C-Arms Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast (2026-2032)

Overview

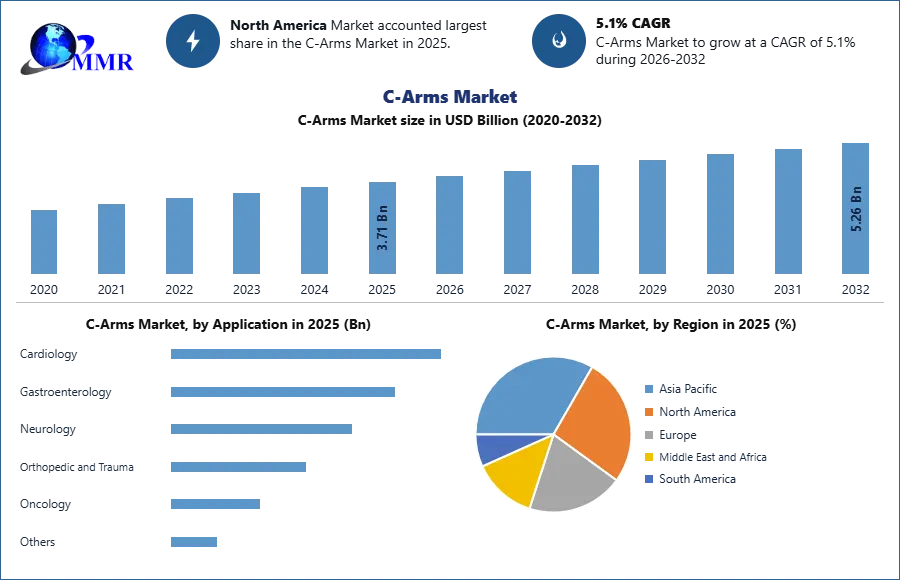

The C-Arms Market size was valued at USD 3.71 Billion in 2025 and the total C-Arms Market revenue is expected to grow at a CAGR of 5.1 % from 2026 to 2032, reaching nearly USD 5.26 Billion.

C-Arms Market Overview

C-Arms are advanced medical imaging devices shaped like a “C”. They are used in surgeries and interventions to provide real-time X-ray images. The C-Arms consists of an arm that holds an X-ray machine and a detector. These devices allow doctors to see detailed images of the patient’s body during procedures. C-arm are flexible and can be moved around the patient to capture images from different angles. They help doctors visualize the patient's anatomy, guide surgical procedures, and ensure accurate placement of medical devices. C-Arms are used in various medical fields like orthopedics, cardiology, and neurology. They are valuable tools in surgeries, angiography, pain management, and other procedures.

To know about the Research Methodology :- Request Free Sample Report

C-Arms Market Dynamics

Rising Demand for Minimally Invasive Procedure Fuels the C-Arms Market Growth

The increasing demand for minimally invasive procedures has been a significant driver for the market growth of the C-Arms market. Minimally invasive surgeries and interventions offer several advantages over traditional open surgeries, such as smaller incisions, reduced trauma, faster recovery, and shorter hospital stays. C- Arms play an important role in these procedures by providing real-time imaging guidance, enhancing accuracy and safety. Several industrial developments have contributed to the growing adoption of C-Arms in a minimally invasive procedure. The market has seen significant industrial developments, including improved image quality, enhanced imaging modes (such as fluoroscopy, DSA, and 3D imaging), and integration with other imaging modalities. C-Arms play a crucial role in facilitating these procedures by providing real-time imaging guidance to surgeons. The growing demand for minimally invasive surgeries across various medical specialties, including orthopedics, cardiology, and neurology, has boosted the adoption of C-Arm systems. C-Arms Market

Improved image quality: C-arms technology has advanced significantly, leading to improved image quality and clarity. High-resolution imaging capabilities allow surgeons to visualize anatomical structures and target specific areas with greater precision. Clearer images facilitate accurate diagnosis, surgical planning, and monitoring during minimally invasive procedures

Enhance imaging modes: Modern C-Arms offer a range of imaging modes, including fluoroscopy, digital subtraction angiography (DSA), and 3D imaging. Fluoroscopy provides real-time X-ray imaging, enabling surgeons to visualize the progress of the procedure continuously. DSA helps in visualizing blood vessels and guiding complex vascular intervention. 3D imaging provides details anatomical information, aiding surgeons in preoperative planning and intraoperative navigation. Such developments are expected to drive the C-Arms Market growth.

