Display Material Market Size by Material, Technology, Application, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2034

Overview

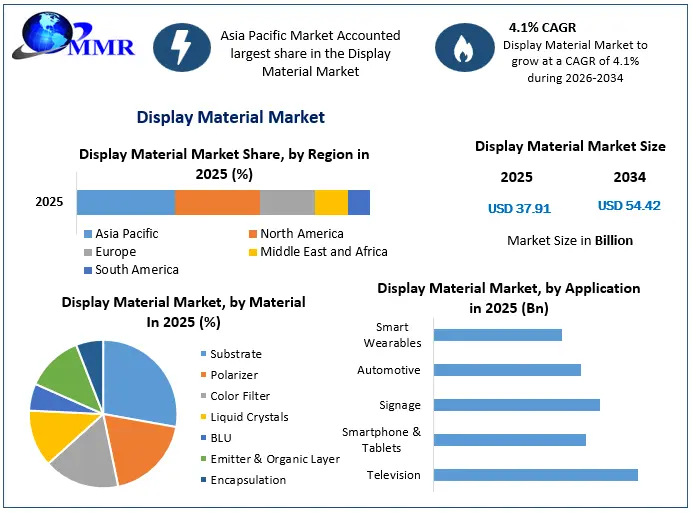

Global Display Material Market size was valued at USD 37.91 Bn. in 2025 and is expected to reach USD 54.42 Bn. by 2034, at a CAGR of 4.1% from forecast 2026 to 2034.

Display Material Market Overview

The display material market is experiencing robust growth due to the rising demand for advanced display technologies across various industries. Advancements in technology in display materials like quantum dots, micro LEDs, and organic semiconductors have led to market expansion by enabling high-resolution, energy-efficient, and flexible displays. The consumer electronics sector is a major consumer of display materials as the demand for immersive visual experiences and high-resolution screens continues to grow.

The automotive industry is also adopting display materials for advanced infotainment systems and digital instrument clusters. Additionally, the market is witnessing a shift towards eco-friendly and sustainable display materials, with manufacturers investing in research and development to reduce energy consumption and promote recyclability. Collaborations, partnerships, and strategic acquisitions among key players are further driving market growth and strengthening product portfolios. Continued research and development efforts are focused on meeting evolving consumer demands and enhancing visual experiences. Overall, the display material market is expected to thrive, offering opportunities for manufacturers, suppliers, and consumers, as the demand for innovative and sustainable display technologies continues to increase across industries.

Display Material Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

Display Material Market Dynamics

Unlocking Growth Opportunities in the Display Material Market

Advanced Material Development, Emerging Technologies, Industry Collaboration, and Sustainable Practices

The display material market presents promising growth prospects for manufacturers looking to capitalize on evolving market dynamics and consumer demands. Advanced material development stands as a key opportunity, as ongoing research and innovation yield materials with improved performance characteristics, such as higher resolution and energy efficiency, to meet the increasing demand for enhanced display technologies. Embracing emerging technologies, such as flexible and foldable displays, presents another avenue for growth, catering to consumer preferences for innovative and immersive visual experiences across various devices.

Collaboration within the industry also unlocks growth potential, as partnerships and alliances can foster knowledge exchange, shared resources, and accelerated development of new display materials. Collaborative efforts can address challenges and promote innovation, driving market growth and competitiveness. Additionally, sustainability is a critical opportunity for manufacturers to respond to the growing consumer demand for environmentally friendly display materials. By adopting sustainable practices, such as using recyclable materials and reducing energy consumption during production, manufacturers can meet consumer expectations, comply with regulations, and enhance their brand reputation.

Overcoming Restraints and Challenges in the Display Material Market

Technological Advancements, Price Competitiveness, and Environmental Sustainability

The display material market encounters various challenges and restraints that necessitate proactive measures to drive growth and success. Technological advancements pose a significant challenge as the market continually evolves. Manufacturers must stay at the forefront of emerging display technologies, such as OLED, micro-LED, and quantum dot, to meet the demand for higher resolutions, improved colour reproduction, and energy efficiency.

