Global Delivery Drones Market Size, Growth, Trends and Forecast (2026–2032): Market Segments, Competitive Landscape, Regional Growth and Industry Dynamics

Overview

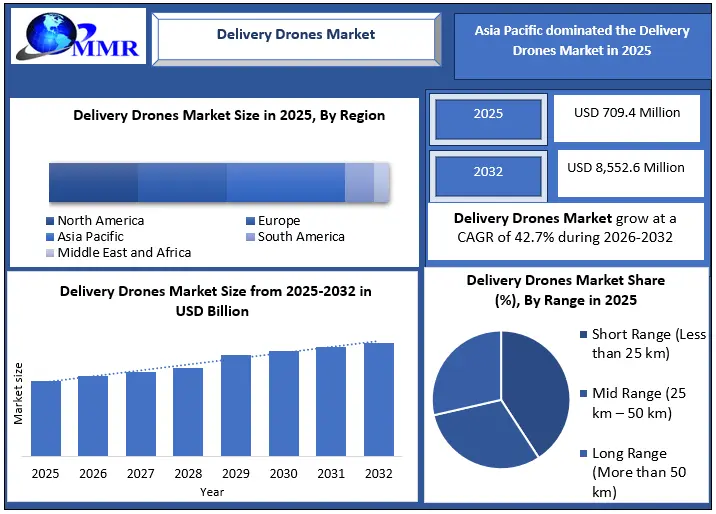

The Global Delivery Drones Market, valued at USD 709.4 Million in 2025, is projected to reach USD 8,552.6 Million by 2032, growing at a CAGR of 42.7% during 2026–2032. Autonomous aerial delivery is no longer limited to pilot programs or regulatory testing—it is steadily becoming part of real-world logistics networks. This growth is being driven by rising last-mile delivery costs, labour shortages in urban logistics, and increasing regulatory approvals such as BVLOS operations. At the same time, improvements in battery performance and autonomous navigation are making drone delivery more practical at scale. What was once seen as an experimental solution is now gradually positioning itself as a viable alternative in specific delivery use cases. In 2025, a drone delivered blood to a trauma patient in Rwanda in 11 minutes. A truck would have taken 3 hours. That single data point tells you everything about where this market is going.

Delivery Drones Market Overview:

Commercial delivery drone deployment has crossed into mass-scale operations, with tens of thousands of active units now generating revenue-grade flight volumes across North America, Europe, and Asia-Pacific. Commercial delivery drones accounted for over 70% of all revenue-generating drone flights globally in 2025, with multirotor platforms dominating short-range urban last-mile delivery while hybrid and fixed-wing systems were deployed for regional logistics and time-critical medical delivery corridors.

Operational expansion is concentrated in regions with regulatory readiness, infrastructure support, and strong logistics demand, enabling a shift from pilot projects to scalable delivery networks.Most markets grow. Few transform. The delivery drones market sits firmly in the second category.

Between 2020 and 2024, the industry was largely a story of pilots, promises, and regulatory friction. What changed in 2025 was the convergence of four forces that rarely align simultaneously — regulatory maturity, unit economics viability, autonomous technology readiness, and mainstream consumer acceptance of aerial delivery.

The result: operators stopped running experiments and started building permanent infrastructure. Hubs. Charging grids. Dedicated airspace corridors. Multi-year retail contracts. The transition from "proof of concept" to "backbone of last-mile logistics" is no longer theoretical — it is underway, and the 42.7% CAGR through 2032 is its numerical signature.

For investors, operators, and logistics strategists, the window to establish position is now. Markets compounding at 42%+ do not stay accessible for long.

Delivery Drones Market Key Highlights:

United States – Largest concentration of FAA-certified drone delivery operators; thousands of daily commercial flights supported by established BVLOS corridors and Drone-as-a-Service models.

China – Dominant global drone manufacturing hub, supplying over 60% of commercial delivery drone hardware worldwide; cost leadership underpins global export competitiveness.

Europe (UK, Germany, France) – Leading BVLOS regulatory pilots and healthcare drone corridors; strong policy framework driving permanent infrastructure investment beyond pilot programs.

