CF & CFRP Market Size by Precursor Type, Source, Resin Type, Manufacturing Process, End-Use Industry, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

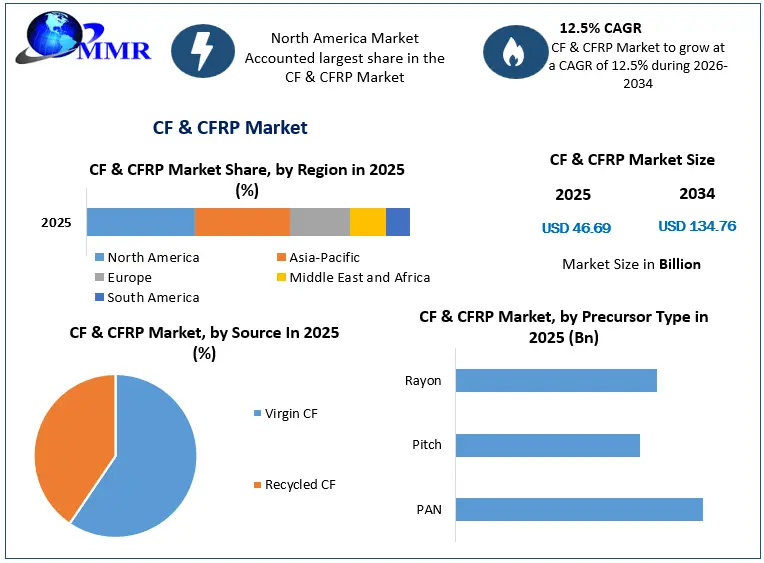

The CF & CFRP Market size was valued at USD 46.69 Billion in 2025 and the total CF & CFRP revenue is expected to grow at a CAGR of 12.5% from 2026 to 2034, reaching nearly USD 134.76 Billion.

CF and CFRPs are widely utilized in industries like aerospace, automotive, rail transport, infrastructure, and renewable energy due to their lightweight characteristics. CFRPs, specifically composed of carbon fiber incorporated into a polymer matrix, offer exceptional strength-to-weight ratios, making them highly desirable for various applications. They are well-suited for applications that demand superior strength, stiffness, reduced weight, and exceptional fatigue resistance. In comparison to aluminum and steel, carbon fiber offers approximately ten times higher specific strength (depending on the type of fiber utilized).

CFRPs have been effectively utilized in the aerospace, automotive, rail transport, marine, and wind energy sectors for over fifty years. In aerospace, the Airbus A350 and Boeing 787, the latest long-range aircraft, have extensively integrated CFRPs into their airframes, constituting more than 50% of the overall weight. In the automotive sector, carbon fibers offer advantages in reducing vehicle weight and enhancing performance, particularly for structures like body panels, roofs, and floor components where stiffness is crucial. the In wind turbine applications, the superior specific modulus of carbon fibers compared to E-glass fibers allows for longer and slimmer blades, resulting in improved aerodynamic performance. As a result, the growing demand for CF and CFRPs across various industries is driving the growth of the CF and CFRP market.

The global CF & CFRP market has been heavily affected by the COVID-19 pandemic, leading to a decrease in the demand for carbon fibers and their composites. This decline can be attributed to various factors, including grounded commercial aircraft resulting in reduced domestic and international travel as well as limitations on sporting activities. The significant decrease in airplane orders directly impacted the demand for composite materials in the aerospace industry. Leading carbon fiber suppliers like Toray and Hexcel experienced a sharp decline in sales as a consequence. Specifically, the aerospace sector witnessed a substantial reduction of approximately 30% in global carbon fiber consumption.

