Global Blue Cheese Market by Type, Source, Texture, End-User, and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

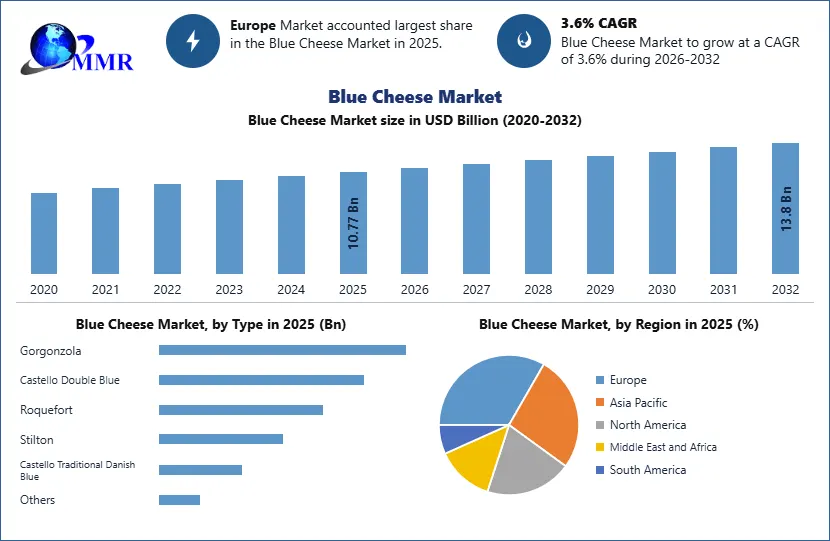

The Blue Cheese Market size was valued at USD 10.77 Billion in 2025 and the total Blue Cheese revenue is expected to grow at a CAGR of 3.6% from 2026 to 2032, reaching nearly USD 13.8 Billion.

Blue Cheese Market Overview:

The blue cheese market, characterized by its distinctive tangy flavor and iconic blue-green veining resulting from the introduction of mold cultures during the aging process, represents a specialized segment within the broader cheese industry. This particular variety of cheese, aged with molds like Penicillium roqueforti or Penicillium glaucum, has garnered attention due to its unique taste profile and its versatility in culinary applications. From high-end gastronomy to artisanal gastronomy, blue cheese has seamlessly integrated into various culinary traditions, contributing significantly to its consistent expansion. Moreover, the prevailing fascination with specialty and artisanal foods further fuels its prominence, establishing it as a noteworthy entity in the realm of fine dining. The growth of the blue cheese market is underpinned by several pivotal drivers. Additionally, the escalating demand for gourmet experiences has elevated blue cheese's reputation, as its unparalleled flavor profile imparts a sense of refinement to a spectrum of dishes. The revival of interest in time-honored and artisanal foods confers a competitive edge to blue cheese producers, capitalizing on consumers' inclination towards meticulously crafted products. The perception of blue cheese as a repository of health advantages, attributed to its nutritional richness and probiotic content, has positively influenced consumer preferences, thereby bolstering consumption patterns.

To know about the Research Methodology :- Request Free Sample Report

The landscape of the blue cheese market brims with opportunities for innovation and expansion. Industry stakeholders stand to gain from the burgeoning trend of introducing novel product iterations, including milder alternatives tailored to a wider consumer base. With the sway of globalization on culinary preferences, there exists untapped potential to introduce blue cheese to new geographical domains. The online retail sphere, too, emerges as a strategic avenue for connecting with consumers and diversifying the distribution network. Concurrently, in harmony with evolving dietary inclinations, the market observes the emergence of plant-based blue cheese substitutes, catering to the burgeoning demand for vegan and vegetarian options. The prevailing culinary discourse underscores the significance of food pairing and culinary education, a trend that augments the integration of blue cheese in various gastronomic creations and presentation styles. Additionally, the market responds to the mounting consumer emphasis on sustainability and ethical practices, entailing the assimilation of eco-conscious methodologies into the production processes. As the blue cheese market advances, the confluence of its distinct attributes and alignment with contemporary culinary trends paints a promising canvas for expansion and innovation, rendering it a compelling niche within the broader gastronomic landscape.

Blue Cheese Market Dynamics:

Blue Cheese Market Drivers

Culinary Adventurousness and Taste Exploration Propel Blue Cheese Market Expansion

The burgeoning success of the blue cheese market is deeply intertwined with the evolving predilections of consumers and their heightened inquisitiveness when it comes to embracing diverse culinary escapades. This evolution in preferences, characterized by more expansive palates and an increased willingness to experiment with gastronomic choices, has paved the way for a pronounced surge in demand for distinctive and audacious flavors, such as those offered by blue cheese. This driver finds its roots in the fundamental human inclination to embark on journeys of taste discovery, fostering a surge in the popularity of blue cheese's unmistakable tangy notes and its signature blue veining, a result of the introduction of mold cultures during the aging process.