Japan & South Korea – Advanced urban drone automation addressing aging-population healthcare logistics; high fleet automation and UTM integration maturity.

Australia & Africa – Highest penetration of rural and remote medical drone delivery; drone networks achieving over 99% delivery success rates in healthcare applications.

The top 5 markets collectively accounted for over 65% of active delivery drone operations in 2025, reflecting strong supply-side concentration in regulatory readiness, infrastructure, and autonomous technology capability.

To know about the Research Methodology :- Request Free Sample Report

Delivery Drones Market Strategic Shift: From Pilot Programs to Scalable Logistics Networks

The Delivery Drones Market is transitioning from isolated pilot deployments to structured logistics infrastructure. Early adoption focused on proof-of-concept operations, while current deployments are centered on scalability, cost efficiency, and integration into existing supply chains.

• Logistics providers are increasingly treating drones as network extensions rather than standalone solutions

• High-frequency, low-weight deliveries are shaping fleet design and operational models

• Regulatory approvals are acting as a key accelerator for commercial expansion

This shift indicates that the market is moving beyond experimentation toward long-term commercial viability.

Delivery Drones Market Dynamics

Shift Toward High-Frequency, Low-Weight Deliveries

In 2025, over 70% of drone-delivered parcels weighed below 3 kg, aligning with food delivery drones, prescriptions, and small e-commerce drone delivery items. Typical payload ranges included:

• Below 2 kg – food delivery, diagnostics, documents

• 2–5 kg groceries, medicines, retail parcels

• Above 5 kg – limited to specialized or hybrid delivery drones

This demand structure favored multirotor and hybrid delivery drones operating within 5–15 km last-mile drone delivery radii.

Delivery Drone Market Strategic Implications: Who Wins, Who Loses, and Why

The Delivery Drones Market does not reward passive participation. Three distinct competitive outcomes are emerging:

Winners — Platform Integrators: Companies that own the full stack — drone hardware, autonomous software, fleet management, and logistics partnerships — are building moats that pure hardware or pure software players cannot replicate. Wing (Alphabet), Zipline, and Amazon Prime Air exemplify this model. Their advantage is not the drone; it is the data generated across millions of flights that continuously improves route efficiency, failure prediction, and regulatory compliance documentation.

Survivors — Specialist Verticals: Players focused on defensible niches — medical delivery in underserved geographies, agricultural drone logistics, government emergency response — can sustain without platform scale. Their protection is mission-criticality, not volume.

Losers — Hardware Commoditisers: Drone manufacturers competing solely on unit price face an accelerating margin compression cycle, particularly as Chinese OEM supply continues to drive down global hardware costs. Without software differentiation or service revenue, hardware-only positioning is structurally disadvantaged.

The market's 42.7% CAGR masks this internal divergence. The aggregate number looks attractive. The distribution of returns will not be uniform.

Technology-Driven Productivity Improvements

Autonomous delivery drone systems increasingly relied on automation and AI to improve drone logistics efficiency:

• AI route optimization improved delivery efficiency by 20–35%

• Automated landing and charging systems reduced turnaround time by 30–40%

• Hybrid delivery drones increased range by 30–50% compared to multirotor drones

• Drone traffic management (UTM) systems managed 100+ simultaneous drones per urban airspace

Battery technology improvements extended average delivery drone flight endurance to 30–40 minutes, enabling higher drone fleet utilization per asset.

Regulatory Enablement and Network Scaling

Regulatory support remained a critical enabler of delivery drones market growth:

• BVLOS drone approvals enabled continuous operations without visual observers

• Remote ID systems enabled real-time tracking of 100% registered delivery drones

• FAA-certified drone corridors supported thousands of weekly commercial drone delivery flights

• Standardized drone approvals reduced deployment timelines by 6–12 months

As a result, operators transitioned from pilot programs to permanent drone delivery infrastructure, including fixed hubs, charging stations, and designated landing zones.