CF & CFRP Market Growth and Share Analysis

To know about the Research Methodology :- Request Free Sample Report

CF & CFRP Market Dynamics:

High demand for Next-Generation Single-Aisle Aircraft

The deployment of Carbon Fiber (CF) and Carbon Fiber Reinforced Polymer (CFRP) in aircraft machinery/ components and constructions is increasing rapidly all across the world. The demand for CF and CFRP is driven by their superior strength-to-weight ratio, which exceeds that of traditional metals. The increasing need for these composites in manufacturing aircraft components like wings, elevators, ailerons, engine nacelles, vertical stabilizers, and floor beams is anticipated to fuel the growth of the CF and CFRP market.

To undertake new projects in manufacturing next-generation single-aisle regional aircraft, aircraft manufacturers are engaging in consolidation efforts, further strengthening their position in the industry. Single-aisle aircraft are expected to dominate new aircraft deliveries, accounting for the largest market share during the forecast period. These aircraft are estimated to meet approximately 70% of the future commercial aircraft demand. As a result, there is expected to be a surge in carbon fiber demand originating from the production of next-generation single-aisle aircraft.

Growing adoption of carbon fiber in 3D printing

3D printing technology revolutionizes the manufacturing process by utilizing a digital model to print three-dimensional objects layer by layer. It offers various advantages, including the ability to print multiple objects quickly and without the need for extensive equipment setup. Carbon fibers have found their application in 3D printing due to their superior strength and rigidity compared to traditional metallic materials. The content and orientation of carbon fiber can be precisely controlled, facilitating optimization processes. 3D printing allows high-precision manufacturing of parts for industries like aerospace, automotive, and dental, by the adoption of carbon fibers. Thus, this technology is expected to present significant opportunities for market players and is expected to drive the growth of the CF & CFRP market during the forecast period.

High cost of CF & CFRP

The high cost of CF & CFRRP is expected to be the key factor restraining the CF & CFRP market growth during the forecast period. These composites still have minimal adoption across multiple end-use industries due to their expensive nature. In the automotive industry, CF & CFRP are expected to be only introduced in high-end and luxury automobiles due to the high cost. The production of CF & CFRPs requires precursor materials like PAN (polyacrylonitrile), pitch, etc. which are relatively expensive. Further, the processing of these precursor materials involves multiple steps, making them further expensive and increasing the overall cost of the CF & CFRP materials.

CF & CFRP Market Segment Analysis:

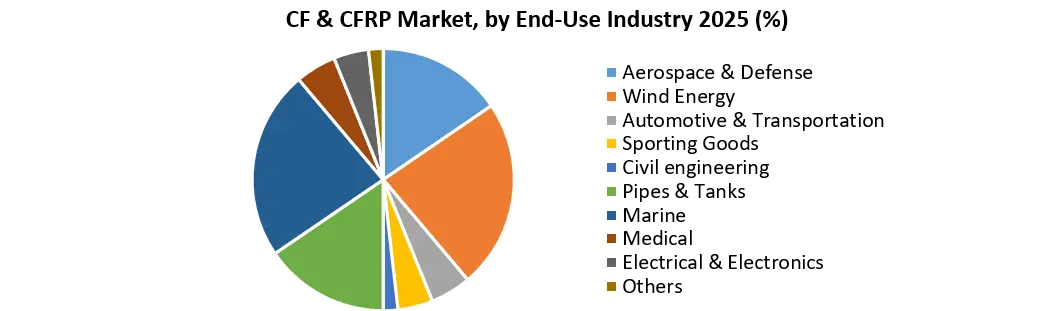

Based on End-Use Industry, the aerospace and defense segment held the largest market share in terms of revenue share in 2025 and is expected to grow at a CAGR of 12.8% during the forecast period. CF & CFRP composites widely found their usage in secondary aircraft components like ailerons, trim tabs, and rudders. CFRPs provide unique mechanical properties, including a high strength-to-weight ratio and a high stiffness-to-weight ratio.

The recent advancements in technology have led the enhancements in the properties of fibers and matrices, thereby improving the overall laminate properties. This progress has facilitated the application of CF & CFRPs in primary aircraft structures such as the fuselage and vertical tail. As a result, the aerospace and defense industry has witnessed an increasing adoption of CF & CFRPs, which has stimulated the growth of the segment.

