Distributed Generation Market Size by Technology, Application, End User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

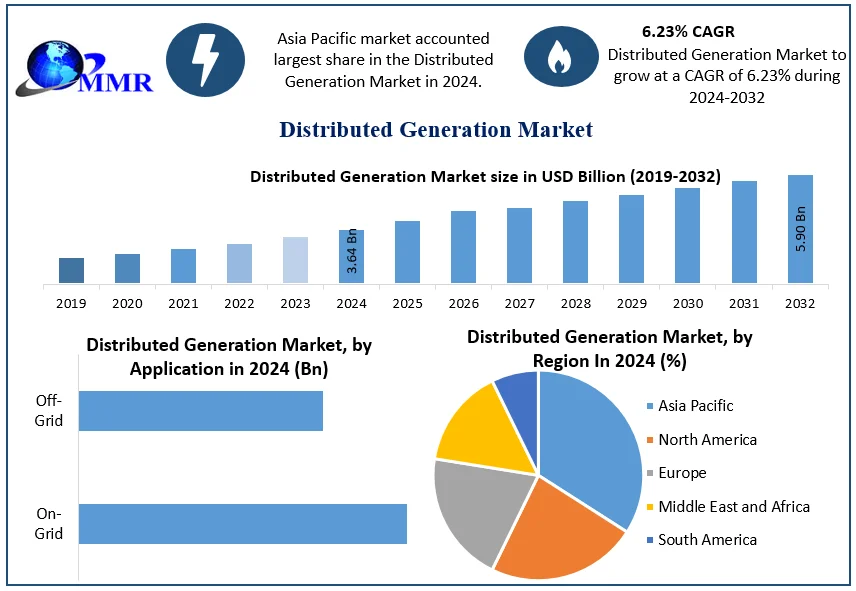

Global Distributed Generation Market size was valued at USD 3.64 Bn in 2024 and is expected to reach USD 5.90 Bn by 2032, at a CAGR of 6.23 %.

Overview

Distributed Generation (DG) represents a paradigm shift in power generation, generating electricity near end-users rather than relying solely on centralized plants. Different from traditional grids, DG includes various sources such as solar, wind, and fuel cells. Its proximity to consumers reduces power losses and offers benefits such as increased grid resilience and capacity expansion without building new central plants. However, challenges arise from the decentralized nature of DG installations, requiring careful regulation and grid integration. Operational and planning considerations must adapt to bidirectional power flows, necessitating updates to interconnection standards, equipment requirements, and planning procedures. Policymakers and utilities need to prioritize advanced inverter functions and transparent interconnection processes to optimize DG's potential while ensuring grid stability and reliability. Key players in the DG market include Siemens AG, General Electric Company, Schneider Electric SE, and ABB Ltd. The Distributed Generation Market continues to grow as advancements in technology and growing environmental awareness drive increased adoption of distributed energy resources.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Distributed Generation Market Dynamics

Renewable Energy Integration to Boost the Market Growth

The Distributed Generation (DG) market is surging due to the increasing demand for renewable energy integration. As society pivots towards sustainable practices, DG technologies, such as solar panels and wind turbines, play a pivotal role in decentralizing power production. This decentralization mitigates transmission losses and enhances grid reliability. Governments worldwide incentivize the adoption of renewable DG sources, driving a favorable market environment. The ability to harness clean energy locally not only reduces carbon footprints but also ensures a more resilient and efficient energy infrastructure.

Another critical trend driving the growth of the Distributed Generation Market is the continuous advancement in energy storage technologies. As energy storage capabilities improve, DG systems become more reliable and efficient. Energy storage solutions, such as advanced batteries, facilitate better grid management, load balancing, and increased resilience during peak demand periods or intermittent renewable energy generation. This trend is pivotal in addressing the intermittency challenges associated with renewable sources, making DG systems more versatile and appealing to a broader range of applications.

The International Energy Agency estimates that the majority of global electricity will need to be generated using renewables to reach net-zero emissions by 2050. The U.S. has set a goal of generating 100% clean electricity by 2035 and many states have implemented targets for lower emissions—all of which have required an increased reliance on renewables. In the U.S., the use of renewables has increased significantly, but even higher levels of renewable integration will be needed to achieve a net-zero economy by 2050.

