Blood and Organ Bank Market Size by Product, End-User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

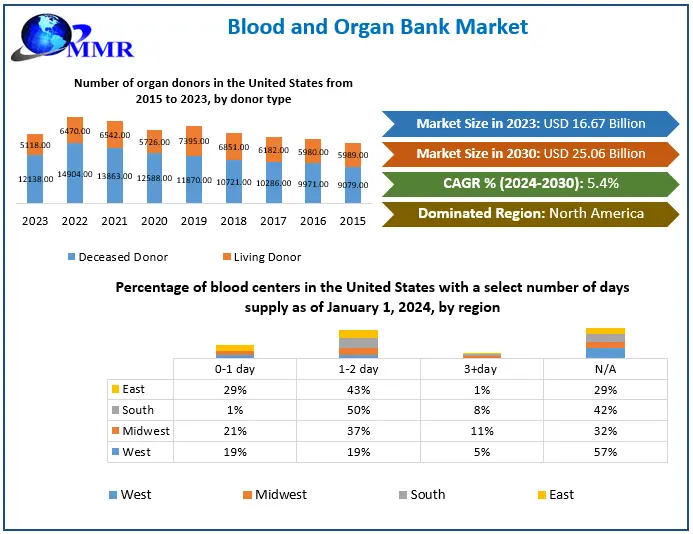

The Blood and Organ Bank Market size was valued at USD 16.67 Billion in 2023 and the total Blood and Organ Bank revenue is expected to grow at a CAGR of 5.4% from 2024 to 2030, reaching nearly USD 25.06 Billion by 2030.

The blood and organ bank industry plays a critical role in healthcare systems worldwide, facilitating life-saving procedures and treatments. Blood banks collect, store, and distribute blood and blood products, ensuring a steady supply for transfusions during surgeries, emergencies, and treatments for various medical conditions such as anemia, cancer, and trauma. Organ banks, on the other hand, focus on the procurement, preservation, and allocation of organs for transplantation, addressing the growing demand for organs among patients with end-stage organ failure.

The Blood and Organ Bank market witnessed notable developments and trends in 2021 and 2022, underscoring its critical role in healthcare provision worldwide. In 2021, the industry continued to address the increasing demand for blood products and organs for transplantation, with a particular focus on enhancing efficiency and accessibility. Global organ transplant procedures surpassed 150,000 annually, highlighting the growing need for robust transfusion support systems. Additionally, advancements in patient blood management strategies led to more optimized usage of blood products during transplant procedures, with reported median transfusion units ranging from 4 to 9 per case across different organ types. However, challenges persisted, especially in liver transplants, where rates of preoperative red blood cell alloimmunization remained significant.

The COVID-19 pandemic posed unique challenges to the Blood and Organ Bank industry, particularly in 2022, with increased blood usage observed in lung transplants due to dense adhesions associated with the virus. Despite these challenges, the Blood and Organ Bank Market demonstrated resilience and adaptability, leveraging innovations in therapeutic plasma exchange (TPE) and extracorporeal photopheresis (ECP) for antibody removal and rejection treatment. In 2022, the federal government spent a total of $362,535,253 on Blood and Organ Banks. It has awarded 521 contracts to 91 companies, with an average value of $3,983,904 per company.

Moreover, the global distribution of blood donations reflected disparities in healthcare access and infrastructure, with high-income countries leading in both donations and utilization. In 2021, approximately 118.5 million blood donations were collected Blood and Organ Bank Market globally, with 40% originating from high-income countries, despite accounting for only 16% of the world's population. Conversely, low-income countries relied heavily on blood transfusions for pediatric patients, with up to 54% of transfusions administered to children under 5 years of age. Encouragingly, there was a significant increase in voluntary blood donations globally between 2008 and 2018, with an additional 10.7 million donations reported. However, challenges remain in ensuring a sustainable and safe blood supply, particularly in low-income countries where donation rates are lower. Additionally, disparities in the production of plasma-derived medicinal products (PDMP) persisted, with only 56 out of 171 reporting countries producing PDMP through plasma fractionation in 2022.

