Coating Resins Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2030

Overview

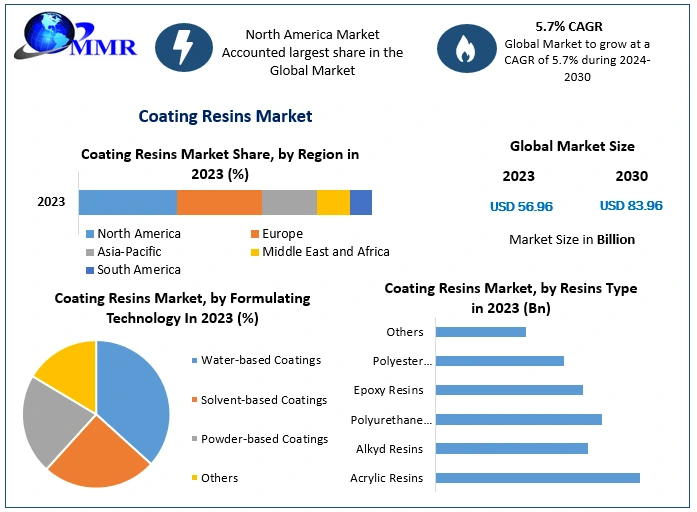

Coating Resins Market was valued at USD 56.96 Billion in 2023, and it is expected to reach USD 83.96 Billion by 2030, exhibiting a CAGR of 5.7% during the forecast period (2024-2030)

Coating resins are polymer compounds that are utilised as major components in the manufacturing of paints and coatings. These compounds are utilised as protective coatings in many sectors, including automotive, architectural, machinery, wood, pulp and paper, and marine, to offer corrosion resistance and to avoid chemical weathering and discoloration. Automobiles, containers, and anti-corrosion coatings employ water-based polyurethane, water-based alkyd, water-based epoxy, and water-based acrylic resins. Although the raw ingredients used to make paints and coatings have a lower profit margin (about 5%), they are critical components of the global chemicals industry.

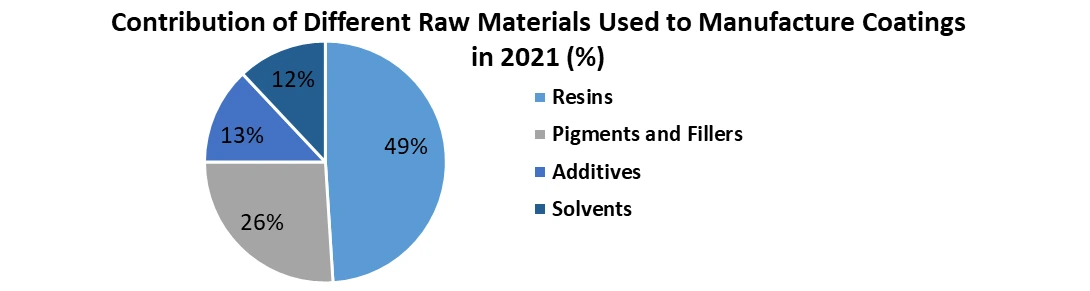

Resins are most often used as raw materials, accounting for around 49% of total raw material value, followed by pigments and fillers, additives, and solvents. Coating resins are used in a variety of sectors, including automotive, pulp and paper, wood aerospace, and architectural and marine coating. Thanks to rising demand from architectural, automotive, and wood coatings, the global coating resins market is expected to grow rapidly in the coming years. Furthermore, rising buying power and rising living standards are fuelling the manufacture of furniture, vehicles, and the development of residential and non-residential structures all over the world. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Research Methodology

The research process comprises the investigation of various factors affecting the industry, such as historical data, market environment, technological innovation, upcoming technologies, government policy, competitive landscape and technical progress in related industries, as well as current market trends, market risks, opportunities, market barriers, and challenges. Primary and secondary methods are used for collecting the data in the report. Secondary sources, such as annual reports, press releases, industry associations, non-profit groups, governmental agencies, and customs data, account for around 25% of data sources.