The wind energy segment is estimated to account for the second-largest market share by 2034. CF & CFRP materials are widely utilized in the production/ manufacturing of wind turbine wings, which is expected to contribute to the production of clean energy from renewable sources. The materials offer resistance to fatigue and corrosion, increasing the lifespan of wind turbine blades, thus widely adopted in the turbines. Wind energy has become increasingly popular as a cost-effective and efficient renewable energy source. The use of wind turbines to convert kinetic energy into electricity provides clean power and contributes to the growth of the CF and CFRP market. Governments and consumers are embracing renewable energy to address environmental concerns, and with the declining costs of renewable energy production and government support, the market is experiencing significant growth. These factors are expected to drive the growth of the CF & CFRP market in the forecast period.

Wind energy has become increasingly popular as a cost-effective and efficient renewable energy source. The use of wind turbines to convert kinetic energy into electricity provides clean power and contributes to the growth of the CF and CFRP market. Governments and consumers are embracing renewable energy to address environmental concerns, and with the declining costs of renewable energy production and government support, the market is experiencing significant growth. These factors are expected to drive the growth of the CF & CFRP market in the forecast period.

CF & CFRP Market Regional Insights:

North America led the global CF & CFRP market with the highest market share of over 40% in 2025. The region is further expected to grow at a CAGR of 11.7% and maintain its growth trend during the forecast period. The strong infrastructures for various end-user industries including aerospace and defense, which are the major consumers of CF & CFRP materials in the region. The aerospace and defense sector is experiencing rapid growth owing to increased defense expenditures.

Besides that, rapid technological advancements including drones and cybersecurity, huge demand for commercial aviation, and the renewed focus on space exploration and defense technologies to combat cyber threats are the further factors supporting the sector. The strong economic dynamics of North America, particularly the USA, and Canada played a significant role in shaping the market growth. The United States, in particular, boasts one of the largest aerospace industries in terms of infrastructure and manufacturing capabilities. The increase in demand for both commercial and military aircraft, coupled with substantial increases in defense spending, drive the CF & CFRP market in the forecast period.

Asia Pacific region is expected to grow at the highest CAGR of 13.8% and offer lucrative growth opportunities for CF & CFRP manufacturers and market players during the forecast period. The increasing urbanization and higher government expenditure on infrastructure projects are expected to drive the demand for CF and CFRPs across various industries.

In particular, the use of construction composites in the construction of tunnels, bridges, and residential buildings in countries like India and China is expected to contribute to market growth. The presence of prominent construction companies in the Asia Pacific region presents significant opportunities for product adoption in the construction sector. Additionally, the growing investments in aviation, aerospace, defense, and renewable energy sectors are boosting the demand for CF and CFRPs in the region. Japan, in particular, is expected to be a significant country for the CF & CFRP market during the forecast period. Japanese companies hold a considerable share in the CF and CFRP markets, and Japan is recognized for its advanced technologies in this field. Moreover, Japan is regarded as a leader in CFRP recycling technologies at present.

CF & CFRP Market Recent Industry Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 12 January 2026 | Toray Advanced Composites | Launched a novel thermal bonding technology that bonds Carbon Fiber Reinforced Plastic (CFRP) components three times faster than conventional production methods. | This technology significantly optimizes manufacturing efficiency and high-rate output for industrial and automotive structures. |

| 11 December 2025 | Toray Industries | Secured a JEC Innovation Award alongside its strategic partners for debuting advanced technologies in composite circularity and recycling. | The milestone aids carbon fiber supply loops by addressing long-term sustainability and waste reduction mandates. |

| 28 October 2025 | Toray Industries | Developed a proprietary thermal degradation recycling technology capable of recovering carbon fiber from nonwoven fabrics while retaining 95% tensile strength and premium surface quality. | The innovation accelerates application integration in major automotive OEMs and drives localized closed-loop circular economies. |

