Cloud Management for the OpenStack Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast (2026-2032)

Overview

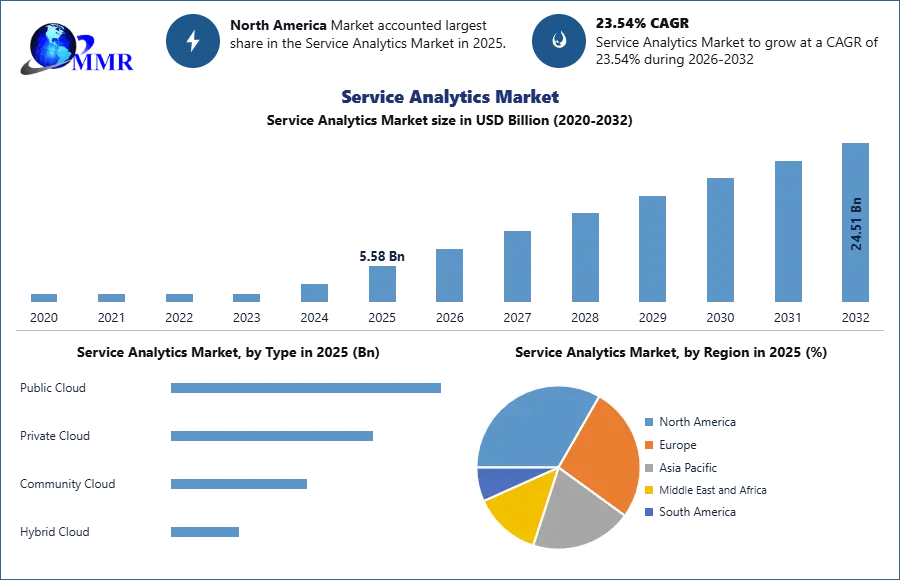

The Global Cloud Management for the OpenStack Market was valued at USD 5.58 billion in 2025 and the total market is forecasted to grow at a CAGR of 23.54% from 2026 to 2032, reaching nearly USD 24.51 billion by 2032.

Overview and Scope

The global cloud management for the OpenStack market encompasses a range of technologies, solutions, and services designed to manage and optimize OpenStack-based cloud infrastructure. This market is experiencing significant growth as organizations increasingly adopt OpenStack for their cloud environments and require efficient management tools to enhance operational efficiency, resource utilization, and cost optimization. OpenStack is an open-source cloud computing platform that provides organizations with the flexibility and scalability to build and manage private and public clouds. However, effectively managing an OpenStack environment requires robust cloud management solutions handling complex tasks such as resource provisioning, workload orchestration, monitoring, and security.

The demand for cloud management solutions for OpenStack is driven by several factors. First, the rapid adoption of cloud computing across industries has resulted in the need for comprehensive management tools to optimize cloud performance and ensure seamless operations. Second, organizations are increasingly leveraging hybrid and multi-cloud environments, and OpenStack-based clouds play a crucial role in such infrastructures. There is a growing need for centralized management solutions that can seamlessly integrate with OpenStack and other cloud platforms.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Research Methodology

The primary and secondary data sources have been utilized for studying the global cloud management for the OpenStack market. The research includes a thorough examination of all factors that may affect the market, validated through primary research and evaluated to provide valuable conclusions. Variables such as inflation, economic downturns, regulatory and policy changes, and others in the market forecasts for top-level markets and sub-segments have also been factored in.

To estimate market size and forecasts, the bottom-up approach has been employed and multiple data triangulation methodologies have been utilized. Weights have been assigned to each segment based on their utilization rate and average sale price to derive percentage splits, market shares, and breakdowns. The country-wise analysis of the market and its sub-segments is based on the percentage adoption or utilization of the given market size in the respective region or country.

To identify the major players in the global cloud management for the OpenStack industry, secondary research was conducted based on indicators like market revenue, price, applications, advancements, mergers and acquisitions, and joint ventures. Also, extensive primary research has been conducted to verify and confirm crucial numbers arrived at, after comprehensive market engineering and calculations for market statistics, market size estimations, market forecasts, market breakdown, and data triangulation. Furthermore, the report offers a clear representation of competitive analysis of key players by price, financial position, growth strategies, and regional presence in the market, making it an investor’s guide.

