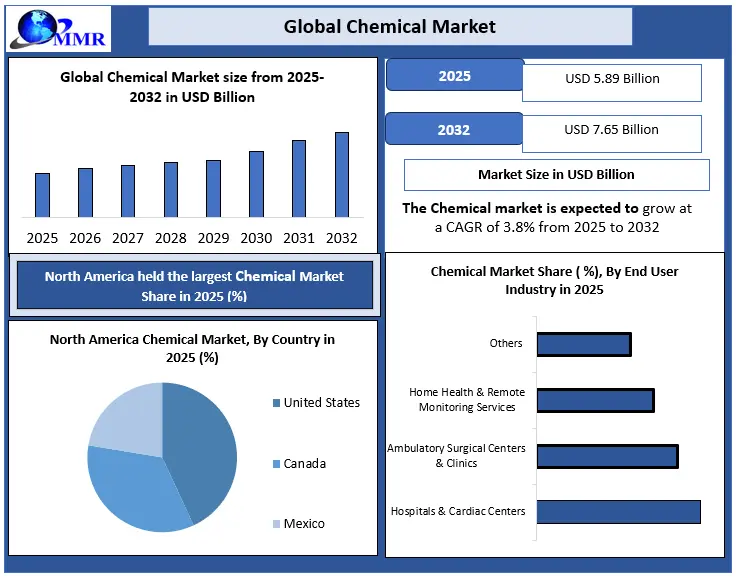

Global Chemical Market Size, Share, Trends & Forecast (2026–2032) – Valued at USD 5.89 Billion in 2025, Projected to Reach USD 7.65 Billion by 2032 at a CAGR of 3.8%

Overview

The Global Chemical Market, valued at USD 5.89 billion in 2025, is forecast to reach USD 7.65 billion by 2032, expanding at a steady CAGR of 3.8% through the forecast period. Chemicals are the invisible backbone of modern industrial civilization — from the polymer inputs shaping automotive light weighting to the sub-ppb-grade solvents enabling next-generation semiconductor fabrication.

Chemical Market Overview

The chemical industry underpins global manufacturing, enabling production across plastics, pharmaceuticals, fuels, electronics, specialty coatings, agrochemicals, and consumer care — collectively supporting over 85% of industrial supply chains worldwide. Chemical production is inherently capital- and energy-intensive; large-scale integrated plants typically require utilisation rates above 80% to maintain viable fixed-cost absorption. A structural shift is now underway: intensifying focus on sustainable chemistry, regulatory-driven reformulation, and high-purity grade requirements is fundamentally reshaping procurement strategy and production investment decisions across commodity, specialty, and performance chemical segments globally. The chemical market size, growth trends, and forecast analysis indicate a gradual transition toward higher-value segments, supported by evolving industrial demand patterns and regulatory-driven innovation.

Chemical Market Key Insights

- Utilisation & Cash-Cost Discipline: Large integrated chemical assets target 85–92% run rates; unplanned downtime beyond 10–15 days/quarter materially disrupts derivative balance and contract service levels.

- Energy & Carbon Economics: Energy represents 25–40% of variable production cost in steam-cracking and chlor-alkali chains; Scope 1–3 disclosure with third-party verification is now actively priced into supplier selection.

- Shift to High-Spec Grades: Electronics, battery, and pharma chains are tightening impurity thresholds to sub-10 ppb — driving 12–24 month qualification cycles and structural supplier lock-in.

- Supply Chain Reconfiguration: Buyers are mandating dual-sourcing (2+ qualified suppliers) and regional hubs; safety stock for critical intermediates has risen to 6–10 weeks from a pre-disruption norm of 2–4 weeks.

- Portfolio & Capex Strategy: Producers are prioritising 3–7% throughput uplift via debottlenecking and digital process control — delivering 18–36 month payback versus 5–8 years for greenfield builds.

To know about the Research Methodology :- Request Free Sample Report

Chemical Market Strategic Lens: From Volume Game to Value Engineering

The global chemical market is no longer a pure scale-driven industry. While historically dominated by volume expansion and feedstock advantages, the current phase reflects a clear transition toward value engineering, where margins are increasingly determined by formulation complexity, regulatory compliance, and application specificity.

• Commodity-driven growth is stabilizing, while specialty chemicals are driving margin expansion and customer stickiness

• Buyers are shifting from price-based sourcing to performance-based procurement, especially in electronics, pharma, and energy applications

• Integration across upstream and downstream value chains is becoming a key differentiator for large chemical producers

This shift is gradually redefining competitive advantage—from cost leadership to capability leadership.