Compact and mobile design: The development of compact and mobile C-arms systems has them more accessible and versatile in various healthcare settings. This portable system can be easily maneuvered in operating rooms, clinics, and ambulatory surgical centers, expanding the reach of minimally invasive procedures.

Advanced software application: C-arms now feature advanced software applications that enhance procedural workflow and image analysis. For example, image fusion software allows the overlay of preoperative image fata onto real-time fluoroscopy, facilitating precise targeting of lesions or anatomical structures, additionally, image stitching and 3D reconstruction software provides comprehensive visualizations of complex anatomies.

Technological Advancements in C-Arm Systems: Enhancing Medical Imaging Capabilities for Improved Patient Care

The continuous advancements in C-Arm technology have been instrumental in driving C-Arms Market growth. Manufacturers are constantly innovating to improve image quality, enhance functionality, and introduce advanced features. Technological advancements in C-Arms systems have transformed. For instance, the integration of high-resolution detection and advanced imaging algorithms enables C-arm systems to produce detailed and sharp images, aiding in accurate diagnosis and treatment planning, additionally, the incorporation of 3D imaging capabilities allows for volumetric reconstruction anatomical structures, facilitating precise visualization and spatial assessment. Furthermore, the introduction of cone beam CT technology enables real-time 3D imaging, particularly valuable in interventional radiology and orthopedics. Improved image-guided navigation, dose optimization features, and integration with other imaging modalities further contribute to the advancement of C-arm systems, revolutionizing various medical specialties and enhancing patient care.

In addition, a recent example of technological advancement in the C-Arm industry is the introduction of Al-powered imaging and analytics systems by companies like Siemens Healthiness. These systems utilize artificial intelligence algorithms to enhance image quality, automate image analysis, and assist in procedural guidance. For example, Siemens Healthiness introduced the Cios flow C-arms system with Al-based features such as intelligent surgical imaging, which automatically adjust image quality based on the surgical scene an optimizes image contrast and brightness. The system also provides automated dose management to minimize radiation exposure. This advancement In Al technology are revolutionizing C- arm imaging by Improving efficiency, accuracy, and patient safety during surgical procedures thereby driving the C-Arms Market.

Advancements and Challenges in Enhancing Shooting Accuracy of C-Arm Machines for Medical Imaging

The shooting accuracy of C-arms machines in surgery has been a concern due to the need for multiple shots, leading to excessive X-rays exposure and increased surgery time. Scholars have attempted to enhance shooting accuracy through various methods, including changing shooting techniques, using reference materials, and improving through various methods, including changing shooting techniques, using reference materials, and improving shooting equipment. Laser lights have been employed as a cost-effective solution, but existing methods have limitations. Recent developments in laser-based positioning systems have addressed some shortcomings but still require further refinement. The author's research group has made progress in this area, obtaining utility model patents and developing prototypes. However, improvements are needed to enhance aesthetics and human-computer interaction. Future research is expected to explore AI-powered automatic locators for increased accuracy.

Restraints Impacting the Growth of the C-Arms Market

High Cost: One of the primary restraints in the C-Arms market is the high cost associated with these imaging systems. C-Arm equipment is expensive to manufacture, maintain, and upgrade, making it a significant investment for healthcare facilities. The high cost can limit adoption, particularly in developing regions with limited healthcare budgets.

Technological Complexity: C-Arm systems are sophisticated and require specialized training to operate effectively. Healthcare providers may face challenges in training their staff or recruiting professionals with the necessary expertise to operate and interpret C-Arm images. The complexity of the technology can create a barrier to widespread adoption and utilization.

Limited Availability in Rural Areas: C-Arm systems are often concentrated in urban areas or major medical centers, making them less accessible in rural or underserved regions. Limited availability can restrict the use of C-Arm technology in these areas, impacting patient access to advanced medical imaging and limiting C-Arms Market growth potential.

Potential Radiation Risks: C-Arm systems use X-rays to generate real-time images, which exposes patients and healthcare professionals to radiation. While modern C-Arm devices are designed to minimize radiation exposure, concerns about radiation risks persist. These concerns can influence the adoption of C-Arm systems and lead to cautious decision-making by healthcare providers.

Lack of Standardization: There is a lack of standardization in C-Arm technology across different manufacturers. This can create compatibility issues, interoperability challenges, and difficulties in integrating C-Arm systems with other medical equipment or healthcare information systems. The lack of standardization can impede seamless workflow integration and limit the market growth.