| 14 October 2025 | Toray Group | Signed a strategic partnership agreement with Hyundai Motor Group to co-develop advanced carbon-fiber-reinforced materials for next-generation core transport vehicles. | This collaboration dramatically drives automotive lightweighting targets to optimize range parameters in electric vehicles (EVs). |

| 04 September 2025 | Teijin Carbon Europe | Achieved its first NCAMP qualification for the VARTM infusion method using non-crimp fabrics, combining its proprietary Tenax™ Dry Reinforcements with Syensqo's PRISM® epoxy resin system. | The benchmark speeds up high-volume aerospace component certification timelines and improves total supply chain security. |

| 15 July 2025 | Teijin Carbon Europe | Successfully passed its rigorous Nadcap audit, securing specialized quality certification for its high-grade carbon fiber processing lines. | This validation cements structural capability metrics required to capture long-term contract allocations in the aerospace and defense sector. |

CF & CFRP Market Scope: Inquire before buying

| CF & CFRP Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 46.69 Billion |

| Forecast Period 2026 to 2034 CAGR: | 12.5 % | Market Size in 2034: | USD 134.76 Billion |

| Segments Covered: | by Precursor Type | PAN Pitch Rayon |

|

| by Source | Virgin CF Recycled CF |

||

| by Resin Type | Thermosetting CFRP Thermoplastic CFRP |

||

| by Manufacturing Process | Lay-up Compression Molding Resin Transfer Molding Filament Winding Pultrusion Injection Molding Others |

||

| by End-Use Industry | Aerospace & Defense Wind Energy Automotive & Transportation Sporting Goods Civil engineering Pipes & Tanks Marine Medical Electrical & Electronics Others |

||

CF & CFRP Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

CF & CFRP Market, Key Players

1. Toray Industries Inc., (Japan)

2. Teijin Limited (Japan)

3. Mitsubishi Chemical Corporation (Japan)

4. Hexcel Corporation (US)

5. Solvay (Belgium)

6. SGL Carbon (Germany)

7. Hyosung Advanced Materials (South Korea)

8. Zhongfu Shenying Carbon Co., Ltd. (China)

9. Kureha Corporation (Japan)

10. DowAksa (Turkey)

11. Jilin Chemical Fiber Group Co., Ltd. (China)

12. Jiangsu Hengshen Co., Ltd. (China)

13. Aeron Composite Pvt. Ltd. (India)

14. BGF Industries (United States)

15. Crosby Composite (United States)

16. Cytec Solvay Group (Belgium)

17. Formosa Plastics Corporation (Taiwan)

18. Gurit Holdings (Switzerland)

19. AG, HC Composite (China)

20. Hindustan Composite (India)

21. Kemrock Industries and Exports Ltd. (India)

22. Nippon Graphite Fiber Corporation (Japan)

23. Park Electrochemical Corporation (United States)

24. Plasan Carbon Composites (United States)

25. Royal DSM (Netherlands)

26. SK Chemicals (South Korea)

Frequently Asked Questions:

1. What are the growth drivers for the CF & CFRP market?

Ans. The increasing adoption across multiple end-use industries is expected to be the major driver for the CF & CFRP market.

2. What is the major restraint for the CF & CFRP market growth?

Ans. The high cost of CF & CFRPs is expected to be the major restraining factor for the CF & CFRP market growth.

3. Which region is expected to lead the Global CF & CFRP market during the forecast period?

Ans. North America is expected to lead the global CF & CFRP market during the forecast period.

4. What was the Global CF & CFRP Market size in 2025?

Ans: The Global CF & CFRP Market size was USD 46.69 Billion in 2025.

5. What segments are covered in the CF & CFRP Market report?

Ans. The segments covered in the CF & CFRP market report are Precursor Type, Source, Resin Type, Manufacturing Process, End-Use Industry, and Region.