Executive Insight: What Is Changing for Industry Leaders?

For chemical manufacturers and investors, the market is entering a phase where operational efficiency alone is no longer sufficient. The focus is shifting toward:

• Portfolio optimization toward high-margin specialty segments

• Investment in sustainable and low-carbon chemical production

• Strengthening regional supply chains to reduce dependency risks

• Digitalization of production for yield improvement and cost control

Companies that fail to adapt to this transition risk being locked into low-margin commodity cycles, while leaders are increasingly positioning themselves around innovation, compliance, and long-term resilience.

Demand Shift Analysis: Where Is Real Growth Coming From?

Growth in the chemical market is becoming increasingly concentrated in specific high-impact sectors rather than broad-based expansion.

• Electronics and semiconductor manufacturing require ultra-high purity chemicals, driving premium pricing

• Renewable energy and battery supply chains are increasing demand for advanced materials and specialty formulations

• Construction and infrastructure continue to provide baseline volume demand, particularly in emerging economies

• Consumer-driven demand is shifting toward eco-friendly and bio-based chemical products

This indicates a transition from volume-led demand to application-driven growth pockets.

Chemical Market Trend: Transition Toward High-Value, Sustainable and Performance Chemicals

A fundamental shift is underway in the chemical market, where producers are moving away from margin-volatile bulk chemicals toward specialty, performance-driven, and sustainable product portfolios. This transition is driven by the need for earnings stability, regulatory compliance, and increasing demand for application-specific formulations across electronics, energy storage, and advanced manufacturing sectors.

• Specialty and performance chemical plants enable 30–50% higher formulation flexibility, supporting customized industrial applications

• Sustainability-linked chemicals now require life-cycle carbon tracking, third-party audits, and traceability compliance, extending qualification cycles by 6–12 months

• Increasing investments are directed toward debottlenecking and process optimization, rather than greenfield expansions, improving yield efficiency and cost control

Strong Downstream Industrial and Manufacturing Demand

Sustained demand from construction, automotive, packaging, electronics, water treatment, and consumer goods industries continues to underpin chemical market growth, where chemicals serve as non-substitutable input materials across both direct and indirect manufacturing processes.

• Large chemical complexes supply multiple downstream derivative units, supporting continuous demand even during industrial slowdowns.

• Electronics, semiconductor, and battery supply chains require ppm- and ppb-level purity standards, increasing dependency on qualified chemical suppliers.

• Urbanisation and infrastructure activity sustain demand for polymers, coatings, adhesives, and construction chemicals, with long project lead cycles improving demand visibility.

Persistent Overcapacity and Structural Margin Pressure Constraining Chemical Market Growth

The global chemical market continues to face structural challenges due to prolonged overcapacity in commodity chemical chains, particularly in olefins, aromatics, and basic intermediates, which suppress pricing power and delay margin recovery.

• Commodity chemical facilities typically require high utilisation rates (above 80%) to achieve stable unit economics; sustained operation below this threshold erodes profitability

• Oil-based producers face increasing cost disadvantages compared to gas-based producers, impacting export competitiveness

• High fixed costs, energy intensity, and regulatory compliance expenses limit operational flexibility, prolonging supply-demand imbalances

Chemical Market Segment Analysis

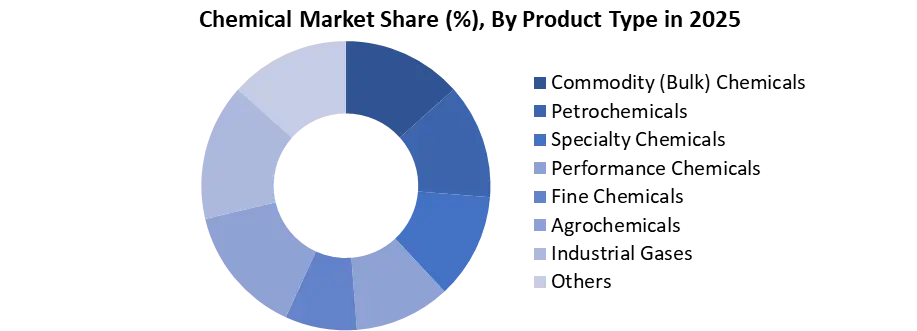

By Product Type, the market is segmented into Commodity (Bulk) Chemicals, Petrochemicals, Specialty Chemicals, Performance Chemicals, Fine Chemicals, Agrochemicals, Industrial Gases, and Others. Commodity (bulk) chemicals held the largest share of the chemical market in 2025, driven by their critical role as foundational inputs across industries such as plastics, construction, automotive, textiles, and packaging.