C-Arms Market Segment Analysis

The report covers the analysis of C-Arms Market trends in each sub-segment from 2025 to 2032 , as well as historical data and estimates for revenue growth at the global, regional, and national levels. Reports and Data have segmented the C-Arms Market based on grade, product, application, and region.

Based on Type, the mobile C-Arms held the largest C-Arms Market Share in 2025 . This segment has a wide range of uses, giving the navigation has a wide range of uses, giving the navigation system more versatility. Rising demand for this type of medical equipment in the healthcare business, particularly in the orthopedic and cardiac departments during difficult surgical operations, has significantly influenced the mobile c-arm segment's growth.

Based on Application, the market segments into cardiology, gastroenterology, neurology, orthopedics, trauma, oncology, and others. The orthopedic and trauma segments accounted for the largest share of the market in 2025. The dominance of these segments can be attributed to the high incidence of musculoskeletal disease, an increase in the number of road accidents and sports-related injuries, and a rise in the geriatric population.

C-Arms Market Regionals Insights

North America dominated C-Arms Market in 2025. This growth is due to the growth in the geriatric population, an increase in the frequency of chronic illnesses, and the advantages of reimbursement policies. The well-developed healthcare infrastructure and the implementation of cutting-edge technology drive market growth. The medical imaging devices used for real-time imaging during various surgical procedures have been experiencing significant regional variation in the forecasting period. The increasing number of minimally invasive procedures and the presence of well–establishes healthcare infrastructure in the region. The region's robust healthcare ecosystem and higher healthcare spending contribute to the widespread adoption of advanced medical imaging technologies like C-arms, consolidating North America's dominance in the market.

Turner Imaging Systems, a company specializing in medical imaging equipment, joined forces with MIS Healthcare, a prominent supplier of medical imaging equipment in the United Kingdom and Ireland in 2025. The collaboration between these two entities was established with the goal of introducing Turner Imaging Systems' SMART-C fluoroscopic mini C-arm into various diagnostic centers and other channels. The SMART-C mini C-arm is a specialized imaging device used in medical procedures to provide real-time imaging guidance. By partnering with MIS Healthcare, Turner Imaging Systems aimed to expand the availability of their SMART-C mini C-arm to a wider customer base, making it accessible to healthcare facilities and professionals throughout the U.K. and Ireland.

Asia Pacific has emerged as a promising market for C-Arms, with a significant growth rate. The region's expanding healthcare infrastructure, increasing healthcare expenditure, and growing awareness of advanced medical technologies have propelled the demand for C-Arm systems. In countries like China and India, the large patient population and the rising prevalence of chronic diseases have further augmented the market growth. Companies such as JKL Medical Devices and MNO Imaging Technologies have established a strong foothold in the Asian market by providing cost-effective C-Arm solutions tailored to the region's healthcare needs.

C-Arms Market Competitive Landscape

The competitiveness of the C-Arms Market industry is increasing due to the ultimate innovations and productions, in a fight to stay ahead in the market. Companies are focusing on improving their product offerings and increasing their distribution networks through partnerships and collaboration to get a larger portion of the market growing start-ups, mergers, and increasing trends of organic and inorganic growth is being witnessed. The key players in the market such as DMS Imaging, Koninklijke Philips N.V., Siemens Healthineers, and GE Healthcare this major key players are using strategies such as acquisition and mergers, partnerships, and investment and divestment, fueling industry growth. Furthermore, large and medium-scale companies are offering highly improved product-type portfolios and customer services. This trend is projected to positively impact the global market during the forecast period.

C-Arms Market Scope: Inquire before buying

| C-Arms Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 3.71 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.1% | Market Size in 2032: | 5.26 USD Billion |

| Segments Covered: | by Technology | 2D Imaging Technology 3D Imaging Technology |

|

| by Detector | Image Intensifiers Flat Panel |

||

| by Model Type | Floor Mounted Ceiling Mounted |

||

| by Application | Cardiology Gastroenterology Neurology Orthopedic and Trauma Oncology Others |

||

| by End User | Hospitals Diagnostic Centers Specialty Clinics Others |

||

C-Arms Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan the and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