Cost and Operational Economics

• Per-delivery operating cost reduction vs ground delivery: 40–60%

• Fuel costs eliminated for short-range UAV delivery routes

• Maintenance cost per delivery drone is lower than that of motor vehicles

• Drone fleet utilization rates improved due to automation

Drone-as-a-Service (DaaS) models expanded rapidly, enabling enterprises to access drone delivery services without upfront capital investment.

Operational Capacity & Flight Volumes

• Average delivery drones per operational hub: 20–50 units

• Average flights per drone per day: 10–25

• Monthly delivery volume per drone delivery network: 20,000–50,000 parcels

• Annual deliveries by leading drone delivery operators: hundreds of thousands to millions

• Healthcare drone delivery networks achieved >99% delivery success rates

Centralised drone fleet-control platforms enabled one operator to oversee 10–20 autonomous delivery drones, significantly improving delivery drone scalability.

Delivery Drones Market Demand Analysis

Demand for delivery drone services is being driven by structural shifts in consumer expectations and logistics economics, with several high-impact forces converging to accelerate commercial adoption across urban, suburban, and remote geographies.

• Increasing demand for same-day and sub-1-hour deliveries

• Urban congestion impacting delivery efficiency

• Labour shortages in logistics operations

• Growth in e-commerce and on-demand delivery services

• Expansion of healthcare logistics for critical supplies

Healthcare remains one of the most stable and high-impact segments, where delivery times are reduced from 60–120 minutes (road) to 10–20 minutes via drones, particularly in emergency and remote-area use cases.

Broad-based demand growth projections can obscure where the real conviction lies. Three segments stand out as structurally high-conviction growth pockets through 2032:

Sub-3kg Urban Last-Mile (Food + Pharma): Over 70% of 2025 drone deliveries fell in this weight class. The economics are proven. Consumer acceptance is established. Infrastructure investment is accelerating. This segment alone justifies the market's base case growth trajectory.

Emergency and Critical Healthcare Logistics: Delivery time reduction from 60–120 minutes by road to 10–20 minutes by drone is not a convenience upgrade — it is a clinical outcome differentiator. Governments and healthcare systems are increasingly treating drone delivery as public health infrastructure, not logistics innovation, which means procurement is shifting toward long-term contracts and budget line items rather than pilot funding.

Rural and Remote Market Access: In markets where road infrastructure is inadequate — Sub-Saharan Africa, Southeast Asian archipelagos, rural India — drones are not competing with ground delivery. They are replacing the absence of delivery entirely. This is a structurally uncaptured demand pool with minimal competitive pressure and strong development-finance tailwinds.

Key Operational and Regulatory Constraints Facing the Delivery Drones Market

• Regulation: Drone airspace management, safety standards, and BVLOS certification frameworks continued to evolve

• Privacy Concerns: Use of cameras and sensors in autonomous drone delivery systems raised privacy concerns

• Weather Limitations: Wind, rain, and snow affected delivery drone performance

• Cost of Infrastructure: Drone hubs, charging stations, and UTM integration required a high upfront investment

Regulatory Analysis:

Regulatory developments such as BVLOS approvals, Remote ID implementation, and dedicated drone corridors are directly accelerating market growth by enabling continuous operations and large-scale deployment. These frameworks reduce operational constraints, shorten deployment timelines, and improve commercial viability, making regulation a key driver rather than a barrier.

What the Delivery Drones Market Data Doesn't Say — But Should

Three structural realities about the delivery drones market are systematically underrepresented in mainstream analysis:

1. Regulation is not the bottleneck anymore — operations are. The narrative around drone market constraints has centred on regulatory friction for years. That story is largely outdated. BVLOS approvals are expanding. FAA corridors are operational. The real constraint in 2025–2026 is operational — building drone hubs, integrating UTM systems, and training fleet operators at the speed that regulatory approvals now permit. Companies that invested in operational infrastructure during the "waiting for regulation" phase are now compounding that advantage rapidly.

2. Healthcare is the market's most durable growth engine — not e-commerce. E-commerce drone delivery generates headlines. Healthcare drone delivery generates defensible, recurring, government-contracted revenue. Blood delivery, vaccine distribution, diagnostic sample transport — these use cases operate independently of consumer sentiment cycles, competitive pricing pressure, or last-mile economics debates. Zipline's 2 million delivery milestone was not built on pizza and parcels.

