China Semiconductor Market – Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

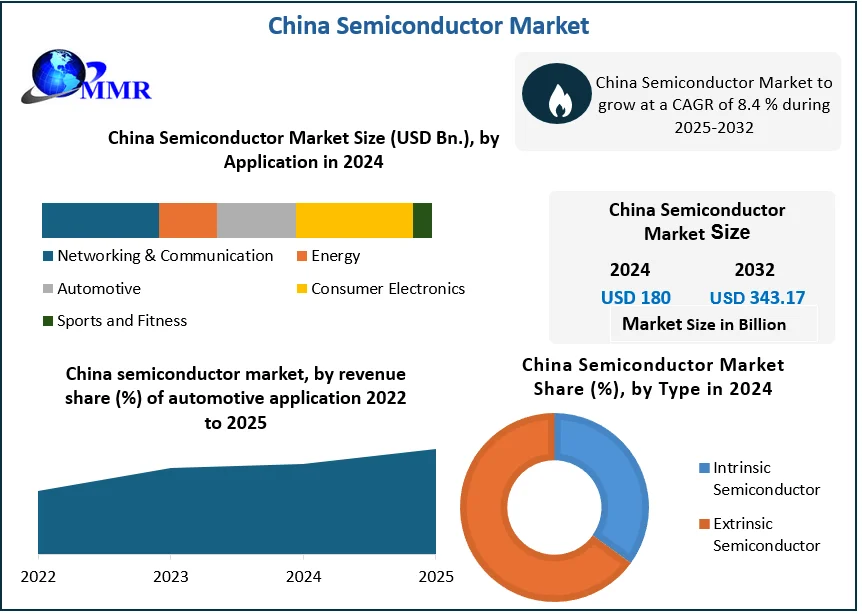

China Semiconductor Market size was valued at USD 180 Bn. in 2024, and the total China Semiconductor revenue is expected to grow by 8.4 % from 2025 to 2032, reaching nearly USD 343.17 Bn.

China Semiconductor Market Overview:

The Semiconductor encompasses the design, fabrication, and distribution of semiconductor devices such as microprocessors, memory chips, sensors, and power semiconductors that form the backbone of modern electronics.

The report defines the China Semiconductor Market as a strategically vital industry underpinning sectors like consumer electronics, automotive, telecommunications, and industrial automation. China accounted for over 34% of global semiconductor sales in 2024, showcasing abundant product availability backed by extensive domestic production and strong imports to meet rising technological demands. The supply chain remains robust due to massive investments in local fabrication plants; China’s semiconductor manufacturing capacity is projected to reach over 20% of global foundry output by the end of 2025.

East China region, especially Shanghai and Jiangsu, dominates semiconductor production due to a dense cluster of fabs and design houses. Major players of the China Semiconductor Market covered in the report include SMIC, HiSilicon, Yangtze Memory Technologies, and emerging design leaders like UNISOC. In terms of end-user contribution, consumer electronics lead with over 40% share, followed by Networking and Communication. The report comprehensively covered all these aspects, providing stakeholders with actionable insights into China’s semiconductor growth trajectory. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

China is the world’s largest manufacturing centre, which is producing 36% of the world’s electronics, such as smartphones, computers, cloud servers, and telecom infrastructure. With one-fifth of the world’s population, which is more than 1.4 billion, China is the second-largest final consumption for electronic devices embedded with semiconductors market after the U.S. The Chinese government is continuously taking serious initiatives to increase the production of semiconductors by investing US$ 150 billion from 2014 through 2030.

China Semiconductor Market Dynamics

Policy Support and Rising Tech Adoption to Drive China Semiconductor Market Growth

The China Semiconductor Market is poised for significant expansion by 2032, driven primarily by robust government initiatives like “Made in China 2025” and heavy investments in domestic semiconductor fabrication facilities. The surge in demand for advanced consumer electronics, 5G-enabled devices, AI applications, and electric vehicle (EV) further boosts market growth. Additionally, strategic partnerships with global technology leaders and the increasing adoption of IoT and smart manufacturing across industries solidify China’s position as a key player in the global semiconductor supply chain.

