Connected and Autonomous Mobility Vehicles Market Size by Level of Automation, Vehicle Level of Automation, Propulsion Level of Automation, Application, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

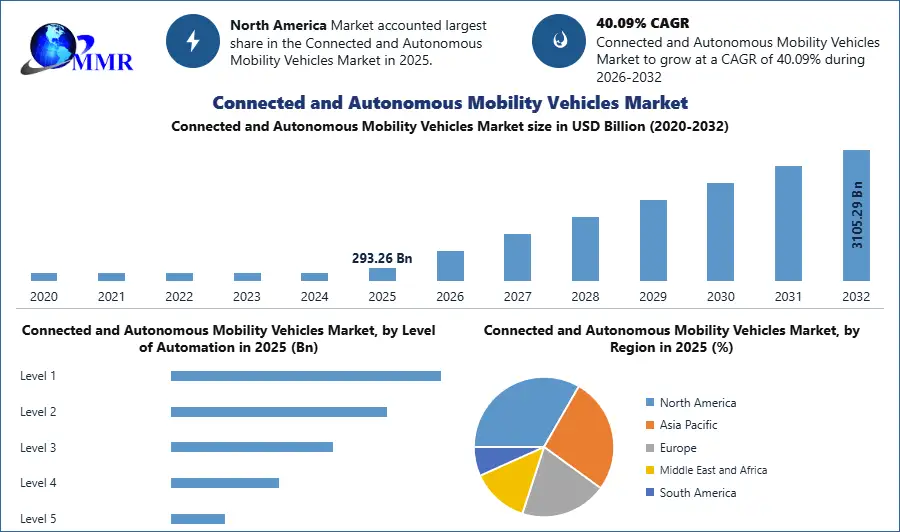

The Connected and Autonomous Mobility Vehicles Market size was valued at USD 293.26 Billion in 2025 and is expected to grow at a CAGR of 40.09% from 2026 to 2032, reaching nearly USD 3105.29 Billion.

The Connected and Autonomous Mobility Vehicles Market is a rapidly evolving sector that has the potential to revolutionize transportation. It represents a convergence of cutting-edge technologies, integrating connectivity, automation, and artificial intelligence to create a new era of safer, more efficient, and sustainable mobility. Connected mobility vehicles are equipped with advanced communication systems that allow real-time data exchange, facilitating vehicle-to-vehicle and vehicle-to-infrastructure communications to improve traffic management and enhance safety. Automation is a crucial aspect, with vehicles equipped with sensors, cameras, and AI-powered algorithms, reducing human errors and fatigue, making transportation safer. AI processes and massive data analysis enhance vehicle performance, optimize routes, and enable predictive maintenance, elevating efficiency and reliability. A significant trend is the focus on sustainability, with many vehicles powered by electric drivetrains contributing to a cleaner transportation ecosystem.

The rise of connected and autonomous mobility has given birth to innovative mobility services, such as ride-sharing and Mobility-as-a-Service platforms. For successful implementation, smart cities and infrastructure play a vital role. Challenges include regulatory hurdles, safety concerns, and data security, requiring comprehensive frameworks and consumer trust. Despite these challenges, the market offers vast opportunities, with new business models emerging, data monetization potential, and improved user experiences. In conclusion, the Connected and Autonomous Mobility Vehicles Market promises safer, more efficient, and sustainable mobility solutions. It is poised for exponential growth and innovation. Integrating technology into urban planning and infrastructure enables efficient traffic management, optimized routing, and seamless communication between vehicles and transportation systems.

Connected and Autonomous Mobility Vehicles Market Scope and research methodology:

The scope of the study focuses on the Connected and Autonomous Mobility Vehicles (CAMVs) market globally, covering a specific period. The research objectives encompass understanding market trends, analyzing market size and growth, identifying key market players, assessing the competitive landscape, exploring regulatory factors, and understanding consumer preferences. Data for the research is gathered from both primary and secondary sources, including surveys among EMS providers, healthcare professionals, and manufacturers. In addition, it is gathered from relevant publications and reports.

Market segmentation categorizes the market based on Vehicle Type Level of automation, Propulsion Type, and geographical regions. Data analysis employs statistical analysis, qualitative content analysis, and visualization methods. Market forecasting involves projecting future growth and trends considering technological advancements, regulatory changes, and market demand drivers. The research also includes a competitive analysis of major players in the CAMVs market globally. This analysis evaluates their market share, Vehicle Type offerings, growth strategies, and competitive advantages. Ethical considerations address data privacy, participant consent, and potential conflicts of interest. In addition, they acknowledge research limitations related to data availability, biases, and unforeseen events.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Connected and Autonomous Mobility Vehicles Market Dynamics:

Smart Cities Embrace Connected and Autonomous Mobility Vehicles for Efficient Mobility.