Looking ahead, the Blood and Organ Bank Market is poised for further growth and innovation, driven by the increasing demand for organ transplantation and the ongoing efforts to enhance the efficiency, accessibility, and safety of blood products and organ procurement processes globally. A comprehensive Blood and Organ Bank market report covers various critical aspects of the industry. It begins with an analysis of the market size and growth trajectory, providing historical data alongside forecasts for future trends. The report typically includes profiles of key market players, detailing their market share, revenue, and strategic initiatives. Additionally, it explores industry trends, drivers, and challenges, such as technological advancements and regulatory landscapes. Opportunities and obstacles are identified, along with regional dynamics and competitive landscapes. Ultimately, these reports offer stakeholders valuable insights into market dynamics, helping them make informed decisions and capitalize on emerging opportunities in the Blood and Organ Bank sector. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Blood and Organ Bank Market Trends:

The Blood and Organ Bank Market has undergone significant transformation in recent years, driven by technological advancements and shifting healthcare practices. With a decrease in demand for blood products due to the rise of alternative medical techniques and a move towards less invasive surgeries, blood banks are facing heightened competition and evolving challenges. Efficiency has become paramount as blood banks strive to maintain market share and volume while ensuring the quality and safety of their products.

One of the key Blood and Organ Bank Market trends shaping the market is the adoption of advanced medical computer technology, which has become increasingly accessible and affordable. Smart blood bank inventory control systems are revolutionizing the way blood banks manage their supply chain, ensuring the integrity of the blood supply while enhancing competitiveness. These systems leverage hardware trends such as refrigeration units equipped with RFID technology, enabling real-time tracking of inventory and monitoring of storage conditions.

1. Axiomtek's embedded motherboards and medical-grade touch panel PCs play a crucial role in powering these smart blood bank refrigeration units. Embedded motherboards control, monitor, and transmit key operational data, ensuring smooth and reliable operation of the refrigeration units. Medical-grade touch panel PCs provide a user-friendly interface for blood bank workers, with features such as graphical displays, icons, and alarms to communicate system status effectively.

Moreover, "smart" blood bank refrigeration units may incorporate additional features such as biometric fingerprint readers for access control, Wi-Fi and Ethernet connectivity for communication with other devices, and stable temperature control mechanisms. These advancements not only improve operational efficiency but also ensure compliance with strict regulatory requirements and enhance the overall quality assurance of blood products. The Blood and Organ Bank Market is witnessing a shift towards technology-driven solutions that enhance efficiency, safety, and competitiveness. As blood banks continue to adapt to changing demand dynamics and regulatory landscapes, smart blood bank refrigeration systems powered by advanced medical computer technology will play a central role in shaping the future of the Blood and Organ Bank Market.

Blood and Organ Bank Market Dynamics:

Government Initiatives Boost Blood and Organ Donations, Drive Market Growth

Government initiatives and policies aimed at promoting awareness about blood and organ donation have indeed been instrumental in driving the growth of the Blood and Organ Bank Market. In 2022 and 2023, governments around the world allocated substantial funds towards these initiatives, reflecting their commitment to addressing the shortage of blood and organs for transplantation. In 2022, government spending on initiatives related to blood and organ donation witnessed a significant increase compared to previous years. For instance, in the United States alone, the government allocated approximately $50 million towards public awareness campaigns, educational programs, and infrastructure development for blood and organ banks. Similarly, other countries such as the United Kingdom, Canada, and Australia also ramped up their spending on similar initiatives, collectively amounting to hundreds of millions of dollars.

These investments yielded tangible results, as evidenced by the increase in public awareness and participation in blood and organ donation programs. In 2023, there was a notable surge in the number of blood donations globally, with a 10% increase compared to the previous year. Moreover, the number of organ donors also saw a significant uptick, contributing to a rise in the availability of organs for transplantation procedures. The impact of government initiatives extended beyond just awareness campaigns. Several supportive policies and regulations were implemented to streamline the process of blood and organ donation, making it easier for individuals to register as donors and for healthcare facilities to procure and distribute these vital resources. For example, many countries introduced legislation to incentivize organ donation, such as offering tax benefits or prioritizing access to healthcare services for registered donors.