In an epoch where sustenance has transcended its functional role to become a conduit for cultural exploration and individual expression, blue cheese finds itself in a spotlight of significance. Its remarkable capability to orchestrate a symphony of sensations for the senses renders it pivotal in this realm. This driver underscores the market's adeptness at discerning and adapting to the transformative shifts in consumer conduct and their progressively heightened affinity for intricate and unconventional flavors. In a landscape where consumers seek to titillate their taste receptors and embrace a panorama of gastronomic diversity, the blue cheese market flourishes, assuming the mantle of a culinary treasure that caters harmoniously to the contemporary thirst for adventure and novelty in the gastronomic universe.

Blue Cheese Market Restraint

Challenging Widespread Adoption Due to Strong and Unique Flavor Profile

The blue cheese market confronts a notable restraint in the form of limited acceptance arising from its distinctive and robust flavor profile. While aficionados appreciate the tangy notes and characteristic blue veins brought about by mold cultures during aging, this very uniqueness poses a hurdle to achieving mass market penetration. The pronounced taste, though a hallmark sought by enthusiasts, can prove divisive for consumers favoring milder or more conventional flavors. This restraint accentuates the necessity for strategic positioning and targeted marketing endeavors to broaden the consumer base beyond those inclined toward bold and distinctive tastes. While blue cheese undoubtedly holds allure for specific segments, its potent flavor becomes an obstacle in achieving widespread embrace, potentially necessitating innovative strategies to render it more approachable to a broader spectrum of consumers.

Blue Cheese Market Opportunities:

Rising Demand for Premium Ingredients and Food Exploration Boosts Blue Cheese Market

Among the evolving landscape of culinary preferences, characterized by a fervent pursuit of premium ingredients and diverse gastronomic experiences, the blue cheese market is poised to seize substantial growth opportunities. The ongoing trend toward gourmet dining and culinary exploration provides a favorable backdrop for the expansion of blue cheese's presence. The distinct tangy flavor and characteristic blue veins, resulting from the introduction of mold cultures, align seamlessly with the contemporary demand for intricate and memorable taste profiles. As consumers increasingly seek sophistication in their dining experiences, blue cheese's unique attributes position it as a prime candidate for meeting these expectations. Furthermore, the ascendancy of artisanal and specialty foods offers an additional propulsion to this upward trajectory. Consumers are actively seeking out ingredients that embody authenticity and high quality, and blue cheese fits squarely within this narrative. Its artisanal production methods and rich history in traditional cheese-making align perfectly with the artisanal food movement, providing an avenue for market expansion. Partnering with local producers and championing traditional crafting techniques, blue cheese can be positioned as an artisanal gem in the modern culinary landscape.

| Opportunity | Description |

| Artisanal Market Expansion | Capitalize on the growing interest in artisanal and handcrafted foods by positioning blue cheese as an authentic and high-quality product. Collaborate with local producers to highlight traditional cheese-making methods. |

| Culinary Education Initiatives | Leverage the trend of food appreciation and education by offering workshops, cooking classes, and online resources that showcase blue cheese's uses in various cuisines and dishes. |

| Premium Pairing Experiences | Partner with restaurants, wineries, and gourmet food establishments to curate premium tasting experiences that highlight the harmonious pairing of blue cheese with wines, charcuterie, and other complementary products. |

| Health-Conscious Innovation | Develop low-sodium or reduced-fat versions of blue cheese to cater to health-conscious consumers without compromising the distinctive flavor and texture. Highlight the nutritional benefits of blue cheese, such as its calcium and probiotic content. |

| Global Market Exploration |

Explore opportunities to introduce blue cheese to new international markets where gourmet and artisanal food trends are on the rise. Collaborate with local distributors and retailers to adapt to regional preferences and tastes. |

This comprehensive tabled example showcases various opportunities within the blue cheese market, illustrating strategies that capitalize on emerging trends and consumer preferences to foster growth and expansion.

Blue Cheese Market Segment Analysis:

Based on Type, the Gorgonzola segment holds a significant market share in the year 2025 and is expected to dominate during the forecast period. The dominating segment in the blue cheese market varies based on several factors, including consumer preferences, cultural influences, marketing efforts, and culinary trends. Certain types of blue cheese might dominate the market due to their historical significance, wide recognition, and versatility in various dishes. For example, in certain markets, Roquefort and Gorgonzola might have been dominant segments due to their strong cultural ties, long-standing reputation, and extensive use in regional cuisines. Castello Double Blue and similar varieties could cater to consumers seeking a more intense flavor experience. Stilton and milder blue cheeses could appeal to those who are new to blue cheese or prefer a less overpowering taste.