Price competitiveness is another challenge in the display material market. As the competition in the market increases, manufacturers strive to find ways to offer solutions that are cost-effective without compromising on quality. To achieve price competitiveness while delivering value to customers, manufacturers work on Effective cost management, efficient supply chain practices, and strategic partnerships

Environmental sustainability is a critical challenge that requires attention in the display material market. As consumers become more environmentally conscious, they demand products and materials that have minimal environmental impact. Manufacturers must prioritize sustainability by using eco-friendly materials, reducing energy consumption during production, and adopting recycling and waste management practices. Meeting sustainability demands not only aligns with consumer expectations but also positions manufacturers as responsible and socially conscious market players.

By addressing these challenges through continuous technological innovation, cost optimization strategies, and sustainability initiatives, manufacturers in the display material market can navigate the complexities of the industry, capture growth opportunities, and establish themselves as leaders in a competitive market landscape.

Trends in the Display Material Market

High Resolution and Enhanced Visual Quality, Flexible and Bendable Displays, Sustainability, and Integration of Advanced Technologies

The display material industry is witnessing notable market trends that are shaping the future of display technology. High resolution and enhanced visual quality are key drivers as consumers demand sharper images, vibrant colours, and immersive viewing experiences. Manufacturers are focusing on developing display materials that offer superior pixel density, wider colour gamuts, and improved contrast ratios to meet these expectations.

Flexible and bendable displays have gained traction as consumers seek more versatile and adaptable screen solutions. These displays offer new possibilities for innovative product designs, including curved screens, foldable devices, and rollable displays. The trend towards flexible displays provides enhanced user experiences and opens up opportunities for unique applications in various industries.

Sustainability is a significant trend driving the display material market, driven by the increasing emphasis on environmental responsibility. Manufacturers are incorporating eco-friendly materials and adopting sustainable production practices to reduce the carbon footprint of display technologies. This includes utilizing recyclable materials, minimizing energy consumption during manufacturing processes, and implementing responsible disposal and recycling methods.

Display Material Market Segmentation

By Technology:

The display material market is segmented based on the technology used in display manufacturing, which include LCD, OLED, LED, and QLED. LCD accounts for approximately 65% of the total revenue. Due to their cost-effectiveness, high resolution, and widespread application in various they are popular. LCD technology offers excellent colour reproduction and energy efficiency, making it a preferred choice for large-size displays in televisions and monitors.

Display Material Market Regional Insight

Display Material Market Regional Insight

The display material market exhibits distinct regional dynamics, presenting diverse growth opportunities for businesses. Asia Pacific commands a significant market share of approximately 45% in 2025, driven by its robust manufacturing base, growing consumer electronics sector, and widespread adoption of digital signage. Key players in this region include China, South Korea, and Japan, known for their technological advancements and major display manufacturing capabilities.

North America holds a market share of around 30%. Prominent technology companies, high consumer purchasing power, and increasing investments in smart technologies fuel the demand. The United States plays a important role in driving market growth, focusing on innovative display technologies for applications in smartphones, televisions, and automotive displays.

Europe represents a significant display material market share of approximately 20%, characterized by its emphasis on high-quality visual experiences, thriving consumer electronics market, and rising demand for digital signage solutions. Germany, the United Kingdom, and France combine advanced manufacturing capabilities with strong consumer demand for cutting-edge display technologies.

Latin America captures a smaller display material market share of around 4%, propelled by its expanding middle-class population, rising consumer spending on electronics, and growing demand for visual displays in the retail and hospitality sectors. Brazil, Mexico, and Argentina are key markets within the region, offering opportunities for display material manufacturers to cater to the demand for vibrant and immersive display solutions.

The Middle East and Africa region represents an emerging market, with a market share of approximately 1%. The region's increasing urbanization, substantial investments in infrastructure projects, and a growing consumer electronics market contribute to market growth. United Arab Emirates, Saudi Arabia, and South Africa serve as key markets, presenting opportunities for display material manufacturers to provide advanced display technologies across various sectors, including retail, hospitality, and healthcare.