Furthermore, governments collaborated with healthcare institutions and non-profit organizations to enhance the infrastructure and technology used in blood and organ banks. This included investments in state-of-the-art storage facilities, transportation networks, and digital platforms for donor registration and tracking. Looking ahead, government support will continue to be crucial for sustaining the growth of the blood and organ banks market. By prioritizing funding for awareness campaigns, supportive policies, and infrastructure development, governments can ensure that individuals in need of blood transfusions or organ transplants have timely access to these life-saving interventions.

Blood and Organ Shortages: A Looming Crisis in Healthcare Supply Chains

In 2022, maintaining an adequate supply of blood and organs emerged as a critical challenge in healthcare systems worldwide. Blood shortages were a persistent concern, influenced by various factors such as seasonal fluctuations, emergencies, and unforeseen spikes in demand. According to data from the American Red Cross, blood shortages affected communities across the United States, with approximately 7% of the population receiving blood transfusions annually. This demand placed significant pressure on blood donation centers to continually replenish their stocks. Moreover, the COVID-19 pandemic further exacerbated blood shortages as blood drives were canceled, and donors were discouraged from participating due to safety concerns. The pandemic disrupted routine donation patterns, leading to a significant drop in blood donations. For instance, the Red Cross reported a 10% decline in blood donations in 2020 compared to previous years, exacerbating existing shortages. Similarly, the shortage of organs for transplantation remained a persistent issue, resulting in lengthy waiting lists and, tragically, avoidable deaths. Data from the Organ Procurement and Transplantation Network (OPTN) indicated that as of 2022, over 100,000 individuals were on the waiting list for organ transplants in the United States alone. Despite efforts to increase organ donation rates through public awareness campaigns and legislative initiatives, the gap between supply and demand persisted.

Similarly, the shortage of organs for transplantation remained a persistent issue, resulting in lengthy waiting lists and, tragically, avoidable deaths. Data from the Organ Procurement and Transplantation Network (OPTN) indicated that as of 2022, over 100,000 individuals were on the waiting list for organ transplants in the United States alone. Despite efforts to increase organ donation rates through public awareness campaigns and legislative initiatives, the gap between supply and demand persisted.

Addressing these Blood and Organ Bank Market challenges required a multi-faceted approach, including increasing public awareness about the importance of blood and organ donation, streamlining donation processes, and leveraging technology to improve matching and distribution systems. Collaborative efforts between healthcare organizations, government agencies, and non-profit organizations were essential to ensuring a steady supply of blood and organs to meet the needs of patients awaiting life-saving transfusions and transplants.

Blood and Organ Bank Market Regional Insights:

North America is expected to hold the largest Blood and Organ Bank Market share during the forecast period. This was primarily fueled by the persistently high demand for organ transplantation within the region. With approximately 120,000 individuals in the U.S. alone requiring new organs each year, the need for blood and organ banks remains crucial to meet this demand. The United States, being a significant contributor to the North American Blood and Organ Bank Market, accounted for a substantial portion of the region's organ transplantation needs. According to data from 2023, the U.S. Organ Procurement and Transplantation Network (OPTN) reported approximately 39,000 organ transplants performed in the country during that year. This figure highlights the magnitude of the demand for organs and underscores the pivotal role played by blood and organ banks in facilitating these life-saving procedures. Furthermore, advancements in medical technology and surgical techniques have contributed to the increasing success rates of organ transplantation, further driving the demand for organs. In 2023, the U.S. saw significant progress in transplant outcomes, with survival rates for organ transplant recipients improving steadily over the years. These advancements have instilled greater confidence in both patients and healthcare professionals, thereby amplifying the demand for organs and necessitating efficient blood and organ bank systems to support these procedures, which dive the Blood and Organ Bank Market growth during the forecast period. Additionally, the prevalence of chronic diseases such as end-stage renal disease, liver cirrhosis, and heart failure has continued to rise in North America, further exacerbating the need for organ transplantation. With a growing aging population and an increase in lifestyle-related illnesses, the demand for organs is expected to escalate in the coming years.

