Defibrillators Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

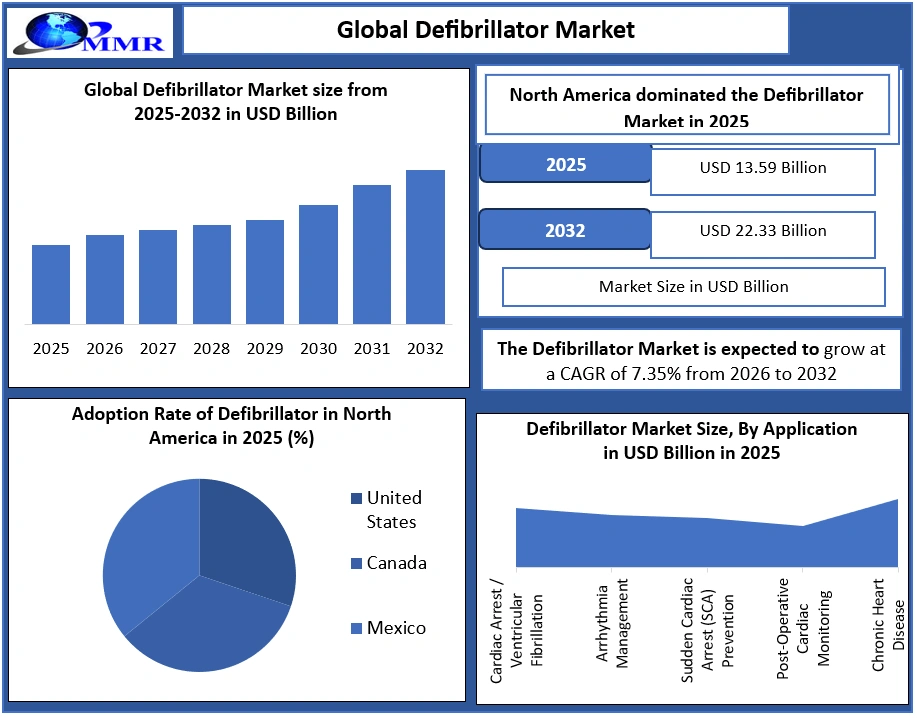

The Global Defibrillator Market Size was valued at USD 13.59 Billion in 2025, and the total revenue is expected to grow at a CAGR of 7.35% from 2026 to 2032, reaching USD 22.33 Billion by 2032

Key Highlights:

• High Initial Investment: Implantable Cardioverter Defibrillator range from USD 30,000 to USD 50,000, while Automated External Defibrillator cost USD 1,200 to USD 2,500. Despite the high upfront cost, these devices are cost-effective long-term, improving survival rates for out-of-hospital cardiac arrest (OHCA) patients.

To Know About The Research Methodology :- Request Free Sample Report

• Increased Efficiency: Innovations in AEDs and ICDs, like automated shock delivery and real-time monitoring, enhance response times. Survival rates can reach 50-70% if CPR is started within 1 minute and defibrillation within 3-5 minutes.

• Precision and Sensitivity: ICDs offer over 95% sensitivity in detecting life-threatening arrhythmias like ventricular fibrillation and tachycardia.

• Wide Clinical Adoption: Over 83,000 AEDs are deployed in public spaces across China, with 200,000 AEDs in the U.S. AEDs are increasingly used in high-traffic areas such as airports and schools.

• Versatility Across Applications: AEDs and ICDs are widely used in public spaces, hospitals, and home healthcare, significantly improving survival chances in sudden cardiac arrest (SCA) situations.

Defibrillator Market Dynamics:

Defibrillator Market Demand Driver

• Urgent Need for Defibrillators: The 19.8 million annual deaths create an urgent and persistent need for defibrillators in healthcare settings.

• Life-Saving Equipment: Defibrillators play a critical role in cardiac emergency and immediate intervention for sudden cardiac arrest (SCA).

Geographic and Demographic Disparities

• CVD Deaths in LMICs: Over 75% of CVD-related deaths occur in Low- and Middle-Income Countries (LMICs), highlighting a geographic mismatch between the need for defibrillators and the availability of advanced medical resources.

• Premature Mortality: 18 million premature deaths from noncommunicable diseases (NCDs) in 2021, 38% were caused by CVDs, with many affecting individuals under the age of 70.

• Economic Loss: Premature CVD mortality represents significant societal and economic loss due to loss of productivity and caregiving costs.

Market Growth: Public Access Defibrillation (PAD)

• Shifting Market Focus: The defibrillator market is expanding beyond clinical settings into public access locations, driving demand for AEDs.

• Impact on Market: Prevention directly influences the defibrillator market's evolution, steering R&D towards solutions that not only respond to emergencies but also support early detection and chronic disease management.

Critical Role of Early Detection and Intervention

• Timely Detection: Early identification of CVD allows for life-saving management through:

o Counselling

o Medication/therapy

• The defibrillator market is increasingly focused on integrated solutions that combine early detection, chronic disease management, and emergency response.