Display Material Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 March 2026 | Samsung Display | The company announced a significant capacity expansion of its eighth-generation OLED production facilities. | This move aims to meet the surging demand for high-performance displays in smartphones, tablets, and IT devices. |

| 12 February 2026 | LG Display | The company finalized the divestment of two Chinese LCD production lines to TCL CSOT for USD 1.5 billion. | This strategic shift accelerates the company's transition toward premium OLED technologies and improved profitability. |

| 10 January 2026 | BOE Technology Group | The manufacturer reached a milestone by securing a dominant 76% share of the global LCD production market. | This dominance underscores the critical role of scale efficiency in maintaining cost leadership for large-area display panels. |

| 18 November 2025 | Vedanta Ltd | The firm confirmed an investment of USD 500 million into AvanStrate Inc for advanced display glass R&D. | This investment strengthens the domestic supply chain for semiconductor and display-grade glass in India. |

Display Material Market Competitive Landscape

The detailed report on the display material market provides comprehensive analysis of each company's SWOT analysis, financial performance, and other relevant factors. Companies internal strengths and weaknesses, external opportunities and threats, and financial stability is provided in the report. The report enables stakeholders to assess the market dynamics, make informed business decisions, and identify growth opportunities.

Several major players have emerged in the market, each employing various strategies to enhance their market presence and solidify their positions. These key players include LG Display Co., Ltd., Samsung Display Co., Ltd., Corning Incorporated, Japan Display Inc., and Universal Display Corporation. They have demonstrated their commitment to the industry through substantial investments in research and development initiatives.

Display Material Market Scope: Inquire before buying

| Global Display Material Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 37.91 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 4.1% | Market Size in 2034: | US $ 54.42 Bn. |

| Segments Covered: | By Material | Substrate Polarizer Color Filter Liquid Crystals BLU Emitter & Organic Layer Encapsulation |

|

| By Technology | LCD OLED AMOLED Others |

||

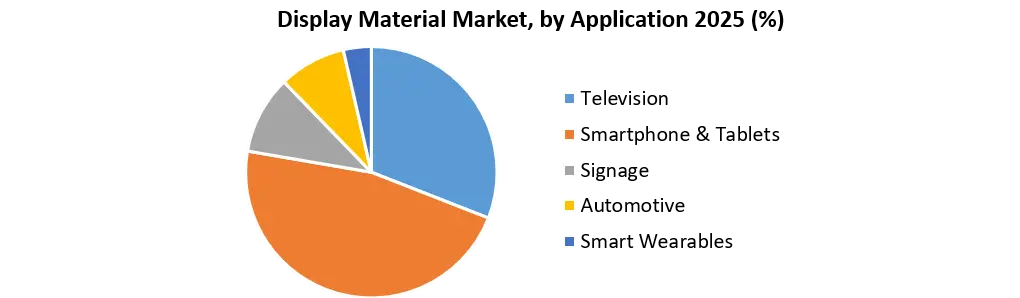

| By Application | Television Smartphone & Tablets Signage Automotive Smart Wearables |

||

Display Material Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Display Material Market Key Players

1. Samsung SDI (South Korea)

2. LG Chem (South Korea)

3. Sumitomo Chemical (Japan)

4. Corning (US)

5. Nitto Denko (Japan)

6. Universal Display Corporation (US)

7. Merck (Germany)

8. Asahi Glass (Japan)

9. Idemitsu Kosan (Japan)

10. DowDuPont (US)

11. Toray (Japan)

12. DIC Corporation (Japan)

13. Samsung Display Co., Ltd.

14. Innolux Corporation

15. AU Optronics Corporation

Frequently Asked Questions:

1] What is the growth rate of the Global Display Material Market?

Ans. The Global Display Material Market is growing at a significant rate of 4.1% during the forecast period.

2] Which region is expected to dominate the Global Display Material Market?

Ans. The Asia Pacific region is expected to dominate the Display Material Market during the forecast period.

3] What is the expected Global Display Material Market size by 2034?

Ans. The Display Material market size is expected to reach USD 54.42 Billion by 2034.

4] Which are the top players in the Global Display Material Market?

Ans. The major top players in the Global Market are LG Display Co., Ltd., Samsung Display Co., Ltd., Corning Incorporated, Japan Display Inc., and Universal Display Corporation.