Secondary sources, directories, and databases such as Factiva (Dow Jones & Company), Bloomberg Business, Hoovers, Wind Info, Statista, Trading Economics, and Avention, Investing News Network, Federal Reserve Economic Data, annual reports, investor presentations, and SEC filings of companies are included in the research report. To deliver the final quantitative and qualitative data, all possible components impacting the markets included in the report were investigated, extensively researched, validated through primary research, and reviewed. Bottom-up technique has been used in the market engineering process, along with several data triangulation methodologies, to estimate the market and forecast the overall market segments and sub-segments covered in the report.

Coating Resins Market Dynamics

Coating Resins Market Dynamics

Increase in Construction Activities Across Middle East & Africa Region

The construction industry is a key sector in the Middle East and Africa. The Middle East and Africa are expected to witness tremendous growth in the construction sector as a result of population growth, economic growth, improved living standards, and more foreign investment. In the Middle East, an estimated $1 trillion in building and infrastructure projects are planned and being bid for completion until 2025. Over the previous decade, the region has seen almost $300 billion in building and $200 billion in infrastructural investments.

The majority of these projects are based in Saudi Arabia, Iraq, the United Arab Emirates, and Qatar. By 2025, an estimated $1.5 trillion will be spent in the region, excluding industrial infrastructure. The majority of projects are focused on highway and intercity transportation systems, communication networks, healthcare facilities, energy infrastructure, and aviation infrastructure. In growth of Coating Resins Market, the growing construction activities across the world play a significant role.

Affordable housing remains a key issue in the area, with low indigenous property ownership, notably in Saudi Arabia and the UAE. Due to the increasing number of immigrants, a comprehensive development strategy in housing infrastructure is required. Saudi Arabia, for example, needs to create 1.5-2 million dwellings by 2022 to meet up with rising demand for residential space. The population growth has required the necessity for a comprehensive housing infrastructure expansion plan, further driving the growth of coating resins industry. Retail building, including huge malls and open areas, is expected to skyrocket in the region. As a result, demand for coating resins will be driven by the building of houses, malls, retail complexes, multiple megaprojects, and railways.

Increasing Use of Powder Coatings in Automotive Industry

Powder coating is a common process for coating metallic items with a protective and/or ornamental layer. A powder coat, unlike liquid paints, is a dry compound that does not dip or run when applied. As a result, powder coatings are widely employed in the automobile sector to give cars an attractive appearance, protect them from environmental harm, and comply with regulatory VOC restrictions. As a result, the growing usage of powder coatings will boost the coating resin industry. Powder coatings are commonly utilised to assure good looks and great performance in automobile components such as bodywork, trims, aluminium wheel rims, and underbody components. These coatings help to safeguard the environment since they do not require solvents and hence emit no hazardous emissions into the atmosphere.

Powder coatings lessen the likelihood of abrasions, scratches, wear and tear, chipping, and fading. They are also employed in rail transportation and components for their anti-graffiti, corrosion resistance, surface hardness, and weathering resilience. These characteristics improve substrate durability and save maintenance costs. Powder coatings are now widely utilised in the automobile industry to protect car structures from damage caused by moisture, chemicals, UV radiation, acid rain, and weather damage, as well as to assist retain moisture. Another key reason for powder coating technology's appeal is its zero VOC emissions, which allows suppliers to comply with laws requiring minimal VOC content. This is expected to drive the growth of coating resins market during the forecast period. Increasing Use of Bio-Based Epoxy Resins

Increasing Use of Bio-Based Epoxy Resins

The coating resins industry has seen a surge in demand for bio-based epoxy resins in recent years. The fast depletion of fossil resources, as well as environmental worries about rising greenhouse gas emissions, have driven to a greater usage of renewable feed supplies. Such environmental concerns have also prompted the long-term development of a variety of polymeric materials, including resins and commodity polymers. Most significantly, the process of converting polymers from renewable resources adheres to green chemistry principles such as pollution prevention, energy efficiency, and carbon footprint reduction. Bio-based epoxy resins have unique qualities that set them apart from other epoxy resins on the coating resins market.

