Car Body-in-White Market Size by Construction, Manufacturing Method, Material, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2029

Overview

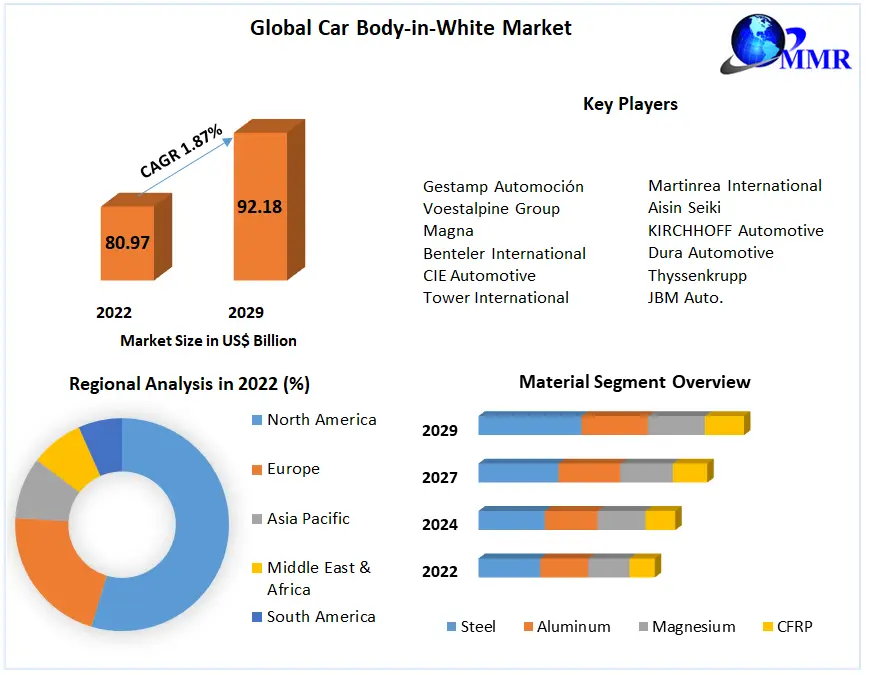

Car Body-in-White Market was worth US$ 80.97 Bn. in 2022 and total revenue is expected to grow at a rate of 1.87 % CAGR from 2023 to 2029, reaching almost US$ 92.18 Bn. in 2029.

Car Body-in-White Market Overview:

Rising global vehicle production of EVs, cars, along with a decline in the vehicle weight to match the fuel economy & emission standards are expected to increase the market. The market for the Car Body-in-White report offers a holistic assessment of the market. The report proposals a complete analysis of key sectors, trends, drivers, restraints, CP, & factors that are playing a substantial role in the market.

Car Body-in-White Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The major influences following the development of the Car Body-in-White are the rise in procurement & growth in the automobile segment worldwide. Research and Development is being done on the car body in white material to improve its strength as well as decrease the weight of the vehicle & expand its effectiveness. Also, the growing emphasis of automobile companies on vehicle weight reduction without compromising its superiority & work is expected to rise the demand for the car body in white made from lighter materials. Also, the car body in white is an essential product for all automobiles & hence, the growth of the automobile industry also improves the development of the car Body in the White Market.

Growth in Automotive Industry:

The automotive industry pushed the brakes hard in the initial months of the worldwide COVID-19 pandemic. The things initiated in China, where sales jumped 71 % in February 2020; by the month of April, sales had fallen 47 % in the US & jumped 80 % in Europe. But the business’s engines never stopped running, & cars & trucks have come roaring back. From the 3rd quarter in the year 2020 over the 1st quarter of 2022, automakers everywhere in the world have seen fast planes of manufacturing. As with many industries through geographic areas, the pandemic has carried a countless acceleration of the movements through the mobility value chain which was building before it occurred.

