Container Fleet Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

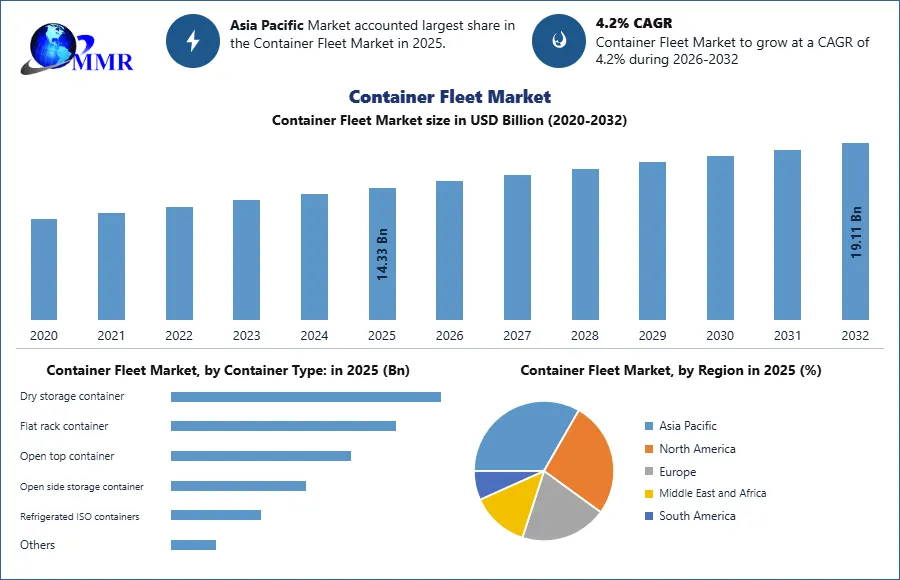

The Container Fleet Market size was valued at USD 14.33 Billion in 2025 and the total Container Fleet revenue is expected to grow at a CAGR of 4.2% from 2025 to 2032, reaching nearly USD 20.59 Billion.

Container Fleet Market Overview

The container fleet market is of paramount importance to global commerce, facilitating the seamless transportation of goods across vast distances. Containerization has revolutionized the logistics industry by offering a standardized, efficient method for cargo transport, significantly reducing costs and improving efficiency. This streamlined approach to shipping has become indispensable for businesses worldwide, driving the market forward as companies seek to capitalize on its benefits to remain competitive in the global marketplace.

Increasing globalization of trade, which has led to rising demand for efficient transportation solutions and it is driving the growth of container fleet industry. As businesses expand their reach to new markets and consumers, the need for reliable and cost-effective shipping services becomes ever more crucial. Additionally, the growth of e-commerce has further fueled demand for containerized shipping, as online retailers rely on timely delivery of goods to meet customer expectations. These factors, combined with advancements in technology and infrastructure, are growing the container fleet market forward, driving revenue growth and market share expansion. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Trends in the container fleet market reflect the industry's ongoing evolution to meet the changing needs of global trade. Key trends include the adoption of digitalization and automation technologies to enhance operational efficiency and transparency. Smart containers equipped with sensors and tracking systems are increasingly being utilized to monitor cargo conditions and optimize shipping routes. Also, there is a growing emphasis on environmental sustainability, with efforts to reduce emissions and minimize the ecological impact of container shipping operations.

End users of container fleet services span a wide range of industries, including manufacturing, retail, agriculture, and consumer goods. These industries rely on containerized shipping to transport raw materials, components, and finished products to markets around the world. As such, the container fleet market serves as a critical enabler of global supply chains, supporting economic growth and trade expansion across diverse sectors.

Key players in the container fleet market include major shipping lines such as Maersk Line, Mediterranean Shipping Company (MSC), and COSCO Shipping Lines, among others. These companies dominate market share through their extensive fleets, global network coverage, and comprehensive service offerings. As leaders in the industry, they drive innovation, set industry standards, and shape the direction of the container fleet market. Additionally, container leasing companies and terminal operators play vital roles in the market ecosystem, providing essential services and infrastructure to support containerized shipping operations.

Container Fleet Market Dynamics

"Dynamic Trends in Container Freight Rates: Insights from 2022 and Prospects for Stabilization in 2023"

The container freight market experienced significant fluctuations throughout 2022, following record-high rates at the end of 2021. Early 2022 witnessed a continuation of this upward trend, but by the third quarter, spot rates on major trade lanes notably decreased, indicating a shift from the extreme levels observed previously. By the close of 2022, container rates approached pre-pandemic levels, subsequently stabilizing in the early months of 2023. Factors contributing to this stabilization include the rebalancing of supply and demand dynamics and a reduction in port congestion.

Global containerized trade saw a slight decline in 2022, but container ship carrying capacity expanded by 3.9%, posing a supply-demand imbalance. This surplus raises concerns about supply overcapacity, with projections suggesting a further capacity influx between 2023 and 2025. Spot container freight rates eased in 2023.

