Bearing Market Size by Technology,Application, Industry and Region - Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

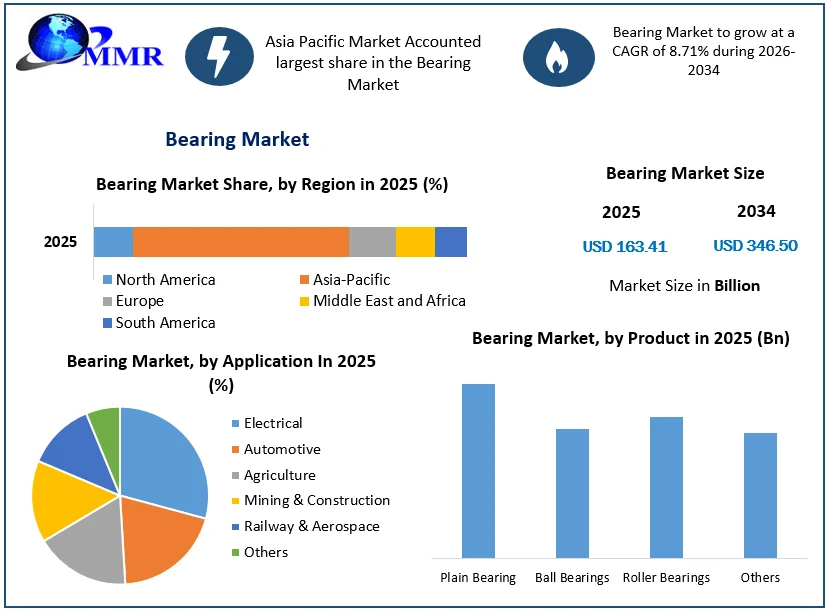

The Bearing Market size was valued at USD 163.41 Billion in 2025 and the total Bearing revenue is expected to grow at a CAGR of 8.71% from 2026 to 2034, reaching nearly USD 346.50 Billion.

Bearing Market Overview

Bearings are precision-engineered components crucial for enabling machinery to operate efficiently at high speeds and carry heavy loads with ease. They must offer reliability, durability, and minimal noise and vibration while rotating at high speeds. Found in various applications such as automobiles, airplanes, computers, and construction equipment, bearings come in different types tailored for specific purposes. The four most common types include ball bearings, cylindrical and needle roller bearings, tapered roller bearings, and spherical roller bearings. Each type possesses unique characteristics suited to different applications, ranging from low friction and high speed to medium-to-heavy loading and misalignment capabilities.

The World Bearing Association leads efforts to combat counterfeit bearings, and educational events like the Advanced Concepts of Bearing Technology conference provide insights into the latest developments in the field. Increasing adoption of industrial automation across various sectors drives demand for bearings, which are essential components in automated machinery and equipment. As industries seek to improve efficiency and productivity, the demand for bearings that can withstand high speeds and loads continues to rise. The automotive industry is a significant driver of the bearing market, as bearings are crucial components in vehicles for various applications such as engines, transmissions, wheels, and steering systems. With the expansion of the automotive sector globally, particularly in emerging markets, the demand for bearings is expected to increase and drive the Bearing Market Growth.

Bearing Market Size, Growth and Share Analysis

To know about the Research Methodology:-Request Free Sample Report

Bearing Market Dynamics

Industrial Automation Advancements to Drive the Market

The increasing demand for precision machinery across various industries, including automotive, aerospace, and manufacturing, is a primary driver for the bearing market. As industries adopt automation to enhance efficiency and productivity, the need for high-performance bearings capable of withstanding heavy loads and operating in harsh environments grows. This trend fuels the demand for advanced bearings with features like high speed, durability, and reliability.

The industrial automation landscape is evolving in 2024 with advancements such as AI, collaborative robots, and IoT integration. Digital technologies such as generative AI and digital twins enhance manufacturing efficiency, quality, and sustainability. Generative AI predicts equipment breakdowns, while 4D vision revolutionizes robot movements. AGVs and AMRs expand beyond warehouses, and speed to automation becomes crucial for competitiveness. Machine learning and predictive analytics analyze automation data for better decision-making. Companies, regardless of size, prioritize automation for thriving in the market. JR Automation, a Hitachi Group company, offers expertise in automation solutions to meet evolving industry needs.

