Global Data Warehousing Market Size, Share & Forecast 2026–2032 | Cloud, Hybrid, Enterprise Analytics & AI Growth

Overview

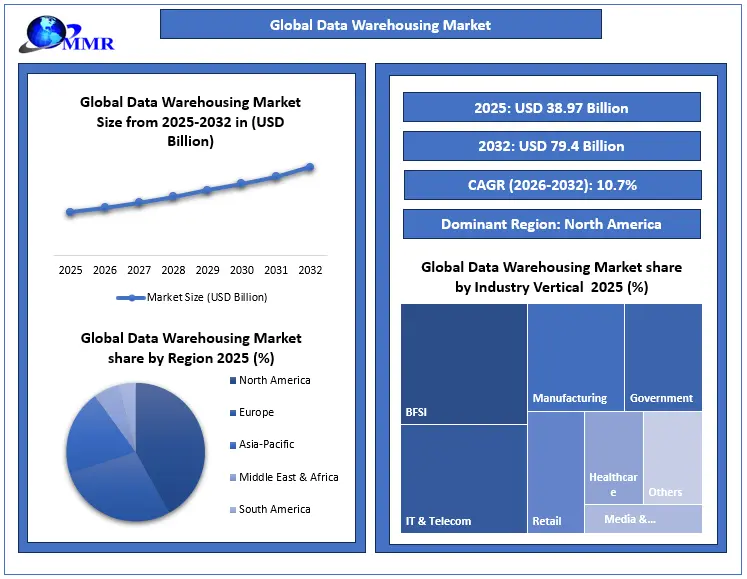

The Global Data Warehousing Market was valued at USD 38.97 billion in 2025 and is expected to reach USD 78.1 billion by 2032, expanding at a CAGR of 10.7% during the forecast period, driven by cloud adoption, enterprise analytics, and AI-driven insights.

Global Data Warehousing Market Overview:

Data warehousing is a centralized system designed to store, manage, and analyze enterprise data for reporting, analytics, and strategic decision-making. It enables organizations to integrate structured and unstructured data, supporting real-time insights and advanced business intelligence.

Growth is driven by real-time business intelligence and customer analytics, cloud-based and hybrid architectures, AI-powered self-service solutions, and automated ETL. Challenges include data security and compliance in multi-cloud environments. North America leads adoption, Europe shows strong cloud growth, and Asia-Pacific accelerates digitalization, shaping the Global Data Warehousing Market.

Data Warehousing Market Key Highlights:

- Cloud Adoption: In 2025, 52.74% of European enterprises utilized paid cloud services, reflecting accelerated migration from on-premise systems to flexible cloud-based data warehousing.

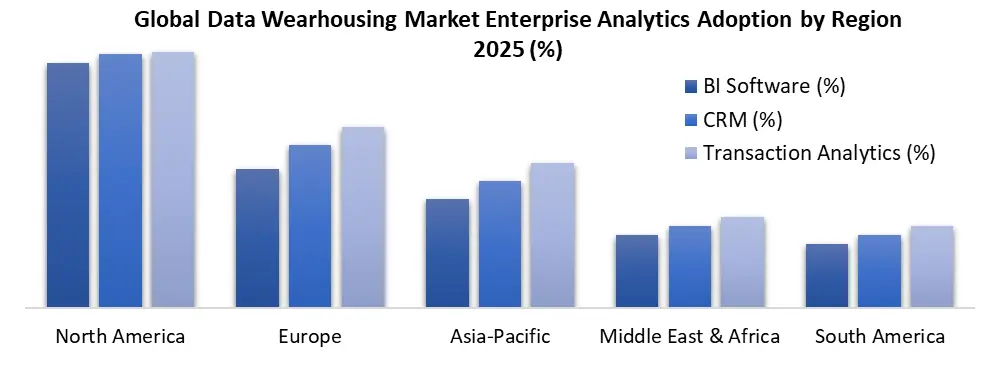

- Enterprise Analytics Penetration: 27% of enterprises used Business Intelligence software, 28% deployed CRM systems, and 28.2% analyzed transaction records in 2025, strengthening real-time analytics capabilities.

- AI Integration: EU AI adoption rose to 20% in 2025 from 8% in 2023, with 10.8% using AI for data mining and 9.3% for natural language generation.

- Cloud Deployment: Cloud adoption in North America reached 45%, with sector leaders in information industries 77% and utilities 72%, highlighting strong digital infrastructure intensity.