3. The real monetisation shift is from hardware to data. A delivery drone that flies 15 routes per day generates location data, weather performance data, airspace conflict data, and package integrity data — all of which are increasingly valuable to insurers, logistics planners, urban mobility designers, and regulators. The companies that monetise this data layer alongside delivery fees will generate revenue structures that pure logistics operators cannot match.

Delivery Drones Market Segment Analysis

Rotary-Wing Drones (Multi-Rotor)

Multi-rotor delivery drones accounted for 60–70% of the delivery drones market in 2025, driven by their maneuverability, VTOL capability, and suitability for dense urban environments. Fixed-Wing Drones and Hybrid Wing Drones segment writeups are missing. Both are listed in the segmentation table but have no corresponding analysis. Must be added before client delivery.

Reasons for Dominance:

• Urban Focus: Ideal for dense urban and suburban drone logistics operations

• Precision Delivery: Hovering capability enabled accurate delivery of food, parcels, and medical supplies

• Regulatory Advantage: Multi-rotor drones received more BVLOS regulatory approvals than fixed-wing platforms

Delivery Drones Market Regional Analysis

Asia-Pacific emerged as the largest and fastest-deploying delivery drones market in 2025, accounting for over 40% of active commercial drone deployments globally. Growth was driven by China, Japan, South Korea, India, and Southeast Asia, supported by dense urban populations, strong e-commerce drone delivery adoption, and government-backed drone corridors.

China dominated delivery drone manufacturing, supplying more than 60% of global commercial delivery drones, while Japan and South Korea led in urban drone automation, medical delivery drones, and aging-population healthcare logistics. India and Southeast Asia witnessed rapid expansion in food delivery drones, last-mile e-commerce drone delivery, and pilot-scale healthcare drone networks, supported by regulatory sandbox programs and rising private investment.

North America represented the most regulatory-mature delivery drones market in 2025, anchored by the United States' FAA-certified operator network and established commercial drone corridors. The region is characterised by high-frequency retail and food delivery drone operations, with Walmart-Wing and Amazon Prime Air scaling rapidly. Canada and Mexico represent emerging growth markets with nascent regulatory frameworks and growing investment in healthcare and rural drone logistics.

Europe demonstrated structured, compliance-led drone market growth in 2025, with the UK, Germany, and France leading BVLOS regulatory pilots and dedicated healthcare drone corridor development. The EU's U-Space framework is progressively enabling large-scale commercial drone operations, with permanent drone delivery infrastructure replacing earlier pilot-phase deployments across major urban centres.

MEA and South America regional narrative writeups are absent — must be added to align with TOC and scope table commitments.

Recent Development Delivery Drones Market

2026 – Walmart announced the expansion of its drone delivery partnership with Wing (Alphabet Inc.), adding 150 new store locations in 2026, with coverage projected to exceed 270 locations by 2027 — enabling rapid last-mile drone delivery across major U.S. metropolitan areas.

Early 2026 – Zipline International confirmed plans to extend medical and commercial drone delivery services into Houston and Phoenix. Having surpassed 2 million cumulative global deliveries and closed a USD 600 million funding round, Zipline is actively scaling partnerships across healthcare, logistics, and retail drone delivery ecosystems.

Delivery Drones Market Scope: Inquire before buying

| Delivery Drones Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 709.4 Mn. |

| Forecast Period 2026 to 2032 CAGR: | 42.7% | Market Size in 2032: | USD 8,552.6 Mn. |

| Segments Covered: | by Drone Type | Rotary-Wing Drones (Multi-Rotor) Fixed-Wing Drones Hybrid Wing Drones |

|

| by Payload Capacity | Below 2 kg 2 kg to 5 kg Above 5 kg / More than 10 kg |

||

| by Range | Short Range (Less than 25 km) Mid Range (25 km – 50 km) Long Range (More than 50 km) |