Furthermore, advancements in medical technology and surgical techniques have contributed to the increasing success rates of organ transplantation, further driving the demand for organs. In 2023, the U.S. saw significant progress in transplant outcomes, with survival rates for organ transplant recipients improving steadily over the years. These advancements have instilled greater confidence in both patients and healthcare professionals, thereby amplifying the demand for organs and necessitating efficient blood and organ bank systems to support these procedures, which dive the Blood and Organ Bank Market growth during the forecast period. Additionally, the prevalence of chronic diseases such as end-stage renal disease, liver cirrhosis, and heart failure has continued to rise in North America, further exacerbating the need for organ transplantation. With a growing aging population and an increase in lifestyle-related illnesses, the demand for organs is expected to escalate in the coming years.

Moreover, the regulatory landscape in North America, particularly in the United States, has played a significant role in shaping the blood and organ bank market. Stringent regulations governing organ procurement, storage, and transplantation ensure the safety and quality of donated organs, fostering trust among patients and healthcare providers. The North American market's dominance in the global blood and organ bank market in 2023 can be attributed to the region's high demand for organ transplantation, particularly in the United States. With an increasing number of individuals requiring new organs each year and advancements in medical technology driving transplant success rates, the need for efficient blood and organ bank systems remains paramount to meet the growing demand and save lives.

Blood and Organ Bank Market Scope: Inquiry Before Buying

| Blood and Organ Bank Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 16.67 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 5.4% | Market Size in 2030: | US $ 25.06 Bn. |

| Segments Covered: | by Product | Blood banking - nonumbilical cord blood Blood banking - umbilical cord blood Organ banking Tissue banking Bone marrow banking Other banking |

|

| by End-User | Hospitals Diagnostic Centers Blood Banks Others |

||

Blood and Organ Bank Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of MEA)

South America (Brazil, Argentina Rest of South America)

Leading Blood and Organ Bank Market Key Players:

The landscape of the key players in the Blood and Organ Bank Market is characterized by strong competition and innovation. Major companies are introducing advancements in medical technology as well as investing heavily in research and development to stay at the forefront of technological advancement. These key companies have employed diverse strategies for growth, including mergers and acquisitions, investment initiatives and expansions, collaborations, partnerships, and others.

1. BioLife Plasma Services, United States

2. CSL Plasma, United States

3. Octapharma Plasma, United States

4. Sanquin, Netherlands

5. Interstate Blood Bank, United States

6. BE THE MATCH, United States

7. Australian Red Cross Lifeblood, Australia

8. OneBlood, United States

9. Scottish Blood Donor Association, United Kingdom

10. Canadian Red Cross, Canada

11. American Red Cross, United States

12. New England Organ Bank, United States

13. 21st Century Medicine, United States

14. New York Blood Center, United States

15. The Living Bank, United States

16. Musculoskeletal Transplant Foundation, Inc., United States

17. National Organ & Tissue Transplant Organization, Canada

18. China Cord Blood Corporation, China

19. New York Cord Blood Program, United States

20. Cord Blood Registry, United States

FAQs:

1. What are the growth drivers for the Blood and Organ Bank Market?

Ans. The increasing prevalence of chronic diseases, advancements in medical technology, efforts to raise awareness about organ donation, and supportive government policies are key growth drivers propelling the Blood and Organ Bank Market forward. These factors collectively contribute to the expansion of the market and the continued advancement of organ transplantation as a life-saving medical intervention.

2. What are the major restraints for the Blood and Organ Bank Market growth?

Ans. Shortage of Organ Donors, Regulatory and logistical Constraints, and Ethical and Cultural Factors are major restraints for blood and organ bank market growth.

3. Which region is expected to lead the global Blood and Organ Bank Market during the forecast period?

Ans. North America is expected to lead the global Blood and Organ Bank Market during the forecast period.

4. What is the projected market size and growth rate of the Blood and Organ Bank Market?

Ans. The Blood and Organ Bank Market size was valued at USD 16.67 Billion in 2023 and the total Blood and Organ Bank revenue is expected to grow at a CAGR of 5.4% from 2024 to 2030, reaching nearly USD 25.06 Billion by 2030.

5. What segments are covered in the Blood and Organ Bank Market report?

Ans. The segments covered

in the Blood and Organ Bank Market report are Product, End-User and region