Aviation Carbon Fiber Market Size by Raw Material, Type, End Use, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2030

Overview

The Aviation Carbon Fiber Market size was valued at USD 1.56 Billion in 2023 and the total Aviation Carbon Fiber Market revenue is expected to grow at a CAGR of 11.5% from 2024 to 2030, reaching nearly USD 3.34 Billion.

Carbon fiber composites have revolutionized the aerospace industry, providing aircraft designers with a strong, lightweight, and durable material that has improved fuel efficiency, extended range, and reduced carbon emissions. These advanced materials offer superior mechanical properties such as high tensile strength, stiffness, and excellent fatigue resistance, making them ideal for critical components such as wings, fuselage, and empennage. However, carbon fiber is also prone to hidden defects and cracks, which can compromise safety and performance if left undetected.

As a result, Non-Destructive Testing (NDT) is an essential tool used throughout the lifecycle of carbon fiber aircraft to ensure their safe and continued operation. The manufacturing process itself also presents a challenge due to the high cost and complexity of producing carbon fiber components, requiring specialized equipment and skilled labour. Despite these challenges, the use of carbon fiber composites in aviation has brought about significant advancements in the industry, enabling the development of modern, fuel-efficient, and environmentally-friendly aircraft.

One unique aspect of the aviation carbon fiber market is the development of new manufacturing techniques that are capable of producing larger and more complex carbon fiber components. For example, a company called Spirit Aero Systems has developed a new process for manufacturing carbon fiber composite fuselages, which allows for the creation of larger and more complex fuselage sections than was previously possible. This new manufacturing technique involves wrapping carbon fiber tape around a mandrel, or mould, in multiple layers. The tape is then infused with resin and cured under high heat and pressure to create a solid composite structure. This process allows for the creation of seamless fuselage sections, reducing the number of joints and fasteners required and increasing structural integrity.

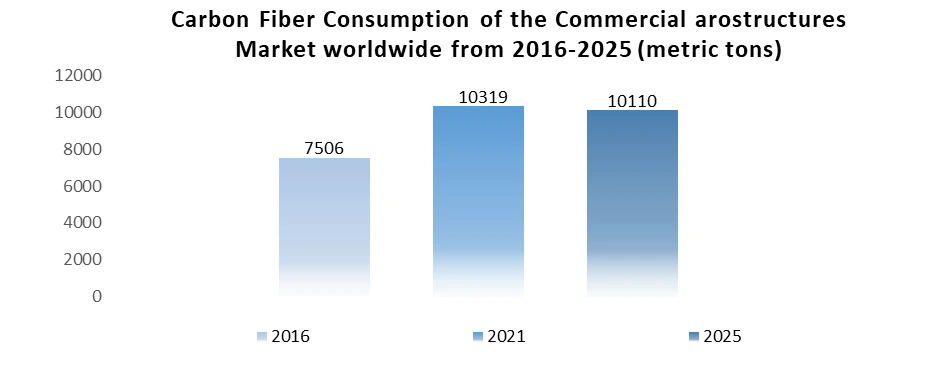

This new process was used in the production of the Boeing 787 Dreamliner, which has a carbon fiber composite fuselage. The Dreamliner is the first commercial aircraft to use a significant amount of carbon fiber composites, and the success of this project has led to increased interest and investment in the aviation carbon fiber market. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Aviation Carbon Fiber Market Dynamics:

Fuel-efficient aircraft penetrate the Aviation Carbon Fiber Market

The increasing demand for fuel-efficient aircraft is one of the most significant drivers of the aviation carbon fiber market. The aviation industry is under increasing pressure to reduce its carbon footprint and improve fuel efficiency, and one of the most effective ways to achieve this is by reducing the weight of aircraft. Carbon fiber is a lightweight material that can significantly reduce the weight of aircraft, which in turn can lead to reduced fuel consumption and emissions.