||

| by Component Type | Hardware Software Services |

||

| by Operation Mode | Remotely Piloted Partially Autonomous Fully Autonomous |

||

| by Duration | Less than 30 Minutes More than 30 Minutes |

||

| by End-User | Retail & E-commerce Companies Healthcare Providers & Hospitals Logistics & Transportation Companies Restaurants & Food Service Chains Government & Public Sector Agricultural Operations |

||

Delivery Drones Market Key Players

The most underappreciated competitive dynamic in this market is the role of the logistics incumbents — FedEx, UPS, and DHL — who are simultaneously the industry's largest potential customers and its most significant strategic threat. Their capital, regulatory relationships, and existing delivery networks give them the option to acquire drone capability rather than build it. How aggressively they exercise that option between 2026 and 2028 will be a primary determinant of whether pure-play drone operators achieve independent scale or become acquisition targets.

1. Wing Aviation LLC (Alphabet Inc.)

2. Zipline International Inc.

3. Flytrex Inc.

4. United Parcel Service of America, Inc. (UPS Flight Forward)

5. Prime Air (Amazon.com, Inc.)

6. FedEx Corporation (retain with qualifier — emerging drone logistics)

7. Wingcopter GmbH

8. Guangzhou EHang Intelligent Technology Co. Ltd. (retain — cargo UAV division)

9. Drone Delivery Canada Corp.

10. Matternet, Inc.

11. Kite Aero

12. Manna Drone Delivery

13. Skyports Drone Services

14. Speedbird Aero

15. Rakuten Group, Inc.

16. JD Logistics / JD.com

17. DroneUp, LLC

18. Volansi (Volans-i)

19. SkyDrop (formerly Flirtey)

20. Swoop Aero

21. Dronamic

22. Astral Aerial Solution Inteliports Limited

23. Drone Delivery Services (multiple integrators)

24. Uber Eats (drone partners)

25. Garuda Aerospace Pvt Ltd.

26. Skycatch, Inc.

27. Verity Studios AG

28. Asteria Aerospace Ltd.

29. FLI Drone / FLIROnline

Frequently Asked Questions

1. What is the size of the Delivery Drones market?

Ans: The global Delivery Drones market was valued at USD 709.4 million in 2025 and is projected to reach USD 8,552.6 million by 2032, growing at a CAGR of 42.7%. This rapid growth is driven by the expansion of last-mile delivery, healthcare logistics, and e-commerce automation.

2. What are the key applications of Delivery Drones?

Ans: Delivery drones are widely used in food delivery, e-commerce parcels, medical and pharmaceutical logistics, blood and vaccine delivery, emergency response, and rural logistics, offering faster, contactless, and cost-efficient delivery solutions.

3. What are the main types of delivery drones used commercially?

Ans: Key delivery drone types include multi-rotor drones, fixed-wing drones, and hybrid VTOL drones, each optimised for different payload capacities, delivery ranges, and urban or regional deployment requirements.

4. What are the benefits of using Delivery Drones?

Ans: Delivery drones enable 40–60% lower delivery costs, faster delivery times, reduced urban congestion, zero fuel consumption for short routes, and high delivery success rates, especially in time-critical healthcare and remote-area deliveries.

5. What is driving the growth of the Delivery Drones market?

Ans: Market growth is driven by rising same-day delivery demand, labour shortages in last-mile logistics, regulatory approvals for BVLOS operations, advances in AI and battery technology, and increasing adoption in healthcare and e-commerce sectors.

MMR Analyst View — The One Paragraph Every Decision-Maker Should Read

The delivery drones market is at the exact stage the ride-sharing market was in 2013 — the technology works, early operators have proven the model, and the regulatory foundation is solidifying. What follows historically in markets at this stage is a rapid scaling phase where the gap between early movers and late entrants becomes structurally irreversible. The 42.7% CAGR through 2032 is not an outlier projection — it reflects a market catching up to infrastructure and regulatory readiness that has been building for a decade. The risks are real: weather constraints, airspace complexity, privacy backlash, and infrastructure capital intensity are not trivial. But the directional conviction is unusually high for a market of this size. For operators, the question is no longer "will drone delivery scale?" — it is "at what cost does the window close if we wait?"