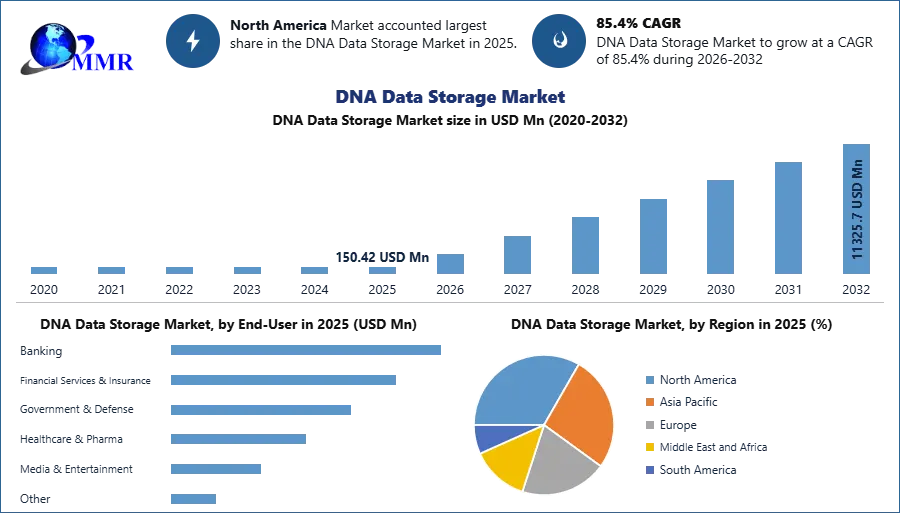

The DNA Data Storage Market size was valued at USD 150.42 Million in 2025 and the total DNA Data Storage Market revenue is expected to grow at a CAGR of 85.4 % from 2026 to 2032, reaching nearly USD 11325.7 Million.

DNA data storage is a revolutionary method that encodes digital information into the nucleotide sequences of DNA molecules. This cutting-edge technology leverages the inherent properties of DNA, such as its high density, long-term stability, and potential for immense data storage capacity. The process involves synthesizing DNA molecules with encoded information and storing them either in biological cells (in vivo) or in vitro. Retrieving the stored data requires selectively reading specific DNA sequences using advanced sequencing instruments. The DNA data storage market is experiencing unprecedented growth, driven by its potential to address the escalating demands for big data storage. As of the latest MMR analysis, the DNA data storage market is projected to grow USD 11325.7 million by 2032, showing a substantial compound annual growth rate (CAGR). Major players in this dynamic market include Illumina, Inc., Microsoft, Iridia, Inc., Twist Bioscience, and Catalog. These companies contribute to shaping the landscape of DNA data storage through innovations and strategic initiatives.

The growth in technological advancements and an increasing recognition of DNA's potential for long-term, high-density data storage. Advancements in soft-decision decoding techniques have mitigated the challenges posed by high error rates, making DNA data storage more reliable. Biomemory, a startup, has introduced DNA cards for consumers, offering a tangible and accessible DNA data storage solution. Innovative approaches like the use of a 'biological camera' for encoding and storing data within living cells show the diverse strategies driving DNA Data Storage Market growth. The unparalleled storage capacity of DNA, environmental sustainability, and the flexibility of in vivo and in vitro storage options position DNA data storage as a promising solution. Biomemory's commitment to sustainability aligns with the growing need for eco-friendly data storage solutions. The surge in global data creation, was 175 ZB in 2025, further drives the quest for alternative storage solutions, creating opportunities for DNA data storage. The DNA Data Storage also benefits from the forecasted growth of the global datasphere, reaching unprecedented levels. The advancements in nanophotonics-enabled optical storage techniques, addressing challenges and contributing to the continuous evolution of storage capabilities in DNA Data Storage market. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

DNA Data Storage Market Dynamics:

Advancements in Soft-Decision Decoding driving DNA Data Storage market growth:

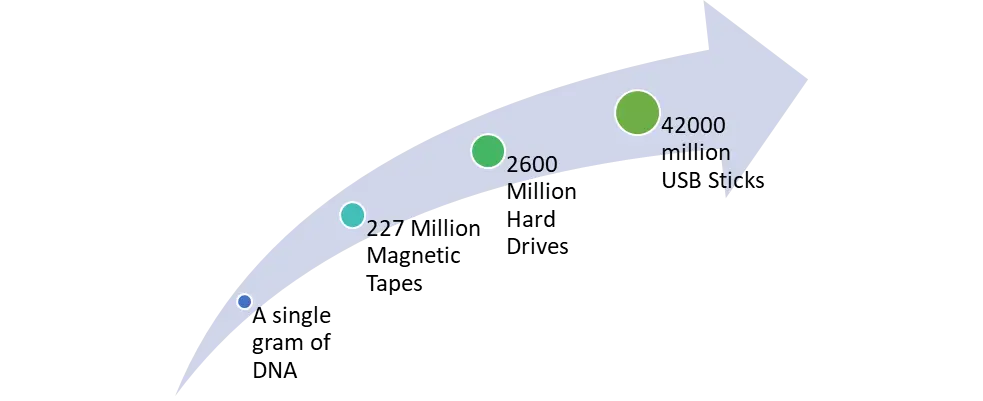

Recent breakthroughs DNA Data Storage market in soft-decision decoding significantly enhance error correction capabilities in DNA digital storage, overcoming challenges related to high error rates during synthesis, replication, storage, and sequencing. Biomemory introduces DNA cards for consumers, offering a tangible DNA data storage solution. Priced at $1,000, each card promises a minimum lifespan of 150 years and signifies a step towards making DNA storage accessible to the public. Researchers at NUS CDE pioneered a 'biological camera,' leveraging living cells to encode and store data directly within DNA. This groundbreaking approach represents a new paradigm in information storage, potentially disrupting the data storage industry. DNA's exceptional storage capacity becomes a driving force. One gram of DNA holds 215 petabytes of data, providing immense potential for addressing the growing demand for big data storage. Biomemory's commitment to environmental sustainability aligns with the growing need for eco-friendly data storage solutions. DNA's longevity and low maintenance costs contribute to a greener approach to DNA Data Storage Market.

The surge in global data creation, estimated to reach 175 ZB by 2025, drives the quest for alternative storage solutions. DNA's stability and durability position it as a viable option amidst the challenges posed by conventional data storage methods. With the global data warehouse forecast to grow exponentially, the DNA data storage market emerges as a potential solution to address the increasing demand for efficient and high-capacity storage solutions. DNA digital storage provides flexibility with options for in vivo and in vitro storage. This versatility caters to diverse storage needs and preferences in different applications. DNA data storage offers a cost-effective solution to long-term data storage needs. Its potential to last millions of years makes it an attractive option for archival purposes, reducing the need for frequent data migrations and updates. Derrick's soft-decision decoding technique not only enhances error correction but also achieves a balance between correction overhead and storage density. This technological innovation contributes to the continuous evolution of DNA data storage market capabilities.

Financial Investment Boosts DNA-Based Computation:

CATALOG's recent $35 million Series B funding, led by Hanwha Impact, accelerates the development of a computing platform utilizing synthetic DNA. This positions DNA-based computation for complex queries in industries like finance, manufacturing, and research, showing a trend toward increased investment in DNA data storage market. CATALOG's technology of encapsulating data in DNA within tiny glass spheres presents an innovative approach to preserving information. Recognized with the European Inventor Award, this trend highlights the growing importance of novel techniques, like DNA encapsulation, for long-term data storage and durability. Digital Bedrock joining the DNA Data Storage Alliance signifies a trend of collaboration among diverse stakeholders.

The Alliance, formed by industry leaders like Illumina, Microsoft, Twist Bioscience, and Western Digital, emphasizes the importance of creating an interoperable storage ecosystem based on DNA, showcasing a shift towards industry-wide cooperation. The DNA Data Storage Market Alliance's focus on DNA as an eco-friendly solution indicates a trend toward environmentally sustainable data storage. As organizations like Digital Bedrock contribute to developing interoperability standards, the industry is recognizing the potential of DNA storage to address the explosive growth of data in an eco-friendly manner. The DNA Data Storage Alliance's mission includes public education and awareness raising, indicating a trend towards promoting understanding and acceptance of DNA as a viable data storage medium. This emphasis on education is crucial for fostering the broader adoption of DNA data storage technologies. Low Speed in Data writing and Reading is the major challenge for the market:

Low Speed in Data writing and Reading is the major challenge for the market:

One major challenge in DNA data storage market is the current intrinsic low speed of data writing and reading. For instance, chemical DNA synthesis, a common method of data writing, is time-consuming, hindering the efficient storage and retrieval of information. The high cost per byte stored poses a significant challenge. Despite DNA's potential for high-density storage, the economic viability is impacted by the expenses associated with chemical DNA synthesis and sequencing processes. Current storage methods, including DNA data storage, need to address energy consumption concerns. Although DNA's archival storage has low power requirements, overall energy consumption throughout the entire storage process remains a consideration. While DNA boasts a theoretical data density of 6 bits per 1 nm of polymer, practical implementations face challenges in achieving such densities. The actual data density achieved is lower due to various factors, impacting the overall efficiency of DNA data storage market. Although DNA is stable for thousands of years under suitable conditions, ensuring long-term stability and low maintenance costs for large-scale DNA data storage systems remains a challenge. The need for consistent and reliable preservation adds complexity to the operational aspects of DNA-based storage solutions.