Constraints and Trials in the Container Fleet Industry

The container fleet market faces significant challenges, primarily stemming from oversupply and pricing pressures. Low freight rates, driven by an oversupply of vessels and low bunker prices, pose a major obstacle. The imbalance between supply and demand in the tanker sector exacerbates pricing issues, making it difficult to predict demand accurately. With buyers initiating pricing due to low demand, shipping companies are forced to reduce prices based on cost per ton or tanker. Consequently, the reduction in freight prices results in operating costs surpassing earnings, leading to financial strain within the industry. Heavy debts further compound the financial crisis, creating a challenging environment for container fleet operators to navigate. Overall, the industry grapples with the ramifications of oversupply, fluctuating demand, and pricing pressures, which collectively hinder profitability and sustainability.

Strategic Initiatives Driving Growth in the Container Fleet Market

The container fleet market is ripe with opportunities driven by strategic maneuvers aimed at maximizing profitability. Companies are increasingly focusing on enhancing supply chain efficiency and operational productivity to gain a competitive edge. The breaking down of geographical barriers and heightened interdependency among industry verticals necessitate streamlined supply chain processes. Implementing efficient intermodal freight transportation solutions emerges as a critical strategy in this regard. Moreover, there is a growing emphasis on boosting operational efficiency amid shrinking profit margins. Leveraging fleet capacity to its fullest potential stands out as a key tactic to augment profit margins. Additionally, a shift in business strategies towards optimizing inventory and warehouse planning further underscores the potential for market expansion. These strategic moves not only present avenues for revenue growth but also underscore the evolving landscape of the container fleet industry, offering promising prospects for companies to capitalize on.

Container Fleet Market Segment Analysis

Dry Storage Container

Dry Storage Containers were the dominant segment in the Container Fleet Market in 2025. These containers held the largest market share due to their widespread versatility and cost-effectiveness in transporting a wide variety of general cargo. Dry storage containers are used extensively in industries such as retail, manufacturing, and electronics for the shipment of non-perishable goods. Their robust construction, standard dimensions, and efficiency in handling diverse goods make them the go-to choice for containerized shipping. Demand for dry storage containers was particularly strong in regions with high industrial production and trade activities, such as Asia-Pacific and North America. The global trade boom, particularly in consumer goods, further solidified dry storage containers as the most frequently used container type.

Container Fleet Market Segmentation, by Material Type

Metal Containers represented the dominant material type in the Container Fleet Market in 2025. The widespread adoption of metal containers, especially those made from steel and aluminum, was driven by their durability, strength, and long lifespan. Metal containers provide optimal protection for goods in transit, making them the most reliable choice for international shipping. Their resistance to corrosion, ability to handle heavy cargo, and suitability for various weather conditions made them the material of choice for container fleet operators. The dominance of metal containers was supported by their cost-effectiveness and the established manufacturing infrastructure, making them a key part of container fleets globally.

Container Fleet Market Segmentation, by Size Type

Large Containers (40 feet) emerged as the dominant size type in the Container Fleet Market in 2025. Their larger capacity allows for more efficient transportation of bulk goods, reducing overall shipping costs per unit of cargo. These containers are the preferred choice for international shipping, especially for industries such as electronics, machinery, and textiles, which require the transport of high volumes of goods. The widespread adoption of 40-foot containers was driven by their ability to fit seamlessly into most global transportation systems, from ships to trucks and trains. Their large capacity has made them a staple in container fleets, particularly as global trade continues to expand.

Container Fleet Market Regional Insights

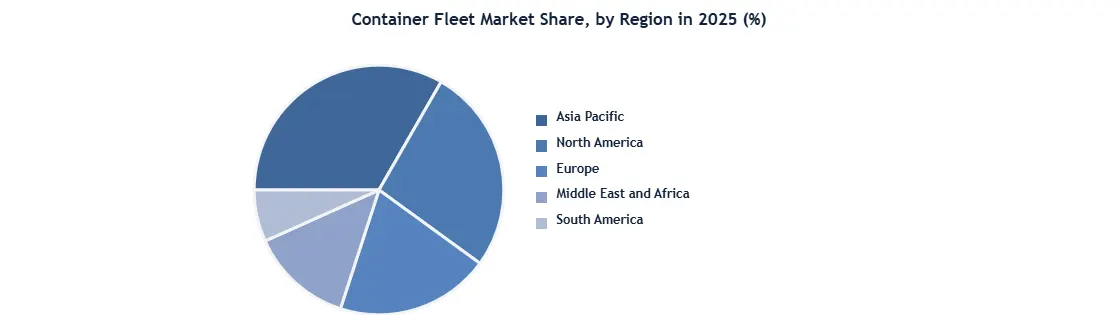

In 2025, Asia-Pacific was the leading region in the Container Fleet Market, primarily driven by the region’s industrial growth, robust trade networks, and significant port infrastructure. China, Japan, and South Korea are among the largest container fleet operators globally. The rapid expansion of manufacturing in China and Southeast Asia, coupled with increasing exports and imports, fueled demand for container fleet services. The region’s dominance can also be attributed to strong policy support from governments, such as incentives for the adoption of eco-friendly vessels and infrastructure investments in maritime logistics.

