Defense Electronics Market Size by Segments, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

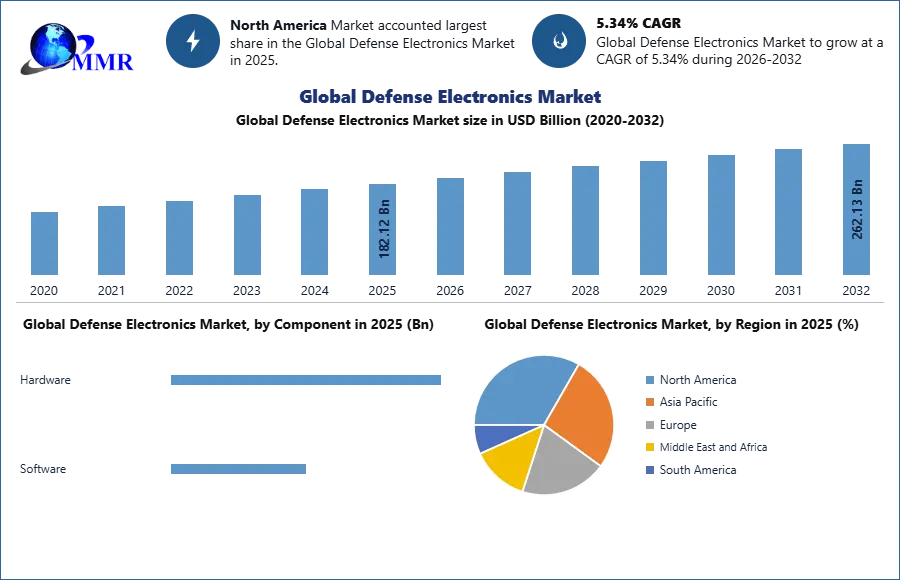

Defense Electronics Market size was valued at USD 182.12 Bn. in 2025 and the total revenue is expected to grow at a CAGR of 5.34 % from 2026 to 2032, reaching nearly USD 262.13 Bn.

Defense Electronics Market Overview

Defense Electronics refers to electronic components and systems designed for technological superiority in national defense. As per the research, the market has experienced significant growth due to several factors such as the increasing advancements in communication systems that offer improved data transmission, encryption, and anti-jamming capabilities. In the Defense Electronics Industry, Lockheed Martin Corporation is one of the largest players. The Defense Electronics Market report includes a detailed analysis of the market size, share with the region-wise and segment-wise market dynamics including growth drivers, major restraints, new opportunities and upcoming challenges. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Defense Electronics Market Dynamics

Increasing Defense Budgets across the World

The allocation of funds to defense spending impacts directly the development of defense electronics technologies. Building and maintaining national security requires large budgets. Governments are increasingly investing in research and development related to defense electronics, which has enabled the exploration of new technologies, innovative solutions and cutting-edge capabilities. These are developing the defense electronics sector by including the acquisition of sophisticated radar systems, unmanned platforms, communication networks, cybersecurity solutions and electronic warfare equipment. Cyber threats are continuously evolving for which defense budgets are playing an important role in financing cybersecurity initiatives. In the past few years, higher defense spending has fostered a healthy and dynamic defense electronics market by attracting investments, encouraging innovation and supporting skilled workforce development.

Increasing Artificial Intelligence (AI) Investment Activities

Militaries across the world are increasingly treating AI as a technology that is central to their long-term strategies and planning. One of the most significant paths of integration of emerging technologies such as AI-enabled technology into defense systems and platforms is through the largest defense companies. With tech giants like Amazon and Google at the forefront of AI innovation, major defense companies are pressed to step up their innovation-related activities to keep pace with the larger commercial market. The AI investment activities in the defense electronics market typically focus on autonomous systems, cybersecurity, data analysis and intelligence, training and simulation, predictive maintenance and communication and networking.

AI's role in cybersecurity is important as it helps identify and counter cyber threats, detect anomalies and protect defense infrastructure from attacks.AI algorithms efficiently analyze massive amounts of data to extract valuable insights, helping defense agencies make informed decisions and anticipate potential threats. These are the main factors due to which the demand for AI in the defense electronics sector is increasing resulting to an increase in AI investment activities.

China and Russia are making significant investments in AI for national security purposes while the Department of Defense (DOD) is investing billions of dollars to develop and integrate AI into defense systems. In recent years, DOD increased investments, reflecting the growing importance of AI. For example, the latest budget request included USD 130.1 billion for R&D in recognition of the need to sharpen readiness in advanced technology including artificial intelligence.

Effects of Geopolitical Uncertainties on the Defense Electronics Industry

Geopolitical uncertainties directly affect defense spending, international trade and technology transfer. They strain international collaboration defense projects. Diverging national interests and concerns over the sharing of technology creates various challenges for multinational defense initiatives. The trade disputes and political sanctions can disrupt the global supply chain for defense electronics components and materials. The reliance on suppliers that are involved in geopolitical conflicts leads to potential supply shortages and higher shortages.

Defense Electronics Market Regional Insights

North America leads the defense electronics market due to its substantial defense spending, advanced technological base, and robust industrial capabilities. The region's dominance is supported by strategic investments in research and development, ensuring that its defense systems remain operationally effective and technologically advanced. This leadership is crucial in maintaining global stability and protecting national security interests amid increasing geopolitical complexities. The focus on innovative obsolescence management strategies further strengthens North America's position in the market. Defense contractors, IT companies, and academic institutions can form strategic alliances to further speed up innovation and create state-of-the-art defense electronics solutions. These partnerships frequently provide cutting-edge goods that are suited to certain defense requirements.