Energy Security and Reliability to Boost the Market

Energy security is a paramount concern driving the growth of the DG market. Distributed Generation provides a solution by diversifying energy sources and reducing dependence on centralized power plants. This decentralized model enhances grid reliability, minimizing the impact of localized outages and improving energy resilience. Industries and communities increasingly turn to DG systems, like combined heat and power (CHP) units, for on-site power generation, reducing vulnerability to disruptions and ensuring a stable energy supply during peak demand periods.

Technological Advancements and Cost Efficiency Trends to Drive the Market

Technological advancements and cost efficiency are key catalysts propelling the DG market forward. Improvements in energy storage, smart grid technologies, and the decreasing costs of solar and wind components make DG solutions more accessible. As the efficiency of distributed generation systems increases, the overall cost of implementation decreases, making them economically competitive with traditional power sources. This cost-effectiveness attracts businesses and consumers alike, accelerating the adoption of DG technologies and further driving innovation in the market.

Opportunity: Microgrid Expansion for Energy Resilience

An exciting opportunity within the Distributed Generation Market lies in the expansion of microgrids to enhance energy resilience. With a growing awareness of the vulnerabilities of centralized power grids to disruptions, there is a rising demand for microgrid solutions that can operate independently or in conjunction with the main grid. This presents an opportunity for DG providers to develop and deploy advanced microgrid technologies that ensure a reliable and resilient energy supply during emergencies, natural disasters, or grid failures. As governments and businesses prioritize energy security, of microgrids represent a strategic avenue for growth in the Distributed Generation Market. Microgrids, revolutionary in energy management, securing a 44% revenue share. This growth is due to governmental incentives, public sectors and institutions adopted electric vehicles (EVs) like buses and taxis, propelling commercial EV growth. Rising fuel costs further incentivized the shift to EVs for long-term operational savings. Looking ahead, from 2025-2032, Battery Electric Vehicles (BEVs) are projected to be the fastest-growing segment, driven by environmental awareness, tax incentives, and government schemes promoting sustainable mobility solutions. This shift signifies a transformative period in the global vehicle market, aligning with the push for cleaner and more sustainable transportation options.

High-Cost Requirement for Grid Integration Issues to Restrain the Market Growth

As the share of distributed energy resources increases, utilities face challenges in managing grid stability, voltage regulation, and power quality. The intermittent nature of renewable sources like solar and wind exacerbates these issues. Upgrading existing infrastructure to accommodate bidirectional power flows and implementing advanced grid management technologies is a costly and time-consuming process. Overcoming grid integration challenges is imperative for maximizing the benefits of distributed generation and ensuring a reliable and resilient energy system for the future.

Such a critical factor limiting the growth of the Distributed Generation market is the difficulty in integrating these decentralized energy sources into existing power grids. For instance, In India, the cost of an on-grid solar power system ranges from Rs.66,999 for a 1 kW system to Rs.4,37,480 for a 10 kW system with installation. Transportation, installation, net metering, and all other costs are included in purchasing a solar system.

Distributed Generation Market Segment Analysis

Based on technology, the fuel cell segment held the largest market share in 2024. This dominance is influenced by the escalating adoption of fuel cells within distributed generation systems, driven by their advantageous features such as high efficiency, reduced emissions, and the capability to convert chemical energy into electrical energy. Particularly, fuel cells boast a 60% higher efficiency, emerging as a significant catalyst for the segment's growth. Also, the solar PV segment is expected to grow at a significant CAGR during the forecast period.

Government subsidies promoting solar energy adoption, coupled with declining costs of solar equipment, have spurred demand for solar PV in the distributed generation market. The concerted efforts of governments and corporations to curtail carbon footprint, coupled with a pursuit of long-term sustainability, are propelling industries towards embracing solar energy sources.