No unpleasant odour, significantly superior to petroleum-based epoxy resins, low VOC content, low odour, greater strength, and UV resistance are just a few of the astonishing qualities of bio-based epoxy resins. As a result of the advantageous features of bio-based epoxy resins, demand for bio-based epoxy resins is expanding. Paints and coatings, electronics, automotive, construction, aerospace, packaging, and adhesives are among applications for biobased epoxy resins. They are utilised in structures as floor or sealant coverings. Biobased epoxy resins are also employed in the production of glass fibre items such as rainwater tanks, marine boats, and electrical circuit boards.

High Raw Material Costs to Restraint the Market Growth

Over the last few years, resin suppliers all over the world have faced certain constraints. Almost majority of these basic ingredients come from crude oil. The price of crude oil is typically high and volatile, and it has a direct influence on the price of resin, which affects the cost of coating goods. Because there are so many FMCG businesses in the market, it is difficult for them to adjust product prices owing to the competitive element and the presence of local players selling the same items at a cheaper price. As a result, such variables may impede suppliers and disrupt their supply chain.

The rising cost of raw ingredients is a perennial annoyance for makers of paints and coatings. The most significant component in the production of any area of the manufacturing business is raw materials. As the global trade war escalates and raw material prices continue to rise, resin suppliers are attempting to cut costs in order to boost profitability. Because most raw materials used in the paint and coatings business are derived from crude oil, the growing price of crude oil and uncertainty caused by political areas in the Middle East and Africa region have had a significant influence on the paint and coating sector. This is expected to restraint the growth of Coating Resins Industry during the forecast period.

Increasing Environmental Regulation to Hamper the Growth of the Market

Many items include volatile organic compounds (VOCs), including coatings, adhesives, sealants, printing inks, organic solvents, and petroleum products. VOC-containing products are a major source of air pollution and haze in cities. To manage air quality, some countries throughout the world have established VOC emission laws. The governments of North America, Europe, and China enacted these restrictions to control the emissions of volatile organic compounds. Paint and coating producers in the United States must aim to reduce harmful waste output and air emissions.

They employ a range of substances, which cause the Toxic Release Inventory to be released (TRI). In 2019, 640 paints and coatings plants reported the emission of 53.82 million pounds of chemicals (including disposal), of which 1.42 billion were controlled through treatment, energy recovery, and recycling. Toxins have been decreased in the United States throughout the years as a result of the introduction of different restrictions. Total TRI disposal and other chemicals released into the environment by paints and coatings dropped significantly in 2019. VOC restrictions and emission requirements pose difficulties for coatings manufacturers. Coatings producers are seeking for new raw materials that are less hazardous to the environment due to government requirements. Coatings makers must seek solutions for producing environmentally friendly coatings without sacrificing performance.

Toxins have been decreased in the United States throughout the years as a result of the introduction of different restrictions. Total TRI disposal and other chemicals released into the environment by paints and coatings dropped significantly in 2019. VOC restrictions and emission requirements pose difficulties for coatings manufacturers. Coatings producers are seeking for new raw materials that are less hazardous to the environment due to government requirements. Coatings makers must seek solutions for producing environmentally friendly coatings without sacrificing performance.

Water-based coatings, powder coatings, UV cure coatings, and other low VOC coatings are becoming more popular as a result of regulatory pressure and ongoing market trends. These coatings aid in the reduction of hazardous air pollutants (HAP) as well as VOC emissions. This is expected to hamper the growth of Coating Resins Industry during the forecast period.