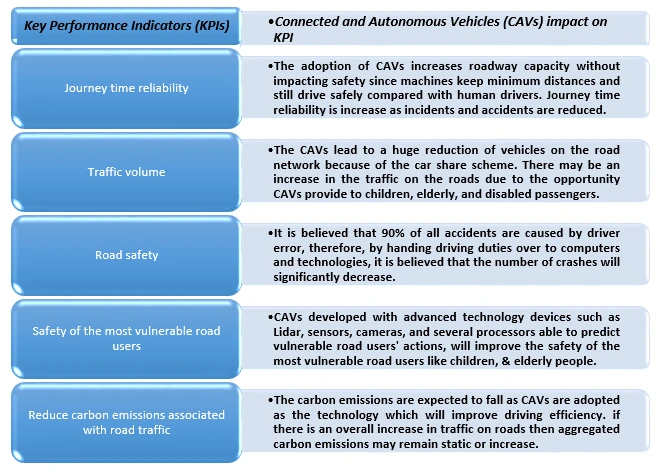

The Connected and Autonomous Mobility Vehicles market has had rapid advancements in recent years, transforming people and goods transportation. These vehicles, equipped with advanced technologies like sensors, artificial intelligence, and connectivity, promise to revolutionize the transportation industry. One of the primary drivers behind CAMVs is improved road safety. Autonomous vehicles are expected to significantly decrease accidents caused by human error, which accounts for a substantial portion of road mishaps. The global increasing focus on environmental sustainability and climate change combat is driving the adoption of connected and autonomous electric vehicles.

These vehicles have the potential to reduce carbon emissions significantly and combat air pollution. CAMVs optimize traffic flow, reduce congestion, and enhance transportation efficiency. Continuous advancements in sensor technology, AI, and data processing have propelled autonomous vehicles. These innovations have made the technology more reliable and capable of handling various real-world scenarios. Ride-sharing and Mobility-as-a-Service platforms have increased demand for connected and autonomous vehicles. CAMVs can serve as a vital component of these services, providing efficient, cost-effective, and on-demand transportation solutions. CAMV can offer accessible and safe transportation options, promoting independence and social inclusion. Governments around the world actively support CAMV development and adoption. Supportive regulations and financial incentives encourage companies to invest in research and development in this field.

Challenges of Ensuring Safety in Fully Autonomous Vehicles.

Developing fully autonomous vehicles with fail-safe systems is complex and expensive. Ensuring the safety and reliability of CAVs remains a significant challenge for manufacturers and regulators. Connected and Autonomous Mobility Vehicles deployment relies on advanced infrastructure, including high-quality road networks, smart traffic signals, and communication systems. Upgrading existing infrastructure to support CAVs can be costly and time-consuming. The lack of standardized regulations for CAVs across different regions and countries is a major hindrance. Clear and consistent regulatory guidelines are essential for widespread CAV adoption. Connected vehicles are susceptible to cyber security threats, including hacking and data breaches. Ensuring the security and privacy of data transmitted and received by CAVs is critical to building trust among consumers.

Convincing the general public about CAV safety and reliability is a challenge. Overcoming scepticism and fear of autonomous technology is crucial to their widespread acceptance. Determining liability in accidents involving CAVs is a complex legal challenge. Addressing liability concerns and establishing a clear legal framework is essential to support the CAV market growth.

Smart Cities Change Governance for Connected and Autonomous Mobility Vehicle Advancements.

Collaboration between technology companies, automotive manufacturers, and governments can accelerate CAV development and deployment. Partnerships leverage various sectors' expertise and resources. Governments around the world that aspire to develop smart cities need to change their governance models. The reduction of greenhouse gas emissions, sustainable development, and improved urban infrastructure energy efficiency are other societal challenges. Smart mobility challenges to create an inclusive, environmentally friendly, and efficient transportation system for people and Vehicle Types. This could be achieved with CAVs. CAVs generate vast amounts of data, offering opportunities for data-driven services and insights.

Companies utilize this data for personalized mobility solutions and urban planning. CAVs drive urban planning initiatives focused on environmentally friendly and efficient transportation. Cities redesign infrastructure to accommodate CAVs and promote sustainable mobility options. Ride-sharing companies can reduce congestion and enhance mobility options for metro dwellers. The Connected and Autonomous Mobility Vehicles Market holds significant potential for transforming transportation and mobility in the future. The benefits of increased safety, efficiency, and environmental sustainability offer exciting opportunities for the automotive industry, technology companies, and governments to shape the future of transportation.