The secondary research phase involved a thorough synthesis of existing publications across the web to gather meaningful insights on the current situation of the market, technology developments, and any other market-related information. Information has been gathered from various sources including industry and government websites, blogs, magazines, and other publications, scientific papers, journals, and publications, trade information, conference proceedings, and association publications, among others. Apart from that, global cloud management for the OpenStack industry experts across the value chain were pooled in to gather first-hand insights on the market studied, including consultants and freelancers to collaborate on assignments that requires real-time industry insights.

In addition to primary and secondary research, market surveys have also been conducted to gather qualitative insights and opinion of individuals related to the industry. The primary research methods used to prepare this report include industry expert review, personal interview, telephonic interview, collecting responses to surveys and questionnaires through email, surveys through fieldwork, and social media monitoring. Primary research has been used to validate the data points obtained from secondary research and fill the data gaps. Critical insights obtained from primary research have been used to ascertain critical market dynamics, market distribution across various segments, market entry for new companies, and insights into the competitive landscape.

Global Cloud Management for the OpenStack Market Trends

One of the prominent trends in the global cloud management for the OpenStack market, shaping its growth and development is the increasing adoption of hybrid and multi-cloud strategies. Organizations are leveraging a combination of public clouds, private clouds, and on-premise infrastructure to create hybrid cloud environments offering flexibility, scalability and cost optimization. Cloud management solutions enabling seamless integration and management of these diverse cloud environments are in high demand. Companies are looking for comprehensive cloud management platforms providing centralized control, orchestration, and automation capabilities to effectively manage hybrid and multi-cloud architectures.

Another trend in the global cloud management for the OpenStack market is the focus on DevOps and containerization. DevOps practices, which emphasize collaboration and integration between development and operations teams, are gaining momentum in the cloud management space. Organizations are adopting containerization technologies such as Docker and Kubernetes to enable efficient application deployment, scalability, and management. Cloud management solutions that support container orchestration and provide streamlined integration with DevOps tools are essential for organizations embracing these modern application development practices. There is a growing demand for cloud management solutions that offer enhanced security and compliance features. As organizations increasingly rely on cloud environments, data security, privacy, and compliance become critical considerations. Cloud management platforms that incorporate robust security measures, encryption, identity and access management, and compliance frameworks are in high demand. Organizations are seeking comprehensive solutions that address their security and compliance requirements, ensuring seamless management of their OpenStack-based clouds.

Cloud Management for the Openstack Market Dynamics

Global Cloud Management for the OpenStack Market Drivers

The global cloud management for the OpenStack market is witnessing substantial growth, primarily driven by the increasing adoption of cloud computing across industries. Organizations are leveraging the flexibility, scalability, and cost-efficiency offered by cloud environments based on OpenStack. As a result, there is a growing need for efficient cloud management solutions to optimize resource utilization, streamline workflows, and ensure seamless operations.

The rise of hybrid and multi-cloud environments is fuelling the demand for cloud management solutions for OpenStack. Organizations are adopting a combination of public and private clouds, including OpenStack-based clouds, to meet their diverse business requirements. However, managing these complex and distributed environments requires robust management tools that can effectively handle resource provisioning, workload orchestration, and integration with other cloud platforms. Cloud management solutions for OpenStack address these challenges and provide centralized control and visibility over hybrid and multi-cloud infrastructures, driving the market's growth.

Restraints

The global cloud management for the OpenStack market faces several restraints that can impact its growth trajectory. One of the significant challenges is the complexity of managing hybrid and multi-cloud environments. As organizations adopt a combination of public and private clouds, along with OpenStack-based clouds, managing these diverse infrastructures becomes increasingly complex. Ensuring seamless integration, interoperability, and efficient resource allocation across different cloud platforms require sophisticated cloud management solutions. The complexity involved in managing hybrid and multi-cloud environments can be a barrier for organizations looking to fully leverage the benefits of OpenStack-based clouds. Another restraint is the concern over data security and privacy. Addressing data security and privacy concerns is crucial for organizations to fully embrace cloud solutions and for the continued growth of the cloud management for OpenStack market.