- Hybrid & Multi-Cloud Strategies:7% of large enterprises maintain hybrid deployments combining ERP and cloud services, supporting scalable, low-latency enterprise data warehousing solutions.

Dominating Region: North America leads the Data Warehousing Market with advanced enterprise analytics adoption, large-scale cloud infrastructure, and widespread integration of AI-enabled and real-time analytics platforms.

To know about the Research Methodology :- Request Free Sample Report

Trends-Shift Toward Cloud-Based Data Warehousing Adoption

The Data Warehousing Market is witnessing structural acceleration in cloud-based infrastructure adoption across enterprise environments. In 2025, 52.74% of enterprises across the European region utilized paid cloud services, indicating sustained digital transformation momentum. In North America, 45% of businesses leveraged cloud computing, with particularly high penetration in information industries 77% and utilities 72%. This reflects a decisive shift toward cloud-native data warehousing, elastic storage frameworks, distributed processing engines, and enterprise-grade analytics ecosystems.

• Transition from capital-intensive on-premise data warehouse models to operational expenditure-based cloud architectures

• Increased demand for scalable compute, real-time query processing, and managed database services

• Acceleration of hybrid and multi-cloud enterprise strategies

• Strengthening foundation for AI-enabled analytics and advanced business intelligence workloads

Drivers-Rising Demand for Real-Time Business Intelligence & Customer Analytics

Rising demand for real-time business intelligence and customer analytics is accelerating Global Data Warehousing Market Growth, reinforcing the importance of scalable, low-latency analytics infrastructure. Verified data indicates that 27% of enterprises use Business Intelligence software, 28% deploy CRM systems, and over 28% analyze transaction records, highlighting strong enterprise analytics penetration. In Lithuania, 81.6% of large enterprises conduct data analytics, while EU-wide BI adoption reached 15.3%. These trends strengthen the Global Data Warehousing Market Size 2025–2032 outlook, as organizations increasingly invest in cloud-based and real-time analytics data warehouse solutions to enhance decision intelligence and customer insights.

Opportunities-Expansion of AI-Powered Self-Service Data Warehousing Solutions

• Accelerating AI Adoption Across Enterprises: EU AI usage rose to 20% in 2025 from 8% in 2023, indicating strong momentum for AI-powered data infrastructure within the Global Data Warehousing Market.

• Growing Use of AI for Data Mining & NLP: In Ireland, 10.8% of firms use AI for data mining and 9.3% for natural language generation, supporting advanced analytics capabilities.

• Automation of ETL & Query Processing: AI-driven tools enable automated ETL, predictive modeling, and AI-assisted SQL, enhancing efficiency and scalability.

• Expansion of Self-Service Analytics: AI-powered platforms empower non-technical users to independently generate insights, strengthening enterprise analytics adoption.

• Commercialization Opportunity: Rising AI integration creates growth potential for cloud-native, AI-enabled data warehouse platforms through 2032.

Restraints-Data Security and Compliance Challenges in Cloud Deployments

Rising cybersecurity incidents and evolving global regulations are emerging as structural restraints for the Global Data Warehousing Market. In 2023, 21.54% of EU enterprises experienced ICT-related security incidents, while only 35.5% maintained formally documented ICT security procedures despite over 92% implementing baseline controls (Eurostat). With cloud adoption surpassing 50% among EU enterprises, compliance maturity continues to lag infrastructure migration, influencing Data Warehousing Market Growth and increasing risk management costs across regulated cloud deployments.

• Expanding multi-cloud ecosystems heighten cross-border data governance complexity.

• Data sovereignty mandates constrain global cloud-based enterprise data warehousing strategies.

• Regulatory frameworks such as FedRAMP, NIST SP 800-63, EU Data Act, eIDAS 2.0, and ISO/IEC 27017/27018 elevate certification burdens.

• Increasing ransomware and breach incidents reinforce demand for secure, compliant data warehouse architectures.

| Restraint Factor | Impact | Likelihood | Severity |

| Expanding multi-cloud ecosystems & cross-border governance complexity | High | High | High |

| Data sovereignty mandates limiting global cloud strategies | High | Medium | High |

| Regulatory frameworks (FedRAMP, NIST SP 800-63, EU Data Act, eIDAS 2.0, ISO/IEC 27017/27018) | Medium | High | High |

| Increasing ransomware & breach incidents | High | Medium | High |

| Low compliance maturity vs cloud adoption | Medium | High | High |

Data Warehousing Market Segmentation Analysis

The Data Warehousing Market Segmentation Analysis highlights differentiated growth across Offering Type, Data Type, Deployment Mode, and Organization Size, and organization size. Increasing enterprise analytics penetration and multi-source data ingestion are reshaping the Global Data Warehousing Market.