The automotive revenue segment will significantly rise & expand toward on-demand mobility facilities & data-driven facilities. This could make up to USD 1.5 Tr., in extra revenue potential by the year 2030, compared with around USD 5.2 Tr from old-style car sales & aftermarket products, up by 50 % from around USD 3.5 Tr in the year 2015. Total car sales will endure to raise, but the yearly growth rate is anticipated to decrease from 3.6 % over the last 5 years to about 2 % by the end of 2030. This drip will be primarily driven by macroeconomic inspirations & the increase of new mobility facilities like car-sharing & e-hailing.

A full study advises that dense zones with a large, recognized vehicle base are productive ground for these new mobility facilities, & numerous cities & suburbs of Europe & North America fit this outline. New mobility facilities may result in a drop in private car sales, but this drop is expected to be offset by improved sales in shared vehicles which need to be exchanged more often owing to advanced utilization & linked wear & tear.

Changing customer choices, tightening rules, & technical breakthroughs add up to a fundamental move in individual mobility performance. People gradually use many ways of transportation to complete their trip; goods & facilities are transported to rather than fetched by customers. As an outcome, the old-style industry model of car sales will be completed by a range of diverse, on-demand mobility keys, particularly in dense city surroundings which proactively discourage private-car usage.

Customers’ new routine of using custom-made solutions for each drive will lead to new sectors of specific vehicles manufactured for very precise needs. As an effect of this move to varied mobility answers, up to 1 out of 10 new cars sold by the year 2030 may possibly be a public vehicle, which could decrease sales of private usage vehicles.

There are certain boundaries experienced that will limit the total market development. The reasons like increasing material price for lightweight vehicles, the higher operational costs for hot stamping are restraining the market development. Similarly, technical challenges & high composite material use can lead to lesser mechanical reliability are the possible limitations hindering the total development of the Market.

In the year 2018, the APAC region was the major market share in the total car body in white market. This APAC region has seen fast YoY development, even with a slowdown in the manufacturing of cars. With ~25 Mn cars manufactured each year, China has been the key donor to the car body in white market in the Asia-Pacific region. It is the main revenue producer for the car body in white market. However, Japan is estimated to be the fastest increasing market over the forecast period with the acceptance of strict emission rules & the adoption of lightweight EVs, which makes the APAC region the major revenue market globally.

The objective of the report is to present a comprehensive analysis of the Car Body-in-White Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Car Body-in-White Market dynamics, structure by analyzing the market segments and project the Car Body-in-White Market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Car Body-in-White Market make the report investor’s guide.

Car Body-in-White Market Scope: Inquire before buying

| Global Car Body-in-White Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 80.97 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 1.87% | Market Size in 2029: | US $ 92.18 Bn. |

| Segments Covered: | by Construction | Monocoque Frame Mounted Oil |

|

| by Manufacturing Method | Cold Stamping Hot Stamping Roll Forming |

||

| by Material | Steel Aluminum Magnesium CFRP |

||

Car Body-in-White Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Car Body-in-White Market, Key players are

1. Gestamp Automoción

2. Voestalpine Group

3. Magna

4. Benteler International

5. CIE Automotive

6. Tower International

7. Martinrea International

8. Aisin Seiki

9. KIRCHHOFF Automotive

10. Dura Automotive

11. Thyssenkrupp

12. JBM Auto.

Frequently Asked Questions:

1) What was the market size of Car Body-in-White Market markets in 2022?

Ans - Car Body-in-White Market was worth US$ 80.97 Bn in 2022.

2) What is the market segment of Car Body-in-White Market markets?

Ans -The market segments are based on Construction, Material, and Manufacturing Method & Region.

3) What is forecast period consider for Car Body-in-White Market?

Ans -The forecast period for Car Body-in-White Market is 2023 to 2029.

4) Which are the worldwide major key players covered for Car Body-in-White Market report?

Ans – Gestamp Automoción, Voestalpine Group, Magna , Benteler International, CIE Automotive, Tower International, Martinrea International, Aisin Seiki, KIRCHHOFF Automotive, Dura Automotive, Thyssenkrupp , JBM Auto.

5) Which region is dominated in Car Body-in-White Market?

Ans -In 2020, Europe region dominated the Car Body-in-White Market.