During the forecast period, Asia Pacific is expected to grow at the fast rate in the global defense electronics market. Because this region has invested in the development of modern technologies and the procurement of new platforms, the Asia Pacific region provides significant opportunities for defense electronics manufacturers. Asian businesses are putting a high priority on and investigating cutting edge technologies, such as big data, robots, digital ledger technologies, artificial intelligence, machine learning, and cryptography. These technologies have the power to completely transform society and the global economy. The epidemic showed how quickly technology is developing.

Europe has a diverse Defense Electronics Market with contributions from both established defense companies and innovative startups. The proliferation of commercial drones has raised security concerns, which has led to the development of counter-unmanned aerial vehicle (UAV) systems in the regional market. The counties in the region are highly investing in electronic warfare systems, including electronic countermeasures and electronic attack technologies.

Defense Electronics Market Segment Analysis

Based on Vertical, the market is divided into Navigation, Communication, Display, C4ISR, Electronic Warfare, Radar and Optronics. The Communication segment held the largest Defense Electronics Market share in 2025. This is because communication systems are essential for facilitating real-time information exchange between military personnel and units, which includes radio communication, satellite communication, and secure data networks. The Radar segment is expected to grow rapidly during the forecast period. The segment also held a major share of the global market as it is crucial for raising awareness about the situation and self-defense.

Based on Component, the defense electronics market is segmented into hardware and software. The hardware segment marks highest market share in 2025. The hardware segment includes various equipment & systems that are important to the development & operation of electrical defense. In addition, the Electronic Warfare (EW) used for defense, electronic surveillance, and electronic evaluation includes hardware such as electronic warfare receivers, jammers, Radar Warning Receivers (RWR), and Electromagnetic Radiation Monitoring (ESM). These hardware components facilitate the development of advanced defense systems and enable capabilities, such as communications, surveillance, detection, routing, and control that are respected in national defense operations. Furthermore, with the increasing reliance on communications and communication security systems, cyber security has become a major concern. The hardware system is propelled by the need for hardware security and strong encryption systems that protect systems from cyber threats and ensure data integrity.

Defense Electronics Market Competitive Landscape

This section of the report provides a detailed analysis of the defense electronics key competitors and information provided by the competitors. The investments by key competitors in research and development with their revenue, sales, production capacities and company overview are all included in the report. SWOT analysis was used to provide the strengths and weaknesses of the key players in the defense electronics industry.

Defense Electronics Market Recent Developments:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 11 March 2026 | Thales Group | Thales officially launched SkyDefender, an AI-powered integrated air and missile defense dome designed to neutralize threats from drones to hypersonic missiles. | The system utilizes the cortAIx AI accelerator to enhance cybersecurity and situational awareness across land, sea, and space domains. |

| 04 February 2026 | Raytheon (RTX) | The company entered into five landmark framework agreements with the U.S. Department of War to triple the annual production of Tomahawk, AMRAAM, and SM-6 munitions. | This multi-year strategic partnership secures the long-term supply of advanced guidance and electronic protection systems for global defense forces. |

| 02 February 2026 | Lockheed Martin | Lockheed Martin and Fujitsu Limited signed a Memorandum of Understanding (MOU) to jointly accelerate dual-use technology development in critical defense sectors. | The collaboration focuses on leveraging 5G.MIL® unified networks and AI/ML to increase connectivity and interoperability in the defense ecosystem. |

| 27 January 2026 | Northrop Grumman | Northrop Grumman reported a 10% growth in its Mission Systems business, driven by the ramp-up of restricted airborne radar programs and F-35 electronics. | This performance underscores the company's leading role in the Joint All-Domain Command and Control (JADC2) market through advanced space-to-ground integration. |

| 19 December 2025 | Space Development Agency (SDA) | The SDA awarded a $764 million contract to Northrop Grumman to build and operate 18 satellites for the Tranche 3 Tracking Layer of the PWSA. | This development advances the Proliferated Warfighter Space Architecture, providing global missile warning and tracking capabilities for contested domains. |

| 13 October 2025 | Anduril Industries | Anduril launched EagleEye, a suite of AI-powered vision products for soldiers that integrate augmented reality into tactical helmets and visors. | The system streamlines real-time decision-making by overlaying critical battlefield data, representing a leap in tactical military electronics. |

Defense Electronics Industry Ecosystem

Defense Electronics Market Scope: Inquire before buying

| Global Defense Electronics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 182.12 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.34% | Market Size in 2032: | 262.13 USD Billion |

| Segments Covered: | by Component | Hardware Software |

|

| by System | Airborne Marine Land Space |

||

| by Technology | Artificial Intelligence (AI) Cybersecurity Systems Advanced Radar Technologies Signal Intelligence Systems Communication Encryption Technologies |

||

Defense Electronics Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Defense Electronics Key Players

1. Lockheed Martin Corporation

2. Northrop Grumman Corporation

3. RTX Corporation (Raytheon Technologies)

4. Thales Group

5. BAE Systems plc

6. General Dynamics Corporation

7. Saab AB

8. L3Harris Technologies Inc.

9. Leonardo S.p.A.

10. Rheinmetall AG

11. Elbit Systems Ltd.

12. Hensoldt AG

13. Hanwha Aerospace

14. Mitsubishi Electric Corporation

15. Indra Sistemas S.A.

16. Israel Aerospace Industries Ltd.

17. Rafael Advanced Defense Systems Ltd.

18. CACI International Inc.

19. QinetiQ Group plc

20. ASELSAN A.S.

21. Bharat Electronics Limited

22. Curtiss-Wright Corporatio

23. Honeywell International Inc

24. Safran S.A.

25. Teledyne Technologies Incorporated

26. Kongsberg Gruppen ASA

27. Cobham Limited

28. Ultra Electronics Holdings plc

29. Kratos Defense & Security Solutions Inc.

30. Mercury Systems Inc.

Others