Global Cloud Management for the OpenStack Market Opportunities

The global cloud management for the OpenStack market presents several opportunities for companies to capitalize on. Firstly, there is a growing demand for advanced automation and orchestration capabilities in cloud management solutions. As organizations strive for greater efficiency and agility in their cloud operations, automation plays a critical role in optimizing resource allocation, scaling, and application deployment. Companies that can develop innovative automation and orchestration features tailored for OpenStack environments can gain a competitive edge and capture market share.

Additionally, the integration of emerging technologies such as artificial intelligence (AI) and machine learning (ML) into cloud management solutions offers significant opportunities. AI and ML algorithms can analyse large volumes of data generated by cloud environments, identify patterns, and provide predictive insights for proactive decision-making. Cloud management solutions that leverage AI and ML capabilities can help organizations optimize resource usage, detect and prevent potential issues, and enhance overall performance. Companies at the forefront of AI-driven cloud management for OpenStack have the potential to revolutionize the market and cater to the evolving needs of organizations across industries.

Global Cloud Management for the OpenStack Market Challenges

The global cloud management for the OpenStack market faces several challenges that can impact its progress. One of the primary challenges is vendor lock-in. Organizations that adopt OpenStack-based clouds need to carefully consider their cloud management solutions to avoid vendor lock-in, which can limit their flexibility and hinder future scalability.

Choosing cloud management solutions that offer interoperability and support for multiple cloud platforms can help organizations mitigate the risk of vendor lock-in and maintain flexibility in their cloud strategies. Interoperability and standardization are also significant challenges in the cloud management for OpenStack market. While OpenStack provides an open-source platform, ensuring seamless integration and interoperability across different cloud environments and technologies remains a challenge.

Organizations often have existing IT infrastructure and legacy systems that need to be integrated with OpenStack-based clouds. The lack of standardized interfaces and protocols can hinder the smooth integration of OpenStack with other cloud platforms and existing IT systems. Efforts towards establishing industry standards and promoting interoperability are necessary to address this challenge.

Global Cloud Management for the OpenStack Market Segment Analysis

The global cloud management for the OpenStack market is segmented based on factors like deployment mode, organization size, vertical, and region. In terms of deployment mode, the market is categorized into public cloud, private cloud, and hybrid cloud. Organizations have different preferences and requirements when it comes to deploying their OpenStack-based cloud infrastructure, and the choice of deployment mode depends on factors such as data sensitivity, control, and scalability needs.

The public cloud segment is witnessing significant growth as organizations seek the agility and cost-effectiveness offered by public cloud providers. Private cloud deployments are favoured by organizations with specific security and compliance requirements, while hybrid cloud deployments provide a balance between control and scalability. Based on organization size, the market is divided into small and medium-sized enterprises (SMEs) and large enterprises. SMEs are increasingly adopting OpenStack-based cloud management solutions to benefit from the scalability and cost advantages of cloud computing. Large enterprises, with their complex IT infrastructures and diverse workloads, require robust cloud management platforms to efficiently manage OpenStack environments.

Vertical-wise, the market is segmented into various sectors such as IT and telecommunications, healthcare, retail, BFSI (banking, financial services, and insurance), manufacturing, and others. Each sector has unique requirements and challenges when it comes to cloud management, and organizations in these sectors are leveraging OpenStack-based solutions to optimize operations, enhance agility, and improve customer experiences.

Regionally, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America and Europe are mature markets with a high adoption rate of cloud technologies and established cloud management practices. The Asia Pacific region is witnessing rapid growth in the cloud management for the OpenStack market due to the increasing digital transformation initiatives, expanding IT infrastructure, and the presence of emerging economies.

Regional Analysis

The global cloud management for the OpenStack market is analysed across five major regions: North America, Europe, Asia Pacific, South America, and the Middle East and Africa. North America is expected to lead the market over the forecast period due to its mature cloud market, strong presence of major cloud providers, and early adoption of OpenStack-based solutions. The region has a well-established IT infrastructure and a high demand for cloud management platforms that offer flexibility, scalability, and control over cloud resources. Europe is anticipated to witness high growth rate in the cloud management for the OpenStack market. The region has a strong focus on digital transformation and cloud adoption across various industries. European enterprises are increasingly embracing OpenStack for cloud management to address their specific data privacy and regulatory requirements while taking advantage of the cost-efficiency and agility offered by cloud computing.

