Diabetes Devices Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2029

Overview

The Diabetes Devices Market was valued at USD 28.12 billion in 2022 & is expected to grow to USD 30.34 billion by 2029, representing a compound annual growth rate (CAGR) of 6.2% during the forecast period.

Diabetes Devices Market Overview

The Diabetes Devices Market focuses on manufacturing, developing and distributing devices for diabetes management and treatment. Diabetes devices aid in monitoring blood glucose, administering insulin and managing the condition. The Diabetes Devices Market is growing due to rising global diabetes prevalence. Blood glucose monitoring systems are essential devices in the market. These devices measure blood glucose levels for individuals with diabetes. Traditional glucose metres require finger pricks for blood samples, while CGM systems offer real-time glucose readings through body-attached sensors. CGM systems are popular for their convenience and ability to minimise finger pricks. Insulin Delivery Systems are essential for managing diabetes. Insulin regulates blood glucose levels and delivery systems aid its administration. The systems consist of insulin pens, pumps and syringes. Insulin pens: portable, convenient method for insulin injection.

Insulin pumps: provide continuous insulin supply through small device. Insulin syringes are used for manual insulin administration and have different sizes and capacities. CGM systems have advanced recently. These devices monitor glucose levels with a subcutaneous sensor. CGM systems offer real-time glucose readings and potential alerts for high or low blood sugar levels. This technology aids diabetes management and prevents hypoglycemia and hyperglycemia. The Diabetes Devices Market is driven by technological innovations. Manufacturers aim for compact, precise and user-friendly devices. Smartphone app integration and connectivity features are growing in popularity for seamless data monitoring and analysis.

The market is experiencing a notable increase in CGM system adoption. CGM systems are popular among people with diabetes due to their ability to provide real-time glucose data without frequent finger pricks. These systems benefit individuals with diabetes by improving glycaemic control, reducing complications risk and enhancing quality of life. Growing focus on closed-loop systems, aka artificial pancreas systems. The goal of these systems is to automate insulin delivery using continuous glucose monitoring. Artificial pancreas systems can revolutionise diabetes care by offering personalised and precise management. The Diabetes Devices Market is growing in emerging markets. In developing countries, diabetes prevalence is rising, driving up demand for diabetes devices. Factors driving market growth in these regions include improved healthcare access, increased diabetes awareness and government initiatives. Personalised diabetes management is growing in popularity. There is a trend towards personalised approaches that cater to individual needs and preferences. The offerings consist of customizable insulin delivery systems, personalised glucose targets and data-driven decision-making via digital platforms. Personalised diabetes management optimises treatment outcomes and improves well-being for individuals with diabetes. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Diabetes Devices Market Dynamics

Market Drivers:

Global diabetes prevalence drives the Diabetes Devices Market. Diabetes devices to manage the disease are in demand as the number of diabetics rises. Manufacturers address patients' needs to develop the market. Technological advancements play a significant role as a market driver. Continuous innovations in diabetes devices, such as miniaturization, improved accuracy, wireless connectivity and integration with smartphone apps, enhance their convenience, usability and effectiveness. These technological advancements attract both healthcare providers and individuals with diabetes, driving market growth. The growing awareness about diabetes and its management, coupled with higher healthcare expenditure, is another driver of the Diabetes Devices Market. Governments and healthcare organizations are increasingly focusing on diabetes prevention and management programs. This heightened awareness and increased healthcare spending contribute to the adoption of diabetes devices, creating a favorable market environment.

Market Trends:

The adoption of Continuous Glucose Monitoring (CGM) Systems is a prominent trend in the Diabetes Devices Market. CGM systems provide real-time glucose readings, reducing the need for frequent finger pricks. They offer improved glycemic control, help prevent hypoglycemia and hyperglycemia and provide valuable insights for personalized diabetes management. The growing acceptance and demand for CGM systems contribute to their increasing adoption in the market.

The integration of Artificial Intelligence (AI) and data analytics in diabetes devices is another significant trend. AI algorithms can process and analyze glucose patterns, predict blood sugar trends and offer personalized recommendations for insulin dosing and lifestyle modifications. This trend enables more precise and data-driven diabetes management, enhancing patient outcomes and driving the market forward. There is a strong trend towards developing user-friendly and convenient diabetes devices. Manufacturers are focusing on creating devices with intuitive interfaces, easy-to-use features, smaller form factors and enhanced portability. These user-centric designs allow individuals with diabetes to manage their condition with greater ease, discretion and convenience.