Top Industrial Automation Trends in 2024

| Artificial Intelligence (AI) | AI is revolutionizing industrial automation by enabling machines to learn, adapt, and make decisions autonomously. It's being used to identify asset patterns and anomalies for optimizing production and reducing downtime. AI-powered solutions like South Korean startup DAIM Research's automated material handling system and Spanish startup Inovako's industrial vision are enhancing efficiency and precision. |

| Advanced Robotics | Robots are replacing workers in hazardous environments and working alongside humans. Collaborative robots (cobots) perform tasks like assembly, packaging, and machine tending. Startups like Isochronic and Botshare are offering innovative solutions for pick-and-place applications and autonomous mobile robots (AMR). |

| Industrial Internet of Things (IIoT) | IIoT is essential for connecting industrial devices and machines to collect and analyze data in real-time. Startups like VISUALYS and Akinê are developing platforms and controllers that monitor and operate various industrial systems, enhancing production, safety, and efficiency. |

| Edge & Cloud Computing | Edge computing offers real-time data processing, while cloud-based solutions simplify remote data access. Indian startup DeepBrainz Technologies and NearbyComputing are providing platforms that integrate both edge and cloud computing, aiding in real-time monitoring, data analytics, and storage. |

| Immersive Technologies | Immersive technologies like virtual reality (VR) and augmented reality (AR) are improving worker efficiency by providing additional visualization and safety measures. These technologies are being used to train workers, simulate complex tasks, and enhance collaboration. |

Continuous advancements in bearing materials, lubrication techniques, and design methodologies contribute significantly to market growth. Innovations such as ceramic bearings, smart bearings equipped with sensors for condition monitoring, and self-lubricating bearings enhance performance, reduce maintenance costs, and extend service life, thereby attracting more customers across diverse industries.

Rising Automotive Production: The automotive sector remains a significant consumer of bearings, driven by the surge in vehicle production globally. With the growing emphasis on electric and hybrid vehicles, there's a notable shift towards bearings designed for improved energy efficiency and reduced emissions. Moreover, the expansion of transportation infrastructure in emerging economies further propels the demand for bearings used in commercial vehicles and railways. As a result, this factor is expected to help the Bearing Market growth.

Growth of Renewable Energy Sector to Create Lucrative Opportunity for the Bearing Market:

promising opportunity lies in the renewable energy sector, particularly wind and solar power generation. With the global push towards sustainable energy sources, there's a growing need for bearings in wind turbines, solar tracking systems, and related equipment. Bearings capable of withstanding heavy loads, extreme temperatures, and prolonged exposure to harsh environmental conditions are essential for ensuring the reliability and efficiency of renewable energy infrastructure. Capturing this market segment requires tailored solutions and strategic partnerships to address the unique requirements of renewable energy applications, presenting a lucrative opportunity for bearing manufacturers to expand their product offerings and Bearing Market presence. The shift towards grid modernization presents a significant growth opportunity for the Bearing Industry. The U.S. electric grid is an engineering marvel with more than 9,200 electric generating units having more than 1 million megawatts of generating capacity connected to more than 600,000 miles of transmission lines. Bearings play a critical role in supporting the efficient and reliable operation of transmission lines and towers, which are essential components of the modernized grid.

The shift towards grid modernization presents a significant growth opportunity for the Bearing Industry. The U.S. electric grid is an engineering marvel with more than 9,200 electric generating units having more than 1 million megawatts of generating capacity connected to more than 600,000 miles of transmission lines. Bearings play a critical role in supporting the efficient and reliable operation of transmission lines and towers, which are essential components of the modernized grid.

Also, the adoption of digital technologies in grid modernization facilitates predictive maintenance and quick fault detection, further emphasizing the importance of reliable bearings in ensuring uninterrupted operation. As utilities and operators embrace grid modernization to accommodate renewable energy sources and efficiently manage peak demand, the demand for bearings with enhanced durability, precision, and performance characteristics is expected to surge.

Government Initiatives and Energy Policies to Fuel the Bearing Market

Governments across the region and regulatory bodies are implementing energy policies that emphasize the development of reliable and resilient power transmission systems. These policies are often aimed at reducing carbon emissions, increasing energy security, and fostering economic growth. Governments incentivize private sector investments in transmission infrastructure through grants, subsidies, or regulatory mechanisms. Such initiatives create a conducive environment for growth in the power transmission lines and towers market, as companies respond to policy-driven opportunities. In the US, the Biden Administration launched $2.5 billion fund to modernize and expand the capacity of America’s power grid.

Technological Limitations and Economic Fluctuations to Restrain the Market Growth:

Despite advancements, certain applications demand specialized bearings that may not be readily available due to technological constraints. For instance, high-speed machinery or extreme temperature environments require bearings with precise specifications, limiting market growth without corresponding technological breakthroughs. The bearing market is sensitive to economic cycles. During periods of recession or economic uncertainty, industries may delay investments in new machinery or infrastructure, leading to decreased demand for bearings. Moreover, currency fluctuations and trade tariffs can impact manufacturing costs and market competitiveness, constraining growth.