Coating Resins Market Segment Analysis

Based on Resins Type, Acrylic coating resins are the most widely used resins in the coating resins industry. Acrylic coating resins segment dominated the coating resins market and is expected to grow at a highest CAGR of 6.05% during the forecast period. Acrylic paints are mostly used outside and are being phased out in favour of water-based acrylic coatings for environmental concerns. As a result of tight laws requiring low VOC content, water-based acrylic paints are more frequently employed in North America and Europe than in APAC.

Acrylic resins are utilised in a variety of applications, including architectural coatings, special purpose coatings, and OEM product finishes (OEMs). Acrylic polymers are in great demand because they are inexpensive and provide strong chemical and photochemical resistance, stain resistance, water resistance, and surface adherence.During the forecast period, the epoxy resins segment is expected to develop at a substantial CAGR of 5.50%. Because of their great strength, adaptability, and good adherence to a wide range of surfaces, epoxy resins are widely utilised in the paints and coatings industry.

Epoxy resins offer strong adhesive properties, making them a flexible product for a wide range of end-use industries. Epoxy resins are popular because to their superior mechanical qualities, which include heat resistance, chemical resistance, durability, corrosion resistance, and electrical insulation. Because of these properties, epoxy coating resins are appropriate for a wide range of end-use applications, including paint cans, metal containers, ornamental flooring, automotive, marine, and aerospace.

Based on Formulating Technology, Water-borne coating segment is expected to dominate the Coating Resins market and grow at a highest CAGR of 6.38% during the forecast period. Because of the minimal VOC emissions, water-borne coating is an environmentally beneficial coating. Water-borne coating is outselling solvent coating due to consumer demand for environmentally friendly coating and government regulations limiting VOC emissions. Water-borne coatings are widely utilised in building, architecture, industrial wood, protective coating, metal packaging, automobile OEM & refinish, and other sectors. Among all industries, the architectural industry consumes the most water-borne coating. Acrylic-based resins are widely utilised to minimise VOC emissions in water-borne coatings.

The largest market for water-borne coating is Europe, followed by APAC. Water based coating is in high demand in Europe due to increased demand in automotive and coil coating. It's applicability in end-user industries is growing as its performance improves. Water coating performance has improved due to advancements in resin chemistry and novel additives especially intended for waterborne formulations. New developments in these materials enable formulators to increase performance in areas historically dominated by solvent-borne coatings, such as direct-to-metal (DTM) coatings and applications requiring specialised qualities such as high gloss.

Based on End-Use, Architectural coating segment dominated the coating resins industry in 2023 and is expected to grow at a CAGR of 5.41% during the forecast. The global architectural coatings market is still in its early stages. The growing global construction industry, the recovery of the US housing market, and the ongoing need for sustainable paints, particularly in APAC's emerging nations, will support the segment's expansion. Furthermore, changing customer tastes and rising consumer knowledge about product safety and VOC emissions from architectural coatings are driving the market. Furthermore, during the forecast period, the move from solvent-borne to water-borne coating formulations will add to the growth of the global architectural coatings market.

Vinyl coating resins are the primary choice for wall emulsion in the interiors of houses in architectural coating. Architectural coatings are accessible to the majority of consumers due to their cheap manufacturing costs. Polyurethane and epoxy-based coatings are now employed in specialist applications; hence their consumption is rather modest. Similarly, the fast falling usage of polyester coatings is due to their high solids content, which leads in greater VOC emissions, making it dangerous to the environment and individuals living within the residential or commercial area.

Coating Resins Market Regional Insights

APAC dominated the global coating resins market in 2023, accounting for 44.56% of revenue, which is expected to grow further in the future years. India, China, and Japan are important consumers of coating resins in APAC, with a combined sales share of around $10,948.50 million in 2021. APAC is expected to develop at the quickest rate during the forecast period, with a CAGR of 5.64%. By 2030, the APAC coating resins market is expected to be worth $30,457.95 million.