Connected and Autonomous Mobility Vehicles Market Segmental Insights:

Based on the Vehicle Level of Automation, In the Connected and Autonomous Mobility Vehicles Market, passenger vehicles dominate the market in 2023 and are expected to grow during the forecast period. CAMVs in passenger vehicles are driven by enhanced safety, convenience, and improved mobility solutions. High initial costs and concerns about consumer acceptance can be significant challenges to CAMV adoption in passenger vehicles. Ride-sharing and Mobility-as-a-Service (MaaS) platforms offer opportunities for CAMV integration, providing cost-effective and efficient transportation services. Commercial Vehicles Fleet operators seek to optimize their operations through autonomous commercial vehicles, reducing labor costs and improving logistics efficiency. The cost of transitioning to CAMVs and the need for specialized training for drivers can be barriers to adoption. Autonomous delivery vehicles and trucks have the potential to revolutionize the logistics and transportation industry, providing faster and more efficient delivery services.

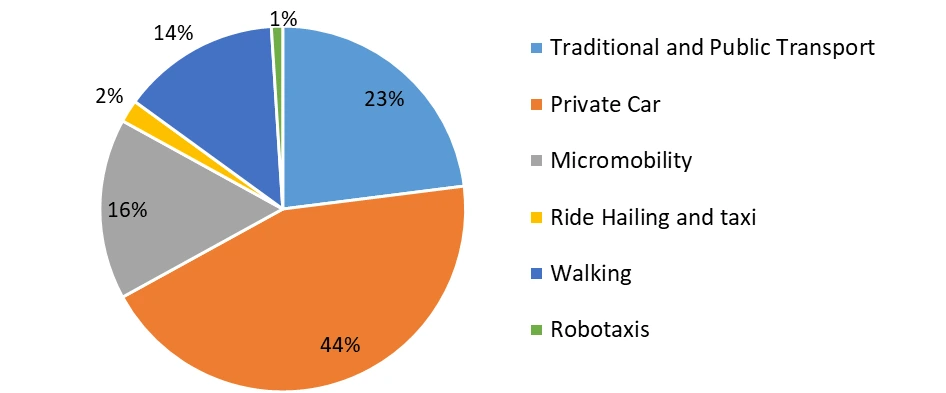

Mobility split by mode of transportation, worldwide, 2023, (%)

Connected and Autonomous Mobility Vehicles Market Regional Insights:

North America is at the forefront of the Connected and Autonomous Mobility Vehicles (CAMV) market, with the United States and Canada leading in research, development, and testing. The region benefits from a strong automotive industry and a vibrant technology ecosystem. Government support and permissive regulations in various states have encouraged companies like Waymo, Tesla, and GM's Cruise to conduct extensive trials and pilot programs. Ride-sharing and Mobility-as-a-Service (MaaS) platforms have become popular, creating an environment conducive to the adoption of CAMVs. Safety, liability, and robust infrastructure remain challenges to address, especially in less populated and rural areas.

Europe presents significant opportunities for CAMVs, driven by strong government support and initiatives. Countries like Germany, the UK, and Sweden have established comprehensive frameworks and regulations to facilitate testing and deployment. Europe's established automotive industry, with companies like Volkswagen, BMW, and Daimler, invests heavily in CAMV development, making substantial progress in Level 2 and Level 3 automation. Urbanization and the need for sustainable transportation solutions propel CAMVs into crowded cities like London, Paris, and Berlin. The region faces challenges of regulatory fragmentation, as each country has distinct autonomous vehicle rules. Data protection laws, particularly in the European Union, impose strict requirements for handling and storing vehicle data, affecting data-driven innovation. Furthermore, Brexit introduces uncertainties regarding cross-border collaborations and regulatory harmonization in the CAMV market. Despite these challenges, Europe's commitment to innovation and robust research and development capabilities continue to drive advancements in the CAMV sector.

Asia-Pacific fast-growing urban centers face increasing transportation challenges, leading to demand for smart and efficient mobility solutions. Asia-Pacific countries, such as China and Singapore, have ambitious plans and policies to support CAMV development. Asian countries, particularly China, invest heavily in AI and autonomous vehicle technologies, driving market growth. International companies form partnerships with local automakers and technology firms to tailor CAMV solutions to the region's specific needs. CAMVs support the growing trend of shared mobility services in urban centers.