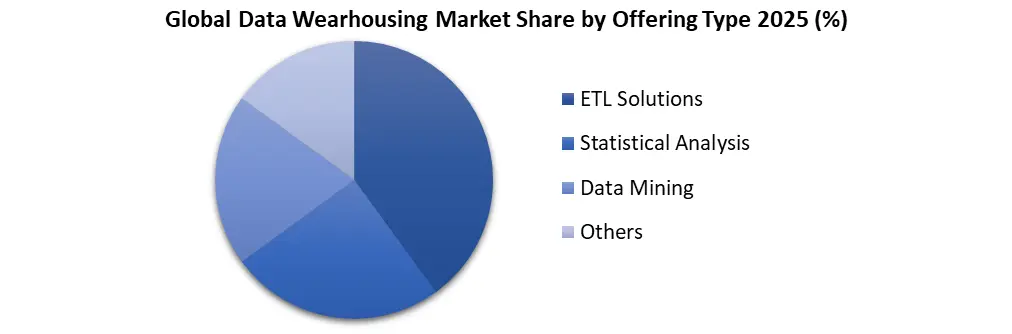

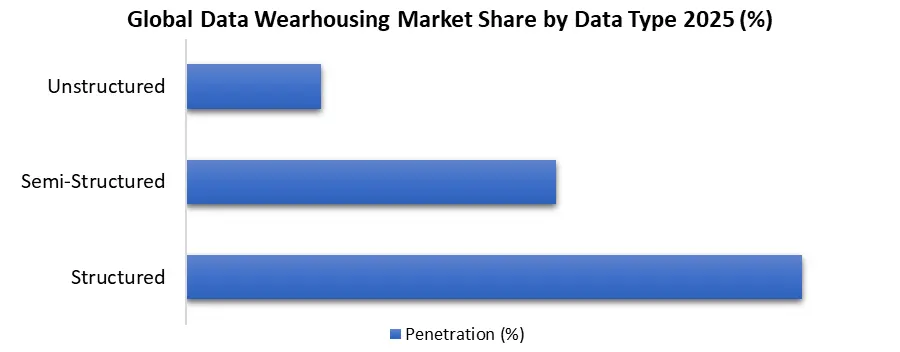

By Offering Type-ETL & database hosting remain foundational, with 45.5% of EU cloud users hosting databases, reinforcing infrastructure demand. Statistical analytics adoption reached 49% in Estonia, while 75.5% BI penetration among large Irish enterprises strengthens integrated enterprise data warehousing growth. By Data Type-Structured data dominates, with 28.2% of enterprises analyzing transaction records and 22.6% customer data, supporting traditional data warehouse architectures. However, unstructured sources including social media 12.7%, web data 12.2%, and IoT streams 5.6% are accelerating hybrid cloud data warehouse adoption.

By Data Type-Structured data dominates, with 28.2% of enterprises analyzing transaction records and 22.6% customer data, supporting traditional data warehouse architectures. However, unstructured sources including social media 12.7%, web data 12.2%, and IoT streams 5.6% are accelerating hybrid cloud data warehouse adoption.

Data Warehousing Market Regional Insights

North America continues to dominate the Global Data Warehousing Market, supported by high enterprise IT expenditure, which exceeds USD 1.5 trillion annually in the U.S., and strong cloud maturity. Over 70% of U.S. enterprises leverage advanced analytics platforms, while large-scale data center capacity continues expanding across major hubs.

Europe demonstrated 52.7% paid cloud adoption in 2025, with over 40% of enterprises performing data analytics in advanced economies. Meanwhile, Asia-Pacific is emerging as the fastest-growing region, driven by double-digit cloud spending growth rates, rapid SME digitalization, and expanding enterprise analytics investments in China and India, strengthening the long-term Data Warehousing Market Forecast trajectory.