Start-Up Ecosystem and Advanced Tech Applications to Create China Semiconductor Market Opportunity

Substantial opportunities lie in the rapid advancement of next-generation technologies such as AI chips, quantum computing, and edge computing solutions within China’s semiconductor ecosystem. The expansion of local foundries and design houses is creating fertile ground for start-ups and research collaborations, opening doors for innovation. Moreover, rising domestic demand for high-performance chips in autonomous vehicles and renewable energy systems presents lucrative prospects for local and foreign semiconductor companies seeking to tap into China’s evolving tech landscape.

Import Dependency, Trade Barriers, and Talent Shortages to Create China Semiconductor Challenge

Despite strong growth potential, the China Semiconductor Market faces critical challenges, including heavy reliance on imported high-end semiconductor equipment and intellectual property. Escalating trade restrictions and export controls from major economies like the US pose threats to technology transfer and supply chain stability. Additionally, the shortage of skilled semiconductor engineers and talent gaps in cutting-edge chip design could hamper China’s ambition to achieve technological self-sufficiency and meet the soaring domestic demand for advanced semiconductors.

Regulatory Pressures and Geopolitical Tensions to Restrain the China Semiconductor Market

Stringent regulatory policies and geopolitical tensions remain significant restraints for the China Semiconductor Market. Heightened scrutiny over cybersecurity and national security concerns could limit foreign investment and technological collaboration. Furthermore, the capital-intensive nature of semiconductor manufacturing, coupled with fluctuating raw material costs and environmental compliance requirements, adds financial strain on local firms. These factors collectively constrain the pace at which China can bridge the technological gap with established global semiconductor leaders.

Segment Analysis of the China Semiconductor Market

Based on Type, the Extrinsic Semiconductors Segment dominated the China Semiconductor Market in 2024, because they are the backbone of nearly all modern electronic devices. Through precise doping, their electrical properties can be controlled, enabling the fabrication of highly efficient integrated circuits, transistors, diodes, and memory chips. The report highlights that China’s booming consumer electronics and telecom equipment industries heavily depend on extrinsic semiconductors to produce smartphones, laptops, servers, and 5G infrastructure. Their adaptability and crucial role in advanced chip design make them far more commercially viable than intrinsic semiconductors, which are mostly used for research and fundamental applications.

Based on Application, the Consumer Electronics segment led the China Semiconductor Market due to China’s massive domestic demand for smartphones, smart TVs, laptops, tablets, and IoT-enabled devices. The country remains the world’s largest producer and consumer of consumer electronics, with brands like Huawei, Xiaomi, and Oppo driving high-volume semiconductor consumption. The continuous upgrade cycle for personal gadgets, smart home devices, and wearables sustains robust semiconductor usage, solidifying Consumer Electronics as the dominant application area in the China Semiconductor Market.

China Semiconductor Market Competitive Analysis

The competitive landscape of the China Semiconductor Market, as outlined in the report, is characterized by a dynamic mix of established domestic giants, state-supported foundries, and emerging fabless design companies striving for technological self-reliance. Leading the market is Semiconductor Manufacturing International Corporation (SMIC) — China’s largest and most advanced foundry, which plays a critical role in local chip production amid global supply chain uncertainties.

HiSilicon, the semiconductor arm of Huawei, is a key player in advanced chip design, especially for mobile processors and AI-enabled devices, despite facing export restrictions from the US. Other notable companies include Yangtze Memory Technologies Co. (YMTC), which focuses on NAND flash memory, and UNISOC, one of China’s prominent fabless IC designers catering to the 5G and IoT segments. The report also notes that intense government funding and policies like “Made in China 2025” have spurred rapid capacity expansion and R&D investments. However, the market remains highly competitive as firms race to close the technology gap with global leaders like TSMC and Intel. Strategic alliances, domestic supply chain strengthening, and talent development are key competitive factors shaping the future of China’s semiconductor industry.