Market Opportunities:

Emerging markets present significant growth opportunities for diabetes device manufacturers. Developing regions, such as Asia Pacific and South America, are experiencing an increasing prevalence of diabetes, coupled with improving healthcare infrastructure, rising disposable incomes and growing awareness of diabetes management. These factors create a favorable market environment and present opportunities for market expansion and penetration. Personalized diabetes management is an emerging opportunity in the market. There is a growing demand for tailored treatment plans and recommendations based on an individual's specific needs, lifestyle and glucose patterns. Innovative diabetes devices and digital health platforms that provide personalized solutions have the potential to meet this demand and capture market opportunities.

Market Threats:

Stringent regulatory requirements pose a significant threat to diabetes device manufacturers. Compliance with regulatory standards and obtaining necessary approvals can be challenging and time-consuming. Changes in regulatory landscapes and stringent regulations can hinder market entry and slow down product development, affecting market growth. Reimbursement issues are another potential threat. Limited or inadequate reimbursement policies for diabetes devices in certain regions may hinder market growth. High costs of devices and consumables, along with reimbursement limitations, can restrict access to diabetes management technologies, affecting market adoption.

Market Challenges:

Product affordability is a major challenge in the Diabetes Devices Market. The high cost of diabetes devices and associated consumables can be a barrier, particularly for individuals in low-income and developing regions. Addressing affordability issues is crucial to ensure broader access and market penetration. Ensuring device accuracy and reliability remains a challenge. Consistent and accurate blood glucose readings, reliable insulin delivery and sensor longevity are essential for effective diabetes management. Manufacturers need to continuously improve device accuracy and reliability to meet the high standards expected by healthcare providers and individuals with diabetes.

Diabetes Devices Market Regional Analysis

North America holds a significant share in the Diabetes Devices Market, driven by its advanced healthcare infrastructure and high prevalence of diabetes. The region benefits from a mature market where the adoption of diabetes management technologies, such as blood glucose monitoring systems, insulin delivery systems and continuous glucose monitoring (CGM) systems, is widespread. Favourable reimbursement policies and supportive government initiatives further contribute to the growth of the market in North America. The presence of key market players and continuous technological advancements in diabetes devices also play a crucial role in driving market expansion in this region. Europe is another prominent region in the Diabetes Devices Market, characterized by a high prevalence of diabetes and a well-established healthcare system.

The region exhibits a growing awareness of diabetes management and favourable reimbursement policies for diabetes devices, which propel market growth. European market players are actively involved in product innovation and technological advancements to cater to the evolving needs of patients. The adoption of CGM systems and insulin delivery devices is on the rise in the region. Collaborations between healthcare organizations and device manufacturers further stimulate market development and drive the growth of the Diabetes Devices Market in Europe. The Asia Pacific region presents significant growth opportunities for the Diabetes Devices Market. The region has witnessed a rapid increase in the prevalence of diabetes due to lifestyle changes, urbanization and an aging population. Improving healthcare infrastructure, rising disposable incomes and increasing awareness of diabetes management contribute to enhanced affordability and accessibility to diabetes devices. Market players recognize the potential in the Asia Pacific market and are expanding their presence by introducing innovative and cost-effective devices tailored to the specific needs of Asian populations. Government initiatives aimed at addressing diabetes and raising awareness among patients further fuel market growth in the Asia Pacific region. South America is experiencing steady growth in the Diabetes Devices Market. The region faces a growing prevalence of diabetes, primarily driven by lifestyle changes and urbanization. Governments in South America have launched initiatives and programs to raise awareness about diabetes management and control the disease burden, which contributes to market growth. However, limited healthcare infrastructure and affordability issues pose challenges to market development.

Manufacturers operating in this region are focusing on providing cost-effective devices and collaborating with local healthcare organizations to overcome these barriers and tap into the market potential in South America. The Middle East & Africa region represents an emerging market for diabetes devices. The prevalence of diabetes is on the rise in this region, prompting governments to launch initiatives and programs focused on diabetes awareness and management. Increasing access to healthcare facilities and growing awareness among the population contribute to the adoption of diabetes devices. However, challenges such as limited access to healthcare facilities in certain areas and affordability issues hinder market growth. Manufacturers are expanding their distribution networks and offering affordable options to cater to the market needs in the Middle East & Africa.

Diabetes Devices Market Segment Analysis

Several parameters can categorise the Diabetes Devices Market, revealing market trends and potential. Product type is a key segmentation, including blood glucose monitoring systems, insulin administration systems, CGM systems, insulin pumps, pens, syringes and other devices. Blood glucose monitoring systems, especially SMBG sensors, dominate the market. Due to their real-time glucose readings and diabetes management insights, CGM systems are rising in popularity. Another important segmentation factor is the end-user category, which includes hospitals, homecare settings, diagnostic centres and other healthcare facilities. The homecare segment is experiencing significant growth as more individuals with diabetes are managing their condition at home. The availability of user-friendly devices and the convenience of self-monitoring and insulin delivery contribute to the increasing demand for diabetes devices in the homecare setting.