Factors such as growing urbanisation and significant government investment to expand housing constructions have led to the rise of the construction sector, which has accelerated demand for resins since they provide buildings a glossy and appealing appearance while also ensuring longevity. Coating resins also provide chemical resistance and UV resistance, preventing building walls from yellowing, which has increased demand for coating resins. Furthermore, rising automobile manufacturing and the popularity of online meal delivery services are driving up demand for coating resins.

North America held a 24.15% revenue share of the global coating resins industry in 2023. North America is the fastest-growing market for coating resins, with a major increase in demand expected in the future years. The growing need for coating resins in North America is being driven by increased demand from aviation, green home development, and other forthcoming construction projects. The United States and Canada are the largest markets for coating resins.

Europe will account for 21.54% of the global coating resins industry in 2023. Germany, Russia, France, and the United Kingdom are the region's largest coating resin markets. Europe is estimated to grow slowly because tight rules imposed by various governments to maintain minimal VOC emissions. Although there is a rising need for water-borne coatings, they are not practical for some sectors such as automobile manufacture and a variety of other applications such as corrosion resistance.

South America coating resins market revenue share was 5.80% in 2023. According to estimates, the coating resins industry will rise significantly over the forecast period due to an increase in building activity in the region. In addition, the Middle East and Africa (MEA) will account for 4.32% of market revenue in 2023. The increased demand for coating resins from the marine, construction, and furniture industries will fuel market expansion.

Coating Resins Market Scope: Inquire before buying

| Coating Resins Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 56.96 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 5.7% | Market Size in 2030: | US $ 83.96 Bn. |

| Segments Covered: | by Resins Type | Acrylic Resins Alkyd Resins Polyurethane Resins Epoxy Resins Polyester Resins Others |

|

| by Formulating Technology | Water-based Coatings Solvent-based Coatings Powder-based Coatings Others |

||

| by End-Use | Architectural Coatings General Industrial Coatings Powder Coatings Wood Coatings Automotive OEM Coatings Automotive Refinish Coatings Protective Coatings Packaging Coatings Others |

||

Coating Resins Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Coating Resins Market, Key Players are:

1. Dow Inc (US)

2. Momentive Inc (US)

3. Coating Technologies LLC (US)

4. The Sherwin-Williams Company (US)

5. Hexion Inc. (US)

6. Valspar Corporation (US)

7. Bayer AG (Germany)

8. Evonik Industries AG (Germany)

9. LANXESS (Germany)

10. BASF SE (Germany)

11. Ceramicoat Limited (UK)

12. Arkema S.A. (France)

13. ICA SpA (Italy)

14. Mutina S.P.A. (Italy)

15. Polynt S.P.A. (Italy)

16. Koninklijke DSM N.V. (Netherlands)

17. Akzo Nobel N.V. (Netherlands)

18. PT. Citra Resins (Indonesia)

19. Allnex Holdings S.A R.L. (Luxembourg)

20. HELIOS Resins (Slovenia)

21. Sumitomo Corporation (Japan)

22. DIC Corporation (Japan)

23. Nuplex Industries Limited (Australia)

24. Eternal Resin Co. Ltd. (Thailand)

Frequently Asked Questions:

1] What segments are covered in the Global Coating Resins Market report?

Ans. The segments covered in the Coating Resins Market report are based on Resins Type, Formulating Technology, End-Use.

2] Which region is expected to hold the highest share in the Global Coating Resins Market?

Ans. The Asia Pacific region is expected to hold the highest share in the Coating Resins Market.

3] What is the market size of the Global Coating Resins Market by 2030?

Ans. The market size of the Coating Resins Market by 2030 is expected to reach USD 83.96 Bn.

4] What is the forecast period for the Global Coating Resins Market?

Ans. The forecast period for the Coating Resins Market is 2024-2030.

5] What was the market size of the Global Coating Resins Market in 2023?

Ans. The market size of the Coating Resins Market in 2023 was valued at USD 56.96 Bn.