Recent key developments in the China Semiconductor Market:

• June 2025, Taiwan, Huawei & SMIC

Taiwan added Huawei Technologies and SMIC to its export control list on June 14, 2025. Taiwanese firms are now required to obtain government permits before exporting high-tech goods to these countries.

• June 2025, China, Xpeng

In June 2025, Xpeng announced that itself developed the “Turing” AI chip, capable of 2,200 TOPS is expected to be integrated into Volkswagen EVs made in China, surpassing Nvidia’s Orin X performance and marking a major milestone for domestic automotive chip design.

• June 2025, China, U.S. Commerce, Huawei

During a June 2025 U.S. congressional hearing, officials revealed that Huawei was expected to be limited to producing a maximum of 200,000 advanced AI chips in 2025. Despite this cap, the rapid narrowing of the U.S.–China technology gap was acknowledged.

Key Trends in the China Semiconductor Market

1. Acceleration of Domestic Innovation and Self-Reliance:

China’s intensified focus on achieving semiconductor self-sufficiency. Driven by trade restrictions and geopolitical tensions, Chinese companies and the government are heavily investing in local fabrication capacity, advanced chip design, and next-generation materials.

SMIC announced plans to increase its domestic production capacity to over 1.5 million 12-inch wafers per month by 2025, while government-backed funding for semiconductor R&D surpassed USD 40 billion in the last two years. This push for self-reliance is reshaping supply chains and fostering a thriving ecosystem of domestic fabs, foundries, and more than 2,000 fabless design startups across China.

2. Rising Demand for Automotive and AI-Driven Chips

Another key trend is the surging demand for high-performance semiconductors driven by the growth of electric vehicles (EVs), autonomous driving, and artificial intelligence applications.

China’s domestic demand for automotive semiconductors is expected to grow at a compound annual growth rate (CAGR) of over 15%, with the market size projected to exceed USD 20 billion by 2025. Companies like Xpeng recently unveiled an in-house AI chip capable of 2,200 TOPS, surpassing Nvidia’s Orin-X, to power their next-generation autonomous vehicles. Such breakthroughs illustrate how the automotive and AI chip segments are emerging as high-growth pillars within China’s semiconductor industry.

China Semiconductor Market Scope: Inquire before buying

| China Semiconductor Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 180 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 8.4% | Market Size in 2032: | USD 343.17 Bn |

| Segments Covered: | by Type | Intrinsic Semiconductor Extrinsic Semiconductor |

|

| by Application | Networking & Communication Energy Automotive Consumer Electronics Sports & Fitness |

||

China Semiconductor Market Key Players are:

East China:

1. SMIC (Semiconductor Manufacturing International Corporation)

2. HiSilicon (Huawei Technologies)

3. Huahong Group

4. Yangtze Memory Technologies Co. (YMTC)

South China:

1. UNISOC

2. ZTE Microelectronics

North China:

1. TSINGHUA UNIGROUP

2. China Electronics Corporation (CEC)

FAQs:

1. What is the market size of the China Semiconductor Market by 2032?

Ans. The market size of the China Semiconductor Market by 2032 is USD 343.17 Bn.

2. What is the growth rate of the China Semiconductor Market?

Ans: The China Semiconductor Market is growing at a CAGR of 8.4% during the forecasting period 2025-2032.

3. What segments are covered in the China Semiconductor market?

Ans: China Semiconductor Market is segmented into Type, Application.

4. Who are the key players in the China Semiconductor market?

Ans: The important key players in the China Semiconductor Market are Semiconductor Manufacturing International Corporation, Fujian Jinhua Integrated Circuit, NXP Semiconductors (Guangdong) Co., Ltd, HiSilicon Technologies CO., Ltd, Infineon Technologies (China) Co., Ltd, ON Semiconductor Corporation (China), Jiangsu Changjing Electronics Technology, Will Semiconductor Co, Hejian Technology Corporation and Others.

5. What is the study period of this market?

Ans: The China Semiconductor Market is studied from 2025 to 2032.