• Average operating rates across large-scale commodity chemical plants typically range between 65%–80% during normal market cycles — below the 85–92% run rates targeted by fully integrated chemical complexes — reflecting the margin sensitivity inherent to bulk chemical production economics. A single world-scale steam cracker supports multiple downstream derivative units, significantly enhancing throughput efficiency

• Commodity chemicals account for the majority of feedstock consumption entering polymers, resins, and intermediates globally

• Production is highly integrated, with continuous processes often exceeding 90% of installed capacity

By Chemical Category, the market is segmented into Organic Chemicals, Inorganic Chemicals, Bio-based Chemicals, and Others. Organic chemicals dominate the chemical category in 2025, forming the backbone of modern chemical manufacturing due to their carbon-based structures and versatility across industrial applications. These chemicals underpin petrochemicals, polymers, solvents, surfactants, agrochemical intermediates, and specialty formulations.

• Organic chemical pathways consume over 90% of global petrochemical feedstocks, including naphtha, ethane, propane, and aromatics.

• The majority of chemical reactions in industrial plants involve organic synthesis, cracking, reforming, or polymerisation processes.

• Large integrated complexes process millions of tons per year of organic intermediates, feeding plastics, fibers, coatings, and elastomers.

• Organic chemical facilities typically operate at higher utilisation consistency than inorganic speciality units due to steady downstream demand.

Chemical Market Regional Insights

Asia Pacific dominated the global chemical market size in 2025 and is expected to maintain its leadership during the forecast period (2026–2032), supported by strong manufacturing infrastructure, downstream integration, and large-scale commodity production.

• The region hosts the highest concentration of chemical production chains, including ethylene, propylene, and aromatics

• Trade exposure risks remain elevated, with tariffs on exports (notably U.S.–China trade dynamics) impacting competitiveness

• Nearly 50% of regional chemical companies face negative credit outlooks, reflecting overcapacity and pricing pressure

• Around one-third of producers operated with high leverage in 2025, limiting expansion capabilities

• India demonstrates stronger utilisation rates due to robust domestic demand, while export-driven markets such as Taiwan face lower utilisation levels

Chemical Market Regulatory frameworks

Regulatory frameworks such as REACH (Europe), TSCA (U.S.), and global GHS standards are increasingly influencing chemical production and consumption patterns. Compliance requirements related to emissions, toxicity, and environmental impact are directly accelerating the adoption of low-VOC, bio-based, and high-purity chemicals, thereby reshaping demand dynamics across industries such as pharmaceuticals, electronics, and consumer goods.

Market Reality Check: Structural Risks That Cannot Be Ignored

Despite stable growth projections, the chemical market continues to face structural risks that could impact profitability:

• Persistent overcapacity in commodity chemicals limiting pricing power

• Volatility in feedstock prices linked to crude oil and natural gas markets

• Increasing regulatory costs impacting production economics

• Geopolitical trade disruptions affecting global supply chains

These factors are expected to create margin pressure cycles, particularly for non-integrated and commodity-focused players.

Chemical Market Competitive Landscape

The Chemical Market Competitive landscape is moderately consolidated, led by global players operating across commodity chemicals, speciality chemicals, and petrochemicals, competing on scale, integration, and compliance capabilities. Key companies focus on capacity optimisation, speciality portfolio expansion, sustainable chemistry, and regional manufacturing hubs to strengthen positioning. Intense competition exists between integrated producers and niche speciality players, driven by regulatory compliance, feedstock security, pricing efficiency, and end-use demand diversification. The global chemical market remains innovation- and efficiency-driven across regions.

Recent Developments

• December 2025 – At the 19th GPCA Annual Forum in Bahrain, SABIC CEO Abdulrahman Al-Fageeh called for intensified regional and global strategic partnerships across the petrochemicals sector, underscoring collaboration as a core lever for sustainability, production efficiency, and long-term industrial resilience across GCC and global markets.

• September 2024 – BASF announced a significant restructuring to divest non-core businesses — including agrochemicals, battery materials, coatings, and environmental catalysts — while refocusing capital on core chemicals and sustainable materials. The plan targets USD 2.3 billion in annual cost savings by 2026.