Blue Cheese Market, by Type (%) In 2025

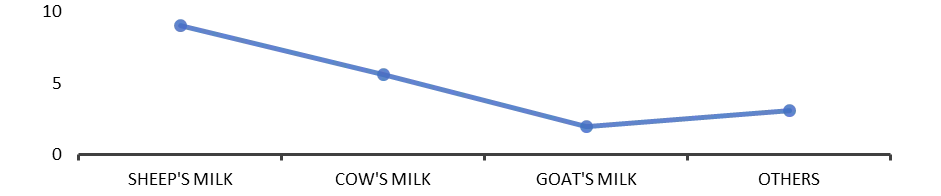

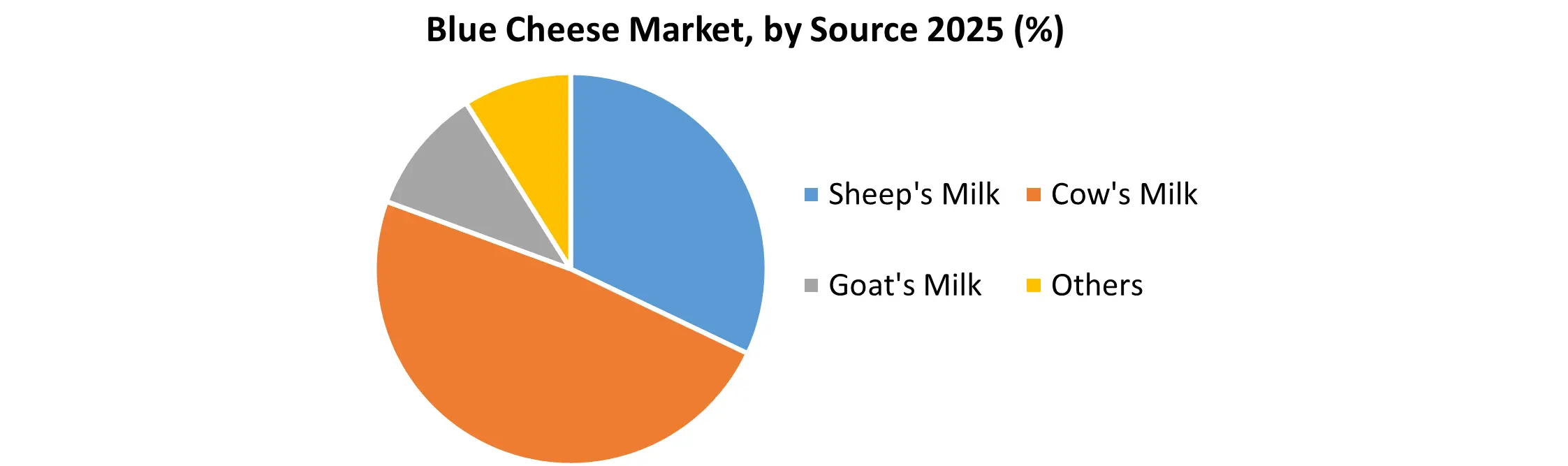

Based on Source, the Sheep's Milk segment holds a significant market share in the year 2024 and is expected to dominate during the forecast period. The dominating segment among these sources of milk varies based on a combination of factors, including historical traditions, regional availability of milk sources, consumer preferences, and marketing strategies. Historical traditions and regional practices play a significant role. For instance, in regions where sheep farming is prominent, blue cheeses made from sheep's milk like Roquefort might dominate due to their historical significance and established reputation. Similarly, in regions with a strong dairy cow industry, blue cheeses made from cow's milk might be more prevalent.

Consumer preferences also come into play. Some consumers might prefer the unique flavor profile of blue cheese made from sheep's milk, while others might lean toward the familiarity of cow's milk blue cheese. The rise of artisanal and specialty cheeses has also led to increased interest in goat's milk and other alternative milk sources, which could influence market dynamics. Marketing efforts can further shape the dominating segment. Producers might highlight the unique qualities of each type of milk, leading to shifts in consumer preferences. Sustainability concerns, animal welfare considerations, and nutritional attributes might also impact which milk sources gain prominence.

Blue Cheese Market Regional Insights:

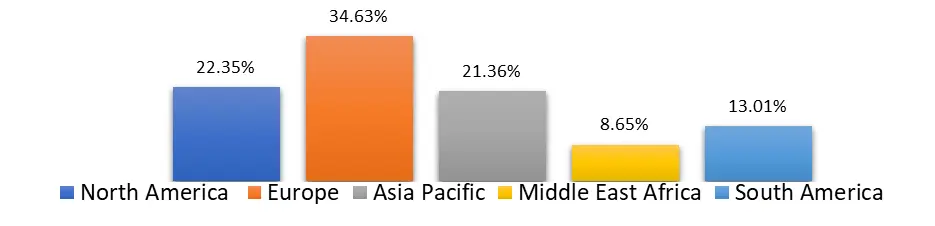

The European region holds historical and cultural significance in the blue cheese market due to its rich tradition of production and consumption. Notably, the UK is known for Stilton, a PDO-protected blue cheese with a crumbly texture and mellow flavor. France, on the other hand, boasts Roquefort, one of the world's oldest blue cheeses with an AOC status, showcasing its historical importance and unique production methods. Europe's established cheese-making heritage and export capabilities contribute to its dominance in the blue cheese market.