North America emerges as a formidable force in the container fleet market, propelled largely by the economic powerhouses of the United States and Canada. The region's robust industrial framework, underscored by thriving sectors such as automotive and oil and gas, underscores a heavy reliance on containerized transportation for facilitating seamless domestic and international trade. This reliance not only underscores the pivotal role of container fleets in sustaining North America's economic vibrancy but also highlights the region's enduring significance as a key player in the global logistics landscape.

Recent Development

Maersk

Maersk ordered eight additional large newbuild vessels in February 2026, bringing its total on order to 33 by the end of that month. Four of these 33 vessels were scheduled for delivery in the remainder of 2026, enhancing its container fleet with more flexible, fuel‑efficient tonnage. The company focused on deployment versatility rather than simply increasing size, aligning with its strategy to serve key trade lanes while managing costs and emissions. By 2025, Maersk had already projected about 4% growth in container volumes, underpinned by this more balanced fleet‑renewal approach.

MSC

In 2025, MSC took delivery of 25 newbuild containerships, adding approximately 316,691 TEU to its fleet that year. These deliveries included 12 Neo‑Panamax ships ranging from about 15,400 to 16,200 TEU, which doubled its Neo‑Panamax capacity and strengthened its position as the world’s largest carrier. The company also expanded its orderbook with additional 11,500‑TEU LNG‑fueled vessels, with deliveries planned from the second half of 2026 into 2027. Through these actions, MSC captured roughly 31% of global fleet growth in 2025, reinforcing its scale and efficiency advantage.

CMA CGM

In 2025, CMA CGM moved about 6.2 million TEUs in the third quarter, a 2.3% year‑on‑year increase, reflecting steady demand despite market volatility. Then, in March 2026, the group signed a letter of intent for six 1,700‑TEU dual‑fuel LNG containerships to be built at Cochin Shipyard in India. These vessels were scheduled for delivery between 2029 and 2031, as part of its fleet‑renewal and energy‑transition strategy. The deal also advanced plans for an Indian‑flagged fleet and supported local crew‑hiring, underlining CMA CGM’s commitment to both regional growth and low‑carbon shipping.

COSCO Shipping

In 2025, COSCO Shipping commissioned three green methanol‑dual‑fuel vessels and announced a major order for 14 additional 18,500‑TEU methanol‑dual‑fuel ships, bringing its total green‑fuel fleet to 42 vessels. The new 18,500‑TEU ships were scheduled for delivery in 2027 and 2028, adding nearly 780,000 TEU of low‑emission capacity. The company also began converting several ultra‑large containerships to methanol use, with work on the first conversion completed in August 2025. Container volumes had risen by about 5.8% year‑on‑year in 2025, demonstrating that COSCO’s “green‑fleet‑expansion” strategy was already underway.

Hapag‑Lloyd

In November 2025, Hapag‑Lloyd announced plans to invest in up to 22 new containerships of under 5,000 TEU as part of its fleet‑modernization and decarbonization program. The investment, disclosed along with its financial results for the first nine months of 2025, targeted the replacement of older small‑to‑medium vessels with more fuel‑efficient designs. The German carrier approached Chinese shipyards to build two series in the 3,100 TEU and 4,500 TEU ranges, with deliveries expected after the orders were finalized. By 2025, Hapag‑Lloyd’s fleet stood at about 2.5 million TEU across 305 vessels, and this expansion aimed to improve efficiency on regional and feeder routes while supporting its net‑zero‑fleet target by 2045.

Container Fleet Market Scope: Inquire before buying

| Container Fleet Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 14.33 Billion |

| Forecast Period 2026-2032 CAGR: | 4.2% | Market Size in 2032: | USD 19.11 Billion |

| Segments Covered: | by Container Type: | Dry storage container Flat rack container Open top container Open side storage container Refrigerated ISO containers Others |

|

| by Material Type: | Metal Wood Bamboo Vinyl Others |

||

| by Size Type | Small Containers (20 feet) Large Containers (40 feet) High Cube Containers (40 feet) |

||

| by End-use Industry: | Food & Beverages Consumer Goods Healthcare Industrial Products Vehicle Transport Others |

||

Container Fleet Market, by Region:

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/competitors profiles covered in the Container Fleet Market report in strategic perspective:

- Maersk Line

- Mediterranean Shipping Company (MSC)

- CMA CGM Group

- COSCO Shipping Lines

- Evergreen Marine Corporation

- Hapag-Lloyd

- ONE (Ocean Network Express)

- Yang Ming Marine Transport Corporation

- Hyundai Merchant Marine

- ZIM Integrated Shipping Services

- K Line

- Mitsui O.S.K. Lines (MOL)

- Hanjin Shipping

- China Shipping Container Lines

- PIL (Pacific International Lines)

- Arkas Line

- X-Press Feeders

- Wan Hai Lines

- SITC International Holdings

- Unifeeder

- Hamburg Süd

- Seaboard Marine

- Swire Shipping

- Euroseas