Chemical Market Scope: Inquire before buying

| Chemical Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 5.89 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 3.8% | Market Size in 2032: | USD 7.65 Bn. |

| Segments Covered: | by Product Type | Commodity (Bulk) Chemicals Petrochemicals Specialty Chemicals Performance Chemicals Fine Chemicals Agrochemicals Industrial Gases Others |

|

| by Chemical Category | Organic Chemicals Inorganic Chemicals Bio-based Chemicals Others |

||

| by Manufacturing Process | Continuous Process Chemicals Batch Process Chemicals Semi-Batch Process Chemicals Others |

||

| by Functionality | Adhesives & Sealants Coatings & Paints Catalysts Additives Surfactants Others |

||

| by End-Use Industry | Construction & Infrastructure Automotive & Transportation Packaging (Rigid & Flexible) Consumer Goods & Home Care Pharmaceuticals & Healthcare Agriculture Electronics & Semiconductors Others |

||

| by Distribution Channel | Direct Sales Chemical Distributors Contract Manufacturing Supply Online Others |

||

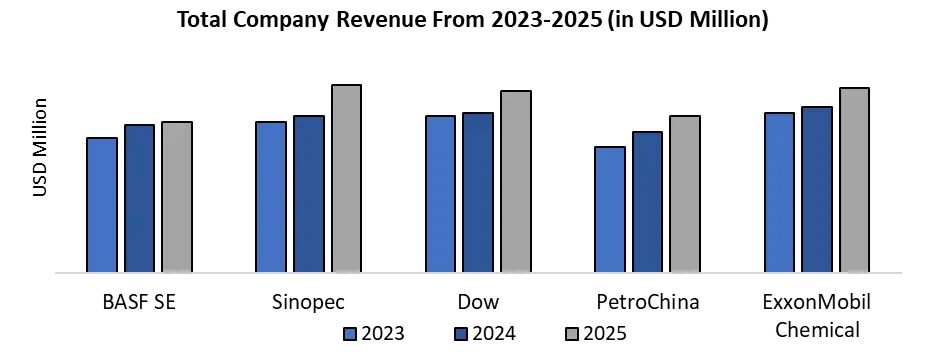

Chemical Key Players area:

1. BASF SE

2. Sinopec

3. Dow

4. PetroChina

5. ExxonMobil Chemical

6. SABIC (Saudi Basic Industries Corporation)

7. LG Chem

8. LyondellBasell Industries

9. Ineos Group

10. Linde plc

11. Air Liquide

12. Formosa Plastics Corporation

13. Wanhua Chemical Group

14. Mitsubishi Chemical Group

15. Shin-Etsu Chemical

16. Evonik Industries

17. Indorama Ventures

18. Covestro

19. Toray Industries

20. Sumitomo Chemical

21. Braskem

22. DSM-Firmenich

23. DuPont

24. Chevron Phillips Chemical

25. Sibur

26. Yara International

27. Arkema

28. Eastman Chemical

29. Quaker Houghton

Frequently Asked Questions

1) What are the growth drivers for the Chemical Market?

Answer: The chemical market is supported by broad-based downstream demand (construction, automotive, packaging, electronics, water treatment, consumer goods) and the industry’s role as a core input across >85% of global manufacturing supply chains.

2) What are the major restraints for the growth of the Chemical Market?

Answer: Key restraints include persistent overcapacity in commodity chains (olefins/aromatics/basic intermediates), causing margin pressure and weak pricing power, alongside high fixed-cost structures.

3) Which region dominated the global Chemical Market in 2025?

Answer: Asia Pacific dominated the market in 2025, driven by the highest concentration of large-scale commodity chains (ethylene/propylene/aromatics) and deep downstream integration across polymers and intermediates. However, the region also carries elevated trade/credit risk exposure (e.g., tariff-led competitiveness pressure on exports) and varying utilisation profiles—India trending stronger on domestic demand while more export-dependent hubs face lower utilisation in select chains.

4) What is the expected market size and growth rate of the Chemical Market?

Answer: The Chemical Market was valued at USD 5.89 billion in 2025 and is projected to grow at a CAGR of 3.8%, reaching USD 7.65billion by 2032, supported by rising downstream demand, a higher value-added speciality mix, and increasing compliance-driven adoption of advanced formulations.

5) What segments are covered in the Chemical Market report?

Answer: The report covers segmentation by: Product Type, Chemical Category, Manufacturing Process, Functionality, End-Use Industry, Distribution Channel and Region.