The Asia Pacific region is poised for substantial growth in the cloud management for the OpenStack market. Rapid digitalization, expanding IT infrastructure, and increasing adoption of cloud technologies by businesses in countries like China, India, and Japan are driving the demand for efficient cloud management solutions. The region offers significant growth opportunities for cloud management vendors due to the presence of emerging economies and a vast customer base. Latin America and the Middle East and Africa are expected to experience moderate growth in the cloud management for the OpenStack market. These regions are witnessing increasing cloud adoption and digital transformation initiatives across various industries. However, challenges such as limited awareness about OpenStack, infrastructure limitations, and the need for local data sovereignty may impact the pace of market growth in these regions.

Global Cloud Management for the OpenStack Market Competitive Analysis

The global cloud management for the OpenStack market is highly competitive, with a range of established players and new entrants vying for market share. The market is dynamic and constantly evolving, with players seeking to differentiate themselves through innovative solutions and expanding their product offerings. Intense competition has resulted in strategic moves such as mergers, acquisitions, and partnerships to strengthen market position and gain a competitive edge.

The barriers for entry in this market are relatively high, with specialized expertise in cloud management and knowledge of OpenStack required. Established players have strong and long term relationships with customers and possess an understanding of their needs, creating additional challenges for new entrants. Key players in the global cloud management for OpenStack market include Mirantis, Red Hat, Platform9, Canonical, and SUSE, among others. These companies are actively involved in research and development activities to introduce advanced technologies and solutions to address the evolving needs of customers.

To succeed in this competitive market, new entrants need to differentiate themselves through innovative solutions, establish strong distribution networks, and build strategic collaborations with customers and industry partners. Understanding customer requirements, adapting to changing market dynamics, and providing comprehensive cloud management solutions are essential strategies for companies looking to thrive in the global cloud management for OpenStack industry. A detailed report by Maximize provides comprehensive insights and recommendations for companies planning to enter or expand their presence in the market, including analysis of market dynamics, competitive landscape, and strategic opportunities for growth and differentiation.

Cloud Management for the OpenStack Market Scope: Inquire before buying

| Service Analytics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 5.58 USD Billion |

| Forecast Period 2026-2032 CAGR: | 23.54% | Market Size in 2032: | 24.51 USD Billion |

| Segments Covered: | by Component | Software Services Infrastructure as a Service (IaaS) Platform as a Service (PaaS) Others |

|

| by Type | Public Cloud Private Cloud Community Cloud Hybrid Cloud |

||

| by Organization Size | Small And Medium-Sized Enterprises (SMEs) Large Enterprises |

||

| by Vertical | IT And Telecommunications Healthcare Retail BFSI Manufacturing Others |

||

Cloud Management for the OpenStack Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Cloud Management for the OpenStack Market Key Players:

The captured list of leading manufacturers of Cloud management for the OpenStack Industry has been compiled after an analysis of multiple factors. It is not an exhaustive list based only on market share ranking. After a regional analysis, a competitive analysis, and other such considerations, the company profiles were selected based on a variety of factors. The comprehensive report contains additional information on the position of each company on the market from a local and global perspective.

North America

1. Cisco Systems, Inc. (US)

2. Dell Technologies (US)

3. IBM Corporation (US)

4. Mirantis (US)

5. Red Hat, Inc. (US)

6. VMware, Inc. (US)

8. Europe

1. Adaptive Computing (UK)

2. Canonical Ltd. (UK)

3. Hewlett Packard Enterprise (UK)

4. Orange (France)

5. Atos (France)

6. Indra Sistemas (Spain)

7. OVHcloud (France)

8. SAP SE (Germany)

Asia Pacific

1. Alibaba Cloud (China)

2. Tencent Cloud (China)

3. Huawei Technologies (China)

4. Fujitsu (Japan)

5. NEC Corporation (Japan)

6. Tech Mahindra (India)

7. Middle East and Africa

8. Etisalat (United Arab Emirates)

9. MTN Group (South Africa)