One unique example of this trend is the Boeing 787 Dreamliner. The Dreamliner is the first commercial aircraft to make extensive use of carbon fiber composites in its structure, including in its wings, fuselage, and other structural components. The use of carbon fiber composites in the Dreamliner helped to reduce the aircraft's weight by up to 20%, compared to traditional aluminium structures. This, in turn, allowed the Dreamliner to achieve fuel savings of up to 20% compared to other aircraft of similar size. The Airbus A350 XWB is another example of an aircraft that makes extensive use of carbon fiber composites. The A350 XWB's wings, fuselage, and other structural components are also made from carbon fiber composites, helping to reduce the aircraft's weight by up to 30%. This translates into fuel savings of up to 25% compared to previous-generation aircraft. The trend towards light weighting in the aviation industry is expected to continue, driven by the need to reduce fuel consumption and emissions.

The Airbus A350 XWB is another example of an aircraft that makes extensive use of carbon fiber composites. The A350 XWB's wings, fuselage, and other structural components are also made from carbon fiber composites, helping to reduce the aircraft's weight by up to 30%. This translates into fuel savings of up to 25% compared to previous-generation aircraft. The trend towards light weighting in the aviation industry is expected to continue, driven by the need to reduce fuel consumption and emissions.

According to a report by Aerospace Manufacturing and Design, the use of carbon fiber composites in commercial aircraft is expected to increase by 10% by 2023, compared to 2019 levels. This trend is expected to continue as aircraft manufacturers look for new and innovative ways to reduce weight and improve fuel efficiency, which will likely drive continued growth in the aviation carbon fiber market.

New Carbon Fiber Materials Revolutionize Aviation Manufacturing, Creating Opportunities for Manufacturers

The development of new carbon fiber materials in aviation creates significant opportunities for manufacturers in the Aviation Carbon Fiber Industry. Carbon fiber is a lightweight material that has been increasingly used in the aviation industry to reduce weight, increase fuel efficiency, and reduce emissions. However, traditional carbon fiber materials have limitations in terms of cost and production processes, which have hindered their widespread adoption. One of the most promising new developments in carbon fiber materials is the use of nanotubes to reinforce carbon fiber.

Nanotube-based carbon fiber is much stronger than traditional carbon fiber and can be produced at a lower cost. This opens up new possibilities for the use of carbon fiber in aviation, as it could make it more cost-effective to produce lightweight aircraft components and drive the Aviation Carbon Fiber Market. Another area of development is in the creation of recyclable carbon fiber materials. Traditional carbon fiber is difficult to recycle and is often sent to landfills or incinerated, which can lead to environmental concerns. Recyclable carbon fiber materials would help to reduce waste and lower the environmental impact of aviation. This could be particularly important in the context of growing concern about the sustainability of aviation in the Aviation Carbon Fiber Market.

The development of new carbon fiber materials is also leading to the creation of new production methods. For example, some manufacturers are exploring the use of 3D printing to produce complex carbon fiber components. This could significantly reduce production time and costs, while also allowing for more intricate designs. An example of the development of new carbon fiber materials is the partnership between Boeing and MIT to develop a new type of carbon fiber material. The material, known as "nano-reinforced resin," is made by combining carbon nanotubes with traditional carbon fiber. The resulting material is stronger and more durable than traditional carbon fiber, and can be produced at a lower cost. This opens up new possibilities for the use of carbon fiber in aviation, as it could make it more cost-effective to produce lightweight aircraft components.

Aviation Carbon Fiber Market Segment Analysis:

By Raw Material: the Aviation Carbon Fiber Market is segmented into PAN-based Carbon Fiber and Pitch-based Carbon Fiber. PAN-based Carbon Fiber is expected to dominate the Aviation Carbon Fiber Market during the forecast period. PAN-based carbon fiber is a type of carbon fiber that is made using polyacrylonitrile (PAN) precursor material. It is known for its high strength, stiffness, and durability, which make it ideal for use in various applications, including the Aviation Carbon Fiber Market.

For example the use of PAN-based carbon fiber in the aviation industry is in the manufacturing of aircraft parts such as wings, fuselage, and tail sections. For instance, the Airbus A350 XWB uses over 50% composite materials, including PAN-based carbon fiber, in its structure, making it lighter and more fuel-efficient than traditional aluminium aircraft. Another example is the Boeing 787 Dreamliner, which also extensively uses PAN-based carbon fiber in its construction. The Dreamliner's fuselage is made up of 50% composite materials, with the majority of it being PAN-based carbon fiber.