Bearing Market Segment Analysis

By Product: The Bearing Market is categorized into ball, roller, plain bearing, and other segments. Roller bearings held the largest share of revenue in 2025, and are projected to maintain their dominance while experiencing rapid growth ahead. These bearings effectively minimize rotational friction, provide support for radial and axial loads, and exhibit superior performance under heavy radial loads compared to alternatives. Their extensive adoption across diverse sectors including capital equipment, automotive, household appliances, and aerospace is poised to drive significant demand.

Additionally, the report discusses ball and other types of bearings. Ball bearings, characterized by reduced surface contact leading to friction reduction, are versatile for use with both thrust and radial loads. Their application in various automotive vehicles, from four-wheelers to two-wheelers, is steadily increasing, indicating a promising growth trajectory for this segment in the forecast period.

By Application: Based on the application, the automotive sector emerged as the dominant force in the bearing market in 2025, capturing a substantial market share. This prominence is primarily driven by the global surge in automotive production. The escalating demand for vehicles equipped with cutting-edge technological solutions is fueling increased manufacturing activity, consequently driving the need for sophisticated bearing solutions. The evolution towards highly advanced vehicles, coupled with enhanced vehicle capabilities, is significantly amplifying the demand for bearings within the automotive industry. The automotive aftermarket segment is poised for robust growth, expected to exhibit a notably higher compound annual growth rate (CAGR) throughout the forecast period. This anticipated expansion in the aftermarket segment further underlines the growing demand for bearings across the automotive landscape.

Bearing Market Regional Analysis

Asia Pacific held the largest Bearing Market share in 2025. the surge in industrialization and infrastructure development in countries like China, India, Japan, and Southeast Asian nations is driving an uptick in the demand for roller and ball bearings. These essential components find applications across diverse industries including manufacturing, automotive, aerospace, and energy. The burgeoning expansion of these sectors is directly contributing to the growth of the roller and ball bearings industry in the region.

Also, region is witnessing a pronounced shift towards automation and the adoption of advanced machinery, where roller and ball bearings play a pivotal role in ensuring precise and efficient operations, thus further fueling the industry's growth. In India, bearing import shipments totaled 6.4 million units, sourced by 27,990 importers from 51,950 suppliers, primarily from China, Germany, and Japan. Conversely, bearing export shipments reached 3 million units, sent by 31,101 exporters to 96,648 buyers, with major destinations being the United States, Germany, and China. India ranks as the world's second-largest bearing exporter, with China leading at 4,090,947 shipments, followed by India at 3,010,181, and Japan at 2,370,707 shipments.

Top Trading Partners of India for Import of Ball or Roller Bearings in 2022

| Country | Share | Value (million US$) |

| China | 42% | 553 |

| Germany | 17.5% | 230 |

| Japan | 11% | 145 |

| USA | 5.17% | 67 |

| Korea | 3.01% | 39 |

| Italy | 2.72% | 35 |

| Singapore | 2.23% | 29 |

| Thailand | 2.22% | 29 |

| France | 1.91% | 25 |

| Sweden | 1.3% | 17 |

North America is experiencing robust industrial growth across multiple sectors such as manufacturing, automotive, aerospace, and energy. Mechanical bearings are integral to these industries, facilitating smooth rotational or linear movement in machinery and equipment. The escalating demand for dependable and high-performance bearings in these sectors is a key driver for the Bearing Market growth of mechanical bearings in North America. The advancement of technologies like Industry 4.0, automation, and the Internet of Things (IoT) is accelerating the adoption of sophisticated machinery and equipment, underscoring the indispensable role of mechanical bearings in ensuring precision, efficiency, and minimized downtime in modern systems.

In Europe, Germany stands out as the Bearing Market leader in 2022 and is poised to maintain its position during the forecast period. This dominance is attributed to Germany's prominence in automotive and industrial manufacturing industries, which significantly boost the utilization of bearings within the country. Moreover, Germany is expected to exhibit the highest Compound Annual Growth Rate (CAGR) during the forecast period, propelled by extensive research and development (R&D) activities and robust manufacturing facilities.

Bearing Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 19 August 2025 | Schaeffler India | Schaeffler India inaugurated a new 16,500-square-meter manufacturing facility in Shoolagiri, Tamil Nadu, to produce high-tech bearings and chassis components. | The expansion significantly boosts localized production capacity for e-mobility solutions and advanced industrial bearings under India's "Make in India" initiative. |

| 18 March 2026 | The Timken Company | The Timken Company acquired the assets and business of Bijur Delimon International to expand its automated lubrication systems platform. | The strategic acquisition enhances Timken's presence in heavy industrial sectors such as rail, power generation, and mining to improve equipment operational efficiency. |

| 12 May 2026 | NSK Ltd. & NTN Corporation | NSK Ltd. and NTN Corporation signed a Memorandum of Understanding to integrate their global business operations under a joint holding company. | The proposed consolidation establishes one of the world's largest bearing entities with USD 11 billion in annual revenue, optimizing manufacturing scale and operational efficiency. |

| 25 June 2026 | SKF Group | SKF Group announced a strategic venture investment in startup Anferra AB to commercialize technology that recycles hazardous steel grinding sludge. | The circular innovation recovers up to 90% iron and provides up to 470 kg CO2-equivalent savings per tonne of sludge, significantly reducing environmental impact. |

| 02 July 2026 | SKF Group | SKF Group signed an agreement with Leaderdrive to establish a joint venture in China dedicated to precision transmission components and bearings for robot joints. | The collaboration accelerates SKF's market positioning in high-growth automation sectors, including industrial robotics and humanoid technology. |