The distribution channel is another key segment in the Diabetes Devices Market. Retail pharmacies, online pharmacies, hospital pharmacies and other channels play a crucial role in providing access to diabetes devices. Retail pharmacies hold a substantial market share as they are easily accessible to patients for purchasing diabetes devices and supplies. Online pharmacies have gained popularity due to the convenience of online ordering and home delivery services, providing an additional distribution channel for diabetes devices. Geographic segmentation is important for market analysis.

The Diabetes Devices Market is segmented into North America, Europe, Asia Pacific, South America and the Middle East & Africa. Each region has its own market dynamics, prevalence of diabetes, healthcare infrastructure and regulatory landscape, which influence the adoption and demand for diabetes devices. Market players need to consider these regional variations and tailor their strategies accordingly to effectively target specific geographic markets. Segmentation based on diabetes type is also significant.

The market can be divided into segments for type 1 diabetes and type 2 diabetes. Type 2 diabetes represents a larger market segment due to its higher prevalence globally. However, the market for diabetes devices in type 1 diabetes is also substantial, as individuals with type 1 diabetes require insulin therapy and continuous glucose monitoring for their management. Understanding the specific needs of each diabetes type is crucial for device manufacturers and healthcare providers in developing suitable products and services. Segmenting the market based on age groups provides valuable insights. This includes paediatric, adult and geriatric populations. Each age group may have distinct device requirements and considerations. For instance, paediatric populations may require devices with smaller sizes, colourful designs and user-friendly interfaces to make diabetes management more appealing and manageable for children. Geriatric populations, on the other hand, may benefit from devices with larger buttons, clear displays and simplified operation to accommodate age-related challenges.

Diabetes Devices Market Competitive Landscape

The Diabetes Devices Market is characterized by intense competition among key players striving for market dominance. Medtronic plc, Dexcom, Inc., Abbott Laboratories, F. Hoffmann-La Roche Ltd. and Novo Nordisk A/S are market leaders with global presences. These firms sell blood glucose monitoring, insulin delivery and CGM systems. To stay competitive, companies in the Diabetes Devices Market focus on continuous product innovation. They invest in research and development to introduce technologically advanced and user-friendly devices.

Continuous glucose monitoring systems with improved accuracy and connectivity features have gained popularity in recent years. Product differentiation and technological advancements are key strategies employed by market players to gain a competitive edge. Strategic partnerships and collaborations are common in the Diabetes Devices Market. Companies often form alliances with technology firms, healthcare organizations and research institutions to develop integrated diabetes management solutions. By combining their expertise and resources, companies aim to deliver comprehensive diabetes care solutions and reach a broader customer base. Strategic partnerships enable companies to expand their product portfolios and enhance their market presence. Mergers and acquisitions play a significant role in shaping the competitive landscape of the Diabetes Devices Market. Companies aim to enhance their market position and access new technologies/markets through strategic moves. Mergers and acquisitions expand product offerings, leverage synergies and enhance global reach. These strategic transactions also facilitate economies of scale and drive innovation through shared resources and expertise. With the rising prevalence of diabetes in emerging markets, key players in the Diabetes Devices Market are increasingly focusing on expanding their presence in these regions. They develop cost-effective devices and customized solutions to cater to the specific needs and preferences of these markets. Collaborations with local healthcare organizations and distributors enable better market penetration and distribution network expansion in these regions. Marketing and promotional activities are crucial for companies in the Diabetes Devices Market to create brand awareness and capture a larger market share.

Companies aim to enhance their market position and access new technologies/markets through strategic moves. Mergers and acquisitions expand product offerings, leverage synergies and enhance global reach. These strategic transactions also facilitate economies of scale and drive innovation through shared resources and expertise. With the rising prevalence of diabetes in emerging markets, key players in the Diabetes Devices Market are increasingly focusing on expanding their presence in these regions. They develop cost-effective devices and customized solutions to cater to the specific needs and preferences of these markets. Collaborations with local healthcare organizations and distributors enable better market penetration and distribution network expansion in these regions. Marketing and promotional activities are crucial for companies in the Diabetes Devices Market to create brand awareness and capture a larger market share.

These activities include product advertisements, educational campaigns and collaborations with healthcare professionals and patient advocacy groups. Building strong brand equity and establishing trust among consumers play a vital role in driving market growth. Compliance with regulatory standards and obtaining necessary certifications is essential for companies in the Diabetes Devices Market. Adherence to quality standards and regulatory requirements ensures product safety and effectiveness, enhancing customer trust and confidence in the devices. Companies invest in rigorous testing and certification processes to comply with regional and international regulations.