PAN-based carbon fiber is also used in other industries such as automotive, sports, and wind energy, due to its excellent mechanical properties and low weight. Aviation Carbon Fiber Market demand is expected to continue growing in the future as more industries adopt carbon fiber materials to improve their products' performance and reduce their environmental impact.

Aviation Carbon Fiber Market Regional Insights:

Asia Pacific held the largest Aviation Carbon Fiber Market share in 2023. The aviation carbon fiber market in the Asia Pacific region is experiencing significant growth due to the region's expanding aviation industry, increasing demand for fuel-efficient aircraft, and the emergence of low-cost carriers. The Asia Pacific region is the fastest-growing Aviation Carbon Fiber Market in the world, with a growing middle class, increasing tourism, and expanding economies driving air travel demand.

According to the International Air Transport Association (IATA), the Asia Pacific region accounted for 39% of global air traffic in 2019, and this is expected to continue growing in the coming years. The aviation industry in the Asia Pacific region is also placing a significant emphasis on fuel efficiency, given the region's high fuel prices and environmental concerns. Carbon fiber composites offer significant weight savings, resulting in more fuel-efficient aircraft. For example, the Airbus A320neo, a popular narrow-body aircraft in the region, features 25% composite materials, including carbon fiber, resulting in 20% fuel savings compared to previous models.

The Asia Pacific region has seen an increase in a local production of carbon fiber and carbon fiber composites, reducing dependence on imports and driving down costs. For example, Japan-based Toray Industries is one of the world's leading producers of carbon fiber and has expanded its production capacity in the region. The Chinese government has also made significant investments in developing its domestic carbon fiber industry, with local companies such as Hengshen Co. and Weihai Guangwei Composites Co. producing carbon fiber composites for aircraft, which penetrate the Aviation Carbon Fiber Market growth globally.

Global Aviation Carbon Fiber Market Scope: Inquire before buying

| Global Aviation Carbon Fiber Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024 - 2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | USD 1.56 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 11.5% | Market Size in 2030: | USD 3.34 Bn. |

| Segments Covered: | by Raw Material | PAN-based Carbon Fiber Pitch-based Carbon Fiber |

|

| by Type | Continuous Long Short |

||

| by End Use | Commercial Military Other |

||

Aviation Carbon Fiber Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Aviation Carbon Fiber Market Key Players:

1. Toray Industries Inc. - Japan

2. Teijin Limited - Japan

3. SGL Carbon SE - Germany

4. Hexcel Corporation - United States

5. Mitsubishi Chemical Holdings Corporation - Japan

6. Solvay S.A. - Belgium

7. Royal DSM N.V. - Netherlands

8. Gurit Holding AG - Switzerland

9. Axiom Materials, Inc. - United States

10.Park Aerospace Corp. - United States

11.Composite Resources - United States

12.Formax UK Limited - United Kingdom

13.Advanced Composites Group Ltd. - United Kingdom

14.Hyosung Advanced Materials Corporation - South Korea

15.Toho Tenax Co., Ltd. - Japan

16.Zoltek Companies Inc. - United States

17.Hexion Inc. - United States

18.Plasan Carbon Composites - United States

19.Cristex Ltd. - United Kingdom

20.TenCate Advanced Composites - Netherlands

FAQs:

1. What are the growth drivers for the Aviation Carbon Fiber Market?

Ans. The increasing prevalence of lightweight material is expected to be the major driver for the Aviation Carbon Fiber Market.

2. What is the major restraint for the Aviation Carbon Fiber Market growth?

Ans. Stringent government regulations are expected to be the major restraining factor for the Aviation Carbon Fiber Market growth.

3. Which region is expected to lead the global Aviation Carbon Fiber Market during the forecast period?

Ans. Asia Pacific is expected to lead the global Aviation Carbon Fiber Market during the forecast period.

4. What is the projected market size & growth rate of the Aviation Carbon Fiber Market?

Ans. The Aviation Carbon Fiber Market size was valued at USD 1.56 Billion in 2023 and the total Aviation Carbon Fiber Market revenue is expected to grow at a CAGR of 11.5% from 2024 to 2030, reaching nearly USD 3.34 Billion.

5. What segments are covered in the Aviation Carbon Fiber Market report?

Ans. The segments covered in the Market report are Type, Applications, End-use, and Region.