Bearing Market Report Scope : Inquire before buying

| Bearing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 163.41 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 8.71% | Market Size in 2034: | USD 346.50 Bn. |

| Segments Covered: | by Product | Plain Bearing Ball Bearings Roller Bearings Others |

|

| by Type | Mounted Bearing Unmounted Bearing |

||

| by Size | 30 to 40 41 to 50 51 to 60 61 to 70 70 & above |

||

| by Application | Electrical Automotive Agriculture Mining & Construction Railway & Aerospace Others |

||

Bearing Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Bearing Market, Key Players are

The Bearing Industry is defined as the worldwide market that deals with the production and commercialization of mechanical bearings that act as devices that prevent friction between moving components. They are mainly used in applications such as the automotive industry, aerospace, railways, and heavy industry.

| Company Name | Headquarters | Core Competencies |

| The Timken Company | United States | Tapered roller bearings, engineered bearings, power transmission products, and industrial motion solutions |

| RBC Bearings Incorporated | United States | Precision bearings for aerospace, defense, industrial, and transportation applications |

| KMS Bearings Inc. | United States | Precision miniature bearings, stainless steel bearings, and custom bearing solutions |

| SKF AB | Sweden | Rolling bearings, seals, lubrication systems, condition monitoring, and industrial services |

| Schaeffler AG | Germany | INA and FAG bearings, automotive components, and industrial motion technologies |

| CW Bearing GmbH | Germany | Precision ball bearings for automotive, industrial, medical, and electric motor applications |

| NBI Bearings Europe S.A. | Spain | Ball bearings, roller bearings, and customized bearing solutions for industrial machinery |

| BNL Bearings | Italy | Plastic bearings, bearing assemblies, and custom engineered bearing solutions |

| NSK Ltd. | Japan | Ball bearings, roller bearings, automotive steering systems, and precision machinery |

| NTN Corporation | Japan | Automotive, aerospace, railway, and industrial bearings and precision equipment |

| JTEKT Corporation (Koyo Bearings) | Japan | Ball bearings, roller bearings, steering systems, and drivetrain components |

| MinebeaMitsumi Inc. | Japan | Miniature ball bearings, precision components, motors, and electronic devices |

| Nachi-Fujikoshi Corp. | Japan | Bearings, machine tools, robotics, hydraulic equipment, and industrial automation |

| Oiles Corporation | Japan | Self-lubricating bearings, bushings, and tribological products for industrial applications |

| THK Co., Ltd. | Japan | Linear motion systems, LM guides, ball splines, actuators, and precision bearings |

| Wafangdian Bearing Co., Ltd. (ZWZ Group) | China | Heavy-duty bearings for mining, railways, wind energy, metallurgy, and industrial machinery |

| C&U Group Co., Ltd. | China | Automotive, industrial, precision, and high-speed bearing manufacturing |

| Harbin Bearing Manufacturing Co., Ltd. (HRB) | China | Ball bearings, roller bearings, and industrial bearing solutions |

| Luoyang LYC Bearing Co., Ltd. | China | Large-size, precision, wind power, railway, and heavy-duty industrial bearings |

| National Engineering Industries Ltd. (NBC Bearings) | India | Automotive, railway, aerospace, and industrial bearing manufacturing |

Frequently Asked Questions:

1] What is the growth rate of the Global Bearing Market?

Ans. The Global Bearing Market is growing at a significant rate of 8.71 % during the forecast period.

2] Which region is expected to dominate the Global Bearing Market?

Ans. APAC is expected to dominate the Bearing Market during the forecast period.

3] What was the Global Bearing Market size in 2025?

Ans: The Global Bearing Market size was USD 163.41 Billion in 2025.

4] Which are the top players in the Global Bearing Market?

Ans. The major top players in the Global Bearing Market are Oiles Corporation (Japan), Kashima Bearings and others.

5] What are the factors driving the Global Bearing Market growth?

Ans. The growth of huge construction activities and mining projects is expected to drive the Bearing Market growth.

6] Which country held the largest Global Bearing Market share in 2025?

Ans. The United States held the largest Bearing Market share in 2025.