Chart: The Future of DNA Data Storage

DNA Data Storage Market Segment Analysis:

Based on Deployment, The DNA Data Storage market, segmented by Deployment into Cloud and On-Premise solutions, exhibits a dynamic landscape shaped by technological advancements and industry demands. Cloud deployment dominates the DNA Data Storage market, driven by its scalability, accessibility, and cost-effectiveness. Major players, including Illumina, Microsoft, and Twist Bioscience, have embraced cloud solutions, leveraging the flexibility it offers for managing vast amounts of genetic data efficiently. The On-Premise segment remains relevant, particularly in contexts where data privacy and security concerns dictate a more localized storage approach. The cloud segment's dominance stems from its ability to accommodate the growing demands of big data storage, enabling seamless collaboration and accessibility as technological innovations continue, Cloud deployment is expected to maintain its dominance, with projections indicating substantial growth, reaching USD 11325.7 million by 2032. Applications of cloud-based DNA data storage span various industries, from healthcare to research, fostering widespread adoption.

On the other hand, On-Premise solutions find prominence in sectors prioritizing stringent control over data management. The market's evolution hinges on balancing the advantages of cloud scalability with on-premise security measures. While cloud deployment currently dominates the DNA Data Storage market, both segments are integral, catering to diverse needs within an ever-expanding landscape of genetic data storage.

DNA Data Storage Market Regional Insights:

The DNA Data Storage market is experiencing significant growth globally. North America stands out as the dominant region in the market. The presence of key players such as Illumina, Inc., Microsoft, and Twist Bioscience in the region has propelled North America to the forefront of DNA Data Storage innovation and adoption. These companies are at the forefront of developing cutting-edge technologies, fostering research, and driving DNA Data Storage growth. For instance, Illumina, Inc., a major player in the DNA Data Storage market, has been instrumental in advancing sequencing technologies.

North America currently dominates the DNA Data Storage market, while the Asia Pacific region emerges as a promising contender for substantial growth. With a burgeoning biotechnology sector and increasing investments in research and development, Asia Pacific is poised to witness rapid market growth. For instance, China-based BGI Shenzhen and Berry Genomics are actively contributing to the market's growth in the region. Their endeavors in developing innovative DNA data storage solutions reflect the region's commitment to technological advancement.

Europe, with companies like Thermo Fisher Scientific and Siemens playing a pivotal role, maintains a strong position in the DNA Data Storage industry. Thermo Fisher Scientific, Siemens, and Eurofins Scientific are key players dominating the European DNA Data Storage market. Their focus on research and development, strategic partnerships, and market growth initiatives contribute to the region's market influence. Europe is expected to experience steady growth, driven by advancements in DNA data storage technologies. The dynamics of the DNA Data Storage market highlight a global landscape where different regions contribute to overall growth, reflecting the industry's collaborative and evolving nature.

| Sector | Organization | Primary Effort |

| Private | Microsoft | R&D with the eventual goal of a proto-commercial DNA data storage system |

| Private | Semiconductor Research Corporation | R&D in advanced alternative data storage solutions |

| Private | Catalog | Commercialization of DNA data storage technology |

| Private | Iridia | Commercialization of DNA data storage technology |

| Public | NSF, IARPA, DARPA, NIH | Funding support to key players in the DNA data storage field |

| Academia | University of Washington | Research that is pushing towards increasing the volume of information stored in DNA |

| Academia | Harvard University | R&D of DNA synthesis technology and novel mechanisms of encoding and retrieving information from DNA |

| Academia | ETH Zurich | Research on storing varying types of files in DNA |

DNA Data Storage Market Competitive Landscape

In recent breakthroughs, Biomemory launched DNA Cards, making DNA data storage accessible to the public, promising a minimum lifespan of 150 years. Catalog secured $35 million in Series B funding, advancing DNA-based computation systems. NUS CDE pioneered a 'biological camera' for encoding data directly within DNA, presenting a paradigm shift. Additionally, the DNA Data Storage Alliance, joined by Digital Bedrock, focuses on creating interoperable standards. These innovations address the pressing need for sustainable, high-capacity data storage solutions amid the explosive growth of global data. Biomemory's consumer-friendly DNA Cards and advancements in DNA computation contribute significantly to shaping the future of data storage.

On December 4, 2023, Biomemory introduced DNA Cards, a groundbreaking leap in data storage technology. These credit card-sized marvels offer one kilobyte of text data storage each, making DNA data storage accessible to the public for the first time. Developed by Biomemory, DNA Cards provide a sustainable alternative to traditional silicon chips, utilizing molecular computing. With a minimum lifespan of 150 years, they set a new standard for data longevity. In a world producing and consuming 100 trillion gigabytes annually, Biomemory addresses the urgency for innovative storage solutions, offering a more energy-efficient and space-saving approach amidst growing concerns about environmental impact.

On June 23, 2022, SNIA declared a significant advancement in the storage industry, initiating technical work and standards development for the interoperability of DNA Data Storage solutions. The DNA Data Storage Alliance established in 2020 by Illumina, Inc., Microsoft, Twist Bioscience Corporation, and Western Digital, joins SNIA as a Technology Affiliate. This collaboration leverages SNIA's 25 years of open standards development experience to accelerate the creation of an interoperable ecosystem for DNA-based data storage solutions under the SNIA IP Policy structure.

On May 30, 2022, MoleculArXiv's exploratory Priority Research Programme and Equipment (PEPR), led by CNRS, launched with a 20 million euro budget over 7 years. The initiative aims to pioneer innovative data storage devices utilizing molecular media, including DNA and artificial polymers. With global data estimated to reach 175 zettabytes by 2025, traditional storage methods have become inadequate. Addressing this, the program explores chemically synthesized DNA as a sustainable and energy-efficient solution, countering the challenges posed by growing data quantities and environmental concerns in conventional data centers.

DNA Data Storage Industry Ecosystem

DNA Data Storage Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 05 May 2025 | Twist Bioscience Corporation | The company officially spun out its specialized DNA data storage technology division into an independent entity named Atlas Data Storage. | This strategic move allows for dedicated capital allocation and accelerated commercialization of molecular storage solutions. |

| 09 March 2026 | Mimulus Technologies Inc. | Entered a strategic partnership with Expand Entertainment LLC to provide customized DNA-based archival solutions for digital media. | The collaboration facilitates the long-term preservation of high-value entertainment content using ultra-high-density molecular storage. |

| 15 January 2026 | Biomemory SAS | Announced the final production phase of Biomemory Prime, a compact DNA storage device with a 100 petabyte capacity. | The launch positions DNA storage as a viable competitor to magnetic tape for large-scale data center operations. |

| 22 October 2025 | Catalog Technologies, Inc. | Successfully demonstrated an automated DNA-based computing and storage workflow integrated with Seagate’s "lab on a chip" technology. | The integration significantly reduces chemical consumption and improves the speed of DNA data retrieval. |

| 11 February 2026 | Iridia, Inc. | Unveiled a new nanopore-based read-head module designed for high-throughput decoding of synthetic DNA strands. | This hardware advancement reduces latency in data access, addressing one of the primary hurdles for commercial DNA storage adoption. |

DNA Data Storage Market Scope: Inquiry Before Buying

| DNA Data Storage Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 150.42 USD Mn |

| Forecast Period 2026-2032 CAGR: | 85.4% | Market Size in 2032: | 11325.7 USD Mn |

| Segments Covered: | by Deployment | Cloud On-Premise |

|

| by Sequencing Platform | Next-Generation Sequencing Nanopore Sequencing |

||

| by Synthesis Platform | Chemical-Column Based Chemical-Microchip Based Enzymatic |

||

| by End-User | Banking Financial Services & Insurance Government & Defense Healthcare & Pharma Media & Entertainment Other |

||

DNA Data Storage Market, by region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

DNA Data Storage Market Key Players

- Illumina Inc. (California, United States)

- Microsoft Corporation

- Twist Bioscience Corporation

- Agilent Technologies Inc.

- Thermo Fisher Scientific Inc.

- Catalog Technologies Inc.

- DNA Script SAS

- Iridia Inc.

- Evonetix Ltd.

- Molecular Assemblies Inc.

- Western Digital Corporation

- Quantum Corporation

- GenScript Biotech Corporation

- Beckman Coulter Inc.

- Eurofins Scientific SE

- Micron Technology Inc.

- Seagate Technology Holdings plc

- Biomemory SAS

- Ansa Biotechnologies Inc.

- Helixworks Technologies Ltd.

- Kilobaser

- DNASign

- BGI Group

- Imec

- Cegat GmbH