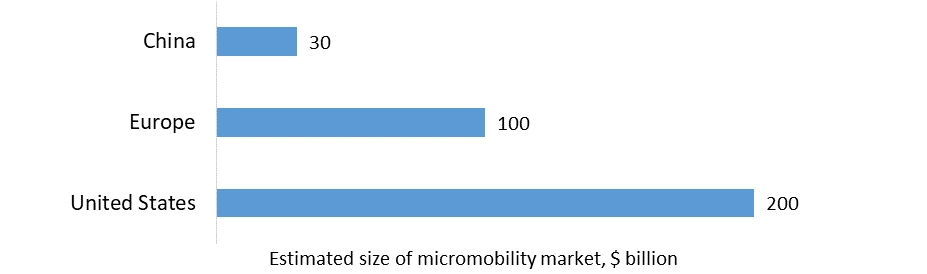

The Shared micromobility market in China, Europe, and The United States. in 2032, (In Billion)

Competitive Landscape

Key Players of the Connected and Autonomous Mobility Vehicles Market profiled in the report include AB Volvo, Amazon Web Services, Inc., Aptiv, ARTHUR D. LITTLE, AVL, BMW AG, Daimler AG, Dassault Systèmes, Ford Motor Company, FutureBridge, General Motors, Honda, Motor Co., Ltd., Hyundai Motor Company, Infineon Technologies AG, Nissan Motors Co., Ltd., Renault Group, SAE International, Segula Technologies, Swiss Re, Tesla, Inc., Toyota Motor Corporation, UITP Advanced Public Transport, Volkswagen AG, WirelessCar, WSP. This provides huge opportunities to serve many End-uses & customers and expand the Connected and Autonomous Mobility Vehicles Market.

Connected and Autonomous Mobility Vehicles Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 11 February 2026 | Mercedes-Benz | The company announced a strategic shift for the 2026 S-Class, replacing the Level 3 Drive Pilot with the MB Drive Assist Pro (Level 2++) in the U.S. market. | This move aims to perfect high-level driver assistance across wider geographies while engineering resources are redirected toward 81 mph Level 3 and Level 4 systems. |

| 17 June 2025 | NXP Semiconductors | NXP finalized the acquisition of TTTech Auto, a leader in safety-critical middleware for software-defined vehicles (SDVs). | The deal strengthens NXP’s ecosystem for autonomous driving architectures by integrating advanced deterministic networking and safety software. |

| 07 August 2025 | Baidu, Inc. | Baidu partnered with Lyft to deploy Apollo Go autonomous vehicles across European markets, starting with pilots in Germany and the U.K. | The collaboration marks a significant international expansion of Chinese autonomous technology into the European Robotaxi sector. |

| 03 October 2025 | Stellantis | The company announced a major expansion of its Gqeberha plant to produce a new lineup of connected commercial vehicles. | This expansion enhances Stellantis' regional manufacturing footprint for smart logistics and autonomous-ready fleet solutions. |

| 10 November 2025 | Waymo (Alphabet Inc.) | Waymo officially opened freeway access for autonomous passenger trips across the San Francisco Bay Area and Los Angeles. | This milestone significantly reduces travel times and demonstrates the commercial viability of Level 4 autonomy in high-speed urban corridors. |

Connected and Autonomous Mobility Vehicles Market Scope: Inquire before buying

| Connected and Autonomous Mobility Vehicles Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 293.26 USD Billion |

| Forecast Period 2026-2032 CAGR: | 40.09% | Market Size in 2032: | 3105.29 USD Billion |

| Segments Covered: | by Level of Automation | Level 1 Level 2 Level 3 Level 4 Level 5 |

|

| by Vehicle Level of Automation | Passenger Car Commercial Vehicle |

||

| by Propulsion Level of Automation | Semi-autonomous Fully Autonomous |

||

| by Application | Residential Commercial |

||

Connected and Autonomous Mobility Vehicles Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina, and the Rest of South America)

Connected and Autonomous Mobility Vehicles Market, Key Players

- AB Volvo

- Amazon Web Services, Inc.

- Aptiv PLC

- AVL List GmbH

- Baidu, Inc.

- BMW Group

- BYD Co. Ltd.

- Daimler AG (Mercedes-Benz Group AG)

- Dassault Systèmes

- Ford Motor Company

- General Motors

- Honda Motor Co., Ltd.

- Hyundai Motor Company

- Infineon Technologies AG

- Intel Corporation

- Magna International Inc.

- Nissan Motor Co., Ltd.

- Nvidia Corporation

- Renault Group

- SAE International

- Segula Technologies

- Swiss Re

- Tesla, Inc.

- Toyota Motor Corporation

- Volkswagen AG