Diabetes Devices Market Scope: Inquire before buying

| Diabetes Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 28.12 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 6.2% | Market Size in 2029: | US $ 30.34 Bn. |

| Segments Covered: | by Product Type | Blood glucose monitoring systems Insulin delivery systems Continuous glucose monitoring (CGM) systems Insulin pumps Insulin pens Insulin syringes Insulin patches Insulin inhalers |

|

| by End-User | Hospitals Homecare settings Diagnostic centres Ambulatory surgical centres Specialty clinics |

||

| by Distribution Channel | Retail pharmacies Online pharmacies Hospital pharmacies Diabetes clinics Direct sales |

||

| by Diabetes Type | Type 1 diabetes Type 2 diabetes Gestational diabetes |

||

| by Accessories and Consumables | Lancets and test strips Infusion sets and reservoirs Sensors Insulin cartridges and vials Needles |

||

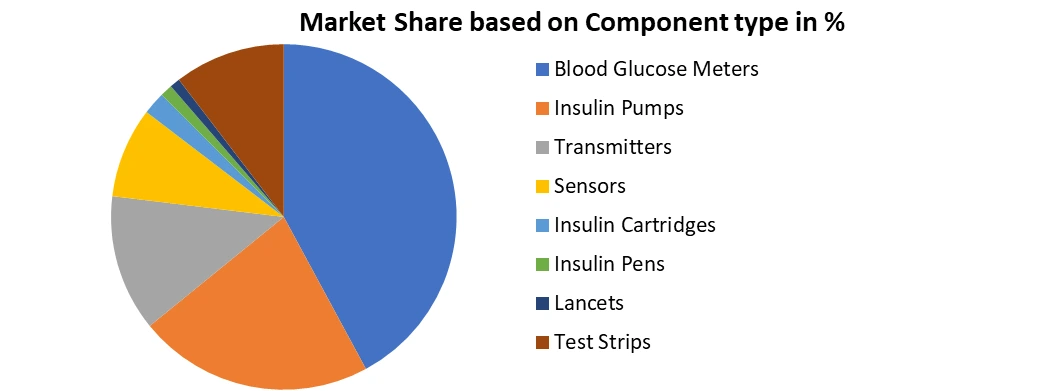

| by Component Type | Blood glucose meters Insulin pumps Transmitters Sensors Insulin cartridges Insulin pens Lancets Test strips |

||

Diabetes Devices Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest)

South America (Brazil, Argetina and Rest of South America)

Company Profile: Diabetes Devices Key players

The captured list of leading manufacturers of Diabetes Devices industry has been compiled after an analysis of multiple factors. It is not an exhaustive list based only on market share ranking. After a regional analysis, a competitive analysis and other such considerations, the company profiles were selected based on a variety of factors. The comprehensive report contains information on the position of each company in the market from a local and global perspective.

North America:

Medtronic plc (United States)

Dexcom, Inc. (United States)

Abbott Laboratories (United States)

Johnson & Johnson (United States)

Insulet Corporation (United States)

Tandem Diabetes Care, Inc. (United States)

Ascensia Diabetes Care Holdings AG (United States)

Roche Diabetes Care, Inc. (United States)

Becton, Dickinson and Company (United States)

Senseonics Holdings, Inc. (United States)

Europe:

F. Hoffmann-La Roche Ltd. (Switzerland)

Novo Nordisk A/S (Denmark)

Siemens Healthineers AG (Germany)

Ypsomed AG (Switzerland)

Medtronic plc (Ireland)

Dexcom, Inc. (United Kingdom)

Abbott Laboratories (United Kingdom)

Terumo Corporation (Switzerland)

B. Braun Melsungen AG (Germany)

Nipro Corporation (Netherlands)

Sanofi (France)

Medtronic plc (Ireland)

Menarini Group (Italy)

Asia Pacific:

Sinocare Inc. (China)

ARKRAY, Inc. (Japan)

MicroPort Scientific Corporation (China)

FAQs

Q: What are the major types of diabetes devices?

A: The major types of diabetes devices include blood glucose monitoring systems, insulin delivery systems such as pumps, pens and syringes and continuous glucose monitoring (CGM) systems.

Q: Are there any technological advancements in diabetes devices?

A: Yes, there have been significant technological advancements in diabetes devices, including improved accuracy in blood glucose meters, integration of CGM systems with insulin pumps and the development of smart insulin pens with digital connectivity.

Q: Who are the key players in the Diabetes Devices Market?

A: Key players in the market include Medtronic plc, Dexcom, Inc., Abbott Laboratories, F. Hoffmann-La Roche Ltd. and Novo Nordisk A/S. These companies are known for their extensive range of diabetes devices and contributions to the market's growth.