C-Arms Key Players

1.1 DMS Imaging

1.2 Koninklijke Philips N.V.

1.3 Siemens Healthineers

1.4 GE Healthcare

1.5 Philips Healthcare

1.6 Ziehm Imaging

1.7 Hologic, Inc.

1.8 Shimadzu Corporation

1.9 Orthoscan, Inc.

1.10 Allengers Medical Systems Limited

1.11 Canon Medical Systems Corporation

1.12 Genoray Co., Ltd.

1.13 ATON GmbH

1.14 Eurocolumbus s.r.l.

1.15 Canon Medical Systems Corporation

1.16 ATON GmbH (Ziehm Imaging, Inc. and OrthoScan, Inc.)

1.17 Hologic, Inc.

1.18 DMS Imaging

1.19 Eurocolombus s.r.l.

1.20 C-Arms International

1.21 AADCO Medical Inc.

1.22 NTERMEDICAL S.r.l.

1.23 FUJIFILM Corporation

1.24 IMD Technologies

1.25 ALMAX IMAGING srl

1.26 Turner Imaging Systems

1.27 SternMed GmbH

Frequently Asked Questions:

1] What is the growth rate of the Global C-Arms Market?

Ans. The Global C-Arms Market is growing at a significant rate of 5.1 % during the forecast period.

2] Which region is expected to dominate the Global C-Arms Market?

Ans. North America is expected to dominate the C-Arms Market during the forecast period.

3] What is the expected Global C-Arms Market size by 2032?

Ans. The C-Arms Market size is expected to reach USD 3.71 Bn by 2032.

4] Which are the top players in the Global C-Arms Market?

Ans. Some of the top players operating in the C-Arms Market are DMS Imaging, Koninklijke Philips N.V., Siemens Healthineers, and GE Healthcare.

5] Which therapy has high demand in the C-Arms Market?

Ans. Minimally Invasive Procedures are in high demand in the C-Arms Market.

Table of Contents

- C-Arms Market: Research Methodology

- C-Arms Market: Executive Summary

- C-Arms Market: Competitive Landscape 3.1. MMR Competition Matrix 3.2. Competitive Landscape 3.3. Key Players Benchmarking 3.4. Market Structure 3.4.1. Market Leaders 3.4.2. Market Followers 3.4.3. Emerging Players 3.5. Consolidation of the Market

- C-Arms Market: Dynamics 4.1. Market Trends by region 4.1.1. North America 4.1.2. Europe 4.1.3. Asia Pacific 4.1.4. Middle East and Africa 4.1.5. South America 4.2. Market Drivers by Region 4.2.1. North America 4.2.2. Europe 4.2.3. Asia Pacific 4.2.4. Middle East and Africa 4.2.5. South America 4.3. Market Restraints 4.4. Market Opportunities 4.5. Market Challenges 4.6. PORTER’s Five Forces Analysis 4.7. PESTLE Analysis 4.8. Value Chain Analysis 4.9. Regulatory Landscape by Region 4.9.1. North America 4.9.2. Europe 4.9.3. Asia Pacific 4.9.4. Middle East and Africa 4.9.5. South America

- C-Arms Market: Segmentation (by Value USD Billion and Volume 000' Units) 5.1. C-Arms Market, by Types (2025-2032) 5.1.1. Mobile C-Arms 5.1.2. Fixed C-Arms 5.2. C-Arms Market, by Application (2025-2032) 5.2.1. Cardiology 5.2.2. Gastroenterology 5.2.3. Neurology 5.2.4. Orthopedic and Trauma 5.2.5. Oncology 5.2.6. Others 5.3. C-Arms Market, by Technology (2025-2032) 5.3.1. Image Intensifiers 5.3.2. Flat Panel 5.4. C-Arms Market, by Model Type (2025-2032) 5.4.1. Floor Mounted 5.4.2. Ceiling Mounted 5.5. C-Arms Market, by End User (2025-2032) 5.5.1. Hospitals 5.5.2. Diagnostic Centers 5.5.3. Specialty Clinics 5.5.4. Others 5.6. C-Arms Market, by Region (2025-2032) 5.6.1. North America 5.6.2. Europe 5.6.3. Asia Pacific 5.6.4. Middle East and Africa 5.6.5. South America

- North America C-Arms Market (by Value USD Billion and Volume 000' Units) 6.1. North America C-Arms Market, by Types (2025-2032) 6.1.1. Mobile C-Arms 6.1.2. Fixed C-Arms 6.2. North America C-Arms Market, by Application (2025-2032) 6.2.1. Cardiology 6.2.2. Gastroenterology 6.2.3. Neurology 6.2.4. Orthopedic and Trauma 6.2.5. Oncology 6.2.6. Others 6.3. North America C-Arms Market, by Technology (2025-2032) 6.3.1. Image Intensifiers 6.3.2. Flat Panel 6.4. North America C-Arms Market, by Model Type (2025-2032) 6.4.1. Floor Mounted 6.4.2. Ceiling Mounted 6.5. North America C-Arms Market, by End User (2025-2032) 6.5.1. Hospitals 6.5.2. Diagnostic Centers 6.5.3. Specialty Clinics 6.5.4. Others 6.6. North America C-Arms Market, by Country (2025-2032) 6.6.1. United States 6.6.2. Canada 6.6.3. Mexico