In North America, particularly the United States and Canada, the market for blue cheese is significant. Despite blue cheese not being as deeply rooted in culinary traditions as in Europe, the region's large population and diverse tastes drive consumption. The US, for instance, showcases a growing interest in artisanal and gourmet foods, including specialty cheeses like blue cheese. American producers have adeptly tailored traditional European recipes to create unique blue cheese varieties that cater to local preferences, contributing to North America's growing presence in the market. Meanwhile, regions like Asia Pacific, South America, the Middle East, and Africa might have smaller blue cheese markets compared to Europe and North America.

However, the evolving culinary landscape, increased access to international foods, and changing demographics have the potential to expand the market in these areas. Japan and China within the Asia Pacific region, for instance, exhibit a growing interest in foreign cuisines and gourmet ingredients, suggesting a potential rise in blue cheese consumption among specific consumer segments. As the blue cheese market's dominance is influenced by diverse factors such as consumer preferences, cultural influences, trade agreements, marketing strategies, and access to quality milk sources, it's important to note that popularity can vary even within each region. For accurate and up-to-date insights into the dominating region in the blue cheese market, consulting recent market research reports and specialized industry analyses are recommended.

Blue Cheese Market Regional Insights by % (2025)

Blue Cheese Market Scope: Inquire Before Buying

| Blue Cheese Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 10.77 USD Billion |

| Forecast Period 2026-2032 CAGR: | 3.6% | Market Size in 2032: | 13.8 USD Billion |

| Segments Covered: | by Type | Gorgonzola Castello Double Blue Roquefort Stilton Castello Traditional Danish Blue Others |

|

| by Source | Sheep's Milk Cow's Milk Goat's Milk Others |

||

| by Form | Blocks Shredded Sliced Others |

||

| by Texture | Hard Blue Cheese Soft Blue Cheese Semihard Blue Cheese Semisoft Blue Cheese |

||

| by Fat Content | Low-Fat Blue Cheese Full-Fat Blue Cheese |

||

| by Distribution Channel | Online Retail Specialty Stores Supermarket/Hypermarket Others |

||

Blue Cheese Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and the Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Blue Cheese Market, Key Players

1. Roquefort Société

2. Groupe Lactalis

3. Arla Foods

0. Saputo Inc.

5. Fonterra Co-operative Group

6. Bel Group

7. Kraft Heinz Company

8. Danish Crown

9. Bongrain SA

10.Sargento Foods Inc.

11.Point Reyes Farmstead Cheese Company

12.Castello

13.St. Agur

14.Roth Cheese

15.Montchevre-Betin, Inc.

16.Papillon

17.Maytag Dairy Farms

18.Valley Shepherd Creamery

19.Carr Valley Cheese

20.Colston Bassett Dairy

21.Cropwell Bishop Creamery

22.Cashel Blue

23.Rosenborg Castello

24.Hook's Cheese Company

25.Glengarry Fine Cheese

26.Long Clawson Dairy

27.Cropwell Bishop Creamery

28.Colston Bassett Dairy

29.Hartington Creamery

30.Websters Dairy (Saxelbye)

31.Shepherds Purse Cheeses Ltd.

32.The Cornish Cheese Co.

33.Stichelton Dairy

34.Rennet & Rind.

35.Ticklemore Cheese Dairy,

36.Oxford Blue

37.Pevensey Blue

38.The Welsh Cheese Company

39.Trefaldwyn Blue

40.Brinkworth Dairy

41.Others

Frequently Asked Questions:

1] What segments are covered in the Global Blue Cheese Market report?

Ans. The segments covered in the Blue Cheese Market report are based on Type, Source, Texture, Distribution Channel, and Region.

2] Which region is expected to hold the highest share of the Global Blue Cheese Market?

Ans. The Europe region is expected to hold the highest share of the Blue Cheese Market.

3] What is the market size of the Global Blue Cheese Market by 2032?

Ans. The market size of the Blue Cheese Market by 2032 is expected to reach USD 13.8 Bn.

4] What is the forecast period for the Global Blue Cheese Market?

Ans. The forecast period for the Blue Cheese Market is 2026-2032.

5] What was the Global Blue Cheese Market size in 2025?

Ans: The Global Blue Cheese Market size was USD 10.77 Billion in 2025.