• Cardiovascular diseases (CVDs) remain a leading cause of mortality globally. The prevalence of heart disease, particularly linked to obesity, hypertension, and diabetes, drives a significant portion of the defibrillator market. With CVD risk factors increasing, especially in regions with rising obesity rates (e.g., North America, the Middle East, and parts of Latin America), the demand for defibrillators such as Automated External Defibrillators (AEDs) and Implantable Cardioverter Defibrillators (ICDs) has escalated.

Role of Defibrillators in Cardiac Emergencies:

• Automated External Defibrillators (AEDs) are crucial for saving lives in cases of sudden cardiac arrest (SCA), which is often caused by arrhythmias like ventricular fibrillation (VF). In the defibrillator market, public access AEDs are increasingly being deployed in public spaces such as schools, airports, and gyms, where people with underlying heart conditions (including those with high BMI) may experience cardiac arrest.

• Implantable Cardioverter Defibrillators (ICDs) are vital for high-risk patients, particularly those with heart failure, arrhythmias, or previous cardiac events, who are at risk for SCA. As the prevalence of heart disease and arrhythmias grows, the demand for ICDs in the defibrillator industry is also expected to rise significantly.

Defibrillators and Aging Populations:

• The global aging population contributes to an increase in cardiovascular diseases. As individuals age, the risk of heart attacks, arrhythmias, and sudden cardiac arrest rises. For example, ICDs are commonly recommended for patients at risk of life-threatening arrhythmias due to age-related cardiac conditions. This demographic shift is driving further growth in the defibrillator market, with ICD devices playing a crucial role in managing age-related heart failure and preventing SCA.

Defibrillator Market Segment Analysis:

By Product :

Implantable Cardioverter Defibrillators (ICD): The ICD segment held a dominant position in the defibrillator market in 2025 due to its critical role in treating patients at high risk for arrhythmias or sudden cardiac arrest (SCA). T-ICD (Transvenous ICD) led the market with a larger share, thanks to its extensive use in managing severe heart conditions. However, S-ICD (Subcutaneous ICD) gained ground in 2025 due to its less invasive nature, making it a favourable option for patients requiring defibrillation but with fewer procedural risks.

Recent Development:

June 2024: Stryker unveiled the LIFEPAK 35 Monitor/Defibrillator, an advanced solution with intuitive features designed to support improved emergency care workflows.

• April 2024: MicroPort Scientific Corporation (China) declared the European debut of its TALENTIA and ENERGYA series Bluetooth enabled ICDs and CRT D devices designed to enhance connectivity and remote diagnostics.

Defibrillators Market Scope: Inquire before buying

| Global Defibrillators Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 11.17 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 8.7% | Market Size in 2032: | US $ 20.03 Bn. |

| Segments Covered: | by Product | Implantable Cardioverter Defibrillators (ICD) S-ICD T-ICD External Defibrillators (ED) Manual ED Automated ED Wearable Cardioverter Defibrillators |

|

| by Application | Cardiac Arrest / Ventricular Fibrillation Arrhythmia Management Sudden Cardiac Arrest (SCA) Prevention Post‑Operative Cardiac Monitoring Chronic Heart Disease Management |

||

| by End User | Hospitals & Clinics Ambulatory Surgical Centers Diagnostic Centers Public Access Sites Home Healthcare Emergency Medical Services (EMS) |

||

Defibrillators Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Defibrillator Market, Key Players:

1. Medtronic PLC

2. Stryker Corporation (Physio-Control)

3. Boston Scientific Corporation

4. Abbott Laboratories

5. Koninklijke Philips N.V.

6. Nihon Kohden Corporation

7. ZOLL Medical Corporation (Asahi Kasei Group)

8. Mindray Medical International Limited

9. Biotronik SE & Co. KG

10. Schiller AG

11. HeartSine Technologies is a subsidiary of Stryker Corporation.)

12. CU Medical Systems, Inc.

13. Mediana Co., Ltd.

14. BPL Medical Technologies

15. Progetti S.r.l.

16. Avive Solutions, Inc.

17. MicroPort Scientific Corporation

18. Kestra Medical Technologies, Inc.

19. Bexen Cardio

20. Others

FAQ

1. What are the growth drivers for the Defibrillator Market?

Answer: Rising cardiovascular diseases, increasing cases of sudden cardiac arrest (SCA), growing healthcare infrastructure, and technological advancements.

2. What are the major restraints for the Defibrillator Market growth?

Answer: High costs of devices, maintenance, need for specialised training, and regulatory challenges, particularly in emerging markets.

3. Which region is expected to lead the global Defibrillator Market during the forecast period?

Answer: North America, due to advanced healthcare infrastructure, high adoption rates, and strong market players.

4. What is the projected market size and growth rate of the Defibrillator Market?

Answer: Valued at USD 13.59 Billion in 2025, projected to grow at a CAGR of 7.35%, reaching USD 22.33 billion by 2032.