Data Warehousing Market Competitive Landscape

• Cloud Hyperscale & Enterprise Leaders: Amazon Web Services 32% global cloud share, Microsoft Corporation 23%, and Google LLC 10% collectively control over 60% of global cloud infrastructure, reinforcing the Global Data Warehousing Market. Oracle Corporation and IBM Corporation strengthen enterprise data warehousing through integrated ERP, BI, and governance ecosystems.

• Cloud-Native & Integration Innovators: Snowflake Inc., Databricks, and Firebolt Analytics drive hybrid lakehouse and multi-cloud analytics adoption. Integration enablers like Informatica Inc., Fivetran, and dbt Labs enhance automated ETL and scalable cloud-native data warehousing deployments.

Recent Development

| Company | Year | Recent Development | Business Implication |

| Amazon Web Services (AWS) | 2024 | U.S. FedRAMP updated cloud security controls for federal authorizations. | AWS Redshift must meet enhanced federal security baselines to serve regulated data warehouse workloads in government and critical sectors. |

| Microsoft Corporation | 2024 | NIST SP 800-63 Digital Identity Guidelines Identity assurance and authentication standards by NIST. | Azure Synapse Analytics must implement multi-factor authentication and identity federation aligned with government identity standards. |

| Google LLC | 2025 | EU Data Act (Journal of the EU): Data access and use rights between cloud/data service providers and users | Google BigQuery must support transparent data access, customer-controlled portability, and governance interfaces. |

| Oracle Corporation | 2025 | eIDAS 2.0 Regulation EU cross-border trusted digital identity standards. | Oracle Autonomous Data Warehouse must enable eIDAS-compliant secure identity and authentication across EU enterprise deployments. |

| IBM Corporation | 2024 | ISO/IEC 27017 & 27018 Adoption International cloud security and cloud privacy standards recognized by ISO member bodies. | IBM Db2 Warehouse must align with formal cloud security and privacy standards to support enterprise global compliance. |

Data Warehousing Market Scope: Inquire before buying

| Data Warehousing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 38.97 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 10.7% | Market Size in 2032: | USD 79.4 Bn. |

| Segments Covered: | by Offering Type | ETL Solutions Statistical Analysis Data Mining Others |

|

| by Data Offering Type | Unstructured Data Semi-Structured & Structured Data |

||

| by Deployment Mode | On-Premise Cloud Hybrid |

||

| by Organization Size | SMEs Large Enterprises |

||

| by Industry Vertical | BFSI IT & Telecom Government Manufacturing Retail Healthcare Media & Entertainment Others |

||

Key Players in the Data Warehousing Market.

1. Amazon Web Services

2. Microsoft Corporation

3. Google LLC

4. Oracle Corporation

5. IBM Corporation

6. SAP SE

7. Teradata Corporation

8. Snowflake Inc.

9. Hewlett Packard Enterprise

10. Cloudera Inc.

11. Databricks

12. Firebolt Analytics

13. Yellowbrick Data

14. Informatica Inc.

15. SAS Institute Inc.

16. Vertica Systems

17. MicroStrategy Incorporated

18. Palantir Technologies

19. Fivetran

20. dbt Labs

21. Exasol AG

22. Micro Focus International

23. Starburst Data

24. Alibaba Cloud

25. Huawei Technologies Co., Ltd.

26. Tencent Cloud

27. ClickHouse, Inc.

28. Dremio Corporation

29. SingleStore Inc.

30. Actian Corporation

31. Others.

FAQs of Global Data Warehousing Market:

Q1: What is driving the growth of the Global Data Warehousing Market?

A1: Growth is driven by cloud adoption, real-time business intelligence, AI-powered self-service solutions, and multi-source enterprise analytics integration.

Q2: Which regions lead the Data Warehousing Market?

A2: North America leads with advanced cloud infrastructure and enterprise analytics, followed by strong cloud adoption in Europe and rapid digitalization in Asia-Pacific.

Q3: What are the main challenges in data warehousing adoption?

A3: Key challenges include data security, compliance with regulations, governance complexity, and managing multi-cloud deployments.

Q4: What are the key opportunities in the market?

A4: Opportunities include AI-powered self-service analytics, hybrid cloud adoption, automated ETL, and expansion of cloud-native and lakehouse architectures.

Q5: Which segments are driving enterprise adoption of data warehousing?

A5: High adoption is seen in ETL & database hosting, BI and CRM-integrated analytics, structured and unstructured data processing, and hybrid deployment models for large enterprises.