- Europe C-Arms Market (by Value USD Billion and Volume 000' Units) 7.1. Europe C-Arms Market, by Types (2025-2032) 7.2. Europe C-Arms Market, by Application (2025-2032) 7.3. Europe C-Arms Market, by Technology (2025-2032) 7.4. Europe C-Arms Market, by Model Type (2025-2032) 7.5. Europe C-Arms Market, by End User (2025-2032) 7.6. Europe C-Arms Market, by Country (2025-2032) 7.6.1. UK 7.6.2. France 7.6.3. Germany 7.6.4. Italy 7.6.5. Spain 7.6.6. Sweden 7.6.7. Austria 7.6.8. Rest of Europe

- Asia Pacific C-Arms Market (by Value USD Billion and Volume 000' Units) 8.1. Asia Pacific C-Arms Market, by Types (2025-2032) 8.2. Asia Pacific C-Arms Market, by Application (2025-2032) 8.3. Asia Pacific C-Arms Market, by Technology (2025-2032) 8.4. Asia Pacific C-Arms Market, by Model Type (2025-2032) 8.5. Asia Pacific C-Arms Market, by End User (2025-2032) 8.6. Asia Pacific C-Arms Market, by Country (2025-2032) 8.6.1. China 8.6.2. S Korea 8.6.3. Japan 8.6.4. India 8.6.5. Australia 8.6.6. Indonesia 8.6.7. Malaysia 8.6.8. Vietnam 8.6.9. Taiwan 8.6.10. Bangladesh 8.6.11. Pakistan 8.6.12. Rest of Asia Pacific

- Middle East and Africa C-Arms Market (by Value USD Billion and Volume 000' Units) 9.1. Middle East and Africa C-Arms Market, by Types (2025-2032) 9.2. Middle East and Africa C-Arms Market, by Application (2025-2032) 9.3. Middle East and Africa C-Arms Market, by Technology (2025-2032) 9.4. Middle East and Africa C-Arms Market, by Technology (2025-2032) 9.5. Middle East and Africa C-Arms Market, by End User (2025-2032) 9.6. Middle East and Africa C-Arms Market, by Country (2025-2032) 9.6.1. South Africa 9.6.2. GCC 9.6.3. Egypt 9.6.4. Nigeria 9.6.5. Rest of ME&A

- South America C-Arms Market (by Value USD Billion and Volume 000' Units) 10.1. South America C-Arms Market, by Types (2025-2032) 10.2. South America C-Arms Market, by Application (2025-2032) 10.3. South America C-Arms Market, by Technology (2025-2032) 10.4. South America C-Arms Market, by Technology (2025-2032) 10.5. South America C-Arms Market, by End User (2025-2032) 10.6. South America C-Arms Market, by Country (2025-2032) 10.6.1. Brazil 10.6.2. Argentina 10.6.3. Rest of South America

- Company Profile: Key players 11.1. DMS Imaging 11.1.1. Company Overview 11.1.2. Financial Overview 11.1.3. Business Portfolio 11.1.4. SWOT Analysis 11.1.5. Business Strategy 11.1.6. Recent Developments 11.2. Koninklijke Philips N.V. 11.3. Siemens Healthineers 11.4. GE Healthcare 11.5. Philips Healthcare 11.6. Ziehm Imaging 11.7. Hologic, Inc. 11.8. Shimadzu Corporation 11.9. Orthoscan, Inc. 11.10. Allengers Medical Systems Limited 11.11. Canon Medical Systems Corporation 11.12. Genoray Co., Ltd. 11.13. ATON GmbH 11.14. Eurocolumbus s.r.l. 11.15. Canon Medical Systems Corporation 11.16. ATON GmbH (Ziehm Imaging, Inc. and OrthoScan, Inc.) 11.17. Hologic, Inc. 11.18. DMS Imaging 11.19. Eurocolombus s.r.l. 11.20. C-Arms International 11.21. AADCO Medical Inc. 11.22. NTERMEDICAL S.r.l. 11.23. IMD Technologies 11.24. ALMAX IMAGING srl 11.25. Turner Imaging Systems 11.26. SternMed GmbH

- Key Findings

- Industry Recommendation