Based on the End User, the industrial segment held the largest market share in 2024. This ascendancy is attributed to heightened government initiatives incentivizing the adoption of renewable energy in commercial and industrial sectors. Additionally, reduced equipment costs and a heightened demand for uninterrupted power supply have driven segment growth. Government-led endeavors to industrialize and urbanize rural regions further bolster the commercial and industrial segment, positioning it for continued dominance throughout the forecast period. The residential segment emerges as a lucrative opportunity, anticipating significant growth. Factors such as the proliferation of large residential complexes and rapid urbanization in rural regions drive this growth. The increasing adoption of distributed generation systems for diverse applications, including heating, ventilation, cooling, and cooking, is poised to elevate demand within the residential segment during the forecast period.

Distributed Generation Market Regional Analysis

In 2024, the Asia Pacific region emerged as the dominant force in the global distributed generation market, seizing a substantial market share exceeding 45%. This dominance can be attributed to the escalating uptake of renewable energy sources, heightened investments in industrialization and urbanization, rapid infrastructural developments, and governmental initiatives fostering the deployment of renewable and eco-friendly energy sources. The region's increasing industrialization has spurred a notable surge in the demand for efficient and uninterrupted power supply, further propelling the growth of the distributed generation market in Asia Pacific.

As the region continues to prioritize sustainable energy solutions, the distributed generation sector stands to benefit from the confluence of these factors, positioning Asia Pacific as a pivotal player in shaping the future landscape of decentralized power generation.

Competitive Landscape

In the competitive landscape of Distributed Generation, key players such as Siemens, General Electric, Schneider Electric, and Bloom Energy stand out. Siemens and General Electric lead with comprehensive solutions, leveraging advanced technologies. Schneider Electric focuses on smart energy management, while Bloom Energy specializes in innovative fuel cell solutions. These industry leaders compete by offering diverse and efficient distributed generation technologies, catering to a growing demand for decentralized energy solutions. The competition is marked by continuous innovation, strategic partnerships, and a commitment to addressing evolving energy challenges in an increasingly decentralized and sustainable global energy landscape.

Distributed Generation Market Scope: Inquire before buying

| Distributed Generation Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | US $ 3.64 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 6.23% | Market Size in 2032: | US $ 5.90 Bn. |

| Segments Covered: | by Technology | Solar PV Wind Reciprocating Engines Microturbines Fuel Cell Gas Turbines |

|

| by Application | On-Grid Off-Grid |

||

| by End User | Industrial Commercial Residential |

||

Distributed Generation Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Distributed Generation Key Players by Region

North America

1. General electric (ge) usa

2. Capstone Green Energy

3. Caterpillar inc. usa

4. FuelCell Energy: USA

5. Cummins Inc.: USA

6. Bloom Energy: USA

7. Bergey Windpower: USA

Europe

8. Siemens AG: Germany

9. Schneider Electric: France

10. Vestas Wind Systems A/S: Denmark

11. Rolls-Royce Power Systems AG: Germany

12. Ansaldo Energia: Genoa, Italy

APAC

13. Mitsubishi Heavy Industries: Japan

14. Torrent Power

15. RattanIndia Power

16. China Yangtze Power Company

17. Tokyo Electric Power Company

18. Distributed Energy

Middle East and Africa

19. Sharaf DG Energy

20. Ignite Power

21. Abu Dhabi National Energy Company

22. Savannah Energy

23. Viathan

South America

24. Eletrobras

25. CPFL Energia

Frequently Asked Questions:

1] What is the growth rate of the Global Distributed Generation Market?

Ans. The Global Distributed Generation Market is growing at a significant rate of 6.23 % during the forecast period.

2] Which region is expected to dominate the Global Distributed Generation Market?

Ans. APAC is expected to dominate the Distributed Generation Market during the forecast period.

3] What is the expected Global Distributed Generation Market size by 2032?

Ans. The Distributed Generation Market size is expected to reach USD 5.90 Bn by 2032.

4] Which are the top players in the Global Distributed Generation Market?

Ans. The major top players in the Global Distributed Generation Market are General Electric (GE), Capstone Turbine Corporation and others.

5] What are the factors driving the Global Distributed Generation Market growth?

Ans. The microgrid expansion and technological advancement in Distributed Generation are key drivers of Distributed Generation Market growth.

6] Which country held the largest Global Distributed Generation Market share in 2024?

Ans. China held